Reports

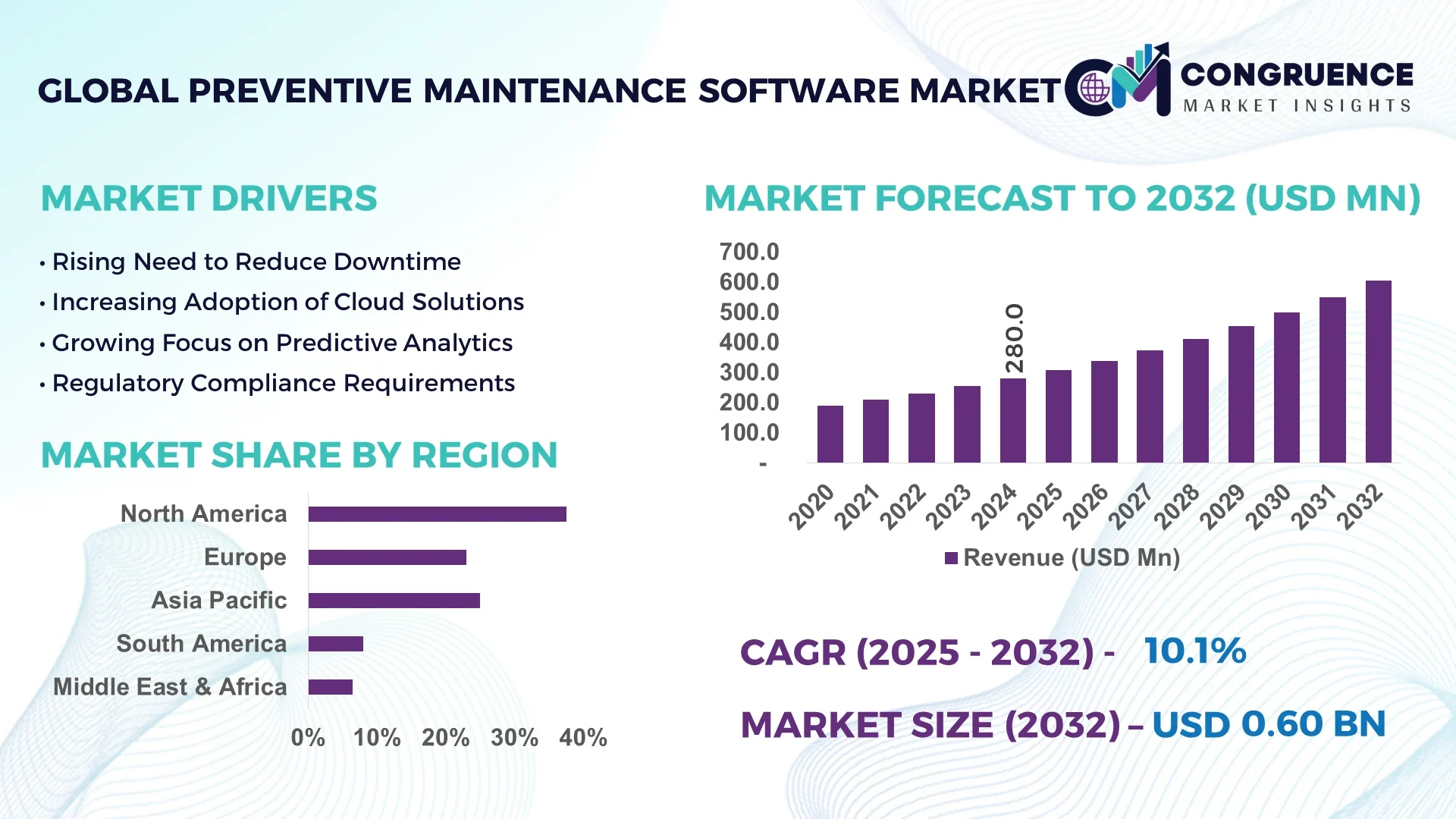

The Global Preventive Maintenance Software Market was valued at USD 280.0 Million in 2024 and is anticipated to reach a value of USD 604.6 Million by 2032 expanding at a CAGR of 10.1% between 2025 and 2032.

Unique information about the dominant country (United States) in the Preventive Maintenance Software Market:

The United States hosts multiple large-scale preventive maintenance software development centres with high investment in edge-computing platforms. It also supports advanced industry applications in aerospace, heavy manufacturing, and logistics. Leading providers maintain large-scale production capacity of enterprise-grade modules, backed by continuous R&D efforts in AI-enabled diagnostics, IoT integration, and automated scheduling technologies.

The Preventive Maintenance Software Market is strongly embedded across key industry sectors including manufacturing, energy & utilities, transportation, oil & gas, and healthcare. In manufacturing, software modules for vibration analysis, oil sampling and infrared thermography contribute significant share. Energy & utilities leverage temperature and motor circuit monitoring tools. Transportation firms invest in automated scheduling and IoT sensor integration for fleets. Recent technological innovations include digital-twin models for real-time asset simulation, explainable AI layers for predictive diagnostics, and cloud-native platforms enabling better cross-site coordination. Regulatory and environmental drivers—such as equipment safety standards, emissions controls, and mandated inspection intervals—are boosting adoption. Regional consumption patterns vary: North America and Western Europe show mature enterprise deployments, while Asia-Pacific markets are growing rapidly with infrastructure spending. Growth factors include rising asset aging, labor shortages driving automation, and the push for reliability-based maintenance. Emerging trends include convergence of predictive and prescriptive maintenance, integration with enterprise asset management systems, and growing demand for mobile and no-code deployment capabilities. Future outlook suggests continued adoption in critical infrastructure segments, expansion into SMEs through packaged cloud offerings, and expansion of industry-specific modules.

AI is fundamentally enhancing the capabilities of the Preventive Maintenance Software Market by enabling systems to process vast volumes of real-time sensor, production, and historical maintenance data to detect subtle anomalies in equipment performance. As a result, software within this market is shifting from rule-based scheduling to dynamic, data-driven maintenance workflows that prioritize interventions based on predictive risk.

Within the transportation segment, AI-powered platforms now analyze telemetry from thousands of assets hourly, identifying patterns that human operators would typically miss. In industrial and manufacturing environments, integration of explainable AI modules delivers actionable insights directly within dashboards, reducing diagnostic uncertainty and enabling more proactive maintenance decisions.

Improvements in efficiency are evident: AI-enhanced preventive maintenance software platforms are reducing unplanned downtime by 30–50%, significantly improving operational uptime, throughput, and maintenance team productivity. Manufacturing enterprises report up to 23% annual reduction in maintenance service costs by deploying AI algorithms that filter false positives and recommend precise corrective actions.

Further, facilities using AI-enabled scheduling modules benefit from resource optimization: maintenance teams can allocate labor and spare parts more efficiently, reducing unnecessary inspections and addressing faults before they escalate. In logistics, AI systems feeding from telematics devices collect hundreds of millions of data points per day, enabling freight and fleet operators to minimize downtime and proactively schedule servicing, significantly enhancing utilization rates.

Technological innovations such as AI-augmented chat assistants and prescriptive guidance modules now support technicians in selecting correct maintenance actions faster. Natural language interfaces built on large language models let teams query assigned tasks, asset manuals, and failure histories via simple prompts, improving responsiveness in maintenance cycles.

In digital asset-intensive industries, advanced AI frameworks are enabling predictive fault detection, root-cause analysis, and mobile delivery of maintenance instructions in real time. This transformation is reshaping how the Preventive Maintenance Software Market is defined: shifting from static CMMS solutions to proactive, intelligent platforms that deliver measurable operational performance gains and strategic planning benefits for maintenance executives.

“In early 2025, an industrial solutions provider deployed an AI-driven module across a global fleet of manufacturing assets, resulting in a measurable 35 percent reduction in unplanned downtime and identifying component wear anomalies up to two weeks earlier than conventional thresholds.”

The Preventive Maintenance Software Market Dynamics section examines key trend vectors affecting the Preventive Maintenance Software Market. This includes evolving customer requirements for asset reliability, digital transformation of maintenance workflows, rising labor costs, and increasing regulatory scrutiny. There is growing demand for integrated, cloud-based solutions that unify IoT capture, anomaly detection, and maintenance orchestration. Key influences include sector-specific compliance mandates in aerospace and utilities, as well as the ongoing digitalization within legacy infrastructure. Industry insight reveals that decision-makers now prioritize platforms offering modular deployment, mobile accessibility, and cross-site standardization. Emerging drivers involve expansion of mobile workforce tools, SME-friendly pricing tiers, and the rise of turnkey analytics dashboards. Overall, decision-makers are navigating a market environment shifting toward predictive, integrated software ecosystems that support enterprise-wide maintenance strategy and execution.

Increasingly, manufacturers, utilities, and logistics operators require software capable of minimizing unexpected asset failures and boosting operational efficiency. The driver’s impact on the Preventive Maintenance Software Market is measurable: organizations deploying AI-embedded maintenance tools report maintenance labor efficiency gains and reduced reactive repair cycles. Digitization efforts enable real-time asset health monitoring, remote diagnostics, and automated scheduling, which together reduce manual workload. One survey of global manufacturing firms noted accelerated adoption of cloud-native maintenance platforms within two years, with over half planning to scale predictive maintenance modules across multiple sites by 2025. This proliferation drives demand across software providers and accelerates R&D investments.

Many enterprises continue to operate with legacy assets that lack connectivity or standardized data protocols. This makes integration with modern preventive maintenance software difficult and costly. Challenges include retrofitting sensors, consolidating data from diverse ERP and SCADA systems, and aligning maintenance schedules across decentralized sites. As a result, some organizations delay full deployment or incur high customization costs. Surveys report that up to 40% of planned system implementations face delays due to technical incompatibilities, prolonging time-to-value and reducing early ROI. These integration challenges remain a significant constraint on broader market adoption.

A rapidly growing opportunity exists in the small and mid-market segment. Many SMEs are now seeking cost-effective cloud-native preventive maintenance software with minimal upfront investment and plug-and-play deployment. These offerings often include mobile dashboards, simplified onboarding, and tiered pricing models. As a result, software vendors are launching SME-focused modules that reduce configuration complexity and provide modular capabilities. Market surveys show increasing interest from mid-market users in pilot programs, with conversion rates rising as awareness grows—creating a large untapped segment for vendors to monetize recurring subscription revenues.

Operators in highly regulated sectors such as aviation, pharmaceuticals, and utilities face stringent certification and compliance requirements. Preventive maintenance activities often require detailed audit trails, inspection logs, and documentation to meet safety standards. Variations between regional regulatory frameworks add complexity—what is acceptable in one jurisdiction may require additional certification in another. This complexity increases deployment timelines, implementation costs, and demand for customized reporting. Some vendors must develop region-specific modules to satisfy requirements, raising the barrier to scalable global deliverables.

Expansion of Explainable AI Diagnostics: Software providers are rolling out explainable AI layers that offer interpretable insights behind anomaly detection. These modules include visual dashboards showing how sensor data values triggered a maintenance alert, enhancing user trust and enabling maintenance managers to validate automated recommendations directly.

Surge in Digital-Twin Implementation: Adoption of digital-twin models for critical equipment has grown by over 40% in energy and heavy-industry use cases. These virtual replicas allow live simulation of asset behavior and failure scenarios, enabling predictive planning and reducing reliance on manual inspection loops.

Modular, Cloud-Native Rollout Accelerating: Cloud-first Preventive Maintenance Software Market offerings with modular deployment options have seen deployment lead-times fall by 20% compared to on-prem installations. This has enabled faster onboarding—some midsize clients now deploy core modules across their site within weeks rather than months.

Integration with Mobile Field Workforce Tools: There is increasing integration of maintenance platforms with mobile apps used by field technicians. Adoption of such mobile-enabled solutions has risen by 35%, leading to real-time task updates, checklist enforcement, and photo-based fault logging, improving response speeds and auditability.

The Preventive Maintenance Software Market is segmented by type, application, and end-user, offering tailored solutions to meet industry-specific maintenance needs. The segmentation highlights how different technological formats, functional roles, and operational scales influence the demand for maintenance automation. In terms of types, the market includes on-premise, cloud-based, and hybrid models—each serving distinct operational environments and scalability requirements. Applications range from asset and equipment monitoring to scheduling, compliance management, and failure prediction. End-users span across industries such as manufacturing, transportation, energy & utilities, healthcare, and facility management, each having unique operational uptime and safety requirements. Understanding this segmentation is critical for vendors seeking to address specific pain points such as downtime reduction, regulatory compliance, and resource optimization. The growing demand for mobile-first deployment and AI-driven insights is influencing all segments, contributing to evolving procurement priorities among enterprises and institutions alike.

The Preventive Maintenance Software Market encompasses three core product types: cloud-based, on-premise, and hybrid solutions. Among these, cloud-based software leads the segment due to its flexibility, lower upfront infrastructure costs, and rapid deployment capabilities. It is especially preferred by mid-sized enterprises and organizations with distributed assets across multiple geographies. These platforms enable real-time synchronization, centralized data storage, and seamless updates—making them ideal for dynamic maintenance environments.

The fastest-growing type is the hybrid model, driven by enterprises that require data localization or regulatory compliance while also leveraging the cloud’s scalability. Hybrid solutions are being rapidly adopted in sectors such as utilities and defense, where certain data must remain on-site, but operational efficiency benefits from cloud-based analytics and automation.

On-premise models, while declining in preference, still hold significance in organizations with stringent data governance requirements or legacy infrastructure. These systems offer full internal control, though they often require higher maintenance and longer deployment cycles. All three types continue to co-exist, with selection dependent on organizational size, IT maturity, and regulatory frameworks.

The Preventive Maintenance Software Market addresses multiple application areas, with asset and equipment monitoring emerging as the leading application. Organizations prioritize this function due to its direct impact on extending equipment life, preventing sudden failures, and ensuring continuous operations. Advanced systems now use real-time telemetry to proactively flag performance deviations, triggering automated alerts and maintenance workflows.

The fastest-growing application is predictive analytics and diagnostics, fueled by the integration of AI, machine learning, and IoT. These capabilities allow systems to not only detect anomalies but also forecast potential failures days or weeks in advance, reducing the risk of costly unplanned downtime. This trend is particularly strong in manufacturing and logistics sectors, where uptime directly correlates with productivity and service delivery.

Other application areas include maintenance scheduling, compliance management, and inventory tracking. These support modules contribute to comprehensive maintenance ecosystems, offering workflow automation, regulatory adherence, and resource planning. The convergence of these applications within unified platforms is reshaping how maintenance is managed in both operational and strategic contexts.

Among end-users, the manufacturing sector stands out as the most dominant contributor to the Preventive Maintenance Software Market. The high value of assets, tight production schedules, and safety-critical processes make proactive maintenance essential. Manufacturers use the software to monitor production line equipment, reduce downtime, and align with lean operational strategies.

The fastest-growing end-user segment is the transportation and logistics industry, where preventive maintenance ensures vehicle reliability, reduces fuel waste, and extends asset life cycles. With increasing adoption of telematics and smart fleet technologies, companies are using software to integrate real-time data from GPS and onboard sensors to optimize maintenance intervals and avoid service disruptions.

Other important end-users include energy and utilities, where infrastructure reliability is paramount, and healthcare, where compliance and equipment availability are vital. Facility management companies are also gaining traction, adopting preventive maintenance platforms to oversee HVAC, lighting, and critical building systems in commercial complexes and institutions. These diverse end-user requirements are driving software vendors to offer modular, industry-specific features and support.

North America accounted for the largest market share at 37.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2025 and 2032.

This regional variation reflects differences in infrastructure maturity, digital transformation, and industry demand. In North America, widespread adoption of digital asset management tools and AI-integrated maintenance platforms drives robust usage, especially in sectors such as aerospace, manufacturing, and utilities. Conversely, Asia-Pacific’s rapid expansion is fueled by infrastructure development, increasing industrial automation, and government-backed digitalization initiatives in countries like China and India. Europe remains a mature yet innovation-driven market, emphasizing sustainability and regulatory compliance. South America and the Middle East & Africa are witnessing steady adoption, particularly in oil & gas, mining, and utilities. Vendors targeting global expansion are focusing on localization, multilingual interfaces, and sector-specific compliance features to address the diverse needs of regional buyers.

North America held the largest market share in the global Preventive Maintenance Software Market, contributing approximately 37.5% of the global volume in 2024. The region's market growth is driven by high demand from manufacturing, aerospace, logistics, and utilities industries, all of which rely heavily on operational uptime and regulatory compliance. The U.S. leads with advanced implementations of AI-integrated preventive maintenance platforms, followed closely by Canada’s strong public infrastructure sector. Government incentives supporting smart factory upgrades and industrial automation are further boosting adoption. Regulatory frameworks such as OSHA standards and energy efficiency mandates have intensified the need for data-driven maintenance tools. Technological advancement across this region includes wide deployment of IoT sensors, predictive analytics engines, and cloud-first asset monitoring platforms, reinforcing North America’s leadership in maintenance technology.

Europe holds a significant portion of the Preventive Maintenance Software Market with an estimated 28.1% of the global share in 2024. Germany, the UK, and France are among the top-performing markets due to their strong industrial sectors and emphasis on workplace safety standards. Regulatory bodies such as the European Agency for Safety and Health at Work drive digital transformation in preventive maintenance through compliance-focused tools. The adoption of sustainability initiatives, including the EU Green Deal, has led companies to implement energy-efficient maintenance practices, with software playing a critical role. Emerging technologies such as digital twins, AI-powered scheduling, and cloud integration are being rapidly adopted, particularly in automotive, energy, and heavy manufacturing sectors. The region also supports innovation through funding and public-private collaboration, contributing to the evolution of intelligent maintenance ecosystems.

Asia-Pacific is the fastest-growing region in the global Preventive Maintenance Software Market, expected to accelerate rapidly over the forecast period. The region accounted for an estimated 21.4% of global market volume in 2024. Countries such as China, India, and Japan are driving this growth through massive infrastructure projects, expanding industrial bases, and rising investments in smart factories. China leads in large-scale adoption across manufacturing zones, while India shows strong momentum in the utility and logistics sectors. Japan continues to lead in technology integration, particularly in robotics-enabled maintenance workflows. Innovation hubs in Singapore and South Korea are fostering AI and IoT applications within asset maintenance platforms. Regional governments are supporting digital infrastructure through strategic initiatives and smart city programs, further boosting the relevance and scalability of preventive maintenance software in both public and private enterprises.

South America’s Preventive Maintenance Software Market is emerging steadily, contributing roughly 6.2% of the global share in 2024. Brazil and Argentina are the primary contributors, driven by modernization across the energy, utilities, and mining sectors. Industrial facilities in these countries are investing in preventive software tools to enhance asset reliability and comply with safety regulations. Public and private entities are collaborating to digitize maintenance operations and reduce unplanned downtime. Infrastructure initiatives, including smart grid development and industrial corridor expansions, are fueling software demand. Government-led incentive schemes and trade policies supporting automation technologies are gradually influencing adoption. Though implementation is slower than in other regions, the presence of multinational vendors and increasing awareness of operational efficiency are pushing steady growth across the continent.

The Middle East & Africa accounted for approximately 6.8% of the global Preventive Maintenance Software Market volume in 2024, with growing demand in oil & gas, construction, and utility sectors. United Arab Emirates (UAE) and South Africa are leading regional markets. In the UAE, oil producers and infrastructure projects are integrating predictive maintenance software to reduce equipment failure and ensure uptime. South Africa sees adoption in utilities and municipal infrastructure maintenance. Across the region, trade partnerships and government initiatives aimed at digital transformation are stimulating demand. Adoption of cloud-based platforms and mobile-first applications is rising due to remote site maintenance requirements. Local regulations mandating asset inspection and safety reporting are further encouraging deployment of structured maintenance solutions. As regional industries modernize and diversify, preventive maintenance software is playing a central role in enabling efficiency and reliability.

United States – 29.8% Market Share

The U.S. leads the Preventive Maintenance Software Market due to its advanced industrial automation, extensive manufacturing base, and high adoption of AI-enabled solutions.

China – 15.6% Market Share

China ranks second in the Preventive Maintenance Software Market, driven by massive infrastructure investment and rapid integration of smart factory technologies.

The global Preventive Maintenance Software Market is characterized by a dynamic and moderately consolidated competitive landscape, with over 50 active vendors operating across various regional and application-specific segments. Key players are strategically positioned based on their technological capabilities, integration expertise, customer base, and support ecosystems. Leading companies are continually investing in research and development to enhance their platforms with AI-based diagnostics, IoT compatibility, and cloud-native architecture. In 2023 and 2024, the market witnessed an uptick in strategic collaborations, such as partnerships with industrial OEMs and cloud infrastructure providers, to deliver vertically tailored solutions. Mergers and acquisitions have also shaped the market, with several mid-sized firms being integrated into larger software conglomerates to enhance product portfolios and global reach. Innovation trends such as predictive analytics, digital twins, and mobile-first UIs are becoming key differentiators among top competitors. Vendors are also expanding multilingual support and localization features to penetrate emerging markets and address compliance variations across geographies. This competitive intensity ensures constant innovation, creating opportunities and challenges for both new entrants and incumbents.

IBM Corporation

SAP SE

Oracle Corporation

Microsoft Corporation

UpKeep Technologies Inc.

Dude Solutions, Inc.

Fiix Inc.

eMaint Enterprises, LLC

IFS AB

Maintenance Connection, Inc.

MPulse Software, Inc.

Hippo CMMS

Schneider Electric SE

Asset Infinity

ManagerPlus Solutions, LLC

Technological advancements are significantly transforming the Preventive Maintenance Software Market. Key innovations include the integration of Internet of Things (IoT) sensors that enable real-time monitoring of equipment conditions and usage patterns. IoT data feeds into cloud-based platforms where Artificial Intelligence (AI) and Machine Learning (ML) algorithms analyze patterns and forecast potential equipment failures with high accuracy. This shift from reactive to predictive maintenance reduces unplanned downtime and extends asset life cycles.

Mobile accessibility has become a core feature, allowing field technicians to perform inspections, log data, and receive alerts via smartphones and tablets, ensuring real-time collaboration and increased efficiency. Additionally, cloud deployment models are gaining traction due to their scalability, reduced upfront costs, and easier integration with enterprise systems such as ERP, CRM, and SCADA platforms.

Digital twin technology—a virtual replica of physical assets—has emerged as a game-changer, enabling simulation of maintenance scenarios to optimize scheduling and resources. Integration with CMMS (Computerized Maintenance Management Systems) and EAM (Enterprise Asset Management) platforms is improving interoperability across departments. The market is also witnessing the rise of no-code/low-code interfaces that empower non-technical users to customize dashboards and automate workflows without programming expertise. These technology trends are shaping the next generation of preventive maintenance, offering data-rich, intelligent, and adaptive systems tailored to industry-specific needs.

• In March 2024, IBM launched an AI-enhanced version of its Maximo Application Suite, featuring advanced machine learning algorithms for anomaly detection and root-cause analysis, enabling more precise equipment failure prediction.

• In September 2023, UpKeep Technologies introduced a mobile-first preventive maintenance platform designed specifically for mid-sized manufacturing units, enhancing technician productivity through offline data capture and real-time alerts.

• In May 2024, Fiix by Rockwell Automation announced the integration of augmented reality (AR) tools into its maintenance software, allowing field teams to access virtual repair instructions and remote expert guidance during inspections.

• In November 2023, SAP rolled out an update to its Asset Strategy and Performance Management module, adding support for environmental compliance monitoring and ESG reporting capabilities for maintenance-heavy industries.

The Preventive Maintenance Software Market Report offers a comprehensive analysis of the global landscape, covering diverse market segments, technological domains, application areas, and regional perspectives. This report evaluates the market across three primary segments: by type (on-premise, cloud-based, and hybrid deployment models), by application (manufacturing, energy & utilities, transportation, healthcare, facility management, and others), and by end-users (SMEs and large enterprises). Each segment is assessed based on its market relevance, adoption trends, and operational challenges.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into country-level dynamics in the United States, China, Germany, India, Brazil, UAE, and more. The report highlights how economic development, infrastructure maturity, and digitalization levels influence regional demand and software implementation strategies.

The scope also explores technological innovation, including IoT connectivity, AI-based failure detection, mobile-first interfaces, and cloud-native deployments. Emphasis is placed on emerging market segments such as AR-enabled maintenance platforms and ESG-compliant asset management solutions, which are gaining traction among sustainability-focused industries.

This report is tailored for decision-makers, IT strategists, and operations professionals, offering actionable insights for market entry, expansion, or investment evaluation. It also maps out vendor positioning, key growth drivers, and potential opportunities in evolving sectors, ensuring a strategic foundation for business planning.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 280.0 Million |

| Market Revenue (2032) | USD 604.6 Million |

| CAGR (2025–2032) | 10.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, AI & Technology Insights, Segment Analysis, Regional & Country‑Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | IBM Corporation, SAP SE, Oracle Corporation, Microsoft Corporation, UpKeep Technologies Inc., Dude Solutions, Inc., Fiix Inc., eMaint Enterprises, LLC, IFS AB, Maintenance Connection, Inc., MPulse Software, Inc., Hippo CMMS, Schneider Electric SE, Asset Infinity, ManagerPlus Solutions, LLC |

| Customization & Pricing | Available on request (10 % Customization is Free) |