Reports

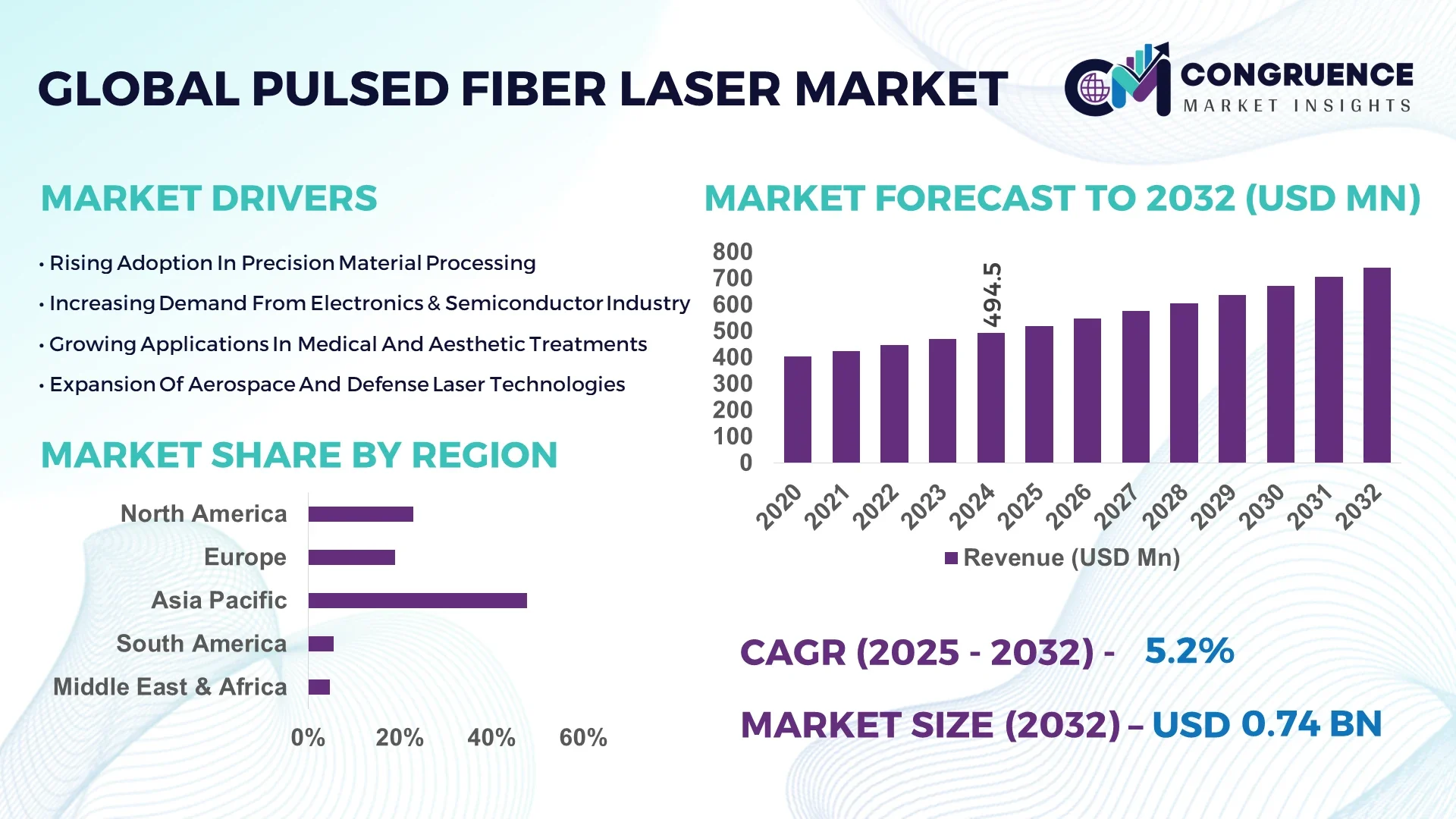

The Global Pulsed Fiber Laser Market was valued at USD 494.5 Million in 2024 and is anticipated to reach a value of USD 741.8 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032. Growth is driven by expanding applications across precision manufacturing, material processing, and medical device sectors.

China dominates the global marketplace with its large-scale production capacity exceeding 40,000 units annually, supported by government-led industrial modernization programs and rising adoption in automotive, electronics, and aerospace industries. Advanced facilities in Shenzhen and Wuhan continue to push innovation, with more than 35% of the country’s output directed toward international exports.

Market Size & Growth: Valued at USD 494.5 Million in 2024, projected to reach USD 741.8 Million by 2032, with a 5.2% CAGR fueled by automation and smart manufacturing adoption.

Top Growth Drivers: 38% adoption in precision cutting, 27% efficiency improvement in energy usage, 22% demand surge from automotive lightweighting initiatives.

Short-Term Forecast: By 2028, fiber laser systems are expected to cut processing costs by 18% and improve throughput by 24%.

Emerging Technologies: Integration of AI-driven control systems, ultrafast pulsed fiber lasers, and green laser modules for sustainability.

Regional Leaders: Asia Pacific projected at USD 320 Million by 2032 (driven by manufacturing), Europe at USD 210 Million (focus on aerospace), North America at USD 155 Million (adoption in medical device production).

Consumer/End-User Trends: Increasing adoption across automotive, aerospace, and medical device sectors, with >40% usage in metal processing.

Pilot or Case Example: In 2023, a German automotive OEM achieved a 26% reduction in downtime using pulsed fiber lasers in EV battery welding.

Competitive Landscape: IPG Photonics leads with approx. 36% share, followed by Trumpf, Coherent, Raycus, and nLight.

Regulatory & ESG Impact: Environmental standards driving 28% higher adoption of energy-efficient lasers; EU carbon reduction policies accelerating compliance needs.

Investment & Funding Patterns: Over USD 120 Million invested in 2023 into fiber laser R&D, with rising venture capital in laser-enabled medtech startups.

Innovation & Future Outlook: Hybrid lasers and integration into robotic automation systems are reshaping industrial production efficiency.

The Pulsed Fiber Laser Market is witnessing high adoption in automotive (34% share), electronics (29%), and aerospace (18%), with innovations such as ultrafast pulse modulation and AI-integrated monitoring. Regional variations highlight strong demand in Asia Pacific for electronics, while Europe prioritizes sustainability-driven laser technologies. Growing regulatory frameworks, advanced materials processing, and digitalization are positioning the market for a robust future trajectory.

The Pulsed Fiber Laser Market holds strategic relevance as a cornerstone of industrial modernization, delivering unmatched efficiency and precision in material processing. Comparative benchmarks show that next-generation ultrafast pulsed fiber lasers deliver 32% improvement in processing accuracy compared to conventional CO2 laser systems, lowering operational waste and improving throughput. Asia Pacific dominates in volume production, while Europe leads in adoption with 48% of enterprises integrating fiber laser technologies across aerospace and medical device manufacturing.

By 2027, AI-driven process optimization in fiber laser systems is expected to reduce energy consumption per unit by 21%, while predictive maintenance solutions will cut downtime by nearly 19%. Firms are also committing to ESG objectives, with major manufacturers targeting 35% energy efficiency gains and 20% carbon reduction by 2030. A key micro-scenario occurred in 2023 when a Japanese electronics company achieved a 27% improvement in yield rates through integration of pulsed fiber lasers in microelectronics assembly.

These measurable advancements highlight the dual role of pulsed fiber lasers in driving industrial competitiveness and supporting sustainability. Positioned at the intersection of digital transformation and green manufacturing, the Pulsed Fiber Laser Market stands as a pillar of resilience, compliance, and long-term growth for global industries.

The Pulsed Fiber Laser Market is shaped by evolving industrial demand, technological innovation, and sector-specific regulatory frameworks. Precision requirements in automotive lightweighting, semiconductor wafer processing, and aerospace component manufacturing are driving widespread adoption. Increasing investment in ultrafast and AI-assisted fiber laser solutions continues to redefine performance benchmarks across industries. Regional consumption patterns differ, with Asia Pacific emphasizing electronics, North America focusing on medical devices, and Europe prioritizing sustainable laser systems. At the same time, strong competition among global and regional players accelerates innovation, reshaping market dynamics through product differentiation and vertical-specific solutions.

The rise in high-precision manufacturing across industries is significantly fueling the Pulsed Fiber Laser Market. Automotive manufacturers increasingly rely on fiber lasers for welding thin materials, achieving dimensional accuracy within ±0.05 mm. Electronics companies use these lasers for micro-drilling and wafer cutting, enabling miniaturization trends in smartphones and wearable devices. In 2023 alone, nearly 42% of semiconductor production lines adopted fiber laser-based solutions, underscoring their critical role. Aerospace applications, including turbine blade drilling and lightweight composite processing, have also increased by 21% compared to traditional methods. This precision-driven adoption directly accelerates market growth.

Despite strong adoption trends, the Pulsed Fiber Laser Market faces challenges from high upfront capital costs. Advanced fiber laser systems require investments ranging from USD 150,000 to over USD 500,000 per unit, depending on power capacity and customization. For SMEs, this creates financial barriers and slower adoption rates. Maintenance costs, including consumables and calibration services, add an estimated 8–12% annually to operating expenses. Furthermore, the requirement for skilled operators and integration into existing production systems increases the overall expenditure burden. These cost constraints limit wider accessibility, particularly in emerging economies, and delay return on investment.

Medical device manufacturing presents a major opportunity for the Pulsed Fiber Laser Market due to the growing demand for minimally invasive surgical tools, implants, and diagnostic equipment. Precision cutting and welding capabilities are vital for stainless steel, titanium, and polymer-based medical devices. In 2024, over 28% of newly developed stents and catheters incorporated fiber laser processing. Moreover, regulatory pressure for biocompatibility and safety compliance drives manufacturers toward laser-enabled solutions. With healthcare expenditures rising globally, the integration of fiber lasers in medical device fabrication is expected to expand significantly, positioning this sector as a high-value growth driver.

Global supply chain disruptions present a critical challenge for the Pulsed Fiber Laser Market. The reliance on rare-earth elements, precision optics, and semiconductor-grade components exposes manufacturers to volatility in availability and pricing. In 2022, disruptions caused a 14% delay in delivery schedules across North America and Europe. Additionally, geopolitical tensions and trade restrictions impact cross-border component sourcing, slowing down production cycles. Limited domestic alternatives for critical raw materials further intensify supply vulnerabilities. As a result, many companies face higher procurement costs and extended lead times, which hinder scaling capabilities and restrain overall market expansion.

• Expansion in EV Battery Welding Applications: Pulsed fiber lasers are witnessing rising demand in electric vehicle battery assembly, with adoption increasing by 31% between 2022 and 2024. Manufacturers report up to 22% improvements in weld consistency and 18% reduction in material waste. This trend is strongest in Asia Pacific, where EV adoption surpasses 15 million units annually.

• Integration of AI in Laser Monitoring Systems: AI-driven monitoring solutions are rapidly being embedded into pulsed fiber lasers, enabling predictive maintenance and real-time optimization. Companies implementing AI monitoring reported a 25% reduction in downtime and 19% higher operational efficiency. By 2026, over 40% of installed fiber laser units are expected to feature integrated AI diagnostics.

• Rise in 3D Printing and Additive Manufacturing: Pulsed fiber lasers are increasingly utilized in 3D metal printing, with adoption growing 28% year-over-year. Precision in layer fusion improved by 17%, enhancing structural integrity in aerospace and medical implants. Europe leads this adoption, with 36% of industrial 3D printers using fiber laser-based systems.

• Growth in Surface Texturing for Medical Devices: Demand for surface modification of medical devices is expanding, with pulsed fiber lasers enabling micro-structuring at sub-micron levels. In 2023, 41% of orthopedic implant manufacturers integrated laser texturing into production lines, achieving a 29% improvement in implant osseointegration success rates. North America remains the leading adopter in this segment.

The AI in Investment Banking and Trading Services market is segmented across product types, applications, and end-user industries, each contributing distinctly to overall adoption trends. By type, solutions such as algorithmic trading platforms, risk management systems, portfolio optimization tools, and fraud detection solutions dominate, with algorithmic trading holding the largest adoption base due to high-frequency trading growth. Application areas extend to wealth management, compliance monitoring, and securities trading, with trading automation leading adoption because of its measurable impact on execution efficiency and cost reduction. End-user analysis highlights large financial institutions as the dominant group, accounting for a majority share due to early infrastructure investments, while fintech firms represent the fastest-growing segment as they leverage AI to offer differentiated services. Combined, niche users such as regulatory authorities and hedge funds also play an important role by driving demand for precision insights and advanced analytics.

In terms of type, algorithmic trading platforms currently account for 46% of adoption, establishing themselves as the leading segment due to their role in enabling high-frequency trading and rapid decision-making. Risk management systems follow with around 21% share, driven by the rising complexity of market volatility and regulatory compliance. Fraud detection and portfolio optimization tools collectively represent 18% of the share, while niche offerings such as AI-powered advisory assistants and natural language processing tools contribute the remaining 15%, catering to specialized use cases like client reporting and sentiment analysis. While algorithmic trading dominates, fraud detection solutions are expected to expand at the fastest rate, projected to grow at 13% CAGR, driven by escalating cyber threats and the increasing sophistication of fraudulent activities in digital banking. The comparative landscape shows algorithmic trading at 46%, risk management at 21%, portfolio optimization and fraud detection together at 18%, while emerging types collectively account for 15%.

According to a 2025 report by the Bank for International Settlements, AI-driven algorithmic trading systems were deployed by over 65% of global investment banks, significantly reducing latency and improving trade execution quality across equity and derivatives markets.

Trading automation currently accounts for 44% of application adoption, making it the largest segment, as institutions prioritize speed, reduced transaction costs, and minimal human error. Wealth management applications, at 23%, are growing steadily as firms integrate robo-advisory tools to deliver personalized portfolio recommendations. Compliance monitoring and fraud detection applications hold 21%, particularly relevant in meeting tightening regulatory requirements. Securities research and sentiment analysis tools collectively account for 12%, serving niche areas like market forecasting and investor insights. Compliance monitoring is the fastest-growing application, expected to expand at a CAGR of 12.8%, fueled by the rise of cross-border regulatory frameworks and the need for real-time reporting. Adoption trends further indicate that in 2024, over 52% of global trading desks reported integrating AI-powered models to improve execution speed, while 39% of wealth management firms incorporated robo-advisors into customer-facing platforms.

According to a 2024 report by the European Securities and Markets Authority, AI-based compliance systems were actively adopted by more than 200 financial institutions across Europe, reducing regulatory reporting errors by nearly 30% within a year.

Large financial institutions account for 49% of end-user adoption, maintaining their lead due to massive technology investments, sophisticated infrastructure, and early experimentation with AI-driven trading systems. Fintech firms follow with 28%, leveraging agile technology stacks to disrupt traditional banking models with faster, data-driven services. Asset management companies and hedge funds together contribute 15%, with strong reliance on AI for predictive analytics and portfolio optimization. Regulatory authorities and specialized market participants hold the remaining 8%, using AI for oversight and anomaly detection. Fintech firms represent the fastest-growing segment, with an adoption CAGR of 14.2%, driven by demand for low-cost, personalized, and mobile-first financial services. Statistics indicate that in 2024, 41% of fintech firms globally integrated AI into customer-facing trading platforms, while 35% of asset managers in the US reported adopting AI models for risk-adjusted portfolio optimization.

According to a 2025 Gartner report, AI adoption among fintech firms increased by 26% globally, enabling more than 600 companies to streamline digital advisory services and enhance cross-border trading capabilities.

Asia Pacific accounted for the largest market share at 47.71% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 11.6% between 2025 and 2032.

Asia Pacific generated the largest regional volume in 2024 with an estimated regional revenue base of several billion dollars and led in production density, manufacturing capacity, and installed units; China alone houses the majority of high-volume fiber laser OEMs, supplying large-volume CW and pulsed fiber laser modules and exporting components to Europe and North America. North America recorded strong demand from medical device and aerospace contract manufacturers with over 20% of global high-precision pulsed systems in operation across the U.S. and Canada. Europe maintained sizeable installed bases in automotive Tier-1 and aerospace applications, with German and French firms accounting for double-digit percentages of regional consumption. South America and Middle East & Africa contributed single-digit shares but showed double-digit year-on-year increases in procurement orders for repair, maintenance, and small-scale manufacturing lines.

How Are Advanced Manufacturing Needs Shaping Regional Laser Demand?

North America accounted for roughly 23% of global pulsed fiber laser demand in 2024, with volume use concentrated in medical device fabrication, aerospace component machining, and precision microelectronics. Key industries driving demand include medical device manufacturing (catheters, stents, implants), aerospace (turbine components, composite drilling), and advanced automotive (EV component welding). Regulatory and standards updates for medical device traceability and manufacturing quality have encouraged capital expenditure on laser-based microprocessing systems and ISO-compliant automation lines. Technological advances include increased deployment of MOPA pulsed architectures, integrated AI process control, and fiber-delivery micro-optics for sub-micron precision. Local players and integrators are expanding service footprints—OEMs and systems integrators in the U.S. are bundling fiber laser sources with robotic welding cells and inline quality inspection to reduce cycle times by double-digit percentages. Regional buyer behaviour skews toward certified, service-backed systems with lifecycle support; enterprises in healthcare and aerospace show higher enterprise adoption and stricter validation requirements compared with other sectors.

Why Is Regulatory Rigor Driving Demand For Explainable Laser Processes?

Europe represented about 19–22% of global pulsed fiber laser consumption in 2024, with Germany, the UK, and France as the leading national markets. Regulatory bodies and sustainability initiatives (product safety directives, waste reduction targets, and energy-efficiency standards) have pushed OEMs and end-users toward energy-efficient pulsed fiber lasers and traceable process control. Adoption of ultrafast lasers and closed-loop process monitoring is rising; over 40% of advanced aerospace suppliers integrated inline laser monitoring for traceability in 2024. Emerging technologies such as kilowatt-class ultrashort pulse sources and hybrid laser-plus-robot workcells are being piloted across metal additive and precision welding lines. A notable European OEM introduced automated punch-laser and bevel-capable cutting solutions during 2024 to enhance downstream welding prep and reduce secondary operations. Consumer behavior in Europe emphasizes explainability, sustainability, and regulatory-compliant documentation for laser-processed parts.

How Are Manufacturing Hubs And Innovation Clusters Accelerating Laser Adoption?

Asia-Pacific remained the largest-volume region in 2024 and ranks first by installed base and manufacturing throughput. Top consuming countries include China, Japan, and India, with China hosting a dense OEM ecosystem for both CW and pulsed fiber laser sources and associated modules. Manufacturing trends show heavy integration of fiber lasers into electronics assembly, EV battery welding and motor component fabrication; over half of regional metal fabrication facilities reported using fiber laser modules in at least one production cell in 2024. Regional tech hubs—Shenzhen, Wuhan, Seoul, and Singapore—drive rapid productization and cost reductions, enabling broader SME uptake via lower-cost domestic laser sources and bundled automation. Local manufacturers are increasingly shipping high-volume MOPA and QCW pulsed modules; some Chinese suppliers reported annualized unit shipments in the tens of thousands for lower-power pulsed sources in 2024. Buyer behavior here skews toward mobile-first procurement, rapid deployment, and strong price-performance sensitivity, supporting higher volumes of lower-cost pulsed systems.

What Role Do Infrastructure And Energy Projects Play In Regional Laser Demand?

South America accounted for around 5–7% of global pulsed fiber laser demand in 2024, led by Brazil and Argentina. Market uptake focuses on heavy industry maintenance, energy sector component repair, and localized manufacturing for agricultural machinery and automotive parts. Infrastructure and energy modernization programs have increased demand for laser cleaning, cladding, and welding solutions to refurbish components and extend asset life. Government incentives in several countries have supported technology importation and domestic training programs, improving system availability. Local integrators in Brazil have applied pulsed fiber lasers to remanufacturing and precision repair use cases, enhancing turnaround times by substantial margins compared with manual methods. Regional consumer behaviour favors durable machines with localized service and language-specific documentation; demand is often tied to project cycles and public works procurement schedules.

Why Are Diversified Investments And Modernization Fueling Regional Adoption?

Middle East & Africa constituted roughly 6–8% of global pulsed fiber laser consumption in 2024, with the UAE, Saudi Arabia, and South Africa registering the largest procurements. Regional demand is driven by oil & gas equipment maintenance, shipbuilding, and construction component manufacturing, alongside sovereign wealth–backed diversification projects that fund advanced manufacturing adoption. Technological modernization trends include the integration of automated laser cutting and welding lines into fabrication yards and the trial of fiber laser cleaning systems for corrosion remediation. Trade partnerships and regulatory frameworks encouraging localized production have spurred equipment imports and JV activity. Local players in the UAE and South Africa are piloting laser-enabled fabrication cells for high-precision parts, and consumer behaviour shows interest in turnkey solutions with bundled training and uptime guarantees.

China – 31% market share

Dominance driven by high production capacity, dense OEM ecosystem, and rapid domestic adoption across electronics, automotive, and energy sectors.

United States – 24% market share

Strong end-user demand in medical devices, aerospace, and high-precision manufacturing supported by advanced R&D and systems integration capacity.

The Pulsed Fiber Laser market combines large global incumbents and numerous regional specialists, resulting in a competitive landscape that is moderately consolidated at the high-power end and fragmented at lower-power, price-sensitive tiers. Approximately 40–60 companies actively compete across source manufacturing, system integration, optics and beam-delivery, and value-added automation. The top five players—led by a major vertically-integrated U.S. supplier—represent roughly one-third to two-fifths of value at the higher-power pulsed segment, while dozens of regional firms in China, Europe, and North America supply lower-power pulsed modules and specialty MOPA units. Strategic initiatives include product launches of ultrafast pulsed modules, partnerships between source suppliers and robot integrators, localized production investments, and targeted acquisitions to secure optics and fiber component supply. Innovation trends shaping competition include MOPA architecture improvements, QCW and nanosecond pulsed tuning, AI-driven process control, and bundled robotic workcells. Key market facts: more than 70% of laser OEM R&D spend focuses on pulse shaping and beam quality; several firms reported single-year shipment increases in lower-power pulsed sources above 20% in 2023–2024; and service & aftermarket contracts account for an increasing share of long-term vendor revenue. These dynamics create room for scale advantages at the high end, while price and service differentiation determine competitiveness in lower-power and emerging markets.

Wuhan Raycus Fiber Laser Technologies

JPT (Shenzhen JPT Electronics)

Han’s Laser Technology Industry Group

Max Photonics

Keopsys

Coherent/II-VI

Han's Laser Group

Pulsed fiber laser technology is evolving along several technical axes—pulse architecture, peak power scaling, beam quality, and digital process control—each delivering discrete industrial benefits. MOPA (Master Oscillator Power Amplifier) pulsed configurations provide tunable pulse width and repetition rate, enabling process flexibility for marking, micro-drilling, and thin-sheet welding; these architectures now dominate many pulsed use cases because they allow independent control over pulse energy and frequency. Ultrafast pulsed (picosecond/femtosecond) fiber sources are expanding into micro-machining and semiconductor device structuring, offering sub-micron feature control and minimal heat-affected zones. QCW and nanosecond pulsed solutions remain widely used for battery tab welding, precision cleaning, and marking due to effective energy delivery and throughput balance. Beam-delivery advances—fiber-coupled optics, dynamic focus heads, and coaxial vision systems—improved in-field uptime and reduced integration complexity; more than half of new installations in 2023–2024 featured integrated beam delivery and process monitoring. AI and edge analytics are increasingly embedded in laser controllers for real-time adaptive control, predictive maintenance, and automated process parameter optimization, reducing scrap and rework. Optical fiber developments (polarization-maintaining and large-mode-area fibers) yield higher peak powers and improved beam quality, enabling kilowatt-range pulsed experiments for novel welding and additive workflows. Concurrently, materials and coating advances (for optics and fiber ends) extend mean time between failures, lowering lifetime service costs. Taken together, these technologies are enabling broader deployment of pulsed fiber lasers across automotive EV battery assembly, high-precision electronics, medical device fabrication, and advanced additive manufacturing—shifting competition toward integrated systems suppliers who can deliver both lasers and turnkey automation.

• In March 2023, IPG Photonics reported a restructuring of its pulsed laser portfolio and noted material shifts in demand across solar-cell and foil-cutting applications, with pulsed laser sales declining in the period while R&D continued on UV and micro-machining sources. Source: www.ipgphotonics.com

• In September 2024, TRUMPF launched a fully automated punch-laser combination machine for the North American market, integrating laser capability with automated material flow to boost productivity and reduce energy consumption. Source: www.trumpf.com

• In August 2024, JPT introduced its M7 series MOPA high-power fiber laser platform, emphasizing flexible pulse shaping and direct-modulation seed sources for industrial marking, welding, and precision cleaning applications. Source: en.jptoe.com

• In 2024, industry analyses noted that fiber lasers (including pulsed variants) accounted for roughly half of laser technologies used in EV battery welding systems, with notable cost-per-watt reductions over the prior five years enabling wider deployment. Source: www.mobilityforesights.com

This report covers the global pulsed fiber laser market across product types, application domains, end-user industries, and geographies. Product-type analysis includes MOPA pulsed fiber lasers, QCW pulsed systems, nanosecond/picosecond ultrafast pulsed sources, and beam-delivery subsystems. Application coverage spans precision welding (EV batteries, motor components), micro-drilling and cutting (electronics and MEMS), marking and engraving, surface texturing (medical implants), additive manufacturing (metal 3D printing), and laser cleaning/cladding for maintenance. End-user segments examined include automotive OEMs and Tier-1 suppliers, electronics and semiconductor manufacturers, medical device companies, aerospace and defense contractors, energy and shipbuilding yards, and contract manufacturing. Geographic scope spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa with country-level insights for leading markets such as China, the United States, Germany, Japan, Brazil, and the UAE. The report also assesses technology readiness (pulse architectures, beam-delivery, AI process control), aftermarket service models, supplier consolidation trends, and capital equipment procurement patterns. Finally, the scope includes emerging niche segments—portable pulsed laser cleaners, UV pulsed sources for micro-machining, and laser-enabled battery assembly cells—alongside practical buyer considerations such as total cost of ownership, integration lead times, and service-network availability to support procurement and investment decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 494.5 Million |

| Market Revenue (2032) | USD 741.8 Million |

| CAGR (2025–2032) | 5.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | IPG Photonics Corporation, Coherent, Inc., TRUMPF GmbH + Co. KG, nLIGHT, Inc., SPI Lasers (a member of the TRUMPF Group), Wuhan Raycus Fiber Laser Technologies Co., Ltd., Han’s Laser Technology Industry Group Co., Ltd., Maxphotonics Co., Ltd., Jenoptik AG, JPT Opto-Electronics Co., Ltd., Hypertherm Associates |

| Customization & Pricing | Available on Request (10% Customization is Free) |