Reports

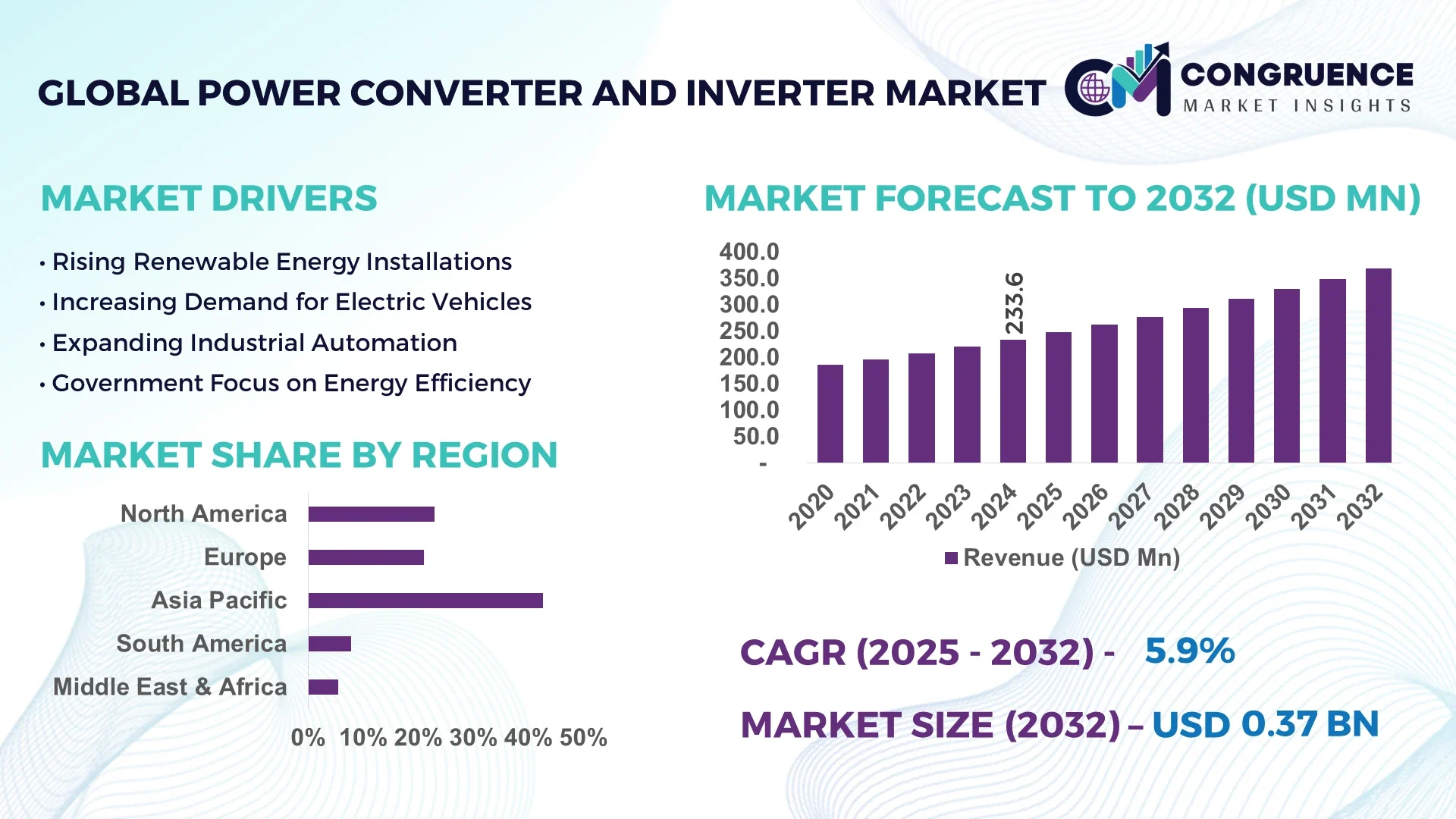

The Global Power Converter and Inverter Market was valued at USD 233.6 Million in 2024 and is anticipated to reach a value of USD 369.5 Million by 2032 expanding at a CAGR of 5.9% between 2025 and 2032.

