Reports

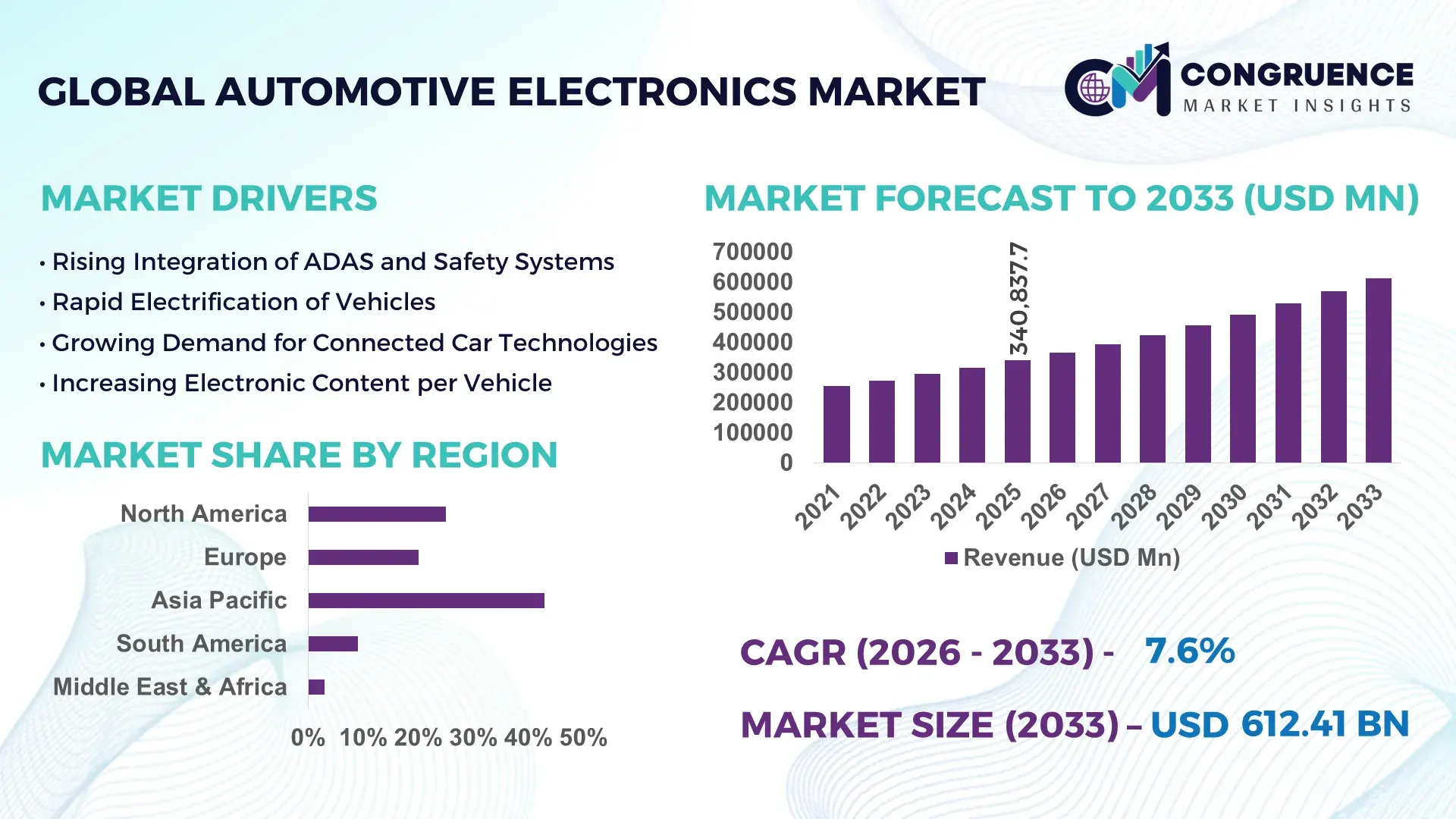

The Global Automotive Electronics Market was valued at USD 340837.67 Million in 2025 and is anticipated to reach a value of USD 612414.92 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033. Growth is driven by rapid electrification, ADAS integration, and rising software-defined vehicle architectures.

China represents the most significant national hub for automotive electronics production and deployment, supported by annual vehicle production exceeding 30 million units and new energy vehicle output surpassing 9 million units. The country has invested over USD 40 billion in automotive semiconductor and sensor manufacturing expansion since 2022, while domestic OEMs increasingly integrate Level 2+ ADAS, high-performance computing units, and domain controllers. Local production of power electronics, battery management systems, and in-vehicle infotainment modules has scaled alongside 5G-enabled connected car platforms and over-the-air software update ecosystems.

Market Size & Growth: USD 340.8B (2025) to USD 612.4B (2033), CAGR 7.6%, driven by EV and ADAS integration.

Top Growth Drivers: EV adoption +38%, ADAS penetration +42%, in-vehicle connectivity +35%.

Short-Term Forecast: By 2028, ECU consolidation improves system efficiency by 18% and reduces wiring costs by 12%.

Emerging Technologies: Zonal architectures, silicon carbide power devices, AI-based driver monitoring systems.

Regional Leaders: Asia Pacific USD 268B, Europe USD 171B, North America USD 143B by 2033; strong EV-electronics uptake.

Consumer/End-User Trends: Demand rising for connected infotainment, safety electronics, and energy-efficient power modules.

Pilot or Case Example: 2026 smart cockpit pilot improved HMI response time by 22% and reduced system faults by 15%.

Competitive Landscape: Bosch ~14% share; Continental, Denso, Aptiv, ZF Friedrichshafen key players.

Regulatory & ESG Impact: Emission norms, vehicle safety mandates, and EV incentives accelerating electronics integration.

Investment & Funding Patterns: Over USD 85B invested in EV electronics, semiconductor fabs, and software platforms.

Innovation & Future Outlook: Centralized computing, OTA upgrades, and integrated power electronics shaping next-gen vehicles.

Automotive electronics demand spans powertrain control, advanced safety systems, body electronics, infotainment, and telematics, with power electronics and ADAS contributing a substantial portion of system value in modern vehicles. Innovations in domain controllers, automotive-grade AI chips, and high-voltage battery control units are redefining vehicle architectures. Regulatory pressure for emission reduction, safety compliance, and digital vehicle standards continues to shape procurement strategies. Asia Pacific leads consumption growth due to EV manufacturing expansion, while Europe emphasizes safety and efficiency electronics. Increasing semiconductor localization, software-defined vehicle platforms, and electrified mobility ecosystems define the market’s forward trajectory.

Automotive electronics has become a core strategic layer of the mobility value chain, shifting competitive advantage from mechanical engineering toward software, semiconductors, and power electronics integration. Vehicles now incorporate more than 3,000 semiconductor devices on average in electric models, and electronic content per vehicle continues to rise as safety, connectivity, and electrification requirements intensify. Silicon carbide (SiC) power devices deliver 8–10% higher drivetrain efficiency compared to traditional silicon IGBTs, enabling extended driving range and reduced thermal losses. Asia Pacific dominates in production volume, while Europe leads in advanced safety-system adoption with over 70% of new vehicles equipped with multi-sensor ADAS platforms.

By 2028, AI-driven predictive diagnostics is expected to reduce vehicle electronic system downtime by 25% through real-time fault detection and over-the-air updates. Firms are committing to ESG metrics such as a 30% reduction in manufacturing-related Scope 2 emissions by 2030 through energy-efficient semiconductor fabrication and recyclable electronic modules. In 2026, a leading Asian EV manufacturer achieved a 15% reduction in power module heat loss through AI-optimized battery management algorithms. The Automotive Electronics Market is positioned as a structural pillar of industrial resilience, regulatory compliance, and sustainable mobility transformation.

Global electric vehicle production has surpassed 14 million units annually, each requiring significantly higher semiconductor and power electronics content than internal combustion models. Battery management systems monitor thousands of data points per second, while traction inverters and onboard chargers depend on high-efficiency switching devices. Electric drivetrains typically incorporate double the number of power modules compared to combustion platforms. Government mandates targeting zero-emission vehicle deployment and stricter fleet emission thresholds are compelling automakers to redesign architectures around high-voltage electronics. The integration of regenerative braking, energy-efficient thermal management, and intelligent charging interfaces further elevates electronic subsystem value and complexity within modern mobility platforms.

Automotive-grade chips must meet rigorous reliability standards, often requiring qualification cycles exceeding 12 months. Global semiconductor shortages have exposed dependency on limited fabrication nodes and specialized packaging capacity. A single advanced vehicle can use over 1,000 microcontrollers and sensors, making production highly sensitive to component lead-time fluctuations. Standardization gaps across communication protocols and software stacks complicate integration, raising validation workloads and testing costs. In addition, long design lifecycles in the automotive sector contrast with rapid semiconductor innovation cycles, creating mismatches in technology refresh rates and limiting swift adoption of next-generation electronic platforms.

Software-defined vehicle architectures centralize computing power into domain and zonal controllers, enabling feature deployment through over-the-air updates rather than hardware replacements. This approach can reduce wiring harness weight by up to 20% while simplifying system scalability. Advanced cockpit platforms integrating AI voice assistants, digital twins for vehicle diagnostics, and cloud-linked navigation systems are expanding electronics functionality beyond traditional hardware roles. Data monetization through telematics, usage-based insurance integration, and predictive maintenance platforms also opens recurring digital service opportunities, positioning electronics suppliers as long-term technology partners rather than one-time component vendors.

Modern connected vehicles generate several terabytes of data daily, requiring robust onboard processing and secure communication channels. Increasing electronic control unit consolidation elevates the impact of potential system failures, demanding higher redundancy and functional safety compliance. Cybersecurity threats targeting vehicle networks have increased significantly, pushing manufacturers to implement hardware-based encryption, intrusion detection, and secure boot mechanisms. Compliance with international vehicle safety and data protection regulations adds design overhead and testing requirements. Thermal management of high-density electronic modules and electromagnetic compatibility considerations further complicate integration in compact automotive environments.

• Rapid Migration to Zonal E/E Architectures Improving Wiring Efficiency by 20–30%

Automakers are transitioning from distributed electronic control units to zonal architectures that consolidate processing into high-performance controllers. This design reduces wiring harness length by nearly 30% and vehicle weight by around 10–15 kg per platform. Fewer control modules lower assembly complexity by 25% and improve diagnostic efficiency through centralized data processing, enabling faster software deployment cycles.

• Silicon Carbide Power Electronics Expanding EV Energy Efficiency by 8–12%

Adoption of SiC-based inverters and onboard chargers is accelerating across electric platforms. SiC devices operate at switching frequencies up to 10x higher than silicon alternatives, cutting power losses by 10% and reducing cooling requirements by 15%. Higher thermal tolerance supports compact module design, allowing up to 20% size reduction in powertrain electronics and extending driving range in high-voltage architectures.

• AI-Driven In-Cabin Electronics Increasing Processing Demand by Over 40%

Next-generation infotainment and driver monitoring systems integrate neural processors capable of handling more than 5 trillion operations per second. Cabin sensing modules now combine 3–5 cameras and radar sensors, improving driver alert detection accuracy by 25%. Voice-enabled and gesture-based interfaces reduce manual control inputs by 30%, enhancing safety and user experience within connected vehicle ecosystems.

• Over-the-Air (OTA) Update Penetration Surpassing 60% in New Connected Vehicles

More than 60% of newly produced connected vehicles now support OTA software updates, cutting dealership service visits by 35%. Centralized update systems enable feature activation within minutes and reduce recall-related service costs by up to 20%. Secure firmware management and cloud-based diagnostics also shorten fault resolution time by nearly 25%, strengthening lifecycle system performance.

The Automotive Electronics Market is segmented across product types, vehicle applications, and end-user categories, reflecting the technological complexity of modern mobility systems. Product segmentation includes power electronics, safety and ADAS modules, infotainment and telematics, body electronics, and electronic control units. Electrification and automation trends are shifting system value toward high-voltage components and sensor-driven safety platforms. Application-wise, electronics integration varies between passenger vehicles, commercial fleets, and emerging autonomous mobility platforms, with increasing feature standardization across vehicle classes. End-user demand patterns are influenced by OEM production strategies, Tier-1 supplier system integration, and aftermarket service ecosystems. Passenger vehicle electronics adoption rates exceed 70% for connected features, while commercial vehicle platforms prioritize telematics and energy management systems for operational efficiency. Industry stakeholders focus on modular design, semiconductor localization, and software-driven architectures to meet safety mandates and performance expectations.

Power electronics, ADAS and safety systems, infotainment and connectivity modules, body electronics, and control units form the primary product categories. ADAS and safety electronics account for nearly 34% of total system integration due to regulatory mandates for electronic stability control, collision avoidance, and driver monitoring. Power electronics are the fastest-growing type, advancing at approximately 9% CAGR, driven by electric vehicle expansion and demand for high-efficiency inverters and onboard chargers. Infotainment and connectivity modules represent around 22% of installations, supporting cloud services and real-time navigation. Body electronics and conventional control units together contribute roughly 24%, maintaining relevance in lighting, climate, and access control subsystems.

Passenger vehicles dominate applications, accounting for about 68% of automotive electronics integration due to rising deployment of infotainment displays, connectivity modules, and driver assistance features. Commercial vehicles represent nearly 22%, with telematics and fleet monitoring electronics improving logistics efficiency and predictive maintenance accuracy. Autonomous and semi-autonomous mobility platforms are the fastest-growing application area, expanding at close to 10% CAGR as sensor fusion, LiDAR interfaces, and AI processors scale in deployment. Remaining applications, including specialty vehicles and off-highway equipment, collectively contribute around 10%, emphasizing durability-focused electronics.

Original equipment manufacturers (OEMs) represent the leading end-user segment, accounting for approximately 72% of automotive electronics procurement as integrated system design shifts upstream into vehicle development cycles. Tier-1 suppliers follow, contributing nearly 20% through module-level integration and subsystem engineering. The aftermarket segment, including retrofitted telematics and infotainment upgrades, holds about 8% but is expanding steadily with connected vehicle adoption. Electric mobility startups and fleet operators are the fastest-growing end-user group, progressing at nearly 11% CAGR due to demand for advanced battery control and predictive maintenance systems. Adoption of connected fleet management platforms exceeds 60% among large logistics operators, reflecting growing reliance on electronics-driven operational analytics.

Asia Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Asia Pacific leads with annual vehicle production exceeding 50 million units, supported by strong electronics manufacturing ecosystems and over 60% of global EV battery cell output. Europe contributes nearly 27% of advanced safety electronics installations, driven by mandatory ADAS integration in new vehicles. North America represents about 21% of total demand, with connected vehicle penetration surpassing 70% in new passenger models. South America and the Middle East & Africa collectively account for roughly 6%, showing rising adoption of telematics and fleet monitoring electronics. Over 85% of newly developed vehicle platforms globally now incorporate centralized computing modules, while more than 40% of vehicles produced in 2025 feature Level 2 driver assistance capabilities, reflecting regional alignment toward software-defined and electrified vehicle architectures.

How Are Software-Defined Vehicles Reshaping Advanced Mobility Platforms?

This market represents approximately 21% of global Automotive Electronics integration, driven by strong demand across passenger vehicles, commercial fleets, and electric mobility startups. Key industries include EV manufacturing, autonomous driving technology, and semiconductor design. Regulatory mandates for advanced driver assistance, cybersecurity compliance, and vehicle emission standards are accelerating electronics deployment. Over 70% of new vehicles feature embedded connectivity modules, while more than 50% integrate driver monitoring systems. Digital cockpit adoption and centralized computing architectures are becoming mainstream. A major regional supplier recently expanded silicon carbide module production capacity by 25% to support EV powertrain demand. Consumers demonstrate high preference for connected infotainment, remote diagnostics, and subscription-based digital vehicle services.

How Are Safety Regulations Accelerating Intelligent Vehicle System Integration?

Europe accounts for nearly 27% of Automotive Electronics deployment, with Germany, the UK, and France leading system integration across passenger and premium vehicles. Strict safety frameworks and sustainability targets drive installation of electronic stability systems, lane-keeping technologies, and battery management modules. Over 80% of new vehicles incorporate advanced braking electronics. Electrified vehicle platforms and digital instrument clusters are widely adopted. A leading regional automotive technology firm is scaling zonal controller production to reduce wiring weight by 20%. Consumers prioritize safety-certified features, energy efficiency, and low-emission mobility solutions aligned with regulatory compliance expectations.

What Drives Large-Scale Electronics Manufacturing and EV Platform Innovation?

Asia-Pacific holds the highest production volume, contributing over 50 million vehicles annually, with China, Japan, and India serving as major consumption and manufacturing centers. The region leads in battery management systems, power modules, and semiconductor packaging capacity. Over 65% of global EV production originates here, strengthening demand for high-voltage electronics. Smart cockpit adoption and 5G-enabled vehicle connectivity are expanding rapidly. A regional electronics manufacturer increased automotive chip output by 30% to meet rising ADAS module demand. Consumers show strong adoption of connected infotainment, digital dashboards, and app-integrated vehicle services.

How Is Fleet Modernization Influencing Vehicle Electronics Demand?

Brazil and Argentina anchor regional demand, contributing nearly 4% of global Automotive Electronics installations. Telematics, fleet tracking modules, and electronic fuel management systems are key growth areas. Infrastructure modernization in logistics and public transport drives adoption of electronic braking and monitoring systems. Trade policies encouraging local vehicle assembly are supporting electronics integration. A domestic mobility solutions provider deployed smart fleet management systems across 5,000 commercial vehicles, improving fuel efficiency by 12%. Consumers emphasize cost-efficient connectivity features, navigation systems, and vehicle security electronics.

How Is Digital Transformation Supporting Connected Mobility Solutions?

This region accounts for roughly 2% of Automotive Electronics adoption, with the UAE and South Africa leading demand. Growth is linked to infrastructure expansion, logistics fleets, and smart city initiatives. Vehicle tracking, advanced navigation electronics, and in-vehicle connectivity systems are widely deployed in commercial segments. Import regulations and regional trade partnerships influence technology adoption. A regional technology integrator implemented connected fleet platforms covering 3,000 transport vehicles, enhancing route efficiency by 15%. Consumers prioritize durability, climate-adapted electronics, and navigation technologies suited to long-distance mobility.

China – 32% share in Automotive Electronics Market: High vehicle production volume, strong EV manufacturing base, and extensive semiconductor and power electronics capacity.

Germany – 18% share in Automotive Electronics Market: Advanced automotive engineering ecosystem, strong safety electronics integration, and premium vehicle digitalization leadership.

The Automotive Electronics market exhibits a moderately consolidated structure, with over 120 active global and regional competitors spanning semiconductor manufacturers, Tier-1 automotive suppliers, software platform providers, and power electronics specialists. The top five companies collectively account for approximately 52% of total market activity, reflecting strong scale advantages in R&D, manufacturing, and long-term OEM supply contracts. Leading firms invest between 8–12% of annual operating budgets into research and development, focusing on silicon carbide modules, AI-enabled ADAS processors, and centralized vehicle computing platforms.

Strategic partnerships between automakers and chipmakers have increased by more than 35% over the past three years, aimed at securing semiconductor supply and co-developing domain controllers. Mergers and acquisitions activity remains robust, particularly in cybersecurity, sensor fusion, and EV power module startups, with over 40 strategic deals recorded industry-wide in a two-year span. Product innovation cycles are shortening, with new automotive-grade chipsets launching every 18–24 months. Competitive differentiation increasingly depends on software integration capability, over-the-air update frameworks, and functional safety certifications. Vertical integration strategies, including in-house semiconductor design and battery electronics manufacturing, are strengthening supply chain resilience and reducing component lead times by nearly 20%.

Bosch

Continental AG

Denso Corporation

Aptiv PLC

ZF Friedrichshafen AG

Valeo

NXP Semiconductors

Infineon Technologies

Renesas Electronics

Texas Instruments

STMicroelectronics

Magna International

Panasonic Automotive

Samsung Harman

ON Semiconductor

The Automotive Electronics Market is being reshaped by rapid adoption of high-voltage power electronics, sensor fusion systems, and software-defined vehicle architectures. Advanced driver-assistance systems (ADAS) now integrate multiple radar, LiDAR, and camera modules, with over 85% of premium vehicles in 2025 equipped with at least three sensor types. Silicon carbide (SiC) and gallium nitride (GaN) power devices are increasingly deployed in electric vehicles, delivering 8–12% higher drivetrain efficiency and enabling inverter operation at voltages above 800V, while reducing thermal dissipation requirements by 15%.

Centralized and zonal electronic architectures are replacing traditional distributed ECU setups, reducing wiring complexity by up to 30% and vehicle weight by 10–15 kg per platform. This shift allows over-the-air (OTA) software updates in more than 60% of newly produced connected vehicles, improving diagnostic speed by 25% and reducing recall-related downtime by nearly 20%. AI-driven driver monitoring and predictive maintenance systems are processing over 5 trillion operations per second in modern cockpit modules, enhancing safety and in-vehicle user experience.

Infotainment systems are also evolving, with high-resolution displays, voice recognition, gesture controls, and cloud connectivity standardizing across 70% of passenger vehicles. Emerging trends include integration of Vehicle-to-Everything (V2X) communication, high-performance computing units for autonomous functions, and cybersecurity-focused hardware encryption modules. Collectively, these technological advancements are driving increased electronic content per vehicle, optimizing energy efficiency, and enabling seamless digital experiences for both consumers and commercial fleets.

• In Q3 2024, Bosch launched a new generation of central vehicle computers designed for advanced driver-assistance systems (ADAS) and automated driving, set for mass integration in production vehicles beginning in 2025, expanding high‑performance electronic control capabilities across multiple domains.

• In Q1 2025, Continental introduced a new line of high‑performance radar sensors aimed at urban mobility applications, marking a milestone with over 200 million radar sensors produced globally and strengthening its safety electronics portfolio for modern vehicles.

• In Q2 2025, ON Semiconductor announced a $600 million expansion of its Czech automotive chip manufacturing facility to increase capacity for EV and ADAS semiconductor components, supporting broader regional electronics supply chain growth.

• In September 2025, Qualcomm and BMW unveiled the Snapdragon Ride Pilot automated driving system in the BMW iX3, offering hands‑free highway driving, automatic lane changes, and parking assistance, validated for over 60 countries and signifying deeper chip‑to‑vehicle ecosystem integration.

The scope of the Automotive Electronics Market Report encompasses detailed segment analysis, covering core product types such as power electronics, safety and ADAS systems, infotainment and telematics modules, body electronics, and control units. It evaluates how increasing electronic content per vehicle, including multi‑sensor suites and centralized computing platforms, shapes system architecture decisions across OEMs and Tier‑1 suppliers. The geographic scope spans major regions—Asia Pacific, North America, Europe, South America, and the Middle East & Africa—analyzing regional production capacities, technology adoption patterns, and regulatory environments influencing electronics integration.

Application segments within the report include passenger vehicles, commercial fleets, urban mobility platforms, and autonomous prototypes, with insights into how feature adoption varies across sectors. Technology focus areas cover emerging and established innovations—such as silicon carbide power devices, wireless battery management systems, zonal E/E architectures, and V2X communications—illustrating how each impacts integration timelines and procurement priorities. The report also highlights niche and future market segments, including software‑defined vehicle platforms, AI‑enhanced driver monitoring, and cybersecurity‑embedded hardware, while assessing end‑user dynamics involving OEMs, Tier‑1 integrators, aftermarket services, and mobility service operators.

Evaluation metrics include production volume trends, semiconductor capacity expansions, sensor penetration rates, and infrastructure developments supporting electronics ecosystems. This comprehensive scope enables stakeholders to benchmark performance, prioritize technology investments, and align business strategies with evolving market requirements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch, Continental AG, Denso Corporation, Aptiv PLC, ZF Friedrichshafen AG, Valeo, NXP Semiconductors, Infineon Technologies, Renesas Electronics, Texas Instruments, STMicroelectronics, Magna International, Panasonic Automotive, Samsung Harman, ON Semiconductor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |