Reports

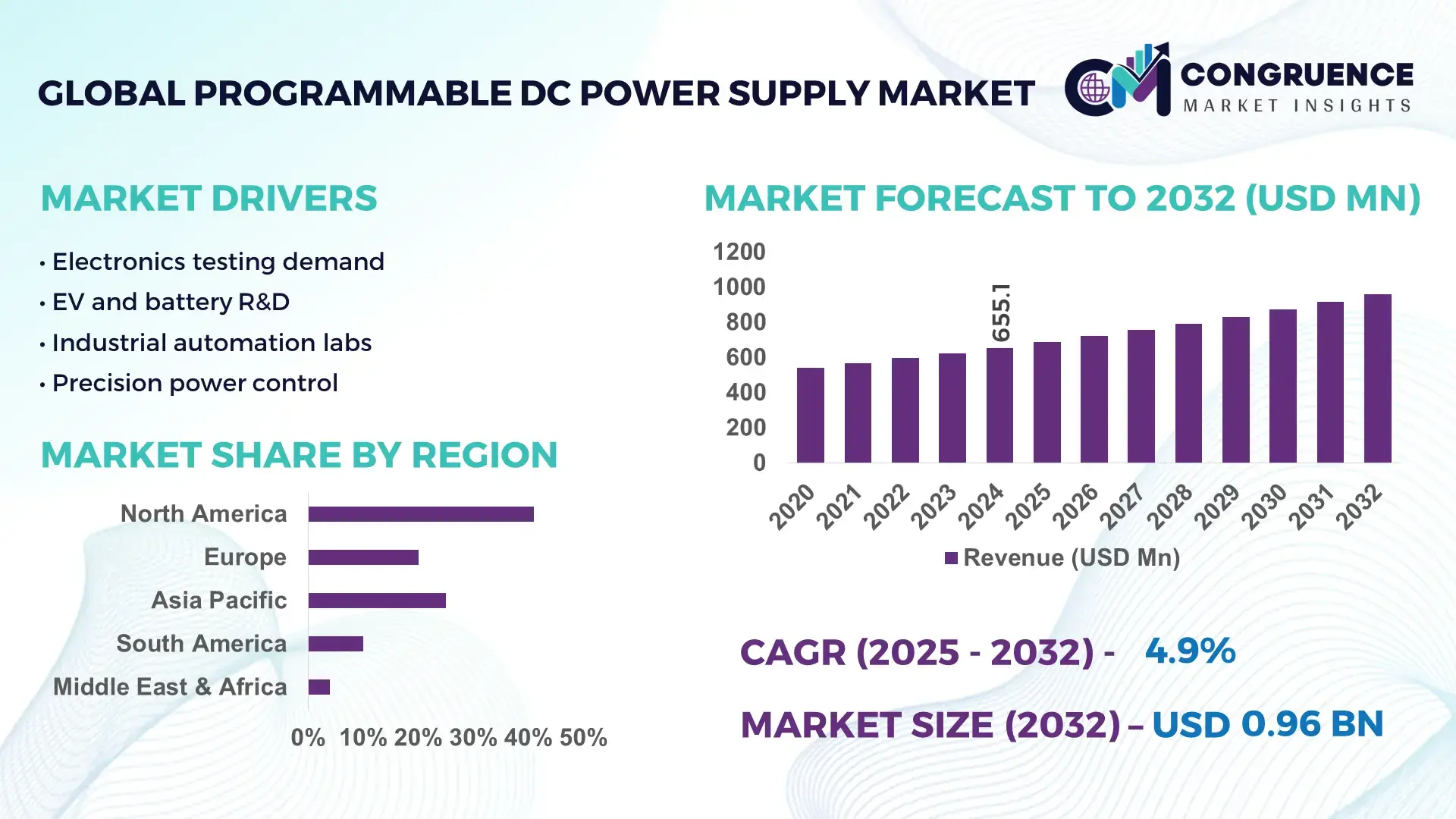

The Global Programmable DC Power Supply Market was valued at USD 655.06 Million in 2024 and is anticipated to reach a value of USD 960.48 Million by 2032 expanding at a CAGR of 4.9% between 2025 and 2032. Growth is driven by rising demand for precision power management across electronics manufacturing, automotive testing, and renewable energy systems.

China represents the dominant country in the programmable DC power supply landscape, supported by large-scale electronics manufacturing and sustained industrial investment. The country hosts over 30% of the world’s electronics production facilities and accounts for more than USD 50 billion in annual power electronics equipment output. Programmable DC power supplies are widely deployed across semiconductor fabs, EV battery testing lines, telecom infrastructure, and photovoltaic inverter testing. China’s annual investment in industrial automation exceeded USD 45 billion in 2024, accelerating adoption of digitally controlled, high-efficiency power supplies. Technological advancements such as wide-bandgap semiconductor integration (SiC and GaN) and Industry 4.0-compatible power systems have improved energy efficiency by over 15% and reduced equipment testing cycles by nearly 20%. Consumer adoption is particularly strong in coastal manufacturing hubs, with automated test equipment penetration exceeding 60% in advanced electronics facilities.

Market Size & Growth: USD 655.06 Million (2024) projected to USD 960.48 Million by 2032 at 4.9% CAGR, driven by increased electronic testing automation

Top Growth Drivers: EV testing adoption +28%, semiconductor equipment demand +22%, energy-efficient power conversion +18%

Short-Term Forecast: By 2028, average test system operating costs expected to decline by 12% due to higher efficiency supplies

Emerging Technologies: GaN-based power devices, digitally controlled multi-output supplies, IoT-enabled remote monitoring

Regional Leaders: Asia-Pacific USD 410 Million by 2032 with factory automation growth; North America USD 290 Million with aerospace testing demand; Europe USD 210 Million driven by renewable integration

Consumer/End-User Trends: Strong uptake among semiconductor fabs, EV OEMs, aerospace labs, and industrial automation integrators

Pilot or Case Example: 2024 EV battery testing pilot achieved 17% faster validation cycles using programmable DC systems

Competitive Landscape: Leader holding ~22% share, followed by AMETEK, Keysight Technologies, TDK-Lambda, Chroma ATE

Regulatory & ESG Impact: Energy efficiency mandates and low-harmonic standards accelerating replacement of legacy supplies

Investment & Funding Patterns: Over USD 1.6 Billion invested since 2023 in power electronics manufacturing expansion

Innovation & Future Outlook: Integration with digital twins, AI-assisted load simulation, and high-voltage modular platforms

The programmable DC power supply market serves critical sectors including semiconductors, automotive electronics, aerospace and defense, renewable energy, and industrial automation. Semiconductor manufacturing and testing account for approximately one-third of total demand due to stringent voltage accuracy and repeatability requirements. Recent innovations include high-density modular architectures, regenerative power supplies capable of energy recovery exceeding 90%, and advanced digital interfaces enabling real-time analytics. Regulatory pressure for energy efficiency, electrification policies, and capital expenditure recovery cycles are shaping procurement decisions. Asia-Pacific leads consumption due to dense manufacturing clusters, while North America and Europe show steady growth from aerospace testing and renewable grid integration. Emerging trends include higher-voltage EV test systems, bidirectional supplies for energy storage validation, and software-defined power platforms supporting future smart factories.

The Programmable DC Power Supply Market holds growing strategic relevance as global industries shift toward precision-driven electrification, automation, and digital validation ecosystems. These systems are foundational to electronics manufacturing, EV powertrain testing, aerospace qualification, and renewable energy validation, where voltage accuracy below ±0.01% and fast transient response times under 50 microseconds are operational requirements. From a strategic perspective, manufacturers increasingly deploy high-density, software-defined power platforms to reduce test cycle times by up to 20% while improving system uptime above 98%.

Wide-bandgap semiconductor-enabled power supplies deliver approximately 15% efficiency improvement compared to traditional silicon-based linear power supply standards, directly reducing thermal losses and facility energy consumption. Asia-Pacific dominates in volume due to large-scale electronics and EV manufacturing output, while North America leads in adoption with over 62% of enterprises integrating digitally programmable or remote-controlled power supplies into automated test environments.

By 2028, AI-enabled adaptive load simulation is expected to improve test throughput by 18% through predictive parameter tuning and automated fault isolation. From a compliance and ESG standpoint, firms are committing to energy intensity improvements such as 25% efficiency gains and 30% recyclable material usage in power electronics by 2030, aligning with industrial decarbonization mandates. In 2024, China achieved a 16% reduction in test energy consumption across EV battery validation lines through deployment of regenerative programmable DC power supplies. Looking ahead, the Programmable DC Power Supply Market is positioned as a core pillar supporting operational resilience, regulatory compliance, and sustainable industrial growth.

The expansion of electric vehicle and lithium-ion battery testing infrastructure is a primary growth driver for the Programmable DC Power Supply market. EV powertrain validation requires high-voltage supplies exceeding 1,000 V, fast current ramping, and regenerative capabilities that can recover up to 90% of discharged energy. Global EV production capacity surpassed 14 million units in 2024, significantly increasing demand for advanced battery cycling and inverter testing systems. Programmable DC power supplies enable precise simulation of charging, discharging, and fault conditions, reducing validation time by approximately 15–20%. Automotive OEMs and Tier-1 suppliers are also deploying multi-channel programmable systems to support parallel testing, improving lab utilization rates and accelerating product launch timelines.

High upfront investment and system complexity remain notable restraints within the Programmable DC Power Supply market. Advanced programmable units can cost two to three times more than conventional fixed-output power supplies, particularly when integrated with regenerative and digital control features. Small and mid-sized manufacturers often face budget constraints that delay upgrades, despite long-term efficiency benefits. Additionally, system integration requires skilled personnel capable of configuring communication protocols, safety interlocks, and software interfaces. In regions with limited technical workforce availability, deployment timelines can extend by several months, reducing short-term adoption. Maintenance and calibration requirements, often mandated annually in regulated industries, further increase operational burden and total cost of ownership.

The growth of renewable energy and grid-scale energy storage presents significant opportunities for the Programmable DC Power Supply market. Solar inverters, wind power converters, and stationary battery systems require rigorous validation under variable load and fault scenarios. Programmable DC power supplies enable accurate emulation of renewable generation profiles and grid disturbances, supporting compliance with evolving grid codes. Global installed energy storage capacity exceeded 180 GWh in 2024, driving demand for high-power bidirectional testing solutions. Regenerative programmable systems reduce test energy losses by up to 70%, making them attractive for utilities and EPC contractors focused on sustainability. This expanding application scope opens new demand channels beyond traditional electronics testing.

Supply chain volatility and regulatory fragmentation pose ongoing challenges for the Programmable DC Power Supply market. Critical components such as power semiconductors, precision sensors, and control ICs are subject to long lead times, sometimes exceeding 30 weeks, affecting production planning. At the same time, differing regional standards for safety, electromagnetic compatibility, and efficiency increase compliance complexity for manufacturers operating globally. Certification requirements across North America, Europe, and Asia often necessitate design modifications, increasing engineering costs and time-to-market. These factors place pressure on margins and complicate scaling strategies, particularly for suppliers attempting to serve multiple high-regulation industries simultaneously.

• Accelerated shift toward modular and prefabricated power system architectures: The adoption of modular and prefabricated design principles is reshaping demand patterns in the Programmable DC Power Supply market. Around 55% of newly deployed industrial test systems report measurable cost benefits through modular configurations, primarily due to reduced installation time and standardized components. Pre-configured power modules are assembled off-site using automated processes, cutting on-site integration effort by nearly 30% and reducing commissioning timelines by 20%. Demand for high-precision modular units is particularly strong in Europe and North America, where factory automation density exceeds 65% in advanced manufacturing facilities and rapid scalability is a procurement priority.

• Growing deployment of high-voltage and bidirectional programmable systems: Industrial electrification and EV battery validation are driving adoption of high-voltage programmable DC power supplies exceeding 1,000 V output capability. More than 40% of newly installed systems in automotive testing now require bidirectional energy flow to support regenerative operation. These systems enable up to 85–90% energy recovery during discharge cycles, lowering facility power consumption by approximately 18%. Adoption rates are highest in Asia-Pacific manufacturing hubs, where multi-channel bidirectional setups have improved test lab utilization by over 25%.

• Integration of digital control, connectivity, and software-defined power platforms: Digitally controlled programmable DC power supplies are becoming standard across electronics and aerospace testing environments. Over 60% of enterprise users now require Ethernet, CAN, or industrial IoT connectivity for remote configuration and monitoring. Software-defined platforms enable dynamic voltage profiling and automated test sequencing, reducing manual intervention by nearly 35%. Advanced analytics embedded in control software have improved fault detection accuracy by 22%, supporting higher uptime and more consistent compliance with test protocols.

• Rising emphasis on energy efficiency, compact design, and ESG alignment: Energy efficiency and physical footprint optimization are emerging as decisive procurement criteria. New-generation programmable DC power supplies deliver power density improvements of 20–25% compared to legacy rack systems, enabling space savings of up to 40% in test facilities. Manufacturers are also targeting environmental metrics, with recyclable material content in power electronics assemblies increasing beyond 30% in recent designs. Enterprises adopting energy-efficient programmable supplies report average reductions of 15% in test-related electricity usage, aligning operational performance with ESG-driven investment strategies.

The Programmable DC Power Supply market is segmented by type, application, and end-user, reflecting diverse performance requirements across precision testing, industrial automation, and electrification ecosystems. Product differentiation is driven by voltage range, output architecture, bidirectional capability, and control intelligence. Application segmentation highlights strong demand from electronics testing, EV powertrain validation, and renewable energy systems, while end-user segmentation underscores adoption disparities between large-scale manufacturers, research institutions, and infrastructure operators. Market behavior indicates increasing preference for flexible, software-defined solutions capable of supporting multiple test scenarios within a single platform. Across segments, purchasing decisions are influenced by accuracy thresholds, scalability, energy efficiency, and compliance alignment rather than basic output capacity alone.

The Programmable DC Power Supply market is primarily segmented into single-output programmable DC power supplies, multi-output programmable DC power supplies, and bidirectional/regenerative programmable DC power supplies. Single-output programmable DC power supplies currently account for approximately 44% of total adoption due to their widespread use in semiconductor testing, component validation, and laboratory environments requiring high accuracy and stability. Multi-output systems represent around 28% of adoption, favored in automated test equipment setups where space optimization and synchronized channel control are critical. However, bidirectional and regenerative programmable DC power supplies are the fastest-growing type, expanding at an estimated CAGR of 7.8%, driven by EV battery testing, energy storage validation, and grid-simulation applications. These advanced systems enable up to 90% energy recovery during discharge cycles, significantly lowering operational energy losses. Other niche types, including high-frequency compact bench-top units and ultra-high-voltage specialty systems, collectively contribute about 28% of the market, serving aerospace, defense, and research-grade applications.

By application, electronics and semiconductor testing leads the Programmable DC Power Supply market with roughly 38% adoption, supported by stringent voltage regulation requirements below ±0.01% and rising automation across fabs and OSAT facilities. Automotive and electric vehicle testing follows at about 27%, reflecting increasing validation needs for onboard chargers, inverters, and battery packs. Renewable energy and energy storage testing is the fastest-growing application segment, advancing at an estimated CAGR of 8.4%, driven by large-scale deployment of grid-connected storage exceeding 180 GWh globally. Aerospace and defense, telecommunications, and industrial equipment testing together account for approximately 35% of applications, relying on programmable supplies for compliance, stress testing, and lifecycle validation.

From an end-user perspective, manufacturing enterprises represent the largest segment, accounting for nearly 46% of market adoption, particularly in electronics, automotive, and industrial automation industries. Research institutions and testing laboratories follow with approximately 24%, driven by demand for high-precision, configurable platforms supporting experimental and compliance-driven testing. Utilities and energy infrastructure operators are the fastest-growing end-user group, expanding at an estimated CAGR of 8.9%, fueled by investments in grid-scale storage, hydrogen electrolysis systems, and power electronics validation. Other end-users—including aerospace agencies, defense contractors, and telecommunications operators—collectively contribute around 30% of demand, with adoption rates exceeding 55% in advanced aerospace test environments.

Asia-Pacific accounted for the largest market share at 41% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Asia-Pacific leadership is supported by high-volume electronics manufacturing, EV battery production, and industrial automation density, with over 65% of global electronics assembly capacity located in the region. North America’s accelerated growth is driven by advanced aerospace testing, EV R&D investment exceeding USD 90 billion annually, and rapid adoption of digitally programmable, regenerative power systems across laboratories and production lines. Europe held approximately 26% market share in 2024, influenced by sustainability-driven equipment upgrades and strict energy-efficiency regulations. South America and the Middle East & Africa together accounted for nearly 14%, supported by energy infrastructure modernization and industrial electrification initiatives. Across regions, demand is increasingly shaped by voltage precision requirements below ±0.01%, bidirectional energy recovery rates above 85%, and compliance with harmonic distortion thresholds under 5%.

How is advanced testing infrastructure accelerating adoption across high-value industries?

North America accounted for approximately 29% of the Programmable DC Power Supply market in 2024, driven by strong demand from aerospace, defense, automotive electrification, and semiconductor R&D. The region benefits from sustained government funding for clean energy and EV programs, alongside defense modernization initiatives that mandate high-precision, programmable testing environments. Regulatory emphasis on power quality, electromagnetic compatibility, and energy efficiency has accelerated replacement of legacy fixed-output systems. Digitally connected power supplies with remote monitoring are used by over 60% of large enterprises in this region. Local players are expanding regenerative and high-voltage product lines to support EV battery validation exceeding 800 V platforms. Regional consumer behavior shows higher enterprise adoption in aerospace, healthcare device testing, and financial data-center power validation, where uptime and traceability are critical.

Why is compliance-led modernization reshaping procurement priorities?

Europe represented nearly 26% of global market share in 2024, with Germany, the UK, and France accounting for more than 55% of regional demand. Strong regulatory oversight related to energy efficiency, harmonic emissions, and sustainability has driven rapid adoption of programmable DC power supplies capable of real-time monitoring and reporting. Sustainability initiatives targeting 20–30% reductions in industrial energy intensity have increased demand for regenerative systems. Emerging technologies such as wide-bandgap semiconductors and compact high-density racks are widely adopted across European test labs. Regional manufacturers are focusing on modular platforms aligned with circular economy principles. Consumer behavior reflects regulatory pressure, leading to preference for transparent, auditable, and software-driven programmable DC power supply solutions.

How does manufacturing scale translate into sustained equipment demand?

Asia-Pacific ranked first globally by volume, accounting for approximately 41% of total demand in 2024. China, Japan, and South Korea collectively contribute over 70% of regional consumption, supported by dense semiconductor fabs, EV battery plants, and electronics assembly lines. Manufacturing automation penetration exceeds 60% in advanced facilities, driving continuous upgrades to programmable power systems. Innovation hubs are increasingly adopting bidirectional supplies for energy recovery, reducing test energy losses by up to 18%. Local suppliers are expanding high-channel-count systems for parallel testing environments. Consumer behavior varies widely, with adoption driven by large-scale production efficiency, fast commissioning, and integration with digital factory platforms across automotive and electronics sectors.

What role does energy and industrial modernization play in shaping demand?

South America accounted for approximately 9% of global market share in 2024, led by Brazil and Argentina. Growth is closely linked to energy infrastructure upgrades, industrial automation investments, and renewable power expansion. Government incentives supporting local manufacturing and import substitution have increased demand for flexible programmable power systems in testing and certification labs. Industrial electrification projects are driving adoption of mid-voltage programmable supplies for power electronics validation. Regional suppliers are focusing on cost-optimized, ruggedized solutions suitable for variable grid conditions. Consumer behavior reflects higher sensitivity to total cost of ownership, with preference for durable systems capable of operating in diverse industrial environments.

How is industrial diversification driving precision power adoption?

The Middle East & Africa region represented around 5% of global demand in 2024, with the UAE and South Africa emerging as key growth markets. Demand is supported by oil & gas electrification, utility-scale renewable projects, and industrial diversification strategies. Technological modernization programs emphasize digital testing infrastructure, increasing adoption of programmable DC power supplies with remote diagnostics. Trade partnerships and industrial localization initiatives are improving access to advanced power electronics. Local integrators are deploying programmable systems in energy storage and grid simulation labs. Consumer behavior shows rising demand for robust, high-reliability equipment capable of operating under extreme environmental conditions.

China – 28% market share: Dominance driven by extensive electronics manufacturing capacity, EV battery production scale, and industrial automation density.

United States – 21% market share: Leadership supported by strong aerospace, defense, semiconductor R&D demand, and rapid adoption of digitally programmable testing systems.

The Programmable DC Power Supply market exhibits a moderately fragmented competitive structure, characterized by the presence of more than 45 active manufacturers globally, ranging from specialized power electronics firms to diversified test and measurement companies. The top five companies collectively account for approximately 55–58% of total market share, reflecting strong brand positioning, global distribution networks, and deep integration with automated test equipment ecosystems. Competition is primarily shaped by product precision, voltage scalability beyond 1,000 V, bidirectional energy recovery rates exceeding 85%, and software-defined control capabilities.

Strategic initiatives increasingly focus on new product launches, with over 30% of vendors introducing modular or regenerative platforms since 2023 to address EV battery and energy storage testing demand. Partnerships between power supply manufacturers and industrial automation or semiconductor equipment firms have risen by nearly 20%, enabling tighter hardware–software integration. Innovation trends include higher power density improvements of 20–25%, AI-assisted diagnostics, and digital twin-enabled testing environments. Mergers and selective acquisitions remain limited but targeted, mainly aimed at expanding regional service coverage and enhancing wide-bandgap semiconductor expertise. Competitive differentiation is shifting from standalone hardware performance toward lifecycle efficiency, software compatibility, and compliance-readiness.

AMETEK Programmable Power

Keysight Technologies

TDK-Lambda

Chroma ATE

Rohde & Schwarz

Kikusui Electronics

EA Elektro-Automatik

ITECH Electronic

B&K Precision

Matsusada Precision

The Programmable DC Power Supply market is undergoing significant technological evolution, driven by the increasing complexity of industrial, automotive, and renewable energy testing environments. Current systems are integrating digitally controlled multi-channel outputs, enabling up to 16 simultaneous voltage and current profiles within a single rack, which reduces laboratory footprint by 30–40% while maintaining high accuracy below ±0.01%. The integration of wide-bandgap semiconductor devices, including SiC and GaN transistors, has improved efficiency by approximately 15–20% and enabled higher switching frequencies, enhancing power density in both bench-top and modular systems.

Emerging trends include bidirectional and regenerative power supplies, which can recover up to 90% of energy during EV battery and energy storage testing, significantly lowering operational energy costs. Software-defined platforms are becoming standard, allowing remote monitoring, automated test sequencing, and dynamic load simulation for complex validation scenarios. These platforms also support IoT connectivity, Ethernet, CAN, and Modbus protocols, enabling predictive diagnostics, fault detection improvements of over 20%, and seamless integration into Industry 4.0 smart factory environments.

Further technological advancements focus on AI-assisted adaptive load testing, which optimizes voltage and current profiles in real time, reducing test cycle times by up to 18%. Compact high-voltage solutions exceeding 1,000 V output are increasingly deployed in aerospace, EV, and semiconductor R&D. Additionally, innovation in regenerative modular architectures and digital twin-enabled simulation is enabling decision-makers to accelerate product validation while improving energy efficiency and traceability, positioning programmable DC power supplies as essential tools in advanced industrial ecosystems.

• In February 2024, Magna-Power Electronics unveiled its 500 kW and 1,000 kW ML Series programmable DC power supplies at Applied Power Electronics Conference, featuring advanced water-cooling and enhanced power density with configurations up to 6,000 Vdc and 5,000 Adc per unit. (Magna-Power)

• In early 2024, CHROMA ATE Inc expanded its programmable DC power supply portfolio by integrating bidirectional current capability, enabling approximately 45% energy recovery during discharge phases, particularly in EV battery and powertrain R&D lab test benches.

• In 2023, EA Elektro-Automatik introduced a new 3U high-density rack-mount programmable DC series, delivering up to 30% more power output within the same footprint and widespread adoption among industrial automation and electronics manufacturing clients.

• During 2023, TDK-Lambda rolled out an advanced software interface with remote diagnostics for its programmable DC platforms, enabling remote firmware updates and reducing large test facility downtime by around 22%, with a strong portion of its installed base transitioning to the updated system.

The scope of the Programmable DC Power Supply Market Report encompasses a comprehensive analysis of the global landscape, detailing segmentation by product types, application domains, and end-user industries. The report’s breadth includes single-output, multi-output, and bidirectional/regenerative programmable DC power supplies, with insights into performance differentiation based on voltage range, control precision, and output versatility. The geographic focus spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing regional deployment trends, infrastructure particulars, and industry-specific demand drivers across manufacturing, research, energy storage, and automotive electrification sectors.

Application coverage examines critical use cases including automotive and EV battery testing, semiconductor validation, renewable energy systems validation, aerospace and defense certification labs, and industrial automation, with measured adoption metrics reflecting precise voltage regulation requirements and advanced communication interface integration. Emerging and niche segments such as modular multi-channel systems, regenerative high-power platforms, and IoT-enabled remote monitoring solutions are also explored, offering nuanced perspectives on how technology trends influence procurement strategies and operational efficiency.

The report further profiles the competitive environment, innovation trends, and technological enablers such as digital control algorithms, industrial protocol connectivity, and high-efficiency wide-bandgap semiconductors, highlighting enhancements in energy recovery, accuracy thresholds below ±0.01%, and adaptive load simulation capabilities. Industry focus areas detail regulatory compliance drivers, product lifecycle considerations, and strategic decision levers for key stakeholders including OEMs, test labs, and system integrators. Overall, the report delivers actionable insights tailored for decision-makers seeking depth on market segmentation, technological evolution, and strategic dynamics shaping the global Programmable DC Power Supply ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 655.06 Million |

Market Revenue in 2032 | USD 960.48 Million |

CAGR (2025 - 2032) | 4.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | AMETEK Programmable Power, Keysight Technologies, TDK-Lambda, Chroma ATE, Rohde & Schwarz, Kikusui Electronics, EA Elektro-Automatik, ITECH Electronic, B&K Precision, Matsusada Precision |

Customization & Pricing | Available on Request (10% Customization is Free) |