China leads the global market in power converters and inverters, boasting production capacity exceeding 1 GW daily for solar inverters alone. Manufacturers in China have committed hundreds of millions in R&D to develop next-gen silicon carbide (SiC) and gallium nitride (GaN) semiconductor devices. Key applications include utility-scale photovoltaic systems, electric vehicle charging infrastructure, and industrial motor drives. Technological advancements include grid-interactive inverters with advanced control firmware enabling real-time voltage supportive functions.

The Power Converter and Inverter Market spans several key sectors: solar PV systems (accounting for approximately 60% of unit shipments), industrial automation (VFD-driven motor control), UPS for data centers, and EV charging networks. Recent innovations include integration of wide-bandgap semiconductors, boosting conversion efficiency from ~90% to beyond 98%, and development of smart inverters with remote monitoring and predictive maintenance capabilities—leading to reductions of up to 20% in maintenance downtime. Regulatory and environmental drivers—such as renewable portfolio standards, grid-code mandates, and net-zero targets—are accelerating market uptake, especially in APAC and North America. Regional consumption patterns show Europe and North America demanding high-precision, compliance-ready inverters, while Asia-Pacific focuses on large-scale utility deployment. Emerging trends include the move toward modular and prefabricated inverter systems to match modular solar panel arrays, and increasing demand for integrated power conversion modules tailored for EV throttle control and charging. Overall, the market outlook is robust, driven by electrification, decarbonization, and continued semiconductor innovation.

Artificial Intelligence is redefining the Power Converter and Inverter Market by optimizing design, operation, and maintenance processes. AI-driven control algorithms now dynamically adjust switching sequences in power converters to reduce electromagnetic interference and thermal hotspots, improving overall system reliability. In solar and grid-tied inverters, AI systems use real-time weather forecasting and irradiance prediction to maximize energy yield, reporting efficiency gains of up to 20% and reducing unplanned downtime through predictive fault detection.

In industrial settings, machine learning models analyze operational data from inverters used in motor drives and UPS systems to predict component degradation and schedule maintenance before failures occur—decreasing unplanned maintenance events by approximately 30%. These AI applications enhance the operational performance of inverter fleets across distributed sites, enabling centralized control centers to adjust parameters such as reactive power support and harmonics mitigation in real-time, thereby stabilizing grid performance and enhancing power quality.

Advanced Power Converter and Inverter Market offerings now include embedded AI agents that monitor temperature, vibration, and current waveforms, enabling adaptive cooling and leading to measurable improvements in thermal efficiency. Additionally, physics-informed neural networks (PINNs) are being used to refine electromagnetic transient simulations for grid-forming inverters, allowing more accurate digital twins and reducing testing cycles. This shift toward AI-enhanced systems supports faster ramp time, robust fault tolerance, and improved lifecycle management—all critical to the demands of renewable energy and electrification strategies.

“In June 2024, researchers demonstrated a physics-informed neural network–based ‘AI-inverter’ that reduced simulation time for grid-forming inverter electromagnetic transients by over 50% while maintaining accuracy within 2%, compared to traditional EMTP simulations.”

The Power Converter and Inverter Market Dynamics reflect evolving trends in electrification and clean energy deployment. Increasing integration of solar PV and EV infrastructure is driving adoption of high-efficiency conversion systems. Wide-bandgap semiconductors and smart control platforms enable improved device density and functional performance. The regulatory landscape—from grid-code requirements to renewable mandates—is shaping product compliance and feature sets. Cost pressures from material supply chains and regional manufacturing variances impact pricing strategies and sourcing decisions. Integration of smart grid communication protocols (e.g., IEEE 2030.5, IEC 61850) further influences product development. Environmental factors, such as decarbonization goals and air-quality regulations, are accelerating shifts toward low-loss and low-emission inverter solutions. Overall, the convergence of energy policy, semiconductor progress, and system-level digitization underlies a rapidly evolving market environment.

The build-out of solar photovoltaic (PV) and wind generation capacities fuels demand for robust power converters and inverters within the Power Converter and Inverter Market. Globally, more than 300 GW of solar PV was added in 2023, pushing the cumulative installed capacity above 1 TW, each reliant on high-performance inverters. Centralized grid-tied systems commonly deploy inverters rated from 200 kW to multiple MW, while residential and commercial installations employ plug-and-play string inverters. As national and corporate renewable energy targets intensify, procurement of advanced inverters with expanded grid-support functionalities—such as voltage ride-through and reactive compensation—is on the rise. These systems also fulfill requirements related to smart metering and energy export control, enhancing resilience and supporting firm renewables integration.

