Reports

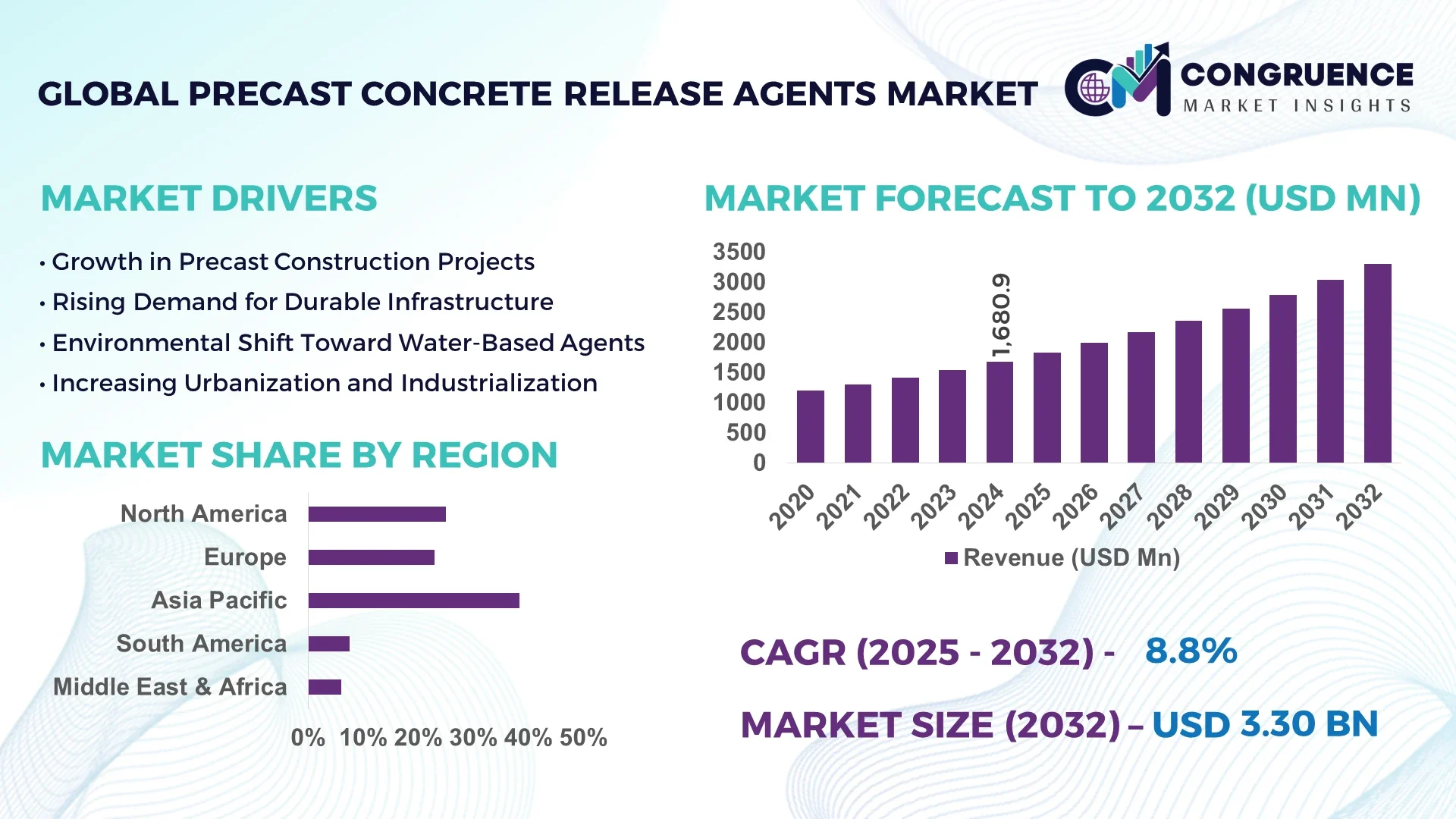

The Global Precast Concrete Release Agents Market was valued at USD 1,680.91 Million in 2024 and is anticipated to reach a value of USD 3,300.48 Million by 2032, expanding at a CAGR of 8.8% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The United States holds a prominent position in the Precast Concrete Release Agents Market due to its advanced construction technologies, substantial infrastructure investments, and strong presence of precast manufacturing plants. Continuous R&D in release agent formulations and automation in application processes further support the country’s industry dominance.

The Precast Concrete Release Agents Market is gaining traction across a variety of sectors such as residential, commercial, and civil infrastructure. These agents are essential for ensuring smooth demolding of precast components, thereby improving surface quality and reducing production defects. Water-based release agents are gaining significant popularity, driven by increasing environmental regulations and sustainability goals. Innovative developments, including biodegradable and solvent-free formulations, are shaping new product lines, particularly in Europe and North America. Additionally, advancements in automation technologies have optimized application processes, reducing material waste and improving operational efficiency. Emerging economies in Asia-Pacific are witnessing rapid adoption due to ongoing infrastructure development and urbanization. The market is expected to benefit from increasing investment in public works and green building initiatives. Demand is further fueled by shifting regulatory standards promoting environmentally safe and VOC-compliant products.

Artificial Intelligence (AI) is revolutionizing the Precast Concrete Release Agents Market by driving operational efficiency, quality assurance, and predictive maintenance within manufacturing and application processes. AI-powered systems enable real-time monitoring of release agent application, ensuring optimal quantity distribution on molds, which minimizes waste and enhances surface finish consistency. Machine learning algorithms are being used to analyze environmental variables such as humidity, temperature, and material composition to determine the most effective type and quantity of release agent for a specific production condition.

AI integration also facilitates process automation, reducing manual labor and human error while accelerating production cycles. Smart dispensing equipment equipped with AI capabilities adapts in real-time to variations in mold material and geometry, ensuring consistent performance. Moreover, AI-driven quality control systems use image recognition to detect imperfections in precast surfaces, allowing for immediate correction and reduced product rejections. In addition, AI tools are helping manufacturers optimize their supply chains by forecasting demand trends, managing inventory levels more accurately, and streamlining logistics operations.

The Precast Concrete Release Agents Market is also benefiting from AI’s role in sustainable practices. Data-driven analytics contribute to the development of eco-friendly formulations by simulating chemical interactions before physical testing, thereby accelerating innovation while minimizing resource use. As construction technologies evolve, AI is proving indispensable in elevating the efficiency and sustainability of the precast concrete industry.

“In 2024, BASF Construction Solutions deployed an AI-powered system within its release agent production facilities, which resulted in a 17% reduction in material wastage and improved consistency in surface quality across large-scale infrastructure projects in Germany.”

Rising global infrastructure investments are a key growth driver in the Precast Concrete Release Agents Market. Rapid urbanization in emerging economies such as India, China, and Brazil is accelerating demand for precast construction components, which in turn boosts the need for efficient release agents. Urban population growth has led to large-scale housing, transportation, and commercial infrastructure projects that rely on the speed and consistency offered by precast systems. Additionally, government-funded programs targeting highway expansions, smart city initiatives, and public utility structures further augment the requirement for high-performance release agents. These agents ensure mold longevity and superior finish, making them indispensable in large-scale, high-volume construction environments. Technological integration, such as automated release agent dispensers, has further enhanced productivity, supporting the continued demand across infrastructure-centric regions.

One of the major restraints impacting the Precast Concrete Release Agents Market is the increasing enforcement of environmental regulations, particularly those targeting volatile organic compounds (VOCs). Solvent-based release agents, traditionally used for their effective performance, are now under scrutiny due to their emissions and adverse environmental impacts. Regulatory agencies in North America and Europe are tightening emissions standards, compelling manufacturers to reformulate or phase out products that fail to meet compliance benchmarks. This transition can be both costly and time-consuming, especially for small to mid-sized companies lacking R&D infrastructure. Moreover, the performance of some water-based alternatives is yet to match the efficiency of solvent-based products under certain conditions, causing reluctance among end-users. The regulatory burden and reformulation demands continue to challenge market players striving to balance performance with environmental responsibility.

The Precast Concrete Release Agents Market is positioned to benefit significantly from the growing demand for environmentally friendly construction materials. Increasing awareness of sustainable building practices is pushing contractors and developers to seek out release agents that are non-toxic, biodegradable, and VOC-compliant. Government initiatives promoting green buildings, especially in developed nations, are creating a favorable environment for water-based and bio-based agent adoption. Moreover, LEED certifications and environmental building standards are incentivizing the use of sustainable materials, opening new avenues for manufacturers offering compliant solutions. Several companies are already investing in research to develop plant-based and polymer-enhanced agents that reduce ecological impact without compromising performance. This transition toward green chemistry offers long-term opportunities for innovation, product differentiation, and increased market penetration across environmentally regulated construction zones.

A significant challenge confronting the Precast Concrete Release Agents Market is maintaining consistent product performance across diverse climatic conditions. In regions with extreme temperature fluctuations or high humidity, the efficacy of certain water-based or eco-friendly agents can diminish, leading to poor mold release, staining, or surface defects. Construction projects in the Middle East, parts of Asia, and sub-zero climates in Europe and North America often encounter such performance variability, affecting project timelines and quality assurance. Manufacturers are under pressure to develop release agents that can adapt to varying environmental factors without compromising ease of application or finish quality. Additionally, supply chain logistics for transporting temperature-sensitive materials present further complexity. Overcoming these technical and environmental hurdles remains a top priority for industry stakeholders aiming for global market expansion and consistent user satisfaction.

• Rise in Modular and Prefabricated Construction: The increasing adoption of modular and prefabricated construction methods is significantly boosting demand within the Precast Concrete Release Agents Market. These construction techniques require fast, efficient mold separation processes to maintain production speed and surface quality. In regions such as Europe and North America, over 35% of new commercial buildings now incorporate prefabricated components. This trend necessitates the use of high-performance release agents compatible with automated formwork systems, further accelerating the need for specialty formulations tailored for mass-scale precast production lines.

• Shift Toward Water-Based and Biodegradable Formulations: Environmental compliance is steering the market toward low-emission, water-based, and biodegradable release agents. Regulatory pressure in the U.S., EU, and parts of Asia is pushing contractors to abandon solvent-based agents. Water-based variants now account for more than 40% of newly manufactured release agents globally. These solutions not only meet sustainability goals but also offer improved worker safety and easier cleanup, which is driving their rapid adoption across municipal and large-scale infrastructure projects.

• Integration of Smart Dispensing Systems: The use of automated and smart dispensing systems in precast factories is rising steadily, improving consistency and reducing material waste. In 2024, over 25% of high-volume precast production plants adopted programmable spray systems that optimize the application of release agents based on mold geometry and environmental conditions. This innovation enhances product efficiency while reducing overspray and operational downtime, presenting cost-saving benefits to manufacturers.

• Custom Formulations for Complex Mold Designs: The rising architectural complexity in commercial and infrastructure projects is prompting a demand for specialized release agents. Custom formulations are increasingly required for intricate mold surfaces to prevent staining, air bubbles, or adhesion failures. These advanced release agents are now used in over 60% of decorative or custom precast projects. Product differentiation based on specific curing times and surface finish quality has become a key competitive factor among market players.

The Precast Concrete Release Agents Market is segmented based on type, application, and end-user verticals, each offering unique growth potential and industrial value. The segmentation by type includes products such as water-based, solvent-based, and bio-based agents, with growing attention on environmentally friendly variants. Applications are spread across civil infrastructure, commercial real estate, industrial plants, and transportation projects, with civil infrastructure leading adoption due to scale and consistency requirements. From an end-user perspective, construction companies, precast manufacturers, and government contractors form the major consumer base. Shifting environmental compliance norms and operational efficiency needs are guiding end-user choices. This segmentation reveals a strong inclination toward automation compatibility, sustainable usage, and sector-specific formulations—driving innovation and strategic investments across the board.

Water-based release agents currently lead the Precast Concrete Release Agents Market, primarily due to increasing environmental regulations and the demand for low-VOC solutions. These agents are preferred in government and public sector construction projects, where safety and ecological considerations are paramount. In 2024, water-based agents were used in more than 50% of new precast operations across urban areas in Europe and North America. Solvent-based agents, while traditionally dominant due to superior performance in challenging mold conditions, are gradually losing share as environmental compliance becomes stricter. Despite this, they maintain relevance in heavy industrial applications and regions with less regulatory oversight. Bio-based release agents are emerging as the fastest-growing category. Their adoption is accelerating, particularly in markets focused on green building certifications and circular economy principles. Although currently limited in scale, they are expected to make notable inroads as product efficacy improves. Hybrid formulations combining water and bio components are also gaining traction for offering a balanced performance profile across varied conditions.

Civil infrastructure represents the leading application in the Precast Concrete Release Agents Market, with large-scale use in bridges, tunnels, highways, and public utilities. These projects demand consistency, durability, and large production volumes—driving bulk usage of high-performance release agents for structural precast elements. Over 45% of release agent consumption in 2024 was attributed to infrastructure projects across developing economies. Commercial building construction is the fastest-growing application area. With urban expansion and smart city initiatives, developers increasingly rely on precast panels for faster completion and architectural precision. This growth is further fueled by a surge in demand for multi-story commercial spaces and institutional buildings. Industrial applications, including warehouses and manufacturing facilities, also contribute significantly. Though more niche, transportation-related structures like railways, sound barriers, and port facilities are seeing rising adoption of precast components, boosting the market need for application-specific agents that ensure seamless demolding without surface flaws.

Precast concrete manufacturers are the leading end-users in the Precast Concrete Release Agents Market. These companies operate high-volume production plants where efficiency, surface finish, and mold reusability are critical. In 2024, this segment accounted for more than half of all release agent purchases, especially in regions with well-established industrialized construction systems. The fastest-growing end-user category is government contractors engaged in public infrastructure development. With increasing allocations toward roadways, sanitation systems, and flood control infrastructure, the reliance on precast solutions is intensifying. Government contracts often mandate environmentally compliant materials, which is pushing the adoption of water-based and biodegradable release agents in this sector. Construction companies, while traditionally reliant on on-site pouring, are progressively shifting toward precast integration, especially for residential and commercial mid-rise buildings. Architectural firms and real estate developers are also emerging as niche end-users, often influencing product selection based on performance, appearance, and environmental certification standards.

Asia-Pacific accounted for the largest market share at 38.4% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

This dominance in Asia-Pacific is largely driven by massive infrastructure projects, rising urbanization, and high demand from China, India, and Southeast Asia. The region’s strong manufacturing base and extensive use of precast elements in commercial and residential developments further enhance consumption. In contrast, South America’s rapid growth is fueled by government investments in public infrastructure and the rising adoption of modular construction. Countries like Brazil and Colombia are emphasizing precast solutions for faster and more cost-effective project delivery. The combination of urban expansion, labor shortages, and technology integration is expected to stimulate higher consumption of precast concrete release agents across these fast-evolving economies.

Innovations in Eco-Formulated Concrete Separators Fuel Industrial Uptake

In 2024, this region held a market share of approximately 26.7%, largely propelled by advanced construction practices and stringent environmental regulations. The demand is heavily concentrated in the United States and Canada, with ongoing investments in highways, bridges, and large commercial structures fueling consistent uptake. Key industries driving market traction include civil infrastructure, institutional construction, and renewable energy. Regulatory frameworks favoring low-VOC and biodegradable materials have accelerated the transition to water-based formulations. Additionally, technological advancements such as automated spraying systems and digital dosing controls are gaining ground, particularly in high-output precast manufacturing facilities. The focus on reducing labor time and improving precision continues to reshape market dynamics, positioning eco-innovation as a competitive edge in this developed region.

Green Compliance Drives Next-Gen Concrete Release Formulations

Europe accounted for 21.3% of the global market in 2024, driven by progressive sustainability initiatives and strict EU directives on construction materials. Germany, France, and the United Kingdom are the leading contributors, where precast usage is highly integrated into both public and private sector developments. European regulatory bodies emphasize eco-labeled materials and reduced chemical emissions, making water-based and biodegradable release agents the preferred choice. Construction firms are increasingly investing in robotic spray systems and sensor-driven monitoring to meet quality standards and minimize waste. Moreover, the EU Green Deal and national carbon-neutral targets are encouraging rapid innovation in concrete formulation and application methods, pushing the market toward advanced product diversification and circular construction models.

Urban Growth and Mass Infrastructure Spur Industrial Adoption

Asia-Pacific leads the global market with the highest volume of precast concrete release agents consumed in 2024, accounting for 38.4% of total usage. China, India, and Japan are the top three consumers, propelled by urban mega-projects, smart city programs, and growing reliance on prefabricated construction techniques. In China alone, hundreds of new metro stations and high-speed rail projects require efficient mold release solutions. The rise of industrial corridors and Special Economic Zones (SEZs) in India further intensifies demand. Regional innovation hubs are also driving change, with startups in South Korea and Singapore developing AI-powered dispensing tools and bio-derived formulations. These technological enhancements are enabling faster mold turnover and better surface finishes, aligning with the region’s need for high-speed, high-volume construction execution.

Public Works Expansion Boosts Need for Efficient Mold Separation

Brazil and Argentina are the primary markets in South America, with Brazil commanding the largest regional market share at 6.2% in 2024. Public infrastructure programs—especially in transportation and sanitation—are fueling demand for cost-effective and fast-to-apply release agents. Government-backed housing projects and commercial real estate expansions are increasingly shifting toward precast components, necessitating reliable separation solutions. Trade policies favoring green imports and regional trade alliances are facilitating easier access to high-performance water-based agents. Additionally, there is a growing trend of public-private partnerships (PPPs) adopting digital platforms to improve procurement and construction management, which indirectly supports the uptake of more technologically advanced release agents.

Construction Growth and Energy Investment Power Market Demand

Construction activity across the UAE, Saudi Arabia, and South Africa is driving consistent demand in this region. In 2024, the region contributed to 7.4% of global precast concrete release agent consumption, with growth supported by megaprojects like NEOM and large oil & gas infrastructure developments. High-temperature conditions in the Middle East require specialized release agents that prevent premature evaporation and maintain mold integrity. Governments are increasingly mandating low-emission materials in alignment with Vision 2030 and similar national frameworks. Additionally, there is rising interest in locally manufactured, cost-effective alternatives due to import duties and supply chain considerations. Digitization is gaining momentum, particularly in the UAE, where BIM and smart construction tools are being integrated into precast workflows, promoting the use of precision dispensing technologies.

China – 24.8% market share

High production capacity and rapid urban infrastructure development drive China's dominance in the precast concrete release agents market.

United States – 18.3% market share

Strong end-user demand from commercial and civil infrastructure sectors, coupled with regulatory compliance for eco-friendly materials, secures its top position.

The Precast Concrete Release Agents market features a dynamic and moderately fragmented competitive landscape with over 100 active participants globally. Key industry players are investing heavily in product innovation, particularly in water-based and environmentally compliant formulations. These advancements aim to meet the increasing demand for eco-friendly construction chemicals driven by stringent environmental policies in North America and Europe. Strategic initiatives such as regional expansion, mergers, and technology licensing agreements are becoming more prevalent. Several top-tier manufacturers are collaborating with construction equipment suppliers to develop integrated release agent solutions that enhance efficiency and surface quality. Additionally, innovation trends such as nano-enhanced agents, automation in application techniques, and IoT-enabled monitoring of release agent performance are influencing competitive dynamics.

A notable trend is the increasing focus on vertical integration, with some companies extending their services from production to direct application and after-sales support. This integrated value proposition strengthens brand loyalty and provides a competitive edge. With regional variations in construction methods and regulatory frameworks, localized product customization is also being leveraged by major players to secure market dominance in emerging economies.

BASF SE

W. R. Meadows, Inc.

Sika AG

Fuchs Lubritech GmbH

MC-Bauchemie Müller GmbH & Co. KG

Evonik Industries AG

Nox-Crete Inc.

Henkel AG & Co. KGaA

Vandex International Ltd.

Fosroc International Ltd.

Technological advancements are significantly reshaping the Precast Concrete Release Agents market, emphasizing sustainability, efficiency, and precision. A prominent trend is the shift towards eco-friendly formulations. Manufacturers are increasingly developing water-based and biodegradable release agents to comply with stringent environmental regulations and meet the growing demand for sustainable construction practices. These formulations reduce volatile organic compound (VOC) emissions, enhancing worker safety and minimizing environmental impact. Nanotechnology integration is another transformative development. Nano-enhanced release agents offer superior coverage and durability, often requiring lower application rates. The nanoparticles create a more uniform barrier between the concrete and the formwork, resulting in easier release and fewer surface blemishes. This advancement not only improves the quality of precast concrete products but also contributes to cost savings by reducing material usage and labor.

Digitalization and smart manufacturing are also influencing the market. The adoption of Internet of Things (IoT) devices and automation in the application of release agents ensures consistent quality and optimizes production processes. Smart application systems can adjust the amount and type of release agent in real-time based on specific conditions, enhancing efficiency and reducing waste. Furthermore, the development of customizable release agent solutions tailored to specific project requirements is gaining traction. Manufacturers are offering products that can be adjusted in terms of viscosity, drying time, and release strength to suit different types of formwork and concrete mixes. This customization allows for optimal results across diverse applications, from intricate architectural elements to large structural components. These technological innovations are collectively driving the evolution of the Precast Concrete Release Agents market, aligning it with modern construction demands and environmental considerations.

In August 2024, Gerdau Graphene introduced NanoCONS, a graphene-based admixture for precast concrete. This innovation enhances concrete strength and durability, reduces porosity, and cuts water consumption by up to 20%, while also accelerating setting time by 30%, facilitating faster construction.

In July 2024, Wells, a U.S.-based provider of prefabricated building solutions, acquired GATE Precast. This acquisition aims to extend Wells' geographic footprint and broaden its range of prefabricated building products, strengthening its capabilities in delivering comprehensive building solutions across multiple sectors.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In May 2023, a leading manufacturer launched a new line of water-based release agents designed for high-performance applications. These agents offer improved release properties, reduced surface defects, and are compliant with the latest environmental regulations, catering to the evolving needs of the construction industry.

The Precast Concrete Release Agents Market Report provides a comprehensive analysis of the industry's full value chain, examining product types, end-user industries, application domains, and regional dynamics. It focuses on key segments including barrier release agents and reactive release agents, with specialized insights into water-based and solvent-based formulations. The report evaluates how each type performs across different concrete surfaces, molding techniques, and environmental conditions. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Particular attention is given to top-performing countries such as the United States, China, Germany, India, and Brazil, where robust infrastructure growth, manufacturing expansion, and government incentives are reshaping market demand. Regional market share data and qualitative trends are included to guide market entry and expansion strategies.

From an application standpoint, the report covers key sectors including architectural components, structural building elements, transportation infrastructure, and utility-based precast segments. The construction industry's growing demand for efficiency and aesthetic finish quality has fueled adoption in commercial, industrial, and residential building sectors. Technology-wise, the report outlines advancements in nanotechnology, biodegradable compositions, and smart application systems. It also touches on innovations in form-release automation and environmentally compliant materials. Additionally, the report evaluates emerging opportunities in niche areas such as 3D-printed formwork and high-performance precast concrete used in modular and green buildings. In essence, this report serves as a strategic tool for stakeholders, offering actionable insights across production, application, technological development, and regional performance within the global Precast Concrete Release Agents landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1680.91 Million |

|

Market Revenue in 2032 |

USD 3300.48 Million |

|

CAGR (2025 - 2032) |

8.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, W. R. Meadows, Inc., Sika AG, Fuchs Lubritech GmbH, MC-Bauchemie Müller GmbH & Co. KG, Evonik Industries AG, Nox-Crete Inc., Henkel AG & Co. KGaA, Vandex International Ltd., Fosroc International Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |