Reports

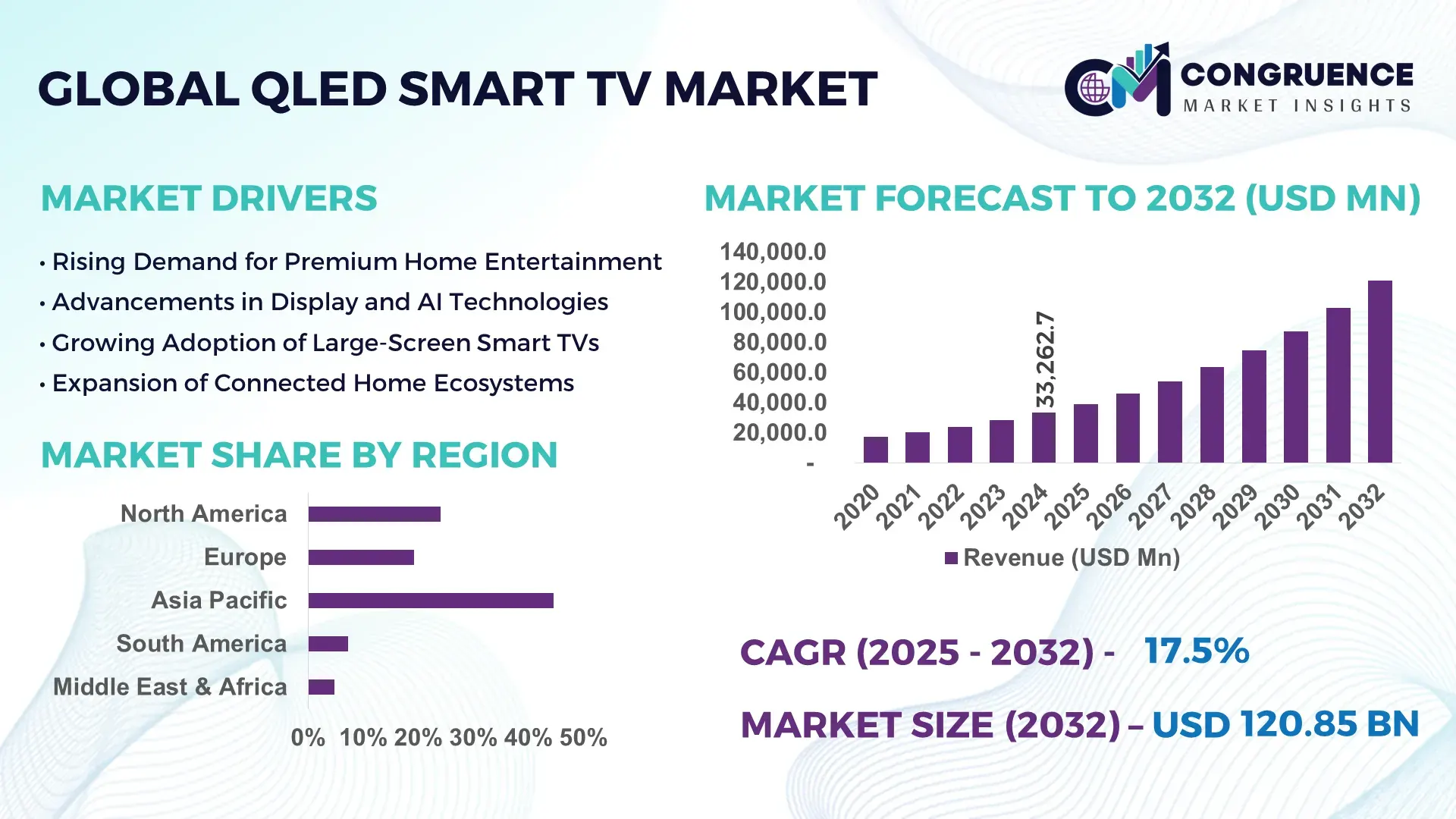

The Global QLED Smart TV Market was valued at USD 33,262.7 Million in 2024 and is anticipated to reach a value of USD 120,853.8 Million by 2032 expanding at a CAGR of 17.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is supported by rapid premium TV replacement cycles and accelerated consumer shift toward high-brightness, color-accurate display technologies.

China represents the most influential production and innovation hub in the QLED Smart TV Market, supported by an annual television manufacturing capacity exceeding 180 million units across integrated display and semiconductor clusters. Over USD 12 billion has been invested in advanced display fabs and quantum-dot material development. Chinese OEMs deploy QLED technology across residential, commercial signage, hospitality, and education applications. More than 68% of urban households now own smart TVs above 55 inches, while domestic brands integrate AI upscaling, Mini-LED backlighting, and low-power display architectures at scale.

Market Size & Growth: Valued at USD 33.26 billion in 2024, projected to reach USD 120.85 billion by 2032, growing at a CAGR of 17.5%, driven by premium display upgrades and smart home convergence.

Top Growth Drivers: Larger screen adoption (+42%), AI-powered image processing (+36%), and Mini-LED backlight penetration (+31%).

Short-Term Forecast: By 2028, average panel energy efficiency is expected to improve by 22% through optimized quantum-dot layers.

Emerging Technologies: Mini-LED backlighting, AI-based upscaling engines, and low-cadmium quantum-dot films.

Regional Leaders: Asia Pacific (USD 46.2 billion by 2032, high-volume manufacturing), North America (USD 31.8 billion, premium adoption), Europe (USD 24.5 billion, energy-efficient upgrades).

Consumer/End-User Trends: Over 61% of buyers prefer 55–75 inch QLED models for OTT streaming and gaming use.

Pilot or Case Example: In 2023, a South Korean OEM pilot reduced power consumption by 18% using AI brightness optimization.

Competitive Landscape: Samsung Electronics (~29% share), followed by TCL, Hisense, LG Electronics, and Sony.

Regulatory & ESG Impact: Energy labeling mandates in the EU push ≥20% efficiency gains in new models.

Investment & Funding Patterns: Over USD 18 billion invested globally in display fabs and smart TV SoC development since 2022.

Innovation & Future Outlook: Integration of smart assistants, cloud gaming, and adaptive picture algorithms is reshaping product differentiation.

The QLED Smart TV Market spans residential entertainment, commercial digital signage, hospitality, and education, with residential use contributing nearly 64% of total demand. Innovations in Mini-LED backlighting, AI upscaling, and low-power quantum-dot films are accelerating product refresh cycles. Regulatory energy standards, rising disposable income, Asia-led consumption growth, and convergence with smart home ecosystems are shaping future market trajectories.

The QLED Smart TV Market holds strong strategic relevance as a convergence point between advanced display engineering, consumer electronics, and digital content ecosystems. Manufacturers increasingly position QLED as a scalable premium alternative to OLED, balancing cost efficiency with high brightness and long panel lifespan. Mini-LED QLED displays deliver nearly 40% brightness improvement compared to conventional LED-backlit LCD standards, enhancing HDR performance for gaming and streaming applications.

From a regional standpoint, Asia Pacific dominates production volumes due to vertically integrated supply chains, while North America leads in premium adoption, with over 58% of households using smart TVs larger than 55 inches. Europe shows accelerated replacement demand driven by energy efficiency compliance and eco-design directives. By 2027, AI-based image optimization is expected to reduce power consumption per viewing hour by 25%, improving total cost of ownership for consumers.

ESG considerations are becoming central to strategy, with manufacturers committing to 30–40% recycled plastic content in TV casings by 2030 and phasing out cadmium-based quantum dots. In 2024, South Korea achieved a 21% reduction in panel defect rates through AI-driven quality inspection systems. Looking ahead, the QLED Smart TV Market is positioned as a pillar of resilient consumer electronics growth, enabling sustainable manufacturing, regulatory compliance, and long-term digital lifestyle integration.

The QLED Smart TV Market dynamics are shaped by rapid technological evolution, premiumization of consumer electronics, and shifting content consumption patterns. Demand is increasingly driven by large-screen formats, with models above 55 inches accounting for over half of new installations. Advancements in Mini-LED backlighting, AI processors, and quantum-dot materials are enhancing picture quality while reducing energy intensity. The market is also influenced by platform-level competition, where smart operating systems, gaming optimization, and voice assistant integration act as differentiation levers. Supply-side dynamics reflect strong investments in panel fabs and semiconductor localization, while demand-side trends are tied to OTT penetration, esports growth, and smart home adoption across urban households.

The shift toward immersive home entertainment experiences is a primary growth driver for the QLED Smart TV Market. More than 72% of global streaming subscribers now consume 4K or HDR-enabled content, directly increasing demand for high-brightness and wide color gamut displays. Gaming adoption has further intensified this trend, with QLED TVs supporting refresh rates above 120 Hz and latency reductions of nearly 35%. Urban households increasingly replace traditional TVs every 4–5 years, driven by screen size upgrades and smart functionality. This behavioral shift sustains high-volume demand for advanced QLED panels across both developed and emerging markets.

High component and manufacturing costs remain a restraint for the QLED Smart TV Market, particularly for entry-level adoption. Mini-LED backlights require thousands of precision-controlled diodes, increasing bill-of-materials costs by 18–25% compared to conventional LED TVs. Advanced quantum-dot films and AI chipsets further elevate production complexity. Supply volatility in semiconductor wafers and specialty chemicals has led to longer lead times and pricing pressure. In price-sensitive regions, these factors slow penetration beyond mid-to-premium consumer segments despite strong aspirational demand.

Smart home convergence presents a significant opportunity for the QLED Smart TV Market. Over 45% of smart TV buyers now use their TVs as centralized control hubs for IoT devices, security systems, and voice assistants. Integration with cloud gaming, fitness platforms, and smart appliances expands functional value beyond entertainment. Emerging markets are adopting bundled ecosystems where QLED TVs are sold alongside smart speakers and routers, increasing average device utilization. This ecosystem-led positioning creates opportunities for recurring software upgrades and service-based monetization.

Sustainability and regulatory compliance pose growing challenges for the QLED Smart TV Market. Energy efficiency standards in Europe and parts of Asia mandate strict power consumption thresholds, requiring continuous redesign of backlight and power modules. Restrictions on hazardous materials push manufacturers toward costly alternative compounds. Recycling compliance for large-format panels remains complex, with recovery rates below 35% globally. Meeting these regulatory and environmental benchmarks increases R&D expenditure and operational costs, especially for smaller manufacturers.

Expansion of Mini-LED Backlighting Architectures: Mini-LED adoption in QLED Smart TVs increased by over 48% between 2022 and 2024, enabling peak brightness levels above 2,000 nits and contrast improvements of nearly 3× compared to standard LED models. TVs with over 1,000 local dimming zones now account for 37% of premium shipments.

AI-Driven Picture and Sound Optimization: More than 62% of newly launched QLED Smart TVs incorporate AI processors capable of real-time upscaling, reducing noise artifacts by 28% and improving motion clarity by 31%. AI-based audio tuning has enhanced perceived sound output efficiency by 24%.

Growth of Large-Screen Consumer Preferences: Demand for QLED TVs above 65 inches has grown by 44%, driven by falling per-inch display costs and home theater adoption. In North America, 71% of QLED purchases now exceed 55 inches, compared to 52% in 2021.

Energy-Efficient and Sustainable Design Focus: Manufacturers have reduced average power consumption per screen inch by 19% since 2022 through improved quantum-dot efficiency and adaptive brightness systems. Over 34% of new models now use recycled plastics and eco-packaging, aligning with tightening global sustainability norms.

The QLED Smart TV Market segmentation reflects clear differentiation across product types, applications, and end-user groups, shaped by screen size preferences, performance expectations, and usage environments. By type, segmentation is driven by panel architecture, backlighting technology, and resolution capabilities, with advanced variants increasingly favored for premium viewing experiences. Application-wise, residential usage dominates due to entertainment, gaming, and OTT consumption, while commercial applications such as digital signage and hospitality displays are expanding steadily. From an end-user perspective, households remain the core demand base, but institutional buyers—including hospitality operators, corporate offices, and educational institutions—are demonstrating rising adoption of large-format QLED displays. Across segments, purchasing decisions are influenced by brightness performance, energy efficiency, AI-driven picture enhancement, and smart ecosystem compatibility rather than price alone, signaling a structurally premium-oriented market profile.

The QLED Smart TV Market by type is segmented into Standard QLED TVs, Mini-LED QLED TVs, 8K QLED TVs, and Hybrid QLED variants integrated with advanced AI processors. Standard QLED TVs currently account for approximately 41% of total adoption, driven by their balance of high brightness, color accuracy, and comparatively lower production complexity. Mini-LED QLED TVs follow closely, offering significantly higher contrast control through thousands of local dimming zones. Mini-LED QLED TVs represent the fastest-growing type, expanding at an estimated CAGR of around 21.8%, supported by declining Mini-LED chip costs, demand for premium HDR performance, and increasing consumer preference for large-screen formats above 65 inches. 8K QLED TVs, while still niche, are gaining relevance in ultra-premium home theaters and commercial visualization environments. Hybrid and specialized QLED variants collectively contribute about 27% of the market, serving gaming-focused users, commercial buyers, and early adopters.

By application, residential entertainment represents the leading segment, accounting for approximately 63% of overall adoption, supported by widespread OTT streaming, console gaming, and home theater upgrades. QLED Smart TVs are increasingly positioned as central multimedia hubs, with high refresh rates and AI-based upscaling driving replacement demand. Commercial digital signage and hospitality applications form the fastest-growing application segment, expanding at an estimated CAGR of about 19.6%, fueled by demand for high-brightness displays in retail storefronts, hotels, airports, and conference venues. QLED’s durability and sustained luminance performance make it suitable for long daily operating hours. Educational and corporate meeting room applications, combined, contribute around 24% of total usage, benefiting from large-screen collaboration needs. Consumer adoption data highlights these trends: in 2024, over 57% of global consumers reported prioritizing screen quality over price when purchasing smart TVs, while nearly 46% of gamers preferred QLED displays for low-latency performance.

From an end-user perspective, households remain the dominant segment, representing roughly 66% of total QLED Smart TV installations, driven by urbanization, rising disposable income, and increased time spent on digital entertainment. Within this group, families with high-speed broadband and subscription-based streaming services show the highest upgrade frequency. The hospitality and commercial enterprise segment is the fastest-growing end-user group, with adoption expanding at an estimated CAGR of approximately 20.3%, supported by hotel renovations, smart room integration, and digital branding initiatives. Corporate offices and educational institutions together contribute about 22% of total demand, while niche end-users such as healthcare waiting areas and control rooms make up the remaining share. Adoption indicators reinforce this shift: in 2024, over 41% of hotels globally reported upgrading to large-format smart displays for guest engagement, while nearly 38% of enterprises deployed QLED displays for internal communication and customer-facing environments.

Asia-Pacific accounted for the largest market share at 44.6% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2025 and 2032.

Asia-Pacific’s leadership is supported by manufacturing output exceeding 180 million TV units annually, strong domestic consumption, and high urban smart TV penetration above 65% in tier-1 cities. North America’s growth momentum is reinforced by premium screen adoption, where over 58% of households own TVs larger than 55 inches, and strong replacement cycles every 4–5 years. Europe held approximately 21.3% share in 2024, driven by sustainability mandates and energy-efficient upgrades. South America and the Middle East & Africa together accounted for nearly 14.7%, supported by expanding broadband coverage, declining panel costs, and rising demand for localized digital content across emerging economies.

The market accounted for 24.1% of global QLED Smart TV demand in 2024, supported by strong household purchasing power and high OTT penetration exceeding 82% of internet users. Demand is driven by residential entertainment, gaming, corporate conferencing, and hospitality installations. Energy-efficiency labeling standards and federal incentives encouraging low-power consumer electronics are influencing product design. Technological advancement is evident in widespread adoption of 120–144 Hz refresh rates, AI-based upscaling, and console-optimized displays. A leading regional electronics brand expanded domestic assembly lines in 2023 to support faster premium TV delivery cycles. Consumer behavior reflects preference for large screens, with nearly 71% of buyers choosing displays above 55 inches, and strong demand from home-based workers and gamers seeking immersive visuals.

Europe represented approximately 21.3% of global QLED Smart TV installations in 2024, with Germany, the UK, and France contributing over 62% of regional volume. Regulatory frameworks emphasizing eco-design, repairability scores, and reduced standby power consumption are shaping procurement decisions. Adoption of Mini-LED QLED TVs is rising, particularly in Western Europe, where over 48% of new premium TV purchases meet advanced energy-efficiency classifications. European manufacturers and distributors are prioritizing recyclable packaging and reduced hazardous material content. Consumer behavior reflects a strong preference for certified low-energy products, with more than 54% of buyers factoring sustainability labels into purchase decisions, accelerating the transition toward energy-optimized QLED displays.

Asia-Pacific led global demand with 44.6% market share in 2024, supported by high-volume manufacturing and consumption across China, India, Japan, and South Korea. China alone accounts for over 50% of regional production output, while India recorded double-digit annual growth in smart TV household penetration, reaching 39% in urban areas. The region benefits from vertically integrated supply chains, local semiconductor fabrication, and government-supported electronics manufacturing clusters. Innovation hubs are advancing Mini-LED, AI image processing, and ultra-thin panel designs. Regional consumer behavior shows strong price-performance sensitivity, with over 63% of purchases occurring via e-commerce platforms, accelerating adoption of mid-to-premium QLED models.

South America accounted for approximately 9.2% of global QLED Smart TV demand in 2024, led by Brazil and Argentina, which together represent over 61% of regional consumption. Expanding broadband infrastructure and rising demand for high-definition sports and streaming content are key growth enablers. Trade policies supporting electronics assembly and reduced import duties on display components are improving affordability. Local assemblers are increasingly introducing QLED models optimized for tropical operating conditions and multilingual interfaces. Consumer behavior highlights strong preference for locally adapted content, with nearly 57% of users prioritizing language support and regional streaming platforms when purchasing smart TVs.

The Middle East & Africa region contributed around 5.5% of global demand in 2024, driven by rising urbanization and digital infrastructure investments. The UAE, Saudi Arabia, and South Africa are key growth markets, supported by smart city initiatives and hospitality expansion. High-brightness QLED displays are favored for well-lit environments, particularly in commercial and luxury residential settings. Regional trade partnerships and import facilitation policies are improving access to premium electronics. Consumer behavior varies widely, with over 46% of purchases in Gulf countries concentrated in the premium segment, while African markets show gradual adoption driven by declining panel costs and mobile-first digital consumption.

China – 31.8% Market Share: Dominance supported by large-scale production capacity, vertically integrated display manufacturing, and strong domestic consumption of smart TVs.

United States – 19.6% Market Share: Leadership driven by high household adoption of premium large-screen TVs, advanced digital infrastructure, and strong demand from entertainment and gaming users.

The QLED Smart TV Market exhibits a moderately consolidated competitive structure, with approximately 25–30 active global and regional manufacturers competing across premium, mid-range, and value segments. The top five companies collectively account for nearly 72% of global unit shipments, reflecting strong brand concentration and high barriers to entry related to panel sourcing, semiconductor integration, and intellectual property in quantum-dot materials.

Market leaders compete primarily on display brightness (exceeding 2,000 nits in premium models), AI-powered image processing, energy efficiency compliance, and smart ecosystem integration rather than price alone. Strategic initiatives include frequent product refresh cycles every 9–12 months, long-term panel supply agreements, and expansion of Mini-LED backlighting portfolios, which now represent over 38% of premium QLED launches.

Innovation-led competition is accelerating, with more than 60% of major brands integrating proprietary AI processors for upscaling, motion enhancement, and adaptive brightness. Partnerships with gaming console manufacturers, OTT platforms, and smart home ecosystems are shaping differentiation strategies. The competitive environment favors players with vertically integrated manufacturing, global distribution reach, and the ability to comply with evolving energy-efficiency and sustainability regulations.

Sony Corporation

Panasonic Corporation

Sharp Corporation

Vizio Holding Corp.

Skyworth Digital

Technology evolution is a core competitive driver in the QLED Smart TV Market, with rapid advancements across panel architecture, backlighting systems, processing chipsets, and energy optimization. Mini-LED backlighting has become a foundational technology, enabling 1,000–5,000 local dimming zones, improving contrast ratios by up to 3× compared to conventional LED-lit QLED displays.

Quantum-dot film innovations now deliver over 90% DCI-P3 color volume, while low-cadmium and cadmium-free materials support regulatory compliance across Europe and Asia. AI processors capable of real-time 4K and 8K upscaling have reduced image noise by approximately 28% and improved motion interpolation accuracy by 30–35% in fast-moving content.

Connectivity technologies are also advancing, with HDMI 2.1 adoption exceeding 70% in premium models, supporting higher refresh rates and low-latency gaming. Energy efficiency remains a critical focus area; adaptive brightness control and AI-driven power management have reduced average energy consumption per viewing hour by 18–22% since 2022.

Emerging technologies include cloud gaming optimization, voice-based content discovery, and smart home dashboard integration, positioning QLED Smart TVs as multifunctional digital hubs rather than standalone entertainment devices.

In June 2024, Samsung unveiled its 2024 QLED 4K TV range featuring Quantum Dot and Quantum HDR technology that delivers over a billion vibrant colours, 4K upscaling, Quantum Processor Lite enhancements, and advanced audio features like Q-Symphony and OTS Lite. This lineup is offered across multiple screen sizes including 55”, 65”, and 75”, aiming to elevate premium home viewing experiences. Source: www.samsung.com

At CES 2024, Samsung introduced its 2024 Neo QLED 8K and 4K TV lineup, powered by the NQ8 AI Gen3 processor which is significantly faster than its predecessor, improving AI-assisted upscaling and motion processing for clearer visuals and smarter content delivery. Source: www.samsung.com

In early 2025, the premium TV market—including QLED models—grew 51% year-over-year in Q4 2024, with Samsung maintaining leadership and TCL surpassing LG to capture second place in global premium smart TV shipments. Source: www.cepro.com

Data from 2024 shows that QLED smart TV shipments in India surged by 182% year-on-year in Q1 2024, while overall smart TV shipments declined; 55-inch and larger models also saw a 23% increase in volume, highlighting consumer preference for larger, premium QLED screens. Source: www.timesofindia.indiatimes.com

The QLED Smart TV Market Report provides a comprehensive evaluation of the global market across product types, applications, end-user categories, technologies, and geographic regions. The scope includes segmentation by Standard QLED, Mini-LED QLED, 8K QLED, and hybrid AI-enabled models, covering screen sizes from 43 inches to above 85 inches. Application coverage spans residential entertainment, hospitality, retail signage, corporate collaboration, education, and public infrastructure deployments.

Geographically, the report analyzes market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level insights for major consumption and production hubs including China, the United States, India, Japan, Germany, and Brazil. The technology scope encompasses quantum-dot materials, Mini-LED backlighting, AI processors, HDMI 2.1 connectivity, and energy-efficient display architectures.

The report also examines competitive positioning, innovation pipelines, regulatory impacts, sustainability initiatives, and consumer adoption behavior, including trends such as large-screen migration, gaming-driven upgrades, and smart home integration. Emerging niches—such as QLED displays for commercial visualization and education—are assessed to provide decision-makers with a forward-looking, strategic understanding of the market’s breadth and evolution.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 33,262.7 Million |

| Market Revenue (2032) | USD 120,853.8 Million |

| CAGR (2025–2032) | 17.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Samsung Electronics; TCL Electronics; LG Electronics; Hisense Group; Sony Corporation; Panasonic Corporation; Sharp Corporation; Vizio Holding Corp.; Skyworth Digital |

| Customization & Pricing | Available on Request (10% Customization Free) |