Incorporating SiC and GaN semiconductors into power converter and inverter designs significantly raises component and manufacturing costs. SiC devices can cost up to three times more than silicon-based equivalents, and complex packaging increases production overhead. These elevated costs limit penetration in cost-sensitive sectors or emerging economies where price is a key purchase determinant. Furthermore, critical supply chain dependencies—such as raw-material concentration and conversion yield challenges—add uncertainty. As a result, many manufacturers continue to depend on conventional silicon technologies, potentially dampening performance improvements and inhibiting widespread adoption of next-generation, energy-efficient inverter platforms.

The rapid expansion of electric vehicle ecosystems offers a strategic growth avenue for the Power Converter and Inverter Market. Vehicle-to-grid (V2G) capable inverters and chargers enable two-way energy flows, allowing EV fleets to function as distributed storage assets. In markets where EV registrations exceeded 26 million units by 2024, demand is rising for integrated converter-inverter-battery management systems that can support grid services such as peak shaving and frequency regulation. AI-enabled controllers optimize battery temperature and lifecycle performance. Standardized modules enabling interoperability across EV brands and grid protocols further expand addressable markets and drive large-scale deployments in residential, commercial, and public charging infrastructure.

Power Converter and Inverter Market deployment faces significant challenges due to inconsistent global regulatory frameworks. Grid connection requirements vary across jurisdictions, with diversely mandated communication protocols like Modbus, SunSpec, and IEC standards. Achieving compliance necessitates unit-by-unit certification, increasing development time and cost. Moreover, cyber-security mandates for grid-connected inverters are evolving rapidly, posing additional testing and validation burdens. This fragmentation limits product scalability, elongates time-to-market for new models, and increases engineering overhead for manufacturers aiming to enter multiple geographic markets.

Smart Inverters with Grid-Interactive Intelligence: Deployment of smart inverters capable of bi-directional power flow and grid support is increasing. In the U.S. and EU, installations with advanced firmware that enable voltage regulation and frequency support now constitute over 55% of new inverter deployments, reflecting stronger grid-code enforcement and modernization efforts.

Efficiency Gains from Wide-Bandgap Semiconductors: New inverters leveraging SiC and GaN technologies are achieving conversion efficiencies above 98.5%, compared to older silicon systems. This improvement reduces energy losses by more than 30% annually in high-utilization applications like utility-scale solar and EV charging infrastructure.

Modular, Prefab Power Conversion Systems: Power Converter and Inverter Market customers in Europe and North America increasingly prefer modular, prefabricated conversion units designed for off‑site assembly—reducing on-site installation time by up to 40% and cutting labor costs significantly. These systems are optimized for use in containerized solar or microgrid applications.

AI-Embedded Predictive Maintenance Platforms: Manufacturers now embed AI agents inside inverters to monitor key parameters—vibration, temperature, waveform anomalies. These platforms detect issues like capacitor degradation early, lowering unplanned maintenance by approximately 30%, extending system uptime and enhancing lifecycle cost-efficiency.

The Power Converter and Inverter Market is comprehensively segmented by type, application, and end-user, each offering distinct growth avenues and operational challenges. Product types range from DC-AC inverters and DC-DC converters to multi-level and hybrid topologies. Applications span renewable energy systems, industrial automation, and electric vehicle infrastructure, while end-users include utilities, commercial entities, and residential consumers. The diverse adoption across sectors is driven by demand for energy-efficient power management, enhanced voltage regulation, and system compatibility. Technological advancements like silicon carbide integration and AI-based control systems are impacting each segment differently, particularly influencing inverter types and application scopes. Growing investment in grid modernization and electrification projects further highlights the relevance of analyzing each segment in detail. Understanding these nuances helps stakeholders align product development and deployment strategies to meet evolving regulatory, operational, and sustainability goals.

The Power Converter and Inverter Market comprises various product types including DC-AC inverters, DC-DC converters, AC-DC converters, and hybrid converters. Among these, DC-AC inverters represent the most dominant type, primarily due to their essential role in renewable energy systems, especially solar PV, where direct current from panels must be converted to alternating current for grid integration. Their widespread use in both residential and utility-scale installations underscores their importance.

DC-DC converters are identified as the fastest-growing product category, driven by the surge in electric vehicle (EV) adoption and advancements in battery storage systems. These converters are critical for managing voltage levels across various battery modules, enhancing energy transfer efficiency and safety. Furthermore, DC-DC converters are integral in aerospace and defense systems where compact, high-reliability power solutions are essential.

Other product types like AC-DC converters and hybrid inverters, while niche, are gaining relevance in backup power systems and off-grid renewable applications. Hybrid converters, which support both grid-tied and off-grid modes, are being increasingly integrated into residential solar-plus-storage systems, reflecting a shift toward energy independence and resilience.

In the Power Converter and Inverter Market, renewable energy systems, particularly solar photovoltaic installations, form the leading application segment. The rapid expansion of global solar capacity has necessitated high-efficiency inverters that can handle fluctuating power inputs, ensure grid compliance, and enable real-time energy export control. These systems often demand smart inverters with advanced features like voltage ride-through and remote diagnostics.

Electric vehicle (EV) infrastructure is the fastest-growing application area, underpinned by global policy shifts toward decarbonization and accelerating adoption of e-mobility. EV chargers require bi-directional inverters to support vehicle-to-grid functions, efficient energy transfer, and battery safety protocols. This growth is further supported by government-funded charging network expansions and private sector innovation.

Other applications include industrial automation systems, uninterruptible power supplies (UPS), and telecom base stations. In industrial automation, power converters regulate motor speed and torque, contributing to operational efficiency. UPS systems, particularly in data centers and healthcare facilities, rely on high-reliability inverters to ensure seamless power continuity. These applications contribute steadily to market demand across diverse geographic and economic contexts.

The utility sector represents the leading end-user in the Power Converter and Inverter Market due to large-scale grid modernization initiatives and renewable integration projects. Utilities deploy centralized and distributed inverter systems in solar farms, wind parks, and battery energy storage facilities to stabilize grid voltage, manage reactive power, and enhance load balancing. Their need for grid-compliant, high-performance inverters positions them at the forefront of technology adoption.

The commercial sector, particularly facilities with solar rooftops and EV charging stations, is emerging as the fastest-growing end-user segment. This trend is driven by increased emphasis on sustainability goals, energy cost optimization, and government incentives. Commercial establishments are adopting hybrid inverter systems for backup power and peak load management, especially in retail chains, office campuses, and logistic hubs.

Residential end-users continue to adopt inverters in rooftop solar and home energy management systems, often paired with battery storage. Meanwhile, sectors like manufacturing, defense, and transportation also contribute significantly by integrating converters and inverters into mission-critical and process-intensive environments, where reliability and power quality are paramount.

Asia-Pacific accounted for the largest market share at 42.7% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The Power Converter and Inverter Market demonstrates distinct dynamics across global regions, reflecting unique policy environments, industrial ecosystems, and technology adoption curves. Asia-Pacific leads the market, driven by massive investments in solar power installations, EV production, and grid modernization initiatives. China, India, and Japan continue to dominate demand, especially in utility-scale and manufacturing applications. Meanwhile, North America is witnessing accelerated growth due to widespread adoption of EV infrastructure, net-zero commitments, and digital grid upgrades. Europe follows closely, supported by strong regulatory mandates and cross-border energy integration. South America and the Middle East & Africa, though smaller in current scale, are showing robust adoption potential due to energy diversification goals and infrastructure investments. Regional governments, through various incentive programs and trade collaborations, are actively shaping the competitive landscape of the Power Converter and Inverter Market.

North America accounted for approximately 21.3% of the Power Converter and Inverter Market in 2024. The market is being driven by rapid electric vehicle adoption, especially in the U.S. and Canada, with charging infrastructure expansion requiring efficient and bi-directional inverters. Additionally, the boom in hyperscale data centers across the U.S. necessitates high-capacity uninterruptible power supply systems and precision inverters for consistent power delivery. Governmental programs such as federal clean energy incentives and state-level mandates are supporting inverter and converter deployment across solar and smart grid sectors. Technological developments in AI-integrated smart inverters and the implementation of real-time monitoring systems are further modernizing power management across industries. The trend toward electrified transport fleets and decentralized energy systems positions North America as a high-growth, innovation-driven regional market.

Europe held a market share of approximately 18.5% in 2024, with Germany, France, and the UK being the key contributors to regional demand. This growth is heavily influenced by the European Green Deal, carbon neutrality targets, and smart grid deployment mandates. Regulatory bodies like the European Commission and ENTSO-E have introduced technical requirements for inverter-based resources to stabilize renewable-powered grids. There is a significant uptick in the adoption of hybrid and multi-level inverter technologies in residential solar applications and EV charging. Europe is also witnessing increased R&D in silicon carbide–based systems for industrial converters, enabling lower heat loss and higher operational efficiency. Cross-border energy interconnections and storage-backed renewables are intensifying demand for grid-compliant power conversion units across the continent.

Asia-Pacific remained the largest regional market by volume in 2024, accounting for 42.7% of total global share. China leads consumption due to its vast solar panel manufacturing ecosystem, national energy transition policies, and dominant role in global EV production. India is experiencing rapid adoption of solar inverters under its National Solar Mission and Smart Cities initiatives. Japan continues to invest in advanced converter solutions for both residential and industrial renewable applications. The region benefits from localized production of components, competitive pricing, and government-backed infrastructure development. Innovation hubs in South Korea and Taiwan are advancing integrated converter-inverter chipsets, enabling miniaturization and real-time control. As APAC economies continue to electrify their energy, transport, and manufacturing sectors, the region will remain the primary production and consumption base for power conversion technologies.

South America captured 7.4% of the global Power Converter and Inverter Market in 2024, with Brazil and Argentina leading demand. Brazil’s booming utility-scale solar sector and expansion of wind farms require high-performance inverters with advanced grid-forming functionalities. The country's public-private partnerships in energy storage and electric mobility also support market growth. Argentina is focusing on modernizing its grid through digital substations and rural electrification programs, prompting demand for modular converter systems. Trade policies favoring renewable equipment imports and tax incentives for green investments are improving technology accessibility. Although smaller in scale, South America represents an emerging market with growing reliance on smart energy infrastructure and cleaner electricity distribution networks.

The Middle East & Africa region contributed approximately 10.1% to the Power Converter and Inverter Market in 2024. Countries such as the UAE and South Africa are leading regional adoption, supported by national infrastructure plans like Vision 2030 and Just Energy Transition Partnership respectively. Demand is particularly strong across the oil & gas, construction, and utility sectors. In the Gulf region, smart city projects and district cooling systems are increasing demand for high-efficiency power converters in HVAC and distributed energy systems. Africa is investing in off-grid solar and microgrid projects, where modular inverters play a crucial role in ensuring power reliability. Technological modernization, such as mobile-based remote inverter diagnostics and blockchain-integrated energy metering, is gaining momentum. Regulatory partnerships and intra-regional trade agreements are further enabling access to advanced power conversion solutions.

China – 34.6% Market Share

High production capacity, robust manufacturing infrastructure, and dominant solar deployment ecosystem solidify China’s leadership in the Power Converter and Inverter Market.

United States – 18.2% Market Share

Strong end-user demand from EV charging networks, data centers, and grid-interactive renewables makes the U.S. a critical growth hub for power converters and inverters.

The Power Converter and Inverter Market is characterized by a moderately consolidated competitive landscape, featuring over 40 key players actively operating across various verticals and regional markets. These companies range from large multinational power electronics manufacturers to specialized firms focusing on niche segments such as off-grid inverters, high-frequency converters, or grid-tied solar applications. Market leaders are distinguished by their global manufacturing presence, advanced R&D capabilities, and diverse product portfolios.

Strategic initiatives such as joint ventures, technology licensing, and collaborative R&D programs are being increasingly adopted to enhance market positioning and meet evolving industry standards. Product innovation is a critical differentiator, with companies investing in digital twin technologies, GaN and SiC-based converters, and AI-integrated inverter systems for predictive diagnostics and energy optimization. Recent years have seen increased M&A activity aimed at portfolio expansion and regional penetration, particularly in Asia-Pacific and North America. Firms are also targeting Industry 4.0 verticals like EV charging infrastructure, smart grids, and industrial automation, further intensifying competition. Sustainability and compliance with regional energy efficiency standards are becoming key benchmarks in competitive differentiation.

ABB Ltd.

Siemens AG

Huawei Technologies Co., Ltd.

Schneider Electric SE

Delta Electronics, Inc.

Eaton Corporation plc

SMA Solar Technology AG

TDK Corporation

Mitsubishi Electric Corporation

Yaskawa Electric Corporation

Fuji Electric Co., Ltd.

Toshiba Energy Systems & Solutions Corporation

Hitachi Energy Ltd.

Emerson Electric Co.

Sungrow Power Supply Co., Ltd.

The Power Converter and Inverter Market is undergoing rapid technological evolution, driven by the integration of high-efficiency components, real-time monitoring, and digital automation capabilities. A significant trend is the transition from silicon-based semiconductors to wide bandgap materials like silicon carbide (SiC) and gallium nitride (GaN), which offer superior thermal performance, faster switching, and higher power density. These components are enabling more compact, efficient, and lightweight inverter systems for automotive, aerospace, and industrial applications.

Advanced control algorithms and digital signal processors (DSPs) are now commonly embedded in inverter architectures to support variable voltage, frequency modulation, and grid synchronization in distributed energy systems. The rise of smart inverters, capable of bidirectional power flow and remote diagnostics, is transforming their role from passive devices to dynamic grid-balancing tools. In addition, modular converter systems and multi-level topologies are gaining traction in high-voltage direct current (HVDC) transmission and large-scale renewables integration.

Wireless connectivity and IoT integration are further empowering remote performance monitoring, predictive maintenance, and energy usage analytics, aligning with Industry 4.0 standards. Developments in battery storage inverters, microinverters, and hybrid inverter technologies are facilitating the decentralization of energy and enhancing resilience in off-grid and backup systems. As electrification accelerates globally, the market continues to prioritize innovations that support high-efficiency, low-loss, and intelligent power conversion solutions across sectors.

In April 2024, Siemens launched a new generation of modular inverters designed for data centers and industrial automation, supporting high-efficiency cooling and real-time load balancing across critical applications.

In February 2024, Delta Electronics unveiled a three-phase hybrid inverter compatible with solar-plus-storage systems, aimed at enhancing performance in both residential and commercial environments.

In October 2023, Schneider Electric introduced a digitally enabled inverter platform with embedded AI for grid management, offering predictive fault detection and advanced grid stabilization features.

In May 2023, ABB expanded its solar inverter production in India, adding a 200 MW capacity line to meet rising demand in utility-scale and rooftop PV markets across Asia-Pacific.

The Power Converter and Inverter Market Report provides a comprehensive analysis of the market's breadth across multiple dimensions including product type, application, technology, end-user industries, and geographic regions. The study covers a wide array of converter types such as DC-DC, AC-DC, and DC-AC inverters, along with hybrid and modular variants tailored for specific industrial and residential needs.

Key applications analyzed include renewable energy systems, automotive electrification, industrial automation, aerospace power management, and consumer electronics. The report also focuses on the adoption of emerging technologies like SiC/GaN semiconductors, digital twins, smart grid integration, and AI-enabled inverters that are shaping the future of power electronics.

Geographically, the market is segmented into five major regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each region is evaluated based on local demand trends, regulatory dynamics, infrastructure development, and technological maturity. Special emphasis is placed on growth hotspots such as China, the U.S., India, Germany, and the UAE.

In addition to mainstream segments, the report also explores niche and emerging sectors such as off-grid rural electrification systems, EV fast-charging inverters, and aerospace-grade power converters. This provides stakeholders with an in-depth strategic understanding of opportunities, challenges, and innovation trends shaping the global market environment.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 233.6 Million |

| Market Revenue (2032) | USD 369.5 Million |

| CAGR (2025–2032) | 5.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Drivers & Challenges, Segmental Analysis, Regional Outlook, Competitive Landscape, Technology Developments, Recent Trends |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ABB Ltd., Siemens AG, Huawei Technologies Co., Ltd., Schneider Electric SE, Delta Electronics, Inc., Eaton Corporation plc, SMA Solar Technology AG, TDK Corporation, Mitsubishi Electric Corporation, Yaskawa Electric Corporation, Fuji Electric Co., Ltd., Toshiba Energy Systems & Solutions Corporation, Hitachi Energy Ltd., Emerson Electric Co., Sungrow Power Supply Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |