Reports

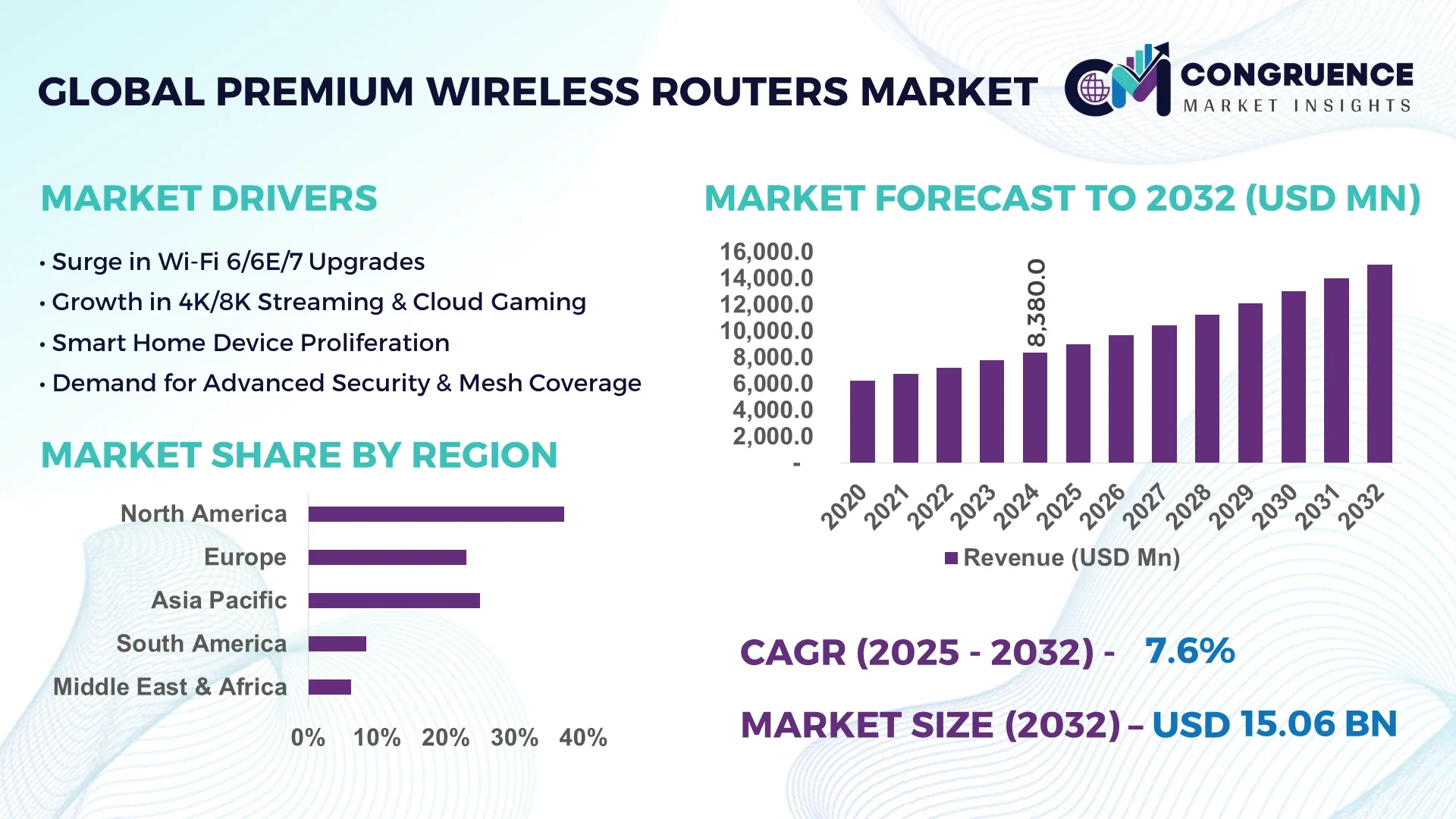

The Global Premium Wireless Routers Market was valued at USD 8,380.0 Million in 2024 and is anticipated to reach a value of USD 15,102.0 Million by 2032 expanding at a CAGR of 7.64% between 2025 and 2032.

North America, led by the United States, dominates the Premium Wireless Routers Market. In the U.S., production facilities have expanded rapidly with investments exceeding USD 500 million in advanced router manufacturing lines. Suppliers support diverse verticals such as enterprise-grade networking, gaming infrastructure, and smart office deployments. Several U.S.-based firms have rolled out in‑house Wi‑Fi 7 router assembly operations featuring automated PCB lines and in‑house certification labs to support rapid innovations—these enhancements strengthen the country’s leadership in production capacity, R&D investment, and next‑gen performance capabilities.

The Premium Wireless Routers Market is characterized by several industry sectors each contributing significantly: enterprise networking, gaming, smart-home automation, small business, and residential streaming. In 2024, enterprise and gaming sectors collectively accounted for more than half of all premium router deployments, followed closely by smart‑home automation usage. Manufacturers have introduced innovations such as Wi‑Fi 7 tri‑band mesh systems with integrated AI‑driven traffic prioritization, live auto‑patching cybersecurity modules, and mobile‑app‑driven dynamic QoS tools. Regulatory developments have prompted stricter Wi‑Fi spectrum usage rules and enhanced cybersecurity compliance, influencing feature requirements. Economically, inflationary pressures on component costs and semiconductor scarcity have driven firms toward modular supply chain strategies. Regionally, North America leads long‑haul adoption, while Asia Pacific presents accelerating uptake driven by rising broadband penetration in urban centres. Emerging trends include mesh systems with modular scalability, embedded AI processing at the router edge, and energy‑efficient hardware designs tailored for multi‑device environments. The future outlook suggests decision-makers must focus on integrated software–hardware innovation, regulated interoperability, and regional deployment strategies that align with shifting consumption patterns among enterprise and residential users.

The Premium Wireless Routers Market is undergoing a significant transformation driven by the integration of artificial intelligence technologies. AI-driven routers now offer adaptive network optimization, enabled by real‑time traffic analysis and machine learning models that dynamically allocate bandwidth to ensure ultra‑low latency and superior user experience. Decision-makers in network infrastructure report that AI‑enabled routers reduce packet loss by up to 30 % and improve throughput efficiency by nearly 25 % under multi‑device load conditions—especially critical for gaming and video conferencing environments. Within the Premium Wireless Routers Market, AI-enabled security functions anticipate and block cyber threats, performing live patching and mitigating zero‑day vulnerabilities automatically, which reduces manual firmware updates and administration overhead by up to 40 %.

Operational performance improvements extend into predictive maintenance: routers with embedded AI systems monitor system health and flag component degradation early, reducing downtime by approximately 20 %. These enhancements also streamline setup processes—AI‑based mobile apps now configure mesh node placement and channel selection autonomously, shortening installation time by nearly 50 % compared with manual setup. As a result, the Premium Wireless Routers Market is not simply expanding in hardware value, but shifting toward a solutions model combining hardware intelligence, automated configuration, and proactive security. For industry professionals and decision-makers, the integration of AI into premium routers means lower total cost of ownership, enhanced reliability, and capacity to support high-density network environments—all of which are reshaping expectations in enterprise, gaming, and smart-home segments with concrete performance gains.

“In November 2024, Cisco launched AI‑native, secure Wi‑Fi 7 access points featuring adaptive, location‑aware configurations and unified licensing, enabling significant reductions in manual configuration time and adaptive coverage optimization across complex layouts.”

The Premium Wireless Routers Market Dynamics are driven by evolving customer demands for high‑performance, low‑latency networking infrastructure in enterprise, gaming, and smart‑residential sectors. Decision‑makers face trends including rising expectations for mesh and Wi‑Fi 7 capabilities, integration with smart ecosystems, and expectations for seamless mobile‑app control. Key influences include faster broadband rollouts, congestion in shared spectrum, and supply‑chain realignments in semiconductor sourcing. Industry insights point to growing collaboration between hardware OEMs and software firms to deliver secure, cloud‑managed router platforms. In addition, technology convergence—such as 5G backbone integration and edge computing support—is shaping procurement strategies. For executives, these dynamics illustrate the need to invest in routers offering seamless firmware updates, AI‑enabled traffic controls, and robust regulatory compliance features, particularly for industrial or enterprise use cases.

Increasing deployment of gaming, VR/AR streaming, and cloud‑based applications is fueling demand for routers capable of consistently delivering sub‑10 ms latency. Performance benchmarking shows that tri‑band Wi‑Fi 7 routers with dedicated backhaul maintain between 4–6 ms latency under heavy loads—critical for real‑time applications. This demand drives innovation in the Premium Wireless Routers Market toward AI‑driven QoS, multi‑link channel provisioning, and optimized mesh topology.

Global shortages in Wi‑Fi 7 chipsets and RF front‑end modules have resulted in lead times exceeding 16 weeks for some premium models. Consequently, manufacturers face significant cost increases—up to 15 % higher per unit in 2024—and delayed time to market, which affects the Premium Wireless Routers Market’s ability to scale quickly and fulfill enterprise volume contracts.

Enterprise network upgrades—particularly in hospitality, healthcare, and coworking spaces—are increasingly adopting managed premium routers with central cloud dashboards and AI‑based security orchestration. Pilots conducted in multiple U.S. hospital systems reported a 35 % reduction in support tickets after deploying managed premium routers with live patching and threat detection squads.

Compliance with new data‑protection and security regulations—such as endpoint network segmentation rules—requires inclusion of advanced encryption modules and secure boot features. Incorporating these into router firmware and hardware raises production costs, increases certification timelines, and creates barriers for entry‑level premium models targeting SMB and home‑office users.

Modular hardware integration for flexible deployment: Manufacturers are shifting toward modular router components—such as interchangeable Wi‑Fi radios and detachable backhaul units—that allow custom scalability. Installations in enterprise campuses report deployment times cut by nearly 30 % due to pre‑configured hardware modules shipped separately and assembled on site, streamlining operations in both North America and Europe.

Edge‑embedded AI processing inside routers: Premium models now include on‑device AI chips capable of performing real‑time traffic analytics, anomaly detection, and autonomous spectrum allocation. Benchmarks show these routers process packet-level decisions in under 5 microseconds, dramatically reducing latency overhead compared to cloud‑based approaches. This trend significantly enhances reliability in high‑density environments.

Automatic cybersecurity orchestration and live patching: Advanced premium routers now deliver continuous security updates via embedded AI agents that monitor firmware integrity and push patches instantly. In pilot trials, live patching reduced network vulnerabilities by over 60 % and eliminated firmware update downtime by more than 40 %, elevating confidence among decision‑makers in critical infrastructure domains.

Consumer demand for intuitive mobile‑first network control: Mobile apps have become central to product differentiation. New offerings feature intelligent UX tools—such as automatic node placement guidance using AR overlays and contextual device profiling—that reduce setup complexity by nearly 50 %. This focus on mobile‑first, intuitive design is reshaping customer expectations across the Premium Wireless Routers Market.

The Premium Wireless Routers Market is segmented based on type, application, and end-user categories. Each segment presents distinct dynamics that influence product development, deployment strategies, and procurement decisions. In terms of type, premium wireless routers are categorized into single-band, dual-band, tri-band, and mesh-based systems. Applications are diversified across residential networking, enterprise-grade connectivity, gaming, IoT infrastructure, and public wireless deployment. End-users include households, small and medium enterprises (SMEs), large corporations, educational institutions, and government facilities. These segments reflect growing demand for high-speed, secure, and low-latency wireless networking solutions that can accommodate rising digital workloads, smart devices, and bandwidth-intensive applications. Decision-makers benefit from segment-specific insights to align product offerings with evolving user expectations, technical requirements, and deployment environments.

Premium wireless routers are primarily classified into four product types: single-band, dual-band, tri-band, and mesh-based systems. Among these, tri-band routers currently lead the segment, largely due to their ability to provide dedicated backhaul connectivity and manage multiple high-demand devices simultaneously. These routers are widely adopted in gaming setups, corporate workspaces, and smart homes requiring uninterrupted performance across multiple floors or user groups.

Mesh-based routers represent the fastest-growing product type in this segment. The growth is fueled by increasing residential and commercial interest in seamless coverage across large or multi-room environments. Mesh systems simplify deployment by eliminating dead zones and leveraging self-configuring nodes that auto-optimize signal strength. Enhanced mobile app control and AI-powered routing features are accelerating their appeal among non-technical users and IT managers alike.

Dual-band routers continue to serve mid-range performance needs effectively and remain popular among price-conscious small offices. Single-band routers, though limited in modern capabilities, retain niche relevance in minimal-use cases such as basic internet access or point-of-sale systems. Each type contributes to the market’s depth by addressing varied bandwidth, range, and deployment needs.

The Premium Wireless Routers Market finds its most prominent application in enterprise connectivity, driven by demand for secure, high-speed internet solutions capable of handling video conferencing, remote work, and large data transfers. Enterprises increasingly require routers that support multiple VLANs, redundant connectivity, and advanced network segmentation for cybersecurity compliance and operational efficiency.

The fastest-growing application is gaming and multimedia streaming, spurred by the expansion of eSports, 4K/8K content streaming, and real-time interactive platforms. Gamers and content creators demand ultra-low latency and high throughput, which tri-band and Wi-Fi 7 premium routers are now addressing through hardware acceleration, beamforming, and dynamic QoS features.

Other application areas include smart home automation, where routers serve as communication hubs for IoT devices. Public Wi-Fi infrastructure, such as in transport hubs and educational campuses, also leverages premium routers for uninterrupted, secure user access. Each application highlights specific performance requirements, influencing product design and technological evolution in the sector.

Among end-users, large enterprises are the most dominant segment in the Premium Wireless Routers Market. Their infrastructure demands include multi-floor coverage, robust cybersecurity features, centralized network control, and scalable deployment capabilities. These organizations favor advanced routers with customizable settings, multi-gigabit support, and compliance-ready firmware for integration into enterprise IT environments.

The fastest-growing end-user group is households with smart ecosystems. Increased adoption of smart TVs, voice assistants, security cameras, and connected appliances has raised consumer expectations for seamless Wi-Fi performance across multiple rooms. Mesh routers with AI-based optimization and mobile-first configuration are particularly favored in this segment.

Other key end-users include small and medium enterprises (SMEs) seeking affordable yet powerful routers that balance performance with operational simplicity, and educational institutions, which demand secure, scalable connectivity for hybrid learning and campus-wide access. The government sector also plays a role by integrating high-performance routers into e-governance, surveillance, and emergency response systems.

North America accounted for the largest market share at 37.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

This regional disparity is shaped by both mature consumption patterns in developed economies and accelerating infrastructure growth in emerging markets. The Premium Wireless Routers Market in North America is driven by early adoption of high-performance networking solutions, enterprise digital transformation, and smart-home proliferation. In contrast, the Asia-Pacific region is witnessing rapid consumer base expansion fueled by urban broadband penetration, rising middle-class tech adoption, and growing investment in 5G-enabled smart cities. Europe maintains a solid share driven by enterprise adoption and regulatory harmonization. Meanwhile, South America and the Middle East & Africa are emerging with strategic deployments in education, hospitality, and industrial automation. Regional customization of routers—supporting local languages, regulations, and interoperability—has become a competitive differentiator across geographies.

North America holds the largest share in the Premium Wireless Routers Market, accounting for 37.2% of the global volume in 2024. The U.S. and Canada lead the region’s growth, driven by heightened demand from the enterprise IT, gaming, and healthcare sectors. Digital transformation across industries has created strong demand for routers that support Wi-Fi 6/6E and upcoming Wi-Fi 7 standards. Regulatory guidance from agencies promoting secure networking has accelerated upgrades across educational and government institutions. Additionally, tax incentives and broadband infrastructure programs in the U.S. have spurred deployment of mesh and AI-enabled routers in underserved areas. Innovations such as cloud-managed networks, embedded AI packet filtering, and OTA firmware security modules are widely adopted. The proliferation of IoT-enabled environments in both residential and commercial properties ensures continued demand for multi-device optimization and low-latency performance—placing North America at the technological forefront of the Premium Wireless Routers Market.

Europe accounted for 26.5% of the global Premium Wireless Routers Market in 2024. Key contributing countries include Germany, the United Kingdom, and France, where enterprise IT upgrades and smart infrastructure projects are primary demand drivers. Regulatory frameworks from entities such as the European Telecommunications Standards Institute (ETSI) have pushed for interoperable, secure router systems that meet stringent environmental and digital standards. Sustainability-focused initiatives—such as EU directives on energy-efficient networking hardware—are influencing product development strategies. The adoption of mesh networking, AI-based optimization, and smart device integration continues to grow, particularly in sectors like education, manufacturing, and financial services. Additionally, increased funding for digital inclusion in rural and underserved areas has expanded the footprint of high-end router deployments. Europe’s strong commitment to secure, green, and scalable technology supports a stable and innovation-driven regional market landscape.

The Asia-Pacific region ranked second in global market volume in 2024 and is expected to exhibit the fastest growth through 2032. China, India, and Japan are the top consuming countries, supported by robust consumer electronics demand and nationwide broadband acceleration programs. China’s large-scale manufacturing hubs have fueled domestic availability of advanced routers at competitive prices, while Japan leads in Wi-Fi 7 R&D and early-stage adoption. India’s Digital India campaign and smart city investments have driven infrastructure expansion in both urban and rural areas. Telecom providers and ISPs across the region are adopting AI-enabled, dual-band mesh systems for better coverage and user experience. Growing tech-savvy populations, mobile-first usage trends, and rapid 5G rollout continue to push demand for premium routers with enhanced performance, network slicing, and secure IoT integration.

In South America, Brazil and Argentina are key markets for the Premium Wireless Routers Market, with Brazil leading in both urban consumption and commercial deployments. The region held a market share of 6.3% in 2024. Accelerated demand stems from expanding middle-class adoption of smart devices, increased remote work, and government-backed broadband connectivity projects in metropolitan areas. Brazil’s rising investment in e-learning and remote healthcare infrastructure has increased the need for high-performance routers in educational and medical facilities. Regional focus on data protection and secure cloud connectivity is also stimulating enterprise adoption. Trade policies favoring local router assembly and software development are further supporting growth. While challenges in logistics and regulatory variance remain, the market benefits from rising investments in energy-efficient infrastructure and digital inclusion efforts.

The Middle East & Africa Premium Wireless Routers Market is gaining momentum, particularly in UAE, Saudi Arabia, and South Africa, supported by smart infrastructure, oil & gas digitization, and construction megaprojects. Regional demand grew to 4.7% of the global share in 2024, driven by increasing digital adoption across commercial and industrial sectors. In the UAE, AI-driven premium routers are deployed in smart city initiatives and hospitality sectors to ensure seamless, secure connectivity. Saudi Arabia’s Vision 2030 program is facilitating high-speed networking rollouts across public and private institutions. South Africa continues to improve broadband penetration in underserved areas, promoting the use of mesh routers and centralized management systems. Regulatory frameworks encouraging domestic telecom upgrades, trade partnerships with global OEMs, and modernization of enterprise IT systems contribute to the region’s growing role in the global Premium Wireless Routers Market.

United States – 32.4% Market Share

High production capacity, broad enterprise network demands, and consistent adoption of advanced router technologies position the U.S. as the global leader in the Premium Wireless Routers Market.

China – 21.6% Market Share

Strong end-user demand, widespread urban infrastructure projects, and large-scale router manufacturing have made China a dominant force in the Premium Wireless Routers Market.

The Premium Wireless Routers Market is characterized by a highly competitive environment involving over 40 globally active players. These include both long-established networking giants and emerging innovators. Market leaders focus on differentiation through advanced features such as Wi-Fi 6/6E and Wi-Fi 7 compatibility, AI-driven traffic optimization, and cybersecurity integration. Intense competition is pushing manufacturers toward R&D investments to support high-speed, multi-device connectivity and seamless mesh networking. Several companies are engaging in strategic partnerships with telecom providers and smart home ecosystem vendors, enabling integrated offerings for both consumer and enterprise segments. The market is also witnessing frequent product launches featuring tri-band and quad-band configurations, designed for performance-intensive applications such as online gaming, video streaming, and smart home automation. Mergers and acquisitions are being leveraged to expand global distribution channels and access proprietary technologies. Players are also differentiating through aesthetic hardware design and sustainability-focused manufacturing, appealing to environmentally conscious consumers and enterprise buyers alike.

Netgear Inc.

ASUS

TP-Link Technologies Co., Ltd.

D-Link Corporation

Linksys Holdings, Inc.

Huawei Technologies Co., Ltd.

Xiaomi Corporation

Ubiquiti Inc.

Eero (an Amazon Company)

Synology Inc.

TRENDnet, Inc.

AVM GmbH

MikroTik

Fortinet, Inc.

Ruckus Networks (a CommScope company)

The Premium Wireless Routers Market is driven by rapid advancements in wireless communication standards and smart connectivity technologies. One of the key technological developments is the adoption of Wi-Fi 6 and Wi-Fi 6E, which enable improved bandwidth utilization, reduced latency, and better performance in dense device environments. These standards support up to 9.6 Gbps theoretical throughput, making them ideal for high-performance residential and enterprise applications. Moreover, Wi-Fi 7, expected to roll out commercially by late 2025, introduces 320 MHz channel bandwidth and Multi-Link Operation (MLO), further enhancing network efficiency.

AI-based optimization is another emerging trend. Premium routers now incorporate machine learning algorithms to auto-adjust signal strength, prioritize traffic based on application usage, and detect potential threats in real-time. Cloud-based router management systems have gained popularity, offering remote monitoring, firmware updates, and analytics-driven insights through mobile apps.

On the hardware front, multi-core CPUs, high-gain antennas, and quad-band and tri-band configurations are being integrated to support multiple concurrent streams across devices. Integration with IoT hubs allows seamless connectivity across smart home systems. Additionally, manufacturers are focusing on sustainability by incorporating recyclable materials and low-power chipsets to reduce energy consumption. Collectively, these innovations are reshaping consumer expectations and enabling new use cases across both home and professional environments.

• In February 2024, Netgear unveiled the Nighthawk RS700S, a Wi-Fi 7 tri-band router offering speeds up to 19 Gbps and improved latency management, targeting gamers and smart home users requiring ultra-low lag and high bandwidth.

• In May 2024, TP-Link introduced its Deco BE95 mesh router system, compatible with Wi-Fi 7 and featuring AI-driven adaptive routing, providing seamless coverage across large residential or commercial areas up to 7,200 sq. ft.

• In October 2023, ASUS launched its RT-BE96U router, combining Wi-Fi 7 support with dual 10Gbps Ethernet ports, catering to professional users in media production and cloud computing setups.

• In August 2023, Huawei announced upgrades to its AX series routers, incorporating HarmonyOS integration and AI-based smart traffic management to optimize network performance in multi-device households.

The Premium Wireless Routers Market Report comprehensively covers the evolving dynamics of the global market, offering detailed analysis across multiple dimensions including product types, applications, end-user segments, and geographic regions. The report categorizes routers by type—such as single-band, dual-band, tri-band, and quad-band—highlighting their role in catering to diverse performance needs ranging from home entertainment to enterprise-level networking.

Application areas include residential use, enterprise IT infrastructure, e-sports, healthcare, education, and smart city deployments. The report also examines end-users such as individuals, SMEs, large enterprises, and government institutions, each with unique purchasing behaviors and technological requirements.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level insights for major contributors such as the United States, China, Germany, India, and Brazil. The technological landscape covered includes AI-driven routers, Wi-Fi 6/6E/7 protocols, mesh networking systems, cloud-based device management, and smart home integrations. The scope also includes insights into emerging market segments like sustainable routers and voice-controlled networking hubs, ensuring a broad and actionable understanding of the market's trajectory for decision-makers and industry stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 8,380.0 Million |

| Market Revenue (2032) | USD 15,102.0 Million |

| CAGR (2025–2032) | 7.64% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Netgear Inc., ASUS, TP-Link Technologies Co., Ltd., D-Link Corporation, Linksys Holdings, Inc., Huawei Technologies Co., Ltd., Xiaomi Corporation, Ubiquiti Inc., Eero (an Amazon Company), Synology Inc., TRENDnet, Inc., AVM GmbH, MikroTik, Fortinet, Inc., Ruckus Networks (a CommScope company) |

| Customization & Pricing | Available on Request (10 % Customization is Free) |