Reports

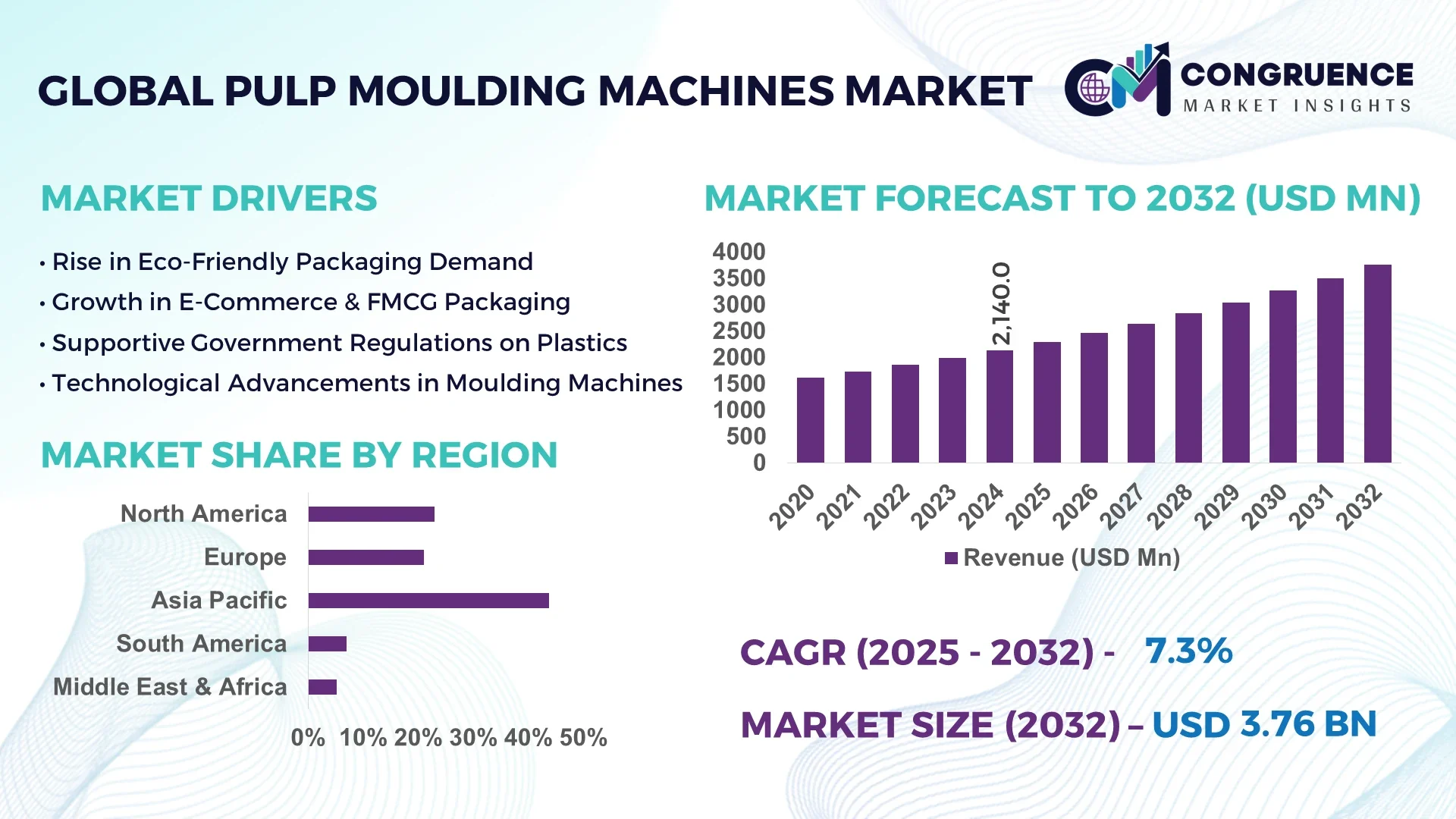

The Global Pulp Moulding Machines Market was valued at USD 2,140.0 Million in 2024 and is anticipated to reach a value of USD 3,760.2 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032.

China leads global activity with factory clusters capable of producing over 800 machines annually. Its top manufacturers have invested USD 150 million in expanding automated lines and high-speed rotary systems. In response to rising demand for food-grade and industrial packaging, Chinese manufacturers pioneered moisture-resistant pulp blends and real-time temperature control systems tailored for high-efficiency foodservice applications.

The Pulp Moulding Machines Market spans a range of industry sectors. Food and beverage packaging consumes approximately 45% of demand, with cup, tray, and bowl formats leading. Electronics and automotive protective packaging account for around 25%, while healthcare and cosmetic packaging drive another 15%. Technological innovations in the past year include precision-controlled rotary forming heads that reduce cycle time by 12%, integrated in-line infrared dryers that shorten drying by 30%, and modular 5-axis trim systems enabling rapid changeovers. Regulatory policies like single-use plastic bans in Europe and North America are accelerating plant upgrades—many manufacturers are installing VOC-free drying ovens and upgrading to biodegradable resin coatings. Consumption patterns are shifting regionally: APAC shows 10% annual volume growth driven by foodservice expansion, whereas North America leads in unit pricing due to higher machine automation and quality standards. Emerging trends point towards hybrid machines combining thermoforming and moulding, and expanded use of 3D-printed fibre molds. The future outlook positions the market for further mechanization, customization, and cross-sector adoption with rising environmental and efficiency demands.

AI is profoundly transforming the Pulp Moulding Machines Market across operational performance, quality control, and maintenance strategies. In production, AI-driven systems now adjust forming pressure and cycle timing in real time, minimizing rejects and stabilizing output. Machine vision cameras paired with AI image analysis detect surface defects—such as fiber voids or moisture spots—with over 98% accuracy, allowing immediate corrective adjustments. Predictive diagnostics based on vibration, motor current, and temperature sensors enable operators to flag maintenance needs two weeks in advance, reducing unplanned downtime by up to 25%.

Within manufacturing environments, AI-integrated human‑machine interfaces support rapid parameter changes when switching between product molds—saving technicians an average of 15 minutes per setup. These systems also log performance data continuously, generating detailed dashboards that benchmark efficiency across shifts and lines. As a result, facilities adopting AI-enhanced pulp moulding machines report up to a 20% increase in overall equipment effectiveness. AI is also enabling remote access and optimization: technicians can now troubleshoot form defects from centralized locations using cloud-based analytics, cutting response time by approximately 40%.

For decision-makers, this means the Pulp Moulding Machines Market is evolving toward intelligent production ecosystems: facilities with AI platforms demonstrate higher throughput, lower waste, enhanced product consistency, and measurable lifecycle cost savings—benefits that are quickly translating into competitive advantage for early adopters in the sector.

“In 2024, a leading OEM launched a Smart Moulding Suite combining AI-based vision and edge analytics; trial installations recorded a 22% drop in scrap rates and a 14-hour/month reduction in unscheduled stoppages.”

Growing global bans on single-use plastics—and increasing adoption of compostable packaging—have driven pulp moulding equipment demand. In 2024, pulp moulding output for foodservice rose by over 18% year-on-year, according to industry associations. Leading pulp moulding OEMs reported that 60% of new machine orders were for models compatible with biodegradable resin coatings. These drivers are enabling faster equipment sales cycles and higher automation standards focused on controlling moisture and forging fiber strength—aligning with sustainability targets across supply chains.

Raw material inputs—especially recycled paper pulp—exhibit price volatility up to ±15% over 12-month periods. This directly impacts operating margins, as many pulp moulding machines require specific fibre mix ratios. In 2024, several manufacturers delayed capital expenditures due to cost uncertainty. Additionally, seasonal swings in pulp availability—driven by recycling rates—resulted in 10–12% fluctuations in monthly production volumes. These constraints limit pricing flexibility and slow purchase cycles for new machinery.

Hybrid systems combining thermoforming and pulp moulding are gaining traction in sectors requiring structural rigidity with sustainable materials—such as consumer electronics and automotive packaging. Pilot installations in 2024 reported 25% faster product development cycles and 30% reduced tool changeover time. These hybrid platforms can switch between production modes within 90 seconds and enable manufacturers to consolidate two separate production lines into one. As customization and structural integrity needs grow, hybrid systems offer a compelling opportunity to migrate equipment portfolios to multifunctional platforms.

Tighter regulations—such as VOC emissions, food-contact safety, and energy efficiency standards—have forced upgrades on existing lines, ranging from USD 100,000 to USD 350,000 per machine. Many facilities, especially mid-tier players, face financial constraints. Compliance steps like installing VOC-free dryers, HEPA filters, and PLC upgrades add per-unit costs and require downtime averaging 10–14 days. These regulatory compliance costs slow replacement cycles and create barriers for smaller manufacturers, complicating the broader transition to next-generation pulp moulding systems.

Modular plant design and scalable footprint: Manufacturers are increasingly adopting modular pulp moulding machines that can be rearranged or expanded onsite. In 2024, modular units comprised 35% of new machine sales in Western Europe, facilitating faster line reconfigurations (under 48 hours) and aligning with agile production strategies.

Edge AI real-time monitoring: Edge AI modules installed on high-speed rotary moulders monitor cycle-by-cycle parameters. These systems detect deviations—like mold temperature drift—within milliseconds, reducing downtime by 18% and minimizing scrap by 12% in two-shift operations.

Energy-efficient drying systems: New in-line infrared and hybrid hot-air dryers combine rapid moisture removal with 25–30% lower energy consumption relative to traditional convection ovens. Installation grew by 28% in 2024 across North American facilities.

3D-printed mould tools for rapid prototyping: Adoption of additive manufacturing for fibre mould prototypes accelerated significantly. Companies deploying 3D‑printed mould inserts report a 40% reduction in lead time—from concept to trial production—supporting more responsive product development cycles.

The Pulp Moulding Machines Market is segmented based on type, application, and end-user industries, each playing a strategic role in shaping market dynamics. Types include rotary, reciprocating, and semi-automatic systems, addressing varied needs in terms of output volume, automation, and production scalability. Application segments span food packaging, industrial packaging, medical uses, and consumer goods. End-user segments include food and beverage manufacturers, electronics companies, healthcare suppliers, and sustainable packaging vendors. The segmentation reflects growing demand for environmentally safe packaging solutions, with food and beverage leading machine utilization, while electronics and healthcare packaging are emerging as high-growth niches. Increasing demand for automation, product customization, and regulatory compliance across industries is encouraging adoption of newer, more adaptive machine models. Regional deployment patterns also vary: while APAC leads in high-volume production for foodservice, Europe shows greater adoption of advanced machines in specialty packaging sectors.

Rotary pulp moulding machines dominate the market due to their high efficiency, capacity, and compatibility with continuous production environments. These machines are favored by large-scale producers for their ability to produce 2,000–7,000 units per hour and for their suitability in packaging formats such as trays and containers. They also offer modular upgrades and reduced labor dependency, making them cost-effective over longer cycles.

The fastest-growing type is semi-automatic pulp moulding machines. Their rise is attributed to increased adoption by small and medium-sized enterprises (SMEs) across developing regions. These machines balance operational control and affordability, offering an ideal entry point for businesses shifting from manual to mechanized production.

Reciprocating machines continue to hold relevance in applications requiring lower output volumes, such as niche food packaging and medical tray production. Their simplicity and low maintenance requirements make them attractive for small-batch manufacturing. Overall, machine type adoption aligns closely with end-use scale, automation needs, and regional investment trends.

Food and beverage packaging remains the leading application segment in the Pulp Moulding Machines Market, driven by surging demand for compostable packaging formats in takeout services, beverage carriers, and ready-to-eat product trays. Machines in this application are increasingly being integrated with coating systems for grease and moisture resistance, aligning with global food safety regulations.

The fastest-growing application area is industrial packaging, particularly in protective packaging for electronics, glassware, and automotive components. Growth in e-commerce logistics has accelerated the need for impact-resistant molded fibre packaging, propelling investments in custom mould design and high-strength fiber blends.

Other applications include medical device packaging, where sterile-grade molded trays are seeing demand, especially in hospital and diagnostics supply chains. Consumer product packaging—such as for cosmetics and personal care—is also expanding, driven by brand demand for plastic-free alternatives. Collectively, application diversity is prompting machine manufacturers to offer greater flexibility in mold customization, drying options, and material compatibility.

Food and beverage manufacturers are the leading end-user group, deploying pulp moulding machines at scale to produce biodegradable packaging alternatives for single-use plastic. These manufacturers often operate multi-line facilities, where machines are optimized for high-speed production, rapid tool changeovers, and certified food-grade output. Their adoption is supported by regulatory pressure and consumer demand for eco-friendly packaging.

The fastest-growing end-user group is the electronics industry, particularly companies involved in high-value or fragile component shipments. Pulp moulding machines are increasingly used to produce tailored inserts, impact-absorbing trays, and anti-static fiber-based packaging. Rising environmental mandates in tech product packaging are accelerating adoption of molded pulp over Styrofoam or plastic fillers.

Other key end-users include healthcare providers and pharmaceutical packaging companies, which require precision-molded trays with sterile properties. Cosmetic brands and personal care companies are also adopting pulp moulding machines to align with their sustainability goals, further contributing to market expansion through diversified demand sources.

Asia-Pacific accounted for the largest market share at 43.8% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to its high-volume manufacturing capacity, particularly in China and India, where food packaging demand is surging. Cost-effective labor and raw material availability further support production growth. Meanwhile, MEA is witnessing strong demand from emerging eco-packaging policies and rising investment in localized manufacturing units. Increasing awareness of sustainable alternatives and government initiatives aimed at reducing plastic dependence are acting as key catalysts for regional adoption.

North America held a market share of 21.5% in 2024, reflecting its strong position in the global pulp moulding machines industry. The region’s demand is primarily driven by the food and beverage sector, with major players shifting toward compostable and recyclable packaging options. Notable regulatory developments, such as statewide bans on Styrofoam and incentives for green packaging in California and New York, are accelerating investments in new machinery. Additionally, digital transformation is reshaping production efficiency, with U.S. facilities adopting AI-integrated moulding systems for real-time defect tracking and predictive maintenance. The growing focus on automation and regulatory compliance continues to solidify North America's leadership in value-added pulp moulding technologies.

Europe accounted for 18.2% of the global pulp moulding machines market in 2024, supported by key countries such as Germany, the UK, and France. The region's leadership in sustainability regulation—including EU-wide bans on single-use plastics and adoption of Extended Producer Responsibility (EPR) frameworks—has made pulp-based alternatives a priority. Organizations like the European Commission and national environment ministries are mandating biodegradable solutions, prompting manufacturers to invest in advanced machinery. European firms are also early adopters of smart moulding technologies, with German manufacturers incorporating edge computing and IoT-based monitoring in pulp forming lines. This trend strengthens the region’s commitment to eco-conscious production and premium machine standards.

The Asia-Pacific region dominates in terms of volume, producing over 48% of global pulp moulding machinery output in 2024. China, India, and Japan are top consumers, leveraging their manufacturing infrastructure to scale operations in both foodservice and industrial packaging sectors. China alone contributes to nearly 60% of Asia-Pacific’s total output due to expansive factory clusters and advanced automation integration. India is emerging rapidly, driven by local regulations phasing out plastic packaging and government subsidies for sustainable technology adoption. Innovation hubs in Japan and South Korea are exploring hybrid thermoforming-moulding platforms, enhancing production flexibility. The region’s low-cost advantage and growing domestic demand make it a cornerstone of global market growth.

In South America, Brazil and Argentina are spearheading regional pulp moulding machine adoption, with the region holding a market share of approximately 8.6% in 2024. These countries are witnessing growth in food processing and retail-ready packaging solutions, which is stimulating machinery investments. Local infrastructure improvements—especially in industrial parks and energy access—are encouraging modernization of legacy equipment. Brazil's regulatory momentum, with new compostability standards and import tax breaks for eco-friendly machinery, is catalyzing growth. Argentina is pushing forward with national sustainability frameworks that favor molded pulp in urban waste management. While the region’s growth is steady, increased focus on trade facilitation and automation is expected to further drive demand.

The Middle East & Africa region is gaining momentum, projected to be the fastest-growing market through 2032, albeit starting from a lower base. Countries like UAE and South Africa are leading regional demand, with the construction, foodservice, and packaging sectors increasingly turning to sustainable solutions. Dubai’s industrial sustainability roadmap and South Africa’s green packaging incentives are encouraging import and adoption of advanced pulp moulding machines. Infrastructure development across emerging markets is fostering demand for local manufacturing of trays and protective packaging. Digitally connected equipment and modular lines are gradually being introduced, particularly in UAE’s free zones. Regional trade partnerships with Asia and Europe are expected to enhance technology transfer and machine deployment.

China – 34.6% Market Share

China leads the Pulp Moulding Machines Market due to its massive manufacturing scale, competitive machine pricing, and dominance in global molded pulp packaging exports.

United States – 17.1% Market Share

The United States holds a strong position thanks to robust demand from foodservice and e-commerce packaging sectors, supported by state-level plastic bans and high automation adoption.

The competitive environment in the Pulp Moulding Machines Market is both diverse and dynamic, encompassing more than 120 active mid‑ and large‑scale equipment manufacturers worldwide. Roughly 30 multinational OEMs operate production hubs across Asia‑Pacific, Europe, and North America, supported by a wider tier of regional specialists and start‑ups focused on custom molds, in‑line dryers, and vision modules. Competitive positioning increasingly hinges on automation depth and energy efficiency: high‑speed rotary platforms (>6,000 cycles h⁻¹) and servo‑driven trim systems are now standard among top‑tier suppliers. Over the last two calendar years, the industry recorded 11 strategic acquisitions—most aimed at securing proprietary drying or AI‑inspection technology—and 9 cross‑border joint ventures to localize assembly in high‑growth markets such as India, Vietnam, and Mexico. Innovation intensity is rising: since 2023, OEMs have announced more than 60 product or software launches, including edge‑AI quality analytics, infrared/heat‑pump hybrid dryers, and hybrid thermoforming‑pulp lines. Strategic initiatives also include multi‑year R&D pacts with fiber‑material developers to commercialize moisture‑resistant pulp blends and government‑backed pilot plants designed to validate net‑zero production footprints. Collectively, these moves illustrate an industry competing on technology leadership, geographic reach, and sustainability credentials rather than on price alone.

Huhtamaki Oyj

Brødrene Hartmann A/S

BeSure Technology Co., Ltd.

Sodaltech

Beston Group Co., Ltd.

Far East Chung Ch’ien Group

DKM Machinery

UFP Technologies, Inc.

Inmaco BV

Southern Pulp Machinery

PulPac AB

QTM Technology

Maspack Limited

Technological progress in the Pulp Moulding Machines Market is shifting production lines toward high‑precision, data‑rich, and energy‑lean operations. Advanced rotary formers now integrate closed‑loop servo control that holds vacuum pressure within ±2 kPa, trimming defect rates below 1.5 %. Edge‑based AI modules analyze live camera feeds at up to 200 fps, flagging micro‑voids or moisture spots in under 120 ms; early adopters report scrap reductions of 18 – 22 %. Infrared/heat‑pump hybrid dryers achieve 25 – 30 % lower kilowatt‑hour consumption than legacy convection tunnels while shortening drying time by one‑third.

Modular “plug‑and‑play” stations enable capacity to be scaled from 3‑stack to 8‑stack forming heads without changing the base frame, cutting expansion downtime to 36 hours. In tooling, 3D‑printed composite molds withstand 500,000 cycles and decrease prototyping lead times by 40 %. Hybrid thermoforming‑pulp platforms—able to switch modes in <90 s—deliver internal part densities up to 650 kg m⁻³, meeting electronics and automotive protection standards.

Predictive maintenance is maturing: vibration and motor‑current sensors stream to cloud dashboards, and anomaly models trigger service alerts an average 14 days before failure, lifting overall equipment effectiveness by 5–7 percentage points. Connectivity follows OPC UA and MQTT protocols, allowing seamless link‑up with MES and carbon‑accounting systems. Looking ahead, vendors are bundling bio‑resin spray stations and low‑temperature plasma coating modules to open new applications in hot‑fill foodservice and medical disposables, underscoring a technology roadmap centered on efficiency, versatility, and sustainability.

• In June 2024 , Far East unveiled a fully automatic tableware line at Propak Asia capable of 18,000 plates h⁻¹ while consuming 28 % less energy than its predecessor, thanks to an integrated heat‑pump dryer and servo‑actuated trim stacker.

• In March 2024 , a newly granted U.S. patent introduced an AI‑driven vision system that inspects every molded pulp batch in real time; pilot plants recorded 97 % defect‑detection accuracy and a 22 % cut in scrap within three months of deployment.

• In November 2023 , BeSure Technology completed a 38,000 m² expansion in Foshan, China, lifting annual machine output to 300 units and adding an R&D center dedicated to AI process control and bio‑coating integration.

• In July 2023, Sodaltech launched a high‑speed egg‑tray machine rated at 20,000 cartons h⁻¹, pairing dual vacuum pumps with a regenerative heat‑exchange dryer that lowers steam consumption by 15 %.

This report offers an all‑encompassing examination of the Pulp Moulding Machines Market, spanning machinery types (rotary, reciprocating, hybrid, semi‑automatic, and manual), key modules (forming, drying, trimming, coating, and vision inspection), and capacity tiers from micro‑lines (<1,500 units h⁻¹) to mega‑lines (>7,000 units h⁻¹). Geographic coverage extends across five core regions—Asia‑Pacific, North America, Europe, South America, and Middle East & Africa—down to 15 high‑potential national markets. Application analysis dissects food and beverage packaging, industrial protective packaging, medical disposables, consumer goods, and specialty tableware, detailing machine adoption drivers, regulatory influences, and output benchmarks (e.g., cycle time, energy intensity, defect ratios).

Technology chapters explore automation architecture, AI/ML quality control, energy‑efficient drying, additive‑manufactured molds, and emerging bio‑coating upgrades. The competitive landscape section profiles seasoned OEMs, tier‑two innovators, and new entrants, mapping product portfolios, strategic alliances, and manufacturing footprints. Supply‑chain evaluations highlight pulp fibre sourcing, component standardization, and service support infrastructure. Additionally, the report tracks adjacent or niche segments such as dry‑molded fiber injection platforms and integrated thermoforming‑pulp systems, providing insight into convergence trends. Scenario analyses address regulatory trajectories, environmental mandates, and capital‑investment cycles, equipping decision‑makers with a clear, forward‑looking view of opportunities and risks across the global pulp moulding machinery ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Pulp Moulding Machines Market |

| Market Revenue (2024) | USD 2,140.0 Million |

| Market Revenue (2032) | USD 3,760.2 Million |

| CAGR (2025–2032) | 7.3 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Market Dynamics, Technological Trends, Segment Analysis, Regional Breakdown, Competitive Landscape, Strategic Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | Huhtamaki Oyj, Brødrene Hartmann A/S, BeSure Technology Co., Ltd., Sodaltech, Beston Group Co., Ltd., Far East Chung Ch’ien Group, DKM Machinery, UFP Technologies, Inc., Inmaco BV, Southern Pulp Machinery, PulPac AB, QTM Technology, Maspack Limited |

| Customization & Pricing | Available on Request (10 % Customization is Free) |