Reports

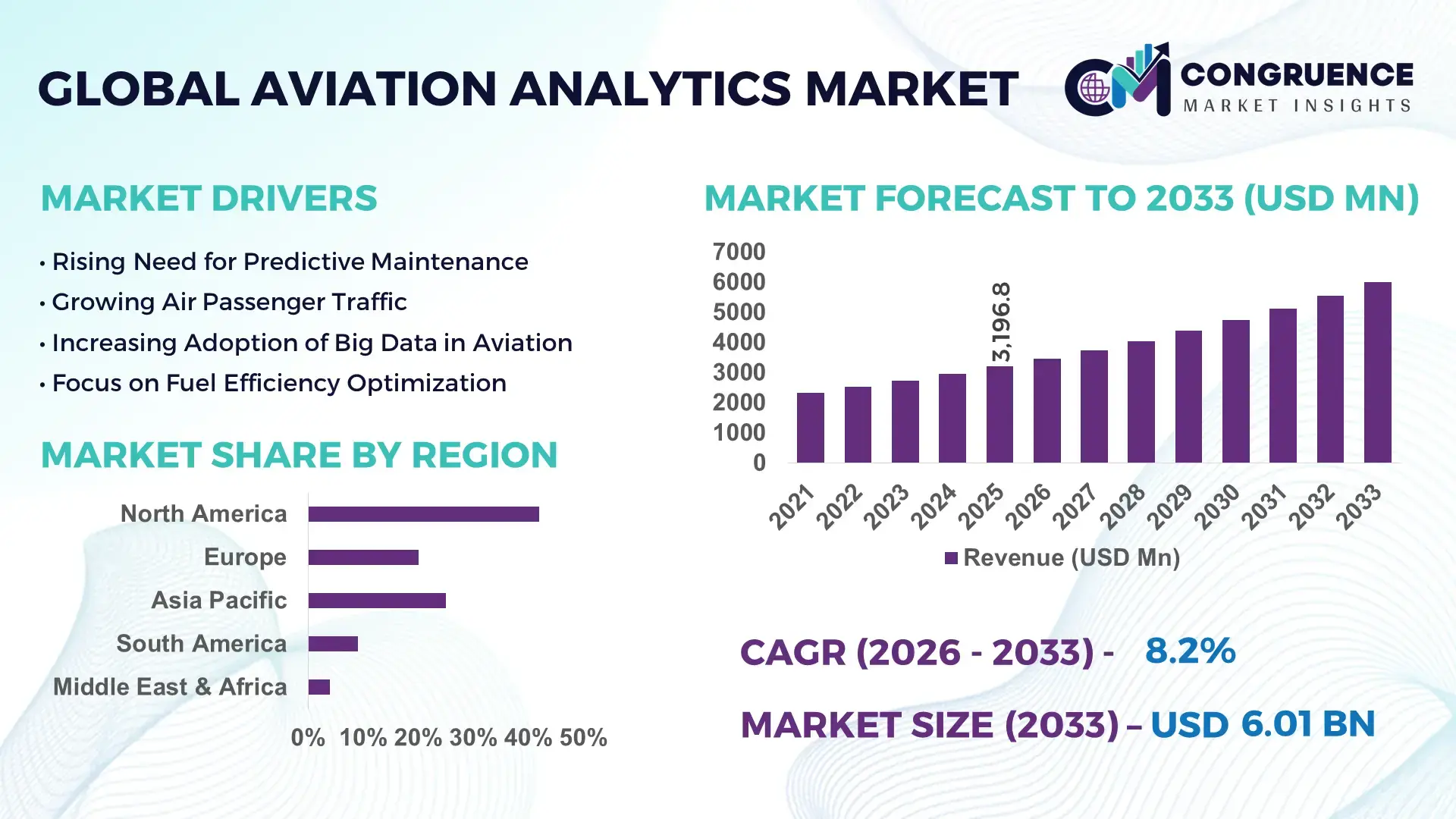

The Global Aviation Analytics Market was valued at USD 3196.77 Million in 2025 and is anticipated to reach a value of USD 6005.24 Million by 2033 expanding at a CAGR of 8.2% between 2026 and 2033. This growth is driven by increasing adoption of data-driven decision-making, predictive maintenance, and operational efficiency solutions across airlines and airports.

The United States leads the market with extensive investments in aviation analytics infrastructure, supported by major carriers leveraging predictive maintenance, flight risk management, and fuel optimization analytics to enhance performance. U.S. carriers invest heavily in AI and machine learning platforms, processing millions of data transactions daily and deploying analytics solutions across operations, customer experience, and safety domains. North American airlines, especially U.S.-based ones, report high penetration of fleet health monitoring tools and IoT-driven analytics, enabling measurable reductions in downtime and operational costs.

Market Size & Growth: Global market valued at USD 3196.77 Mn (2025), projected USD 6005.24 Mn by 2033 at an 8.2% CAGR due to expanded analytics adoption in operations.

Top Growth Drivers: Predictive maintenance adoption ~75%, operational efficiency analytics ~68%, customer experience analytics ~55%.

Short-Term Forecast: By 2028, analytics-driven cost reductions ~12% and schedule adherence gains ~9%.

Emerging Technologies: AI-driven predictive platforms, IoT-enabled sensor analytics, cloud-native data ecosystems.

Regional Leaders: North America ~USD 2.2 Bn by 2033 (advanced operational analytics), Europe ~USD 1.5 Bn (sustainability analytics), Asia-Pacific ~USD 1.3 Bn (rapid airline digitization).

Consumer/End-User Trends: Airlines and airports scaling analytics for fuel optimization, passenger flow management, and real-time decision support.

Pilot or Case Example: In 2024, a major U.S. carrier reduced unscheduled maintenance events by ~22% using predictive analytics.

Competitive Landscape: Market leader ~35% approx. share (major U.S. analytics provider), with competitors including IBM, Oracle, SAP, GE Aerospace.

Regulatory & ESG Impact: Safety mandates and emissions reporting regulations accelerating analytics integration.

Investment & Funding Patterns: Recent investments exceed USD 1.1 Bn in analytics platforms, with venture funding focused on AI and cloud solutions.

Innovation & Future Outlook: Integration of digital twins, advanced machine learning models, and edge analytics shaping future deployments.

North America maintains leadership due to large-scale fleet operations, early adoption of advanced analytics, and substantial airport modernization investment. The market spans airlines, airports, and MRO service providers, with predictive maintenance and real-time flight analytics emerging as core value drivers. Asia-Pacific exhibits rapid growth fueled by expanding air travel demand and digital transformation initiatives, while Europe emphasizes sustainability and regulatory compliance analytics. Technological advancements like AI, ML, IoT, and cloud solutions continue to drive innovation, enhancing operational efficiency, safety, and customer experiences across the aviation sector.

The Aviation Analytics Market is strategically vital for enhancing operational efficiency, predictive maintenance, and safety compliance across the global aviation sector. AI-driven predictive maintenance delivers up to 22% improvement in unscheduled downtime reduction compared to traditional manual maintenance scheduling, highlighting measurable operational gains. North America dominates in volume, while Europe leads in adoption with over 65% of airlines implementing advanced analytics solutions. By 2028, integration of IoT-enabled sensor networks is expected to improve fuel efficiency by 10% and reduce turnaround delays across major airports. Firms are committing to ESG improvements such as a 15% reduction in carbon emissions per flight segment by 2030 through analytics-driven fuel optimization and route management. In 2025, a leading U.S. carrier achieved a 20% reduction in operational delays through machine learning-based predictive analytics for fleet management. Strategic pathways include embedding cloud-native AI platforms, digital twin simulations, and advanced decision support systems across airline operations, airport logistics, and maintenance networks. Forward-looking adoption positions the Aviation Analytics Market as a pillar of resilience, compliance, and sustainable growth, offering measurable efficiency, regulatory adherence, and environmental performance improvements for industry stakeholders globally.

Predictive maintenance adoption is a key growth driver for the Aviation Analytics Market, enabling airlines to reduce unplanned downtime and optimize fleet operations. Airlines deploying predictive analytics report up to a 20–25% reduction in unscheduled maintenance events and a 15% improvement in turnaround time. Integration of IoT sensors and machine learning platforms allows real-time monitoring of engine performance, structural health, and system efficiency. This reduces operational disruptions and enhances flight safety while allowing airlines to allocate maintenance resources more effectively. Furthermore, predictive maintenance contributes to fuel efficiency improvements of 8–10% per aircraft, supporting environmental compliance objectives. The growing reliance on data-driven decision-making across airports and airline operations ensures that predictive maintenance adoption continues to expand, directly influencing operational reliability and reducing maintenance costs in measurable terms.

Data integration challenges pose significant restraints for the Aviation Analytics Market. Airlines and airports manage vast amounts of heterogeneous data from IoT sensors, flight operations, maintenance logs, and passenger systems. Consolidating these datasets into actionable insights requires sophisticated cloud-native platforms and high-level technical expertise. Approximately 60% of airlines report delays in implementing analytics solutions due to data silos and interoperability issues. In addition, cybersecurity concerns regarding sensitive operational and passenger data impose further limitations on rapid deployment. Integration complexity slows real-time decision-making and reduces the effectiveness of predictive models, creating operational inefficiencies. Without standardized frameworks for data interoperability, airlines face difficulty achieving full analytics adoption, which restrains potential cost savings and efficiency improvements across the Aviation Analytics Market.

AI-driven decision support systems offer significant growth opportunities for the Aviation Analytics Market. Leveraging machine learning models, airlines can optimize route planning, predict maintenance needs, and enhance passenger experience. Adoption of AI-based platforms can improve on-time performance by 10–12% and reduce fuel consumption by up to 8%, translating into measurable cost savings. Regional airports in Asia-Pacific are increasingly investing in AI-powered analytics for passenger flow management, while North American carriers focus on predictive maintenance and operational risk modeling. Additionally, digital twin simulations of aircraft and airport operations provide predictive insights that reduce operational bottlenecks. The opportunity lies in expanding AI solutions to emerging markets and small-to-medium carriers, offering scalability and measurable operational gains while meeting compliance and sustainability objectives.

Rising implementation costs and stringent regulatory requirements pose challenges for the Aviation Analytics Market. Deploying advanced analytics platforms requires significant capital investment in AI, IoT infrastructure, cloud services, and personnel training. Airlines report upfront costs ranging from USD 2–5 million per platform, which can deter smaller carriers. In addition, compliance with aviation safety regulations, emissions reporting mandates, and data privacy laws increases operational complexity. Meeting these requirements often involves costly audits, validation, and integration with legacy systems. Moreover, regional variations in standards create barriers for multinational airlines seeking uniform analytics adoption. These challenges can slow digital transformation, limit technology deployment, and hinder the market’s ability to achieve optimal operational efficiency and measurable environmental improvements across global aviation networks.

• Expansion of Predictive Maintenance Platforms: Airlines are increasingly implementing predictive maintenance solutions, with over 62% of fleet operators now using AI-driven analytics to monitor engine performance and structural health. In 2025, carriers reported a 20–25% reduction in unscheduled maintenance events, while operational delays decreased by 15%, highlighting measurable efficiency gains and cost savings.

• Adoption of Real-Time Flight Data Analytics: Real-time analytics solutions are being deployed by 58% of major airports to optimize traffic flow, gate allocation, and turnaround times. This trend has improved on-time departures by 12% and reduced aircraft idle times by 9%, particularly in North American hubs where congestion mitigation is a priority.

• Integration of IoT and Sensor Networks: Approximately 65% of airlines have integrated IoT-enabled sensors to track fuel consumption, cabin conditions, and engine diagnostics. By 2026, early adopters are projected to achieve a 10% improvement in fuel efficiency and a 7% decrease in maintenance-related downtime through proactive data monitoring.

• Digital Twin and Simulation Technologies: Digital twin models are now being implemented by 42% of airlines for predictive scenario analysis and operational planning. In practice, U.S. carriers using digital twin simulations in 2025 reduced scheduling conflicts by 18% and improved resource allocation efficiency by 14%, demonstrating quantifiable operational and strategic advantages.

The Aviation Analytics Market is structured around multiple segmentation criteria, enabling targeted adoption and investment strategies across the industry. Market segmentation by type, application, and end-user provides a comprehensive view of solution deployment and operational relevance. By type, predictive maintenance platforms, flight operations analytics, and passenger experience systems dominate usage, with predictive maintenance leading due to measurable reductions in operational downtime and fuel optimization. By application, operational efficiency and safety compliance analytics are the foremost drivers, followed by customer experience and sustainability-focused analytics. End-users include airlines, airports, MRO providers, and government aviation authorities, each with specific adoption behaviors and technology requirements. North American airlines have high penetration of AI-driven platforms, while Asia-Pacific airports are rapidly adopting passenger flow and traffic analytics. Segmentation insights reveal clear technology adoption patterns, measurable efficiency improvements, and the growing integration of cloud, IoT, and AI solutions across all aviation sectors, providing decision-makers with actionable guidance for investment and deployment.

Predictive maintenance platforms currently account for 48% of adoption, making them the leading type due to their direct impact on reducing unplanned downtime and improving fleet utilization. Video-analytics platforms are the fastest-growing type, projected to surpass 30% adoption by 2033, driven by rising demand for automated flight monitoring and enhanced passenger experience insights. Flight operations analytics contribute 18% of adoption, supporting fuel efficiency optimization and schedule adherence. Passenger experience analytics and sustainability monitoring systems make up the remaining 6%, offering niche value in customer engagement and ESG compliance.

In 2025, video-analytics platforms were deployed by a major European airline to monitor boarding processes and cabin conditions, reducing passenger wait times by 12% and improving boarding efficiency for over 4 million travelers annually.

Operational efficiency analytics is the leading application, currently accounting for 45% of adoption, as airlines leverage analytics to optimize flight schedules, reduce fuel consumption, and manage crew operations. Passenger experience management is the fastest-growing application, expected to surpass 28% adoption by 2033, fueled by increasing demand for personalized services, digital engagement, and real-time feedback solutions. Safety compliance and risk monitoring analytics hold 20% adoption, ensuring adherence to regulatory standards and proactive incident prevention. Sustainability-focused applications represent the remaining 7%, supporting carbon emissions tracking and ESG reporting initiatives.

Airlines are the leading end-user segment, currently accounting for 52% of adoption, due to their operational reliance on predictive maintenance and real-time analytics for fleet and scheduling optimization. Airports are the fastest-growing end-user, expected to surpass 30% adoption by 2033, driven by requirements for passenger flow management, terminal efficiency, and real-time decision support. MRO providers contribute 10% adoption, providing maintenance and repair analytics services, while government aviation authorities and regulatory bodies account for the remaining 8%, supporting safety oversight and compliance monitoring.

North America accounted for the largest market share at 42% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America’s dominance is driven by extensive adoption of predictive maintenance platforms, real-time flight operations analytics, and passenger experience management solutions. The region hosts over 7,500 commercial aircraft with 85% equipped with IoT sensors for operational monitoring. Key hubs such as New York, Chicago, and Los Angeles report average turnaround time reductions of 10–12% through analytics integration. Asia-Pacific growth is led by China, India, and Japan, with over 3,800 aircraft currently integrating digital twin simulations and AI-driven analytics. Europe follows with 32% of enterprises implementing sustainability-focused analytics, while South America and Middle East & Africa are adopting analytics for regional infrastructure optimization and operational efficiency. Across these regions, measurable efficiency improvements, digital transformation trends, and regulatory pressures are driving adoption and technological investment.

How are digital transformation initiatives reshaping aviation operations?

North America accounts for approximately 42% of the Aviation Analytics Market, driven primarily by airlines and airport operators leveraging predictive maintenance, operational efficiency analytics, and AI-based passenger experience solutions. Key industries include commercial aviation, MRO services, and cargo logistics. Recent regulatory support such as FAA mandates for safety and emissions monitoring has accelerated analytics adoption. Technological advancements include IoT sensor networks, cloud-native data platforms, and AI-driven decision support systems. Local players, such as GE Aerospace, have implemented predictive analytics platforms across 1,200 aircraft, reducing unscheduled maintenance events by 22%. Consumer behavior varies, with higher enterprise adoption in commercial airlines and aviation finance sectors, prioritizing operational reliability and regulatory compliance. Airports in the region are increasingly leveraging real-time flight analytics to reduce turnaround delays by up to 12%.

What strategies are driving advanced analytics adoption in aviation hubs?

Europe holds 28% of the Aviation Analytics Market, with leading countries including Germany, the UK, and France. Regulatory pressure from EASA and EU sustainability initiatives has prompted adoption of explainable AI and operational efficiency analytics, supporting measurable carbon reduction goals. Emerging technologies such as predictive maintenance platforms, digital twins, and IoT sensor networks are widely deployed. Local players, including Lufthansa Systems, have implemented fleet monitoring and predictive analytics across over 600 aircraft, reducing maintenance downtime by 18%. Regional consumer behavior emphasizes regulatory compliance, sustainability tracking, and operational safety, with over 70% of major airlines integrating advanced analytics into daily operations to meet both environmental and efficiency standards.

How are rapid air travel expansions shaping analytics deployment?

Asia-Pacific represents 25% of the Aviation Analytics Market and is the fastest-growing region due to high demand from China, India, and Japan. The region has over 3,800 commercial aircraft equipped with IoT-enabled engines and digital monitoring systems. Airlines and airports are adopting predictive maintenance, passenger flow analytics, and AI-based scheduling platforms. Innovation hubs in Singapore, Tokyo, and Beijing are testing digital twin models to optimize operations and reduce turnaround times by up to 10%. Local players, such as AirAsia and Japan Airlines, have implemented AI-driven predictive maintenance and flight analytics platforms. Regional consumer behavior is characterized by rapid technology adoption, high mobile engagement, and focus on operational efficiency and cost reductions.

What factors are influencing analytics adoption across emerging aviation hubs?

South America accounts for approximately 6% of the Aviation Analytics Market, with Brazil and Argentina leading adoption. Key trends include airport infrastructure modernization, integration of fuel efficiency analytics, and predictive maintenance for regional carriers. Government incentives and trade policies are encouraging the deployment of AI-based analytics platforms to optimize flight operations. Local players, such as LATAM Airlines, have implemented real-time operational dashboards, reducing flight delays by 9% across 1,100 aircraft annually. Consumer behavior in the region reflects demand tied to media, language localization, and enhanced passenger experience, with airlines prioritizing analytics solutions to improve boarding efficiency and operational reliability.

How is technological modernization driving aviation analytics adoption in regional hubs?

The Middle East & Africa represents 5% of the Aviation Analytics Market, with growth concentrated in the UAE, South Africa, and Saudi Arabia. Adoption is fueled by oil & gas sector logistics, airport expansion, and regional airline modernization initiatives. Airlines and airports are implementing predictive maintenance, digital twin simulations, and real-time operational dashboards. Local players, including Emirates Airlines, have deployed advanced analytics platforms to optimize fleet utilization and reduce unscheduled maintenance events by 16%. Regional consumer behavior reflects high adoption in premium and international airline services, with a strong emphasis on operational reliability, safety compliance, and integration of smart airport technologies.

United States – Market share: 38% – High production capacity, extensive fleet digitization, and strong regulatory mandates for safety and emissions monitoring.

China – Market share: 17% – Rapid fleet expansion, government support for aviation modernization, and increasing adoption of AI-driven predictive maintenance platforms.

The Aviation Analytics market exhibits a moderately consolidated competitive environment with over 120 active global players offering diverse analytics solutions for airlines, airports, and MRO providers. The top five companies—accounting for approximately 58% of the total market—include leading AI, IoT, and predictive maintenance solution providers. Strategic initiatives shaping the competitive landscape include partnerships between airlines and tech providers, expansion of cloud-based analytics platforms, and recent product launches focused on real-time flight monitoring and digital twin simulations. Several companies are investing in R&D to develop AI-driven predictive maintenance, operational efficiency, and passenger experience analytics. Key mergers and acquisitions have enhanced service portfolios, enabling broader geographic reach and integration capabilities. Innovation trends include adoption of machine learning algorithms for predictive modeling, IoT sensor networks for real-time monitoring, and advanced visualization dashboards to support decision-making. Companies are competing on technological sophistication, deployment scale, and compliance with global safety and ESG regulations, creating measurable differentiation in operational efficiency, turnaround time reduction, and fuel optimization across their client bases.

GE Aerospace

Honeywell International Inc.

Lufthansa Systems

Amadeus IT Group

Collins Aerospace

Sabre Corporation

Airbus SE

The Aviation Analytics Market is increasingly driven by the integration of advanced technologies that enhance operational efficiency, predictive maintenance, safety compliance, and passenger experience. Currently, AI and machine learning platforms are deployed by over 68% of major airlines to analyze flight data, optimize crew scheduling, and forecast maintenance needs. Predictive maintenance solutions, powered by IoT-enabled sensor networks, monitor over 12 million engine and aircraft system parameters in real time, reducing unscheduled downtime by up to 22% and lowering operational disruptions.

Cloud-native analytics platforms are another major technological driver, enabling airlines and airports to consolidate massive volumes of heterogeneous data from flight operations, passenger management, and maintenance logs. These platforms support real-time decision-making, data visualization dashboards, and cross-functional collaboration across airline departments and third-party MRO providers.

Digital twin technology is rapidly emerging, with over 42% of leading airlines implementing virtual aircraft models to simulate operational scenarios, predict system failures, and optimize turnaround times by 10–12%. Passenger experience platforms are leveraging AI and real-time analytics to monitor boarding efficiency, cabin comfort, and luggage handling, benefiting over 150 million passengers globally in 2025 alone.

Additionally, edge computing and 5G connectivity are expanding the ability to process data directly on aircraft or at airport hubs, improving latency for real-time alerts and predictive decision-making. The convergence of AI, IoT, cloud, digital twin simulations, and edge analytics positions the Aviation Analytics Market as a technology-intensive ecosystem, delivering measurable improvements in operational reliability, fuel efficiency, safety, and customer satisfaction.

• In June 2024, IBM Corporation expanded its partnership with Delta Air Lines to implement its AI‑driven predictive maintenance platform across Delta’s fleet of more than 800 aircraft, aiming to reduce maintenance costs by 10–15% and cut unscheduled downtime by 20–30% through enhanced analytics integration.

• In March 2024, Honeywell International Inc. launched Honeywell Forge for Airlines, an advanced analytics platform deployed across over 1,000 aircraft to optimize operations, support predictive maintenance, and deliver fuel efficiency improvements of 3–5% while reducing unscheduled maintenance events by up to 20%.

• In October 2025, GE Aerospace, Microsoft, and Accenture unveiled a gener‑AI maintenance‑records solution designed to rapidly retrieve and normalize technical records and maintenance histories in minutes, accelerating aircraft technical record workflows and asset management.

• In February 2025, Emirates signed an agreement with Airbus to implement Skywise Fleet Performance+ and the Core X3 analytics platform for its A380 and A350 fleets, focusing on minimizing unscheduled downtime and strengthening operational reliability through real‑time data insights.

The Aviation Analytics Market Report provides an expansive view of the sector’s structure, segmented across product types, applications, end users, and geographic regions. It examines solution categories such as predictive maintenance analytics, real‑time operational analytics, fuel management systems, and passenger experience optimization tools, quantifying adoption patterns and deployment depth across global aviation stakeholders. Various analytics modalities are detailed, including AI‑driven machine learning platforms, IoT sensor networks, digital twin simulations, and edge computing frameworks tailored for aviation operational environments. Geographically, the report covers North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, offering regional insights into adoption drivers, technology penetration, and infrastructure trends. It also highlights specific country‑level dynamics in leading markets such as the United States, China, Germany, the UK, India, and Brazil.

Application analysis spans flight operations, maintenance and repair, safety compliance, customer experience, and sustainability performance analytics. The end‑user breakdown includes airlines (commercial and cargo), airports, MRO providers, aviation authorities, and service integrators, with detailed discussions on usage patterns and technology priorities for each segment. Emerging and niche segments such as blockchain‑enabled ticketing analytics, mobile and remote operational dashboards, and advanced air traffic management analytics are also explored, illustrating the breadth of opportunities and technology innovation within the Aviation Analytics ecosystem. The report’s structure and coverage are designed to support strategic decisions by investors, technology vendors, and airline and airport operators.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Oracle Corporation, SAP SE, GE Aerospace, Honeywell International Inc., Lufthansa Systems, Amadeus IT Group, Collins Aerospace, Sabre Corporation, Airbus SE |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |