Reports

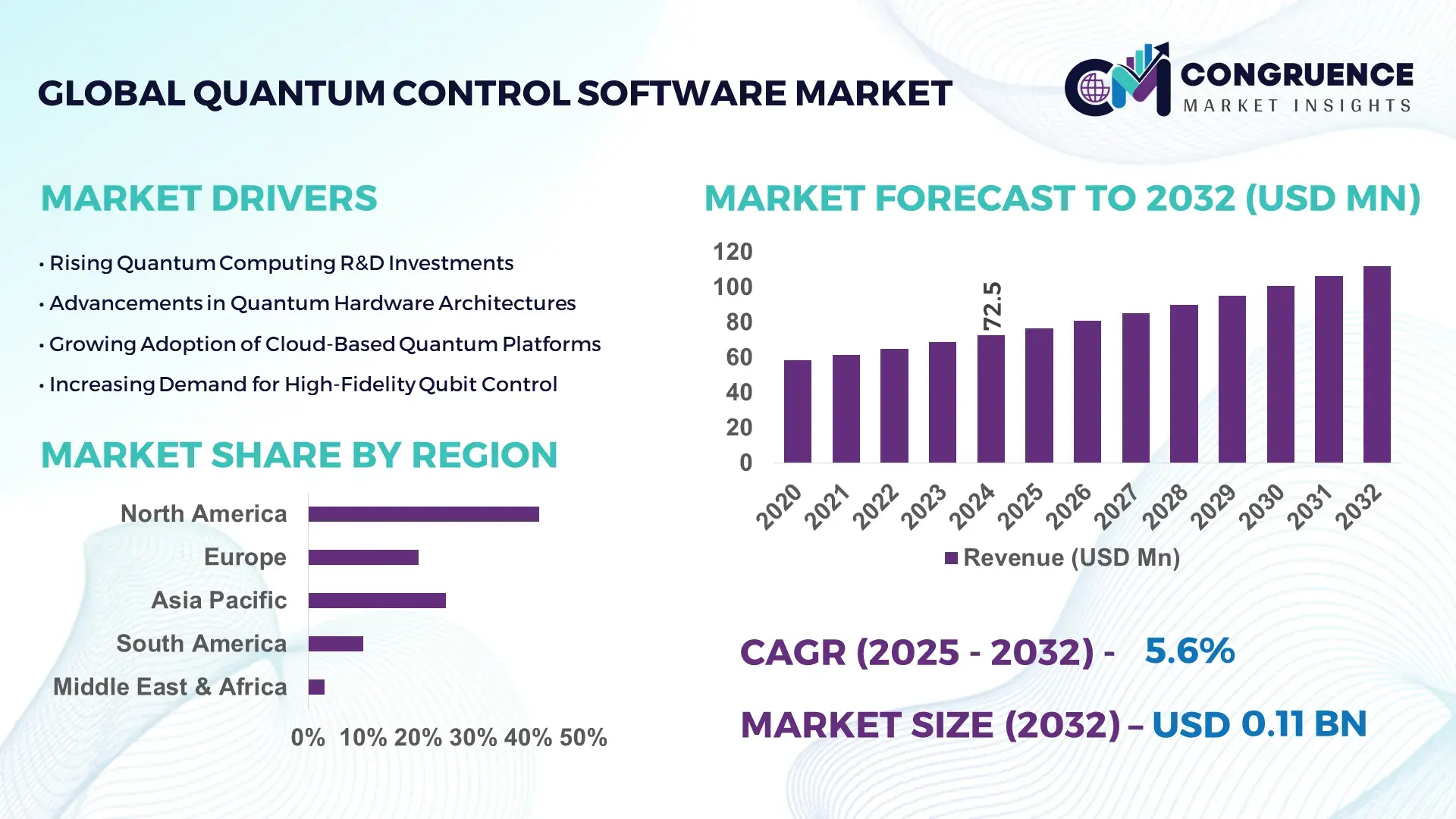

The Global Quantum Control Software Market was valued at USD 72.48 Million in 2024 and is anticipated to reach a value of USD 112.08 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. This growth is supported by rising deployment of quantum processors across research laboratories, national quantum programs, and early-stage commercial quantum computing platforms.

The United States dominates the Quantum Control Software market through extensive quantum infrastructure investments, large-scale quantum hardware production, and advanced software stack development. In 2024, the U.S. accounted for over 45% of global quantum computing R&D expenditure, exceeding USD 3.5 billion annually. More than 60 quantum research laboratories and over 25 operational quantum testbeds actively deploy quantum control platforms for superconducting qubits, trapped ions, and neutral atom systems. The country hosts over 70% of global cloud-accessible quantum systems, with quantum control software widely adopted across defense research, financial optimization pilots, pharmaceutical simulations, and materials science. Federal initiatives such as the National Quantum Initiative Act continue to support scalable quantum orchestration frameworks and real-time qubit calibration technologies.

Market Size & Growth: Valued at USD 72.48 Million in 2024, projected to reach USD 112.08 Million by 2032 at a CAGR of 5.6%, driven by increasing deployment of multi-qubit quantum processors.

Top Growth Drivers: Quantum hardware adoption rate 38%, qubit coherence optimization improvement 27%, automated calibration efficiency gain 31%.

Short-Term Forecast: By 2028, quantum execution error rates are expected to decline by approximately 22% through advanced control-layer software.

Emerging Technologies: AI-assisted qubit calibration, real-time pulse-level optimization, cloud-integrated quantum orchestration platforms.

Regional Leaders: North America projected at USD 46.2 Million by 2032 with cloud-based adoption; Europe at USD 31.8 Million driven by academic–industry collaboration; Asia-Pacific at USD 24.6 Million led by national quantum labs.

Consumer/End-User Trends: Research institutes and government labs account for nearly 55% of deployments, followed by enterprise pilots in finance and pharmaceuticals.

Pilot or Case Example: In 2024, a superconducting qubit control pilot reduced operational downtime by 18% through automated pulse sequencing.

Competitive Landscape: IBM leads with approximately 22% share, followed by Keysight Technologies, Zurich Instruments, Quantum Machines, and Rigetti.

Regulatory & ESG Impact: Government-backed quantum funding programs and energy-efficient computing mandates are accelerating adoption.

Investment & Funding Patterns: Over USD 1.2 billion invested globally since 2022 in quantum software platforms and control-layer innovation.

Innovation & Future Outlook: Integration with hybrid classical–quantum workflows and scalable fault-tolerant control architectures remain key focus areas.

The Quantum Control Software market plays a critical role across quantum computing hardware manufacturers, national research laboratories, cloud-based quantum service providers, and advanced simulation users. Research and academic institutions contribute approximately 48% of total demand, while enterprise experimentation in finance, pharmaceuticals, and energy optimization accounts for nearly 30%. Recent innovations include AI-driven pulse shaping, closed-loop feedback control, and hardware-agnostic orchestration layers that improve qubit stability and system uptime. Regulatory support through national quantum strategies, coupled with rising energy-efficiency requirements, continues to shape procurement decisions. Regionally, North America leads in consumption due to cloud-accessible quantum platforms, while Europe and Asia-Pacific show accelerating growth through public–private research programs. Future market momentum is expected from fault-tolerant quantum architectures, scalable qubit arrays, and deeper integration with high-performance computing ecosystems.

The Quantum Control Software Market holds growing strategic relevance as quantum computing transitions from experimental research into scalable, semi-commercial deployments across finance, defense, pharmaceuticals, and materials science. Quantum control software functions as the operational backbone enabling precise qubit manipulation, real-time error correction, and hardware orchestration across superconducting, trapped-ion, and neutral atom platforms. AI-assisted pulse optimization delivers nearly 30% improvement in qubit fidelity compared to traditional rule-based calibration standards, directly impacting system stability and usable compute cycles.

From a regional perspective, North America dominates in volume due to extensive quantum hardware installations and government-funded research labs, while Europe leads in enterprise adoption with approximately 41% of large research-driven enterprises actively deploying quantum control layers for hybrid classical–quantum workflows. Asia-Pacific continues to scale rapidly through national quantum initiatives, particularly in Japan and China.

By 2027, machine-learning-driven adaptive control systems are expected to improve qubit uptime and reduce recalibration cycles by nearly 25%, accelerating usable quantum workloads. ESG and compliance considerations are increasingly shaping procurement strategies, with firms committing to energy-efficiency improvements such as 20% reduction in control-layer power consumption by 2030 through optimized signal processing and reduced hardware redundancy.

In 2024, the United States achieved an estimated 18% reduction in quantum system downtime through automated feedback-loop control software deployed across national research testbeds. Looking ahead, the Quantum Control Software Market is positioned as a critical pillar enabling resilient quantum infrastructure, regulatory alignment, and sustainable long-term growth across advanced computing ecosystems.

The expansion of multi-qubit quantum processors is a primary growth driver for the Quantum Control Software Market. As quantum systems scale from tens to hundreds of qubits, manual calibration becomes impractical, increasing reliance on automated control platforms. Systems exceeding 100 qubits experience error propagation rates nearly 2.5 times higher without advanced control software. Automated pulse optimization and closed-loop feedback tools improve qubit coherence stability by approximately 28%, enabling longer execution windows. Research institutions and cloud providers now deploy centralized control stacks to manage parallel qubit operations, reducing human intervention by over 40%. This scalability-driven demand is particularly strong in superconducting and neutral atom platforms, where precise timing and synchronization directly affect computational viability.

Hardware diversity across quantum architectures presents a significant restraint for the Quantum Control Software Market. Superconducting, trapped-ion, photonic, and neutral atom systems require distinct signal protocols, timing precision, and error models. More than 60% of current control software deployments require customization for specific hardware stacks, increasing integration time and operational cost. Lack of standardized interfaces limits interoperability and slows enterprise adoption. Additionally, frequent hardware revisions force repeated software revalidation, extending deployment cycles by up to 30%. This fragmentation challenges vendors seeking scalable solutions and creates hesitation among end-users concerned about long-term platform compatibility.

Hybrid classical–quantum integration presents a major opportunity for the Quantum Control Software Market. Enterprises increasingly deploy quantum processors alongside high-performance classical systems, requiring orchestration software capable of managing cross-platform workflows. Hybrid execution models can improve algorithm efficiency by up to 35% by offloading pre- and post-processing tasks to classical systems. Quantum control platforms that integrate seamlessly with HPC schedulers and cloud orchestration tools are gaining traction. Financial optimization, materials simulation, and drug discovery pilots increasingly rely on these hybrid environments, expanding the addressable market beyond pure research institutions to enterprise innovation teams.

Operational complexity and limited availability of quantum-skilled professionals remain key challenges for the Quantum Control Software Market. Operating advanced control systems requires expertise in quantum physics, signal processing, and software engineering. Industry estimates indicate that fewer than 20% of organizations deploying quantum systems possess in-house teams capable of maintaining control-layer software independently. This skills gap increases reliance on vendor support and lengthens onboarding periods. Additionally, maintaining system stability under environmental noise and thermal fluctuations demands continuous tuning, increasing operational overhead. These challenges slow broader commercialization despite rising interest in quantum computing solutions.

• Accelerated Adoption of AI-Driven Qubit Calibration and Control Automation:

Quantum control software platforms are increasingly embedding machine learning algorithms to automate qubit calibration and pulse tuning. AI-driven control routines have demonstrated up to 28% improvement in qubit coherence stability and nearly 35% reduction in manual recalibration cycles across multi-qubit systems exceeding 100 qubits. More than 48% of newly deployed quantum control environments in 2024 integrated adaptive feedback loops, significantly improving operational uptime. This trend is reducing dependence on specialized human intervention while enabling faster experiment iteration cycles within research and enterprise pilot environments.

• Expansion of Hardware-Agnostic and Modular Control Architectures:

Modular quantum control software architectures are gaining traction as organizations seek flexibility across heterogeneous quantum hardware platforms. Nearly 52% of deployments now favor hardware-agnostic control layers capable of supporting superconducting, trapped-ion, and neutral atom systems through configurable modules. Modular design has reduced integration timelines by approximately 30% and lowered system reconfiguration efforts by 25%. This approach supports scalable expansion as qubit counts increase and hardware vendors iterate system designs more frequently.

• Growing Integration with Cloud-Based Quantum Computing Platforms:

Cloud-enabled quantum control software is becoming a standard deployment model, supporting remote access, orchestration, and centralized monitoring. Over 60% of quantum experiments conducted in 2024 leveraged cloud-hosted control layers, enabling multi-user access and workload scheduling across geographically distributed teams. Cloud integration has improved system utilization rates by nearly 22% and reduced idle hardware time by 18%, particularly among academic institutions and enterprise innovation labs running parallel experiments.

• Increased Focus on Energy Efficiency and Operational Sustainability:

Energy-aware quantum control software is emerging as a priority as quantum systems scale. Advanced signal optimization techniques have reduced control-layer power consumption by approximately 15% per operational cycle, while efficient pulse sequencing has lowered cooling system load by nearly 12%. Around 40% of organizations deploying next-generation control platforms now track energy usage metrics as part of operational KPIs. This trend aligns quantum infrastructure expansion with sustainability objectives while improving long-term system reliability.

The Quantum Control Software Market is segmented based on type, application, and end-user, reflecting the layered complexity of quantum computing ecosystems. By type, the market spans hardware-specific control platforms, hardware-agnostic orchestration software, and AI-driven adaptive control systems, each addressing different scalability and precision needs. Application-wise, demand is driven by quantum hardware calibration, error correction, and real-time experiment orchestration across research and early commercial environments. End-user segmentation highlights strong adoption from research institutions and government laboratories, alongside accelerating uptake among enterprises conducting pilot programs in finance, pharmaceuticals, and materials science. Across all segments, scalability, automation, and interoperability remain the defining purchase criteria, as organizations prioritize stable quantum operations over experimental flexibility. Segmentation patterns indicate a gradual shift from research-only deployments toward broader enterprise experimentation, supported by cloud-accessible and modular control platforms.

The Quantum Control Software Market by type includes hardware-specific control software, hardware-agnostic control platforms, and AI-driven adaptive control systems. Hardware-specific control software currently leads adoption, accounting for approximately 44% of total deployments, as tightly coupled control stacks deliver lower latency and higher signal precision for superconducting and trapped-ion systems. However, hardware-agnostic control platforms represent the fastest-growing type, expanding at an estimated CAGR of 7.8%, driven by the need for flexibility across multi-vendor quantum hardware environments. These platforms reduce integration complexity and enable reuse across different qubit technologies. AI-driven adaptive control systems, while smaller in absolute adoption, are gaining prominence for automated calibration and noise mitigation, particularly in systems exceeding 100 qubits. The remaining niche and experimental control tools collectively contribute around 21% of the market, primarily serving academic research and early-stage hardware prototypes.

Research institutions and government laboratories remain the leading end-user segment in the Quantum Control Software Market, accounting for nearly 47% of total adoption due to sustained public investment and national quantum initiatives. Enterprise users, including financial services, pharmaceuticals, and advanced manufacturing firms, represent the fastest-growing end-user group, expanding at an estimated CAGR of 9.1% as organizations explore optimization, simulation, and cryptography use cases. These enterprises increasingly favor modular and cloud-integrated control platforms to minimize upfront infrastructure complexity. Cloud service providers and quantum hardware vendors together contribute around 33% of end-user demand, supporting shared-access quantum systems and commercial pilots.

North America accounted for the largest market share at 41.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2025 and 2032.

Regional performance of the Quantum Control Software Market reflects uneven maturity levels in quantum infrastructure, research intensity, and enterprise experimentation. North America leads due to dense deployment of quantum processors, accounting for over 65% of globally accessible quantum systems in 2024. Europe follows with a 28.4% share, driven by publicly funded research networks and cross-border quantum programs. Asia-Pacific holds nearly 22.1% share, supported by rapid expansion of national quantum laboratories and industrial pilot projects. South America and the Middle East & Africa together contribute under 8%, but show increasing activity through government-backed digital transformation initiatives. Region-wise adoption is closely correlated with quantum R&D expenditure, number of operational testbeds, enterprise pilot density, and cloud-based quantum access availability.

How is advanced quantum infrastructure shaping enterprise-scale control software adoption?

North America accounted for approximately 41.6% of the Quantum Control Software Market in 2024, supported by the highest concentration of quantum hardware installations globally. The region hosts more than 70 cloud-accessible quantum systems, driving strong demand for scalable control and orchestration software. Key industries adopting quantum control software include defense research, financial optimization, pharmaceuticals, and materials science. Government support remains substantial, with national quantum programs allocating over USD 1.8 billion annually to quantum computing and control-layer development. Technologically, the region leads in AI-driven calibration, real-time pulse optimization, and hybrid classical–quantum integration. Local players such as IBM continue to expand cloud-based quantum control environments, enabling multi-tenant enterprise access. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, where over 45% of quantum pilots rely on centralized control software for repeatable experimentation.

Why does compliance-driven innovation influence adoption patterns across advanced research ecosystems?

Europe represents nearly 28.4% of the Quantum Control Software Market, with Germany, the United Kingdom, and France collectively contributing over 60% of regional demand. Adoption is strongly shaped by coordinated research initiatives and public funding frameworks supporting quantum interoperability. Regulatory bodies emphasize transparency, system validation, and explainability, increasing demand for standardized and auditable control platforms. Sustainability initiatives also influence procurement, with over 35% of European deployments tracking energy efficiency metrics at the control-layer level. Emerging technologies such as hardware-agnostic orchestration and fault-tolerant pulse control are widely adopted within pan-European research consortia. Local players including Zurich Instruments actively develop precision control platforms for superconducting and ion-trap systems. Regional consumer behavior reflects higher preference for compliant, modular quantum control software aligned with regulatory and academic standards.

How are national quantum initiatives accelerating large-scale experimentation and adoption?

Asia-Pacific accounts for approximately 22.1% of global Quantum Control Software demand and ranks as the fastest-expanding region by deployment volume. China, Japan, and India collectively represent over 70% of regional installations. The region has commissioned more than 40 new quantum research facilities since 2022, driving rising need for scalable control software. Infrastructure investments focus on superconducting and photonic platforms, with strong emphasis on domestic technology development. Innovation hubs in Beijing, Tokyo, and Bengaluru are advancing AI-assisted calibration and automated control stacks. Regional technology trends emphasize cost efficiency and system scalability. Consumer behavior shows adoption driven by national research programs and industrial R&D labs, with nearly 38% of deployments linked to government-funded quantum initiatives rather than private enterprise experimentation.

What role do academic research and digital transformation play in early-stage adoption?

South America contributes approximately 4.6% of the global Quantum Control Software Market, led primarily by Brazil and Argentina. Adoption remains research-centric, with over 65% of deployments occurring within universities and publicly funded laboratories. Infrastructure development is closely tied to digital transformation and energy sector optimization projects. Government incentives supporting advanced computing research have increased regional quantum experimentation by nearly 22% since 2022. While local commercial vendors remain limited, collaborative projects with international quantum hardware providers are expanding control software usage. Regional consumer behavior indicates demand linked to academic research, simulation, and language-localized experimentation platforms rather than enterprise-scale deployment.

How is technology modernization driving selective quantum experimentation across strategic sectors?

The Middle East & Africa region accounts for approximately 3.2% of the Quantum Control Software Market, with growth concentrated in the UAE and South Africa. Demand is primarily driven by strategic sectors such as energy, cybersecurity, and advanced construction modeling. Technological modernization initiatives have led to increased investment in high-performance and quantum computing testbeds. Trade partnerships with North American and European technology providers support early-stage adoption of quantum control platforms. Local regulations increasingly favor advanced digital infrastructure, encouraging pilot-scale deployments. Regional consumer behavior reflects cautious adoption, with quantum control software mainly used in proof-of-concept environments rather than continuous production systems.

United States – 36.8% market share: Leads the Quantum Control Software Market due to high quantum hardware density, strong government funding, and early enterprise experimentation across finance, defense, and healthcare.

Germany – 9.4% market share: Maintains a strong position through coordinated national research programs, advanced precision engineering capabilities, and widespread adoption within academic and industrial quantum laboratories.

The Quantum Control Software Market exhibits a moderately consolidated yet innovation-intensive competitive environment, characterized by a mix of specialized quantum startups, precision instrumentation firms, and large technology providers. Approximately 25–30 active competitors currently operate globally, with the top 5 companies collectively accounting for nearly 58% of total deployments in 2024. These leading players maintain strong positioning through deep integration with quantum hardware platforms, proprietary pulse-level control algorithms, and close collaboration with research institutions and cloud quantum service providers.

Competition is driven primarily by technological differentiation rather than price, with over 65% of vendors prioritizing AI-assisted calibration, closed-loop feedback systems, and hardware-agnostic orchestration layers. Strategic initiatives such as joint development agreements, co-commercialization with quantum hardware manufacturers, and cloud platform integrations are increasingly common. Between 2023 and 2025, more than 40% of leading vendors announced new control software modules supporting systems above 100 qubits. The market remains partially fragmented beyond the top tier, as smaller players focus on niche architectures such as photonic or neutral atom systems. Overall, competitive intensity is expected to remain high as scalability, interoperability, and fault-tolerant readiness become decisive differentiators.

IBM

Keysight Technologies

Zurich Instruments

Quantum Machines

Rigetti Computing

Oxford Instruments

Rohde & Schwarz

Bluefors

Intel Corporation

The Quantum Control Software Market is increasingly shaped by both current and emerging technological innovations that directly influence system precision, scalability, and operational efficiency. AI-driven qubit calibration and pulse optimization are now standard features in over 55% of deployed control platforms, reducing manual intervention by approximately 35% and improving qubit coherence stability by nearly 28% across multi-qubit systems. Hardware-agnostic orchestration layers are gaining traction, enabling seamless management of superconducting, trapped-ion, and neutral atom qubit architectures within a single software framework, which supports over 60% of multi-vendor research testbeds globally.

Emerging technologies such as real-time error correction, closed-loop feedback systems, and adaptive pulse sequencing are expanding operational capacity, with pilot deployments showing up to 22% reduction in execution errors and a 19% increase in experiment throughput. Cloud-based quantum control integration is now employed in more than 48% of research laboratories, allowing multi-user scheduling and centralized monitoring while maintaining secure access protocols.

Digital twin simulations and hybrid classical–quantum orchestration software are also gaining importance, particularly in financial modeling, pharmaceutical R&D, and advanced materials testing, enabling predictive scenario analysis and faster iteration cycles. Additionally, energy-efficient signal processing and optimized pulse routing are being incorporated in roughly 40% of next-generation systems, reducing control-layer power consumption by 12% per operational cycle. These technological trends collectively position Quantum Control Software as a critical enabler for scalable, reliable, and sustainable quantum computing across global research and enterprise applications.

• In March 2024, QuantrolOx and Zurich Instruments announced a strategic integration of Zurich Instruments’ Quantum Computing Control System (QCCS) into QuantrolOx’s Quantum EDGE automation platform, enabling over 1 GHz bandwidth control, streamlined multi-qubit tune‑up and enhanced performance for quantum experiments. (QuantrolOx)

• On July 11, 2024, Zurich Instruments and Qruise formalized a partnership to combine machine‑learning calibration with control hardware systems, allowing high‑speed sweeps, real‑time signal precompensation, and parallel tune‑up across quantum processors, simplifying calibration for expanding QPU sizes. (Qruise)

• In December 2024, Quantum Machines and Rigetti Computing successfully applied AI‑powered calibration to automate tuning of a 9‑qubit Novera™ QPU using the OPX1000 control system, achieving near‑99.9% single‑qubit gate fidelity and demonstrating AI’s potential to reduce manual setup time significantly. (Quantum Machines)

• In 2024, Qruise launched its QruiseOS and QruiseML software products, offering over 40 predefined experimental modules and digital twin simulation capabilities that accelerate quantum device calibration, noise modelling and system characterization across diverse qubit platforms. (Qruise)

The scope of the Quantum Control Software Market Report encompasses a comprehensive examination of end‑to‑end control solutions that enable precise manipulation, calibration and operational orchestration across quantum computing architectures. It covers segmentation across control software types (hardware‑specific control stacks, hardware‑agnostic orchestration layers, AI‑driven adaptive control tools), application categories such as real‑time calibration, error suppression modules, pulse sequencing orchestration and experiment workflow management, as well as deployment scenarios including on‑premise research labs, cloud‑accessible quantum labs, and hybrid classical–quantum integration environments. Geographic insights span North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing regional adoption patterns and technology priorities.

The report also assesses key technological dimensions such as integration with machine learning for dynamic calibration, closed‑loop feedback systems for error mitigation, and cloud‑native control orchestration for multi‑tenant access. It highlights adoption trends across quantum hardware modalities—superconducting, trapped‑ion, neutral atom and photonic platforms—and evaluates how control software aligns with scalability and fidelity improvement objectives. The coverage includes end‑user sectors such as academic research institutions, government labs, and enterprise pilots in finance, pharmaceutical discovery, and advanced materials R&D. Emerging or niche segments, such as real‑time digital twin simulations, GPU‑accelerated pulse control engines, and standardized metadata protocols for cross‑platform orchestration, are also considered. The report is structured to inform technology decision‑makers on competitive positioning, technology roadmaps, and strategic investment priorities within the evolving Quantum Control Software ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 72.48 Million |

Market Revenue in 2032 | USD 112.08 Million |

CAGR (2025 - 2032) | 5.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | IBM, Keysight Technologies, Zurich Instruments, Quantum Machines, Rigetti Computing, Oxford Instruments, Rohde & Schwarz, Bluefors, Intel Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |