Reports

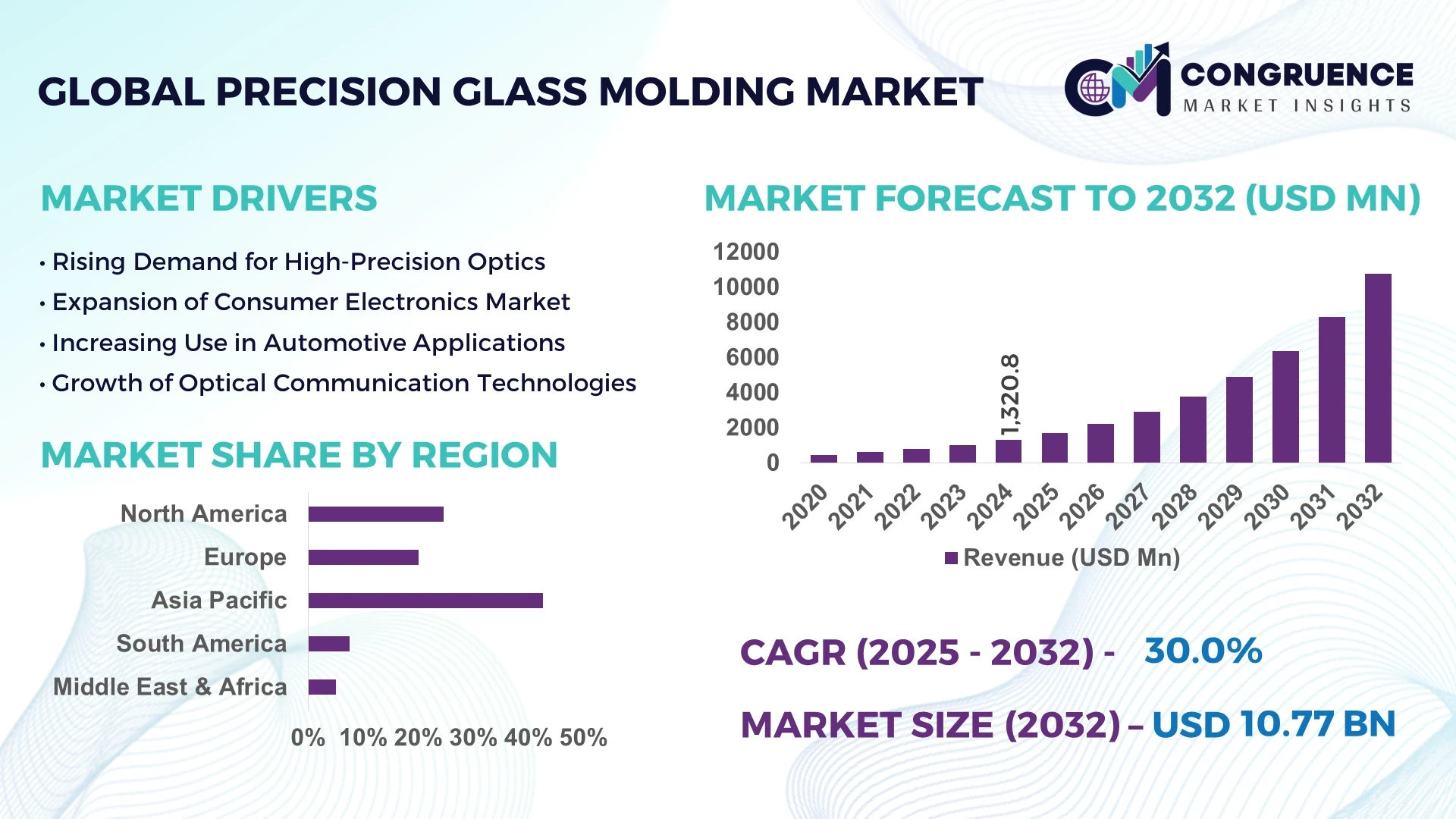

The Global Precision Glass Molding Market was valued at USD 1,320.8 Million in 2024 and is anticipated to reach a value of USD 10,774.17 Million by 2032 expanding at a CAGR of 30.0% between 2025 and 2032.

Germany leads the global landscape with its extensive production capacity supported by robust government-backed R&D initiatives. The country has seen significant capital inflows into optics manufacturing, particularly for precision glass components used in automotive sensors and biomedical imaging technologies.

The Precision Glass Molding Market is experiencing rapid evolution across key verticals such as automotive optics, semiconductor equipment, medical devices, and consumer electronics. Automotive applications, particularly head-up displays and advanced driver-assistance systems (ADAS), have witnessed rising demand for ultra-precise molded glass optics. In the medical field, compact imaging devices and laser delivery systems increasingly rely on molded lenses for their accuracy and stability. With regulatory pressures to reduce optical component weight and environmental impact, manufacturers are shifting toward cleaner, high-efficiency molding techniques. The Asia-Pacific region continues to show robust consumption patterns, driven by expanding electronics manufacturing hubs in countries like China, South Korea, and Taiwan. Recent technological advancements, including hybrid molding machines and low-temperature molding processes, are reshaping production lines with improved yield rates and minimized cycle times. Furthermore, smart factory adoption is fueling demand for real-time monitoring and predictive maintenance in molding operations. As demand for high-performance optical components increases, the market outlook remains optimistic with significant growth projected in precision metrology, defense optics, and next-generation communications.

Artificial Intelligence (AI) is revolutionizing the Precision Glass Molding Market by introducing intelligent automation, process optimization, and predictive analytics into traditional manufacturing workflows. AI-driven quality control systems are being adopted to reduce defect rates in molded glass optics, enhancing precision and consistency at microscopic levels. Using high-resolution vision systems combined with machine learning, manufacturers can now detect sub-micron defects in real-time, eliminating post-production inspection delays and costly waste.

In smart production environments, AI-powered algorithms are continuously optimizing parameters such as mold temperature, pressure cycles, and material flow rates. This adaptive process control enables higher throughput while maintaining ultra-tight tolerances required in precision optical applications. Additionally, AI-integrated simulation software is shortening product development cycles by allowing virtual prototyping and real-time stress modeling of complex lens geometries.

The integration of AI in the Precision Glass Molding Market also enables predictive maintenance of high-value molding machines. Through sensor networks and data analytics, AI identifies early signs of equipment wear or deviation, minimizing unplanned downtimes and improving asset utilization. In logistics, AI assists with inventory management, ensuring availability of high-grade optical glass materials in sync with production schedules. The continued convergence of AI with robotics, data platforms, and edge computing is paving the way for smart, fully digitized molding facilities, positioning AI as a cornerstone in the market's evolution toward higher productivity and innovation.

“In April 2024, a Japanese optics manufacturer deployed an AI-based adaptive process control system across its molding lines, resulting in a 32% reduction in thermal deformation errors and a 27% improvement in lens surface uniformity for high-refractive index optical components used in biomedical applications.”

The Precision Glass Molding Market is shaped by the increasing demand for compact, high-performance optical components across diverse sectors such as automotive, consumer electronics, healthcare, and defense. This demand is driven by advancements in camera systems, LiDAR technologies, and wearable medical devices that require miniaturized optics with extreme surface accuracy and thermal stability. Additionally, advancements in mold materials, coating technologies, and molding process automation are enabling manufacturers to meet high-volume production needs without sacrificing quality. Rapid growth in electric vehicles and autonomous driving solutions is also contributing to the expansion of molded optics for head-up displays and camera modules. Furthermore, regulatory trends encouraging eco-friendly production processes are leading to the adoption of lead-free glass materials and energy-efficient molding systems.

The rapid proliferation of smartphones, AR/VR headsets, and compact imaging systems has significantly fueled the demand for miniature optical elements produced through precision glass molding. These devices rely on lenses with ultra-fine tolerances and consistent thermal stability, which traditional polishing methods struggle to deliver at scale. Precision glass molding addresses this gap by enabling mass production of complex optical geometries with minimal post-processing. For instance, the growing integration of facial recognition and 3D imaging technologies in mobile devices has led manufacturers to adopt aspheric and freeform lenses made via advanced molding techniques. The compactness, durability, and high refractive performance of molded lenses make them an ideal solution for next-gen consumer electronics, directly influencing procurement strategies and product design innovation.

Despite its technological advantages, the Precision Glass Molding Market faces challenges related to the high capital investment required for molds, equipment, and process development. Custom molds for complex lens profiles often involve extensive design iterations and precision machining, resulting in elevated upfront costs. Additionally, achieving consistent output in volume production necessitates cleanroom infrastructure and advanced temperature control systems, further increasing operating expenses. These cost barriers are especially restrictive for small and mid-sized enterprises attempting to enter the market or expand their product lines. Moreover, the complexity of aligning mold materials with specific glass compositions to avoid deformation or optical aberrations introduces additional technical and financial constraints, hindering widespread adoption in cost-sensitive sectors.

The Precision Glass Molding Market is witnessing expansive opportunities in the automotive and medical imaging industries, both of which demand high-precision, thermally stable optical components. In the automotive segment, precision-molded optics are becoming essential for ADAS, LiDAR systems, and head-up displays, where clarity, durability, and resistance to environmental conditions are critical. As OEMs prioritize safety and automation, suppliers are investing in high-output molding lines to meet the demand for multi-lens assemblies. Simultaneously, the medical sector’s growing preference for minimally invasive diagnostics is boosting demand for compact, high-resolution endoscopes and optical coherence tomography (OCT) devices. Precision glass molding allows for scalable production of the intricate lenses needed for these devices, offering medical OEMs consistent quality with reduced lead times—opening new avenues for innovation and market penetration.

One of the primary challenges affecting the Precision Glass Molding Market is the limited compatibility between available mold materials and certain high-performance optical glasses. Some specialty glasses, particularly those with high refractive indices or unique transmission properties, require extremely narrow processing windows and can degrade mold surfaces over repeated cycles. Additionally, the molding process is highly sensitive to fluctuations in temperature, humidity, and surface cleanliness, making quality control more complex. Any deviation during pre-heating, pressing, or cooling phases can result in deformation or optical distortion, reducing yield rates. These process sensitivities demand rigorous operator training and continuous equipment calibration, both of which elevate the operational risk and cost burden for manufacturers aiming to maintain high-volume, precision output.

• Surge in Automotive Lens Miniaturization: The increasing integration of optical systems in automotive safety and navigation technologies is leading to a noticeable shift toward miniaturized lenses manufactured using precision glass molding. Automakers are incorporating ultra-compact optical components into ADAS, LiDAR, and night vision systems. In 2024 alone, over 25 million vehicles globally were equipped with molded glass optics in sensor arrays, with the majority deployed in advanced European and Japanese models. This trend is creating demand for high-output, multi-cavity molding systems capable of producing micro-lenses with sub-micron surface accuracy.

• Growth of Hybrid Mold Materials: To improve durability and production efficiency, manufacturers are adopting hybrid mold materials combining tungsten carbide and glass-like ceramics. These materials offer superior thermal resistance and dimensional stability during repeated molding cycles. Recent production lines using such hybrid molds reported a 40% increase in cycle durability and a 22% reduction in surface degradation. The development of nano-coated molds has also enhanced release efficiency, minimizing defect rates and boosting output consistency.

• Expansion of Optical Applications in Medical Devices: The medical optics segment is seeing heightened adoption of precision glass molding for components used in diagnostic imaging and surgical tools. Demand is especially strong for molded aspheric lenses in endoscopy and OCT devices. Between 2023 and 2024, shipments of precision-molded optical parts for medical use increased by over 30%, with North America leading procurement, particularly from surgical device OEMs expanding minimally invasive product lines.

• Shift Toward Smart Manufacturing and AI Integration: Digitization and smart factory concepts are influencing how precision glass molding facilities operate. With AI-based process monitoring and adaptive controls, molding operations now achieve tighter control of pressure, alignment, and heating parameters. In 2024, over 60% of new molding equipment installations included AI-enabled systems, enabling predictive maintenance and faster material changeovers. These systems reduced production downtime by up to 28% and improved throughput by approximately 18%, fostering stronger margins for manufacturers.

The Precision Glass Molding Market is segmented by type, application, and end-user verticals, each contributing uniquely to the market's evolution. On the type front, the market includes aspheric lenses, spherical lenses, freeform lenses, and others tailored to specific functional requirements. Application-wise, precision glass molding serves domains such as automotive optics, medical imaging, consumer electronics, defense, and industrial metrology. Automotive optics remains the dominant application, driven by increased adoption of ADAS systems. From an end-user perspective, OEMs in the automotive and medical industries form the bulk of demand, with rising interest from defense and semiconductor manufacturers. Each segment reflects specific performance standards and regulatory compliance needs, dictating the choice of glass, coatings, and manufacturing precision. As innovation accelerates, segmentation trends point toward increasing customization, shorter design-to-market timelines, and deeper integration with smart manufacturing systems across multiple verticals.

Aspheric lenses lead the type segment within the Precision Glass Molding Market due to their superior light focusing capabilities and reduced spherical aberrations. Their application in automotive sensors, smartphone cameras, and medical imaging systems has made them the most widely produced type, owing to their balance of performance and compactness. Freeform lenses are emerging as the fastest-growing type, particularly in augmented reality devices and wearable displays, where complex geometries are required for unique light-path engineering. The demand for personalized and space-constrained optical solutions has accelerated their development. Spherical lenses, although more traditional, continue to serve mass-market applications where performance requirements are moderate but cost and production speed are critical. Cylindrical and diffractive lenses make up the niche end of the spectrum, used in laser optics and instrumentation where specialized beam shaping is needed. Each type contributes to the market’s diversity, offering tailored solutions across industries.

Automotive optics remains the leading application in the Precision Glass Molding Market, particularly as ADAS and sensor-based navigation become standard features in new vehicle models. Molded glass lenses are critical for ensuring optical clarity and alignment accuracy in cameras and LiDAR systems. The fastest-growing application is in medical imaging, where molded optics are increasingly used in diagnostic endoscopes, ophthalmic devices, and compact laser delivery systems. The miniaturization of these tools without compromising optical performance is driving rapid adoption. Consumer electronics, particularly smartphones and VR headsets, continue to rely heavily on molded lenses for compact camera modules and projection systems. The defense sector is another key application area, utilizing precision-molded optics in range finders and surveillance systems. Industrial metrology, though a smaller application segment, benefits from precision optics for accurate measurement tools and sensor calibration systems. Each application is influenced by demand for high precision, thermal stability, and mass production scalability.

Automotive OEMs form the leading end-user segment in the Precision Glass Molding Market due to their intensive use of optical sensors and cameras in both traditional and electric vehicles. Their need for high-volume production of durable, accurate optical components makes molded lenses ideal for integration into headlights, ADAS modules, and interior monitoring systems. Medical device manufacturers represent the fastest-growing end-user group, driven by an expanding portfolio of optical diagnostic and therapeutic tools. The preference for compact, sterilizable, and thermally stable lenses is prompting increased investment in molded optics across surgical and imaging devices. Consumer electronics companies, particularly in Asia-Pacific, also contribute significantly through demand for lenses in mobile phones, wearables, and virtual displays. The defense and aerospace sector, while smaller in volume, prioritizes precision and reliability, sourcing custom-molded optics for advanced targeting and imaging systems. These varied end-user needs are influencing design requirements and production scale across the global market.

Asia-Pacific accounted for the largest market share at 42.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 32.4% between 2025 and 2032.

Asia-Pacific’s dominance is driven by a vast electronics manufacturing base, rapid industrialization, and growing demand for molded optics in automotive and mobile devices. Countries like China, Japan, and South Korea lead in production volume, with substantial investment in automated molding lines and optical R&D infrastructure. Meanwhile, North America's rapid advancement is attributed to strategic tech partnerships, AI integration, and surging demand in medical and defense applications.

The global Precision Glass Molding Market continues to experience evolving regional patterns shaped by diverse industrial needs, regulatory environments, and tech innovation cycles. While Europe prioritizes sustainability and precision engineering, Latin America and the Middle East are increasingly investing in modern optics for energy and infrastructure applications. Localized manufacturing initiatives, government-backed tech adoption, and industrial digitization efforts are driving the market forward. Global players are expanding into emerging regions with modular production models, while established markets are optimizing operations with AI, hybrid mold materials, and real-time monitoring. As geopolitical shifts and reshoring strategies reshape global supply chains, region-specific dynamics will remain pivotal in influencing procurement, pricing, and innovation cycles.

Adoption of Smart Optics and AI-led Manufacturing Accelerates Regional Growth

North America captured a 24.6% share of the global Precision Glass Molding Market in 2024, supported by high-value demand from the automotive safety, medical device, and aerospace sectors. U.S.-based companies are at the forefront of integrating AI-driven molding automation, enabling faster cycles and minimized lens defects. The U.S. government’s emphasis on reshoring optical manufacturing, combined with regulatory incentives for advanced material R&D, has created favorable conditions for market expansion. Furthermore, FDA support for optical medical devices and new defense procurement regulations have accelerated investment in precision glass molding facilities. Canadian manufacturers are investing in green energy-based molding units to comply with regional carbon reduction targets. Adoption of ultra-compact lens modules for LiDAR and 3D imaging in vehicles is further expanding regional demand.

Green Manufacturing and Optical Standardization Drive Production Evolution

Europe held approximately 20.1% of the global Precision Glass Molding Market in 2024, with strong contributions from Germany, the UK, and France. Germany leads in optical precision machinery, driven by its automotive, healthcare, and metrology sectors. The European Union’s RoHS and REACH regulations are pushing companies toward lead-free optical materials and sustainable production methods. Regional standardization for medical optics has also improved cross-border product compatibility and export readiness. France has invested in photonics clusters, while the UK is promoting research initiatives through its Innovation Strategy. Companies are adopting low-energy molding techniques and digital twin simulations to enhance design accuracy and efficiency. The convergence of optical manufacturing and sustainability mandates is reshaping operational models across the region.

Manufacturing Hub Expansion and Technology Clusters Propel Market Leadership

Asia-Pacific leads the global Precision Glass Molding Market by volume, contributing 42.7% of the total market output in 2024. China remains the dominant producer, with extensive investments in high-speed optical production lines and domestic tech clusters supporting integrated component manufacturing. Japan is focused on ultra-precision optics for semiconductor and biomedical applications, while South Korea is expanding production for consumer electronics and display modules. India is emerging as a cost-effective alternative, leveraging its growing medical device sector and expanding optical glass infrastructure. Regional governments have invested in optical metrology and AI-integrated production tools, enhancing both volume and quality. Smart manufacturing zones across Shenzhen, Osaka, and Seoul are accelerating time-to-market while reducing cost per unit.

Optical Integration in Infrastructure and Energy Drives Emerging Market Demand

South America contributed approximately 7.6% to the global Precision Glass Molding Market in 2024, with Brazil and Argentina leading in demand. Brazil’s expanding telecommunication infrastructure and energy-efficient construction sectors are incorporating molded glass optics in surveillance and smart lighting systems. Government-backed tax incentives for industrial modernization and clean energy adoption have attracted global optics manufacturers to establish regional assembly lines. Argentina’s demand is growing in the medical imaging segment, supported by imports and local assembly of precision lenses. Challenges in logistics and material sourcing persist, but regional collaborations with North American firms are enabling technology transfer and capacity-building.

Defense Procurement and Digital Infrastructure Projects Boost Market Entry

The Middle East & Africa accounted for 5.0% of the Precision Glass Molding Market in 2024, with notable growth in the UAE and South Africa. Demand is driven by the integration of precision optics in defense surveillance, aviation systems, and smart city technologies. UAE’s Vision 2031 and investments in digital infrastructure have enabled collaborations with global optics firms for localized assembly and prototyping. South Africa is focusing on medical device manufacturing and educational research tools that use compact, precision optics. Regional trade zones and bilateral agreements with Asian and European manufacturers are fostering supply chain accessibility. Emerging regulations on import duties and technology transfer frameworks are further improving entry feasibility for optical component producers.

China – 33.2% Market Share

High production capacity combined with massive electronics and automotive component manufacturing base drives its leadership in the Precision Glass Molding Market.

Germany – 16.4% Market Share

Strong demand from automotive, metrology, and photonics sectors, backed by precision engineering excellence, secures Germany’s position in the global market.

The Precision Glass Molding Market features a moderately fragmented competitive landscape, with over 60 active global players operating across key regions including Asia-Pacific, North America, and Europe. Industry participants range from specialized optics manufacturers to vertically integrated companies with capabilities in mold fabrication, automated assembly, and metrology. Leading competitors are pursuing strategic partnerships and joint ventures to enhance their global production footprint and develop advanced glass molding solutions for high-growth sectors such as automotive ADAS, medical imaging, and consumer electronics.

Recent years have seen a surge in innovation-driven competition, with companies investing heavily in AI-enabled molding systems, hybrid mold material development, and multi-cavity high-throughput production lines. Firms are also launching custom-engineered molded lenses targeting niche applications such as AR/VR, semiconductor lithography, and laser optics. Mergers and acquisitions are being utilized to gain access to proprietary technologies and expand regional market presence. Additionally, players are aligning with sustainability goals by incorporating lead-free glass compositions and low-emission molding systems. Intellectual property protection around lens geometries and mold technologies has also become a key competitive factor. Companies that can ensure tight tolerance control, faster production cycles, and material flexibility are strengthening their position within an increasingly quality-sensitive and innovation-driven global market.

Asahi Glass Co., Ltd.

Panasonic Industry Co., Ltd.

HOYA Corporation

Loh Optical Machinery

Canon Inc.

SCHOTT AG

Evaporated Coatings Inc.

Hymite GmbH

Shanghai Optics Inc.

Precision Optics Corporation, Inc.

The Precision Glass Molding Market is increasingly shaped by rapid technological advancements designed to improve product accuracy, production speed, and process sustainability. One of the most impactful innovations is the integration of ultra-high-precision molding systems capable of maintaining sub-micron tolerances and consistent lens surface uniformity. These machines, equipped with real-time process monitoring and adaptive control systems, ensure repeatability and reduce defect rates significantly in high-volume production.

Advanced mold materials such as tungsten carbide composites, fused silica, and nano-coated ceramics are enabling extended mold life and reduced thermal wear during repeated cycles. These innovations contribute to longer production runs and higher yields, particularly in the manufacturing of high-index and chalcogenide glass optics. Automation continues to transform the production line, with robotic handling systems and cleanroom-compatible conveyors reducing human error and increasing throughput.

Additionally, hybrid molding techniques combining traditional molding with glass reflow and laser-assisted shaping are gaining momentum for producing freeform and non-rotationally symmetric optics. AI-powered simulation software is now widely used to model mold behavior, glass flow, and thermal gradients during pressing, allowing engineers to fine-tune production parameters before actual fabrication begins. Multi-cavity mold configurations have also gained popularity, enabling manufacturers to simultaneously produce multiple lens shapes with varying geometries in a single pressing cycle—significantly improving production efficiency across industries such as automotive optics, wearable displays, and medical imaging.

• In March 2023, SCHOTT AG expanded its manufacturing capabilities in Germany with a new precision glass molding line optimized for aspheric lenses, achieving production accuracy of less than 100 nanometers and increasing capacity by 15%.

• In September 2023, Panasonic Industry introduced a precision molding platform integrating AI-driven process control, reducing defect rates by 28% and improving output consistency for automotive sensor optics.

• In February 2024, Shanghai Optics installed a fully automated glass molding unit in its Shenzhen facility, increasing daily lens production volume by 40% while reducing thermal cycling energy consumption by 18%.

• In May 2024, HOYA Corporation launched a new range of freeform molded lenses tailored for wearable AR/VR devices, utilizing hybrid mold materials that extended operational life by 30% under high-temperature conditions.

The Precision Glass Molding Market Report provides a comprehensive analysis across product types, industry applications, regional dynamics, and technological innovation layers. It covers various molded glass lens types including aspheric, freeform, and cylindrical lenses, each with distinct use cases in automotive, consumer electronics, medical, and industrial sectors. The report segments the market by application into categories such as automotive optics, medical imaging, defense systems, AR/VR devices, and laser-based instrumentation. Geographically, the report includes detailed assessments of Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with further insights into top-performing countries such as China, Germany, the United States, and Japan. Each regional analysis focuses on local manufacturing trends, infrastructure development, government support, and end-user demand.

Technological focus areas within the report include the development of AI-powered molding systems, hybrid mold materials, multi-cavity molds, and the use of laser-assisted forming techniques. Additionally, the report evaluates the influence of automation, cleanroom environments, and smart factory integration on production efficiency and precision quality. This study also highlights emerging and niche segments such as molded lenses for LiDAR, wearable optical systems, biomedical sensors, and photonics-based measurement devices. Tailored for strategic decision-makers, the report supports investment planning, market entry analysis, competitive benchmarking, and product development initiatives across the value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1320.8 Million |

|

Market Revenue in 2032 |

USD 10774.17 Million |

|

CAGR (2025 - 2032) |

30% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Asahi Glass Co., Ltd., Panasonic Industry Co., Ltd., HOYA Corporation, Loh Optical Machinery, Canon Inc., SCHOTT AG, Evaporated Coatings Inc., Hymite GmbH, Shanghai Optics Inc., Precision Optics Corporation, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |