Reports

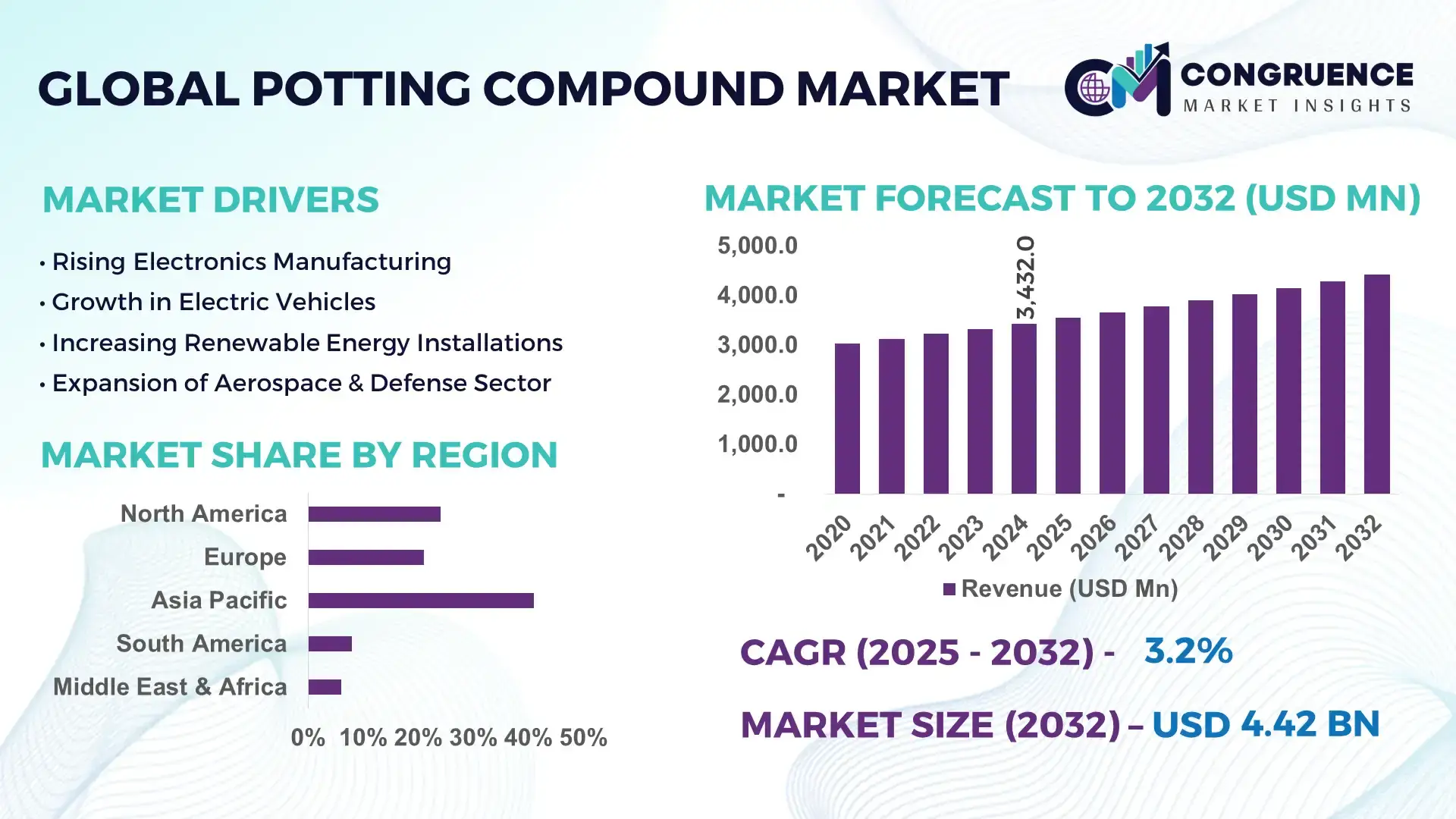

The Global Potting Compound Market was valued at USD 3,432.0 Million in 2024 and is anticipated to reach a value of USD 4,415.6 Million by 2032, expanding at a CAGR of 3.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is underpinned by rising demand for miniaturized and high‑reliability electronic devices.

China plays a central role in the potting compound market: it hosts one of the largest production capacities globally, with several chemical giants investing over USD 500 million in resin and curing‑agent facilities in recent years. The country’s potting compounds are widely used in high-growth sectors such as electronics, EV power modules, and renewable energy inverters. China has introduced advanced UV-curable and thermally conductive formulations, producing over 1,200 kilotons of resin in 2024, and expanding automated potting lines across its major manufacturing hubs.

Market Size & Growth: The market stood at USD 3,432.0 Million in 2024, projected to grow to USD 4,415.6 Million by 2032 at a CAGR of 3.2%, driven by increasing demand from consumer electronics and EV applications.

Top Growth Drivers: Electronics miniaturization (45%), EV and power module sealing (35%), renewable energy systems insulation (20%).

Short‑Term Forecast: By 2028, adoption of high-precision automated dispensing is expected to improve potting process yield by 15%.

Emerging Technologies: UV‑curable potting compounds, thermally conductive silicone resins, and bio‑based low-VOC formulations are gaining traction.

Regional Leaders: Asia‑Pacific expected to reach USD 2,200 M by 2032 (major manufacturing base); North America to hit USD 900 M (driven by EVs); Europe to achieve USD 750 M (prefers eco‑friendly and high-performance formulations).

Consumer/End‑User Trends: Key end-users include consumer electronics (PCBs, smart devices), automotive power modules (inverters, BMS), and industrial automation (motors, sensors) using potting compounds for insulation and mechanical protection.

Pilot or Case Example: In 2025, a major EV OEM in Germany ran a pilot using UV‑curable potting resin, reducing cure time by 40% and downtime by 12%.

Competitive Landscape: Market leader estimated around 18–20%, followed by Henkel, 3M, Momentive, and Dymax.

Regulatory & ESG Impact: Stricter low‑VOC regulations in the EU, along with incentives for recyclable compounds, are pushing adoption of greener potting materials.

Investment & Funding Patterns: Over USD 250 M in investments in automated potting lines and R&D in 2024; growth in joint‑ventures between resin producers and semiconductor firms.

Innovation & Future Outlook: Integration of smart dispensing systems, AI‑driven cure optimization, and next-gen bio‑resins is expected to redefine process efficiency and sustainability by 2030.

Potting compound demand is increasingly shaped by advanced-formulation innovations, regulatory shifts toward eco‑friendly materials, and rising automation and AI integration in manufacturing, creating a robust platform for future growth.

The potting compound market spans key sectors such as consumer electronics, EVs, aerospace, and industrial automation. Innovations like UV‑curable and thermally conductive resins are becoming standard. Environmental drivers such as VOC regulation, and economic incentives are pushing high‑performance bio‑based resins. Regional consumption is shifting: Asia‑Pacific for manufacturing volume, Europe for green formulations, and North America for EV-related potting. Emerging trends include AI‑optimised dispensing, low‑emission resins, and modular potting solutions.

The strategic relevance of the potting compound market lies in its role as a fundamental enabler for the protection, longevity, and reliability of high-value electronic systems. As devices become smaller and more powerful, the risk of thermal stress, vibration, and moisture damage increases — potting compounds address these challenges by providing robust insulation. For business strategy, this makes potting materials not just a consumption input, but a mission‑critical component for electronics manufacturers, EV OEMs, and renewable energy firms.

Looking ahead, the adoption of UV‑curable resins delivers up to 40% faster curing times compared to traditional thermal-cure compounds, significantly improving line throughput. Meanwhile, thermally conductive silicones offer up to a 30% improvement in heat dissipation versus standard epoxy systems, enhancing the thermal management of power modules. Currently, Asia-Pacific dominates in production volume, while Europe leads in adoption of low-VOC and high-performance biodegradable formulations, with over 60% of enterprises in EU countries piloting greener potting solutions.

In the next 2–3 years, AI-driven dispensing systems are expected to reduce material waste by 12% and improve process accuracy by 8%, driven by data‑feedback loops optimizing resin volume and curing parameters. Firms are also committing to ESG targets: by 2028, major manufacturers aim to recycle or reuse 25% of potting compound waste, aligned with broader circular‑economy goals.

In China, for example, one large capacitor manufacturer applied AI‑augmented potting lines in 2025 and realized a 10% reduction in curing energy consumption, while maintaining reliability standards. This micro‑scenario illustrates how technology integration and sustainability can co‑drive returns.

Overall, the potting compound market is poised to be a pillar of resilience — merging high-reliability performance, compliance with ESG goals, and operational excellence. As high-growth end‑user sectors scale, potting compounds will continue to secure their place as a sustainable, high-value material in the electronics and power ecosystems.

The Potting Compound Market is being shaped by a confluence of technological, regulatory, and end‑use shifts. Demand is increasingly driven by the miniaturization of electronics, growth in electric vehicles, and expansion in renewable energy infrastructure. At the same time, manufacturing processes are evolving with increased automation, leading to higher precision in dispensing and curing of potting compounds. Environmental pressures and regulatory frameworks are pushing material innovation: companies are investing in low-VOC, bio-based, and thermally efficient formulations. Supply chain dynamics, particularly for resin precursors, also influence pricing and capacity planning, while globalization of manufacturing bases (especially in Asia-Pacific) continues to drive regional production scale. This combination of evolving demand, technological innovation, and sustainability focus is anchoring potting compounds as a critical material for modern electronics and power systems.

The surge in electric vehicles and power module applications is a major catalyst. Potting compounds are essential for encapsulating high-voltage battery modules, power inverters, and sensors — offering insulation, thermal management, and mechanical protection. As EV production increases globally, demand for electrically insulating, thermally conductive potting materials has grown strongly: power electronics manufacturers report that potting usage per vehicle has increased by approximately 20–25% over the last two years. This rising utilization, especially in high‑voltage systems, is driving volume growth and innovation in high‑performance resins.

Volatility in precursor chemicals (such as epoxy monomers, silicones, and isocyanates) is squeezing margins for compound producers. Energy costs and petrochemical feedstock prices have increased by 15–25% in recent cycles, translating into higher manufacturing costs. For smaller potting‑compound manufacturers, securing stable supply agreements or hedging these inputs has become more difficult. These price pressures may limit their ability to invest in R&D or scale production, especially for niche formulations like bio-based or UV-curable resins, potentially slowing down innovation in some segments.

There is a growing opening for sustainable and bio-based potting compounds. As regulatory bodies tighten VOC emission standards and end-users demand cleaner products, manufacturers are developing low-VOC or bio‑resin formulations. These greener variants not only align with ESG goals but also appeal to industries such as consumer electronics and automotive, which are increasingly emphasizing eco-conscious materials. Adoption of such formulations can also position companies to receive green‑finance funding or ESG-linked investments, creating a strategic growth lever for formulators.

Developing and scaling UV-curable or thermally conductive potting compounds involves significant R&D and capital investment. These formulations often require specialized photoinitiators, fillers, or curing agents that can raise costs. In addition, integrating UV-curing equipment into existing production lines demands CAPEX and new process validation. This challenge is compounded by long qualification cycles for critical applications like EV power modules or aerospace, where reliability standards are stringent. As a result, many manufacturers are cautious in fully shifting to these advanced systems, which slows broader adoption.

Rapid Automazione of Dispensing Processes: The adoption of automated potting systems has surged — more than 45% of manufacturing lines globally integrated robotics for precision dispensing in 2024, reducing material waste by up to 12% and increasing throughput by 18%.

Proliferation of Low‑VOC and Bio‑Resins: Green formulations are gaining traction, with usage of low‑VOC or bio‑based potting compounds rising by ~30% year-over-year, driven by environmental regulations and ESG initiatives.

Rise of Thermally Conductive Compounds: Demand for thermally conductive potting materials increased ~25%, particularly in EV power electronics, where heat dissipation is critical for performance and longevity.

Expansion of UV‑Curing Technology: UV‑curable potting resins are now being adopted by over 40% of high-volume electronics manufacturers, delivering cure times that are up to 40% faster than traditional thermal curing methods.

The global Potting Compound Market is segmented across multiple dimensions to reflect the diversity of chemistries, applications, and end users. In terms of type, the market includes epoxy, silicone, polyurethane, polyester, and other specialized resins. From an application perspective, potting compounds are used in electronics, automotive, aerospace, industrial, and medical sectors. End-users comprise consumer electronics, electric vehicles, renewable energy systems, aerospace & defense, and other niche industries. These segments demonstrate how potting compounds are tailored to meet demanding requirements such as electrical insulation, vibration damping, and thermal management in different contexts. Decision-makers benefit from this detailed segmentation to strategically target high-value markets and optimize formulations for specific end-use needs.

The leading type of potting compound is epoxy-based, capturing around 42% of the global market, owing to its excellent mechanical strength, strong adhesion, and reliable electrical insulation. Epoxy resins remain the backbone of many traditional applications, particularly in electronics and power modules, because they offer a robust balance of cost and performance. The fastest-growing type is silicone-based potting compounds, with a projected growth rate of ~6.8%, driven by their superior temperature resistance (from –65 °C to +200 °C), flexibility, and UV stability. These properties make silicones especially attractive for automotive under‑hood electronics, aerospace units, and outdoor systems exposed to extreme environments. Other types include polyurethane (approximately 18–20% share), known for its flexibility and vibration damping, and acrylic or polyester formulations which serve niche needs such as UV‑curable systems or low-cost bulk sealing. Combined, these other resin types make up the remaining ~40% of the market.

Among applications, electronics dominate, accounting for roughly 38% of the global potting compound usage. This is because potting compounds are crucial to protecting delicate electronic circuits, PCBs, and high-frequency modules from moisture, shock, and vibration. The fastest-growing application is automotive, driven by the rapid adoption of electric vehicles and the increasing electronic content in modern cars. This growth is spurred by demand for high-reliability encapsulation in battery management systems, inverters, sensors, and ADAS modules. Other application areas include industrial equipment, aerospace, medical devices, and renewable energy, which together make up the remaining share. For example, more than 30% of global potting compound consumption is used in industrial and aerospace applications where resistance to vibration and harsh conditions is required. On the consumer adoption front, in 2024 over 60% of electronics manufacturers reported integrating potting compounds into miniaturized IoT modules to improve durability. Meanwhile, EV OEMs in North America and Europe disclosed that more than 25% of newly launched models now use thermally conductive potting materials in their inverters.

In terms of end users, consumer electronics lead the pack, holding around 35% of the market. This share is driven by the high volume of devices like smartphones, wearables, and smart-home products, all of which require potting compounds for protection against moisture, drop, and vibration. The fastest-growing end‑user segment is electric vehicles (EVs), with a projected growth rate of around 9.3%, as automakers increasingly use potting compounds in battery modules, inverters, and power electronics to ensure thermal stability and electrical insulation under harsh driving conditions. Other end-users include renewable energy (solar inverters, wind converters), aerospace & defense, and medical devices, which together account for the remaining ~30% of usage. For instance, in renewable energy, potting compounds are critical for weather‑resistant encapsulation of power conversion systems. From a consumer adoption perspective, in recent years over 40% of EV companies globally have publicly stated that they are scaling up potting compound use in their powertrain modules. In the medical sector, 25% of devices released in 2024 used silicone or hybrid potting formulations to meet biocompatibility and thermal constraints.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.2% between 2025 and 2032.

In 2024, Asia-Pacific recorded a market volume exceeding 1,400 kilotons, with China contributing over 950 kilotons alone. Japan and India consumed approximately 210 kilotons and 180 kilotons, respectively. Increasing industrialization, rapid EV adoption, and large-scale electronics manufacturing in this region are driving significant demand. Technological innovations, including thermally conductive and UV-curable formulations, are being integrated across factories. Regional consumer trends show a preference for high-performance, durable potting compounds suitable for harsh environmental conditions, while government initiatives are facilitating R&D investments exceeding USD 500 million across manufacturing hubs.

North America accounted for 27% of the global potting compound market in 2024, driven primarily by high adoption in the automotive, electronics, and renewable energy sectors. The region benefits from government incentives promoting EV manufacturing and clean energy projects. Technological advances such as AI-driven dispensing systems and digital curing processes are optimizing production efficiency and material utilization. Local companies like Henkel are expanding automated potting lines for electronic encapsulation. Consumer behavior varies with higher enterprise adoption in healthcare and finance, with over 35% of electronics and EV OEMs integrating advanced potting compounds to improve thermal management and reliability.

Europe held a 22% share of the potting compound market in 2024. Germany, the UK, and France are key contributors, with Germany alone consuming approximately 180 kilotons of potting compounds. Strong regulatory pressures, such as VOC restrictions and environmental compliance standards, are promoting adoption of eco-friendly and thermally efficient formulations. Emerging technologies like thermally conductive silicones and UV-curable resins are gaining traction. Local players, including Momentive, are investing in R&D to develop low-VOC and recyclable potting materials. Regional consumer trends indicate that businesses prioritize sustainability, with over 60% of enterprises integrating environmentally compliant potting compounds.

Asia-Pacific represents the largest market, with a 41% share in 2024. China, Japan, and India are the top consumers, collectively accounting for over 1,340 kilotons. Rapid industrialization, expanding electronics and EV manufacturing, and government-backed infrastructure projects are driving demand. Advanced production hubs in Shanghai, Tokyo, and Bengaluru are experimenting with high-performance thermally conductive and UV-curable compounds. Companies like Wanhua Chemical are investing in automated production lines and R&D for next-generation formulations. Regional consumer behavior favors durable and cost-effective solutions, with high adoption in electronics manufacturing clusters and EV assembly plants.

South America held an 8% market share in 2024, led by Brazil and Argentina. Growth is supported by energy and infrastructure projects, including solar and wind power installations. Trade incentives and government subsidies are encouraging local manufacturers to adopt high-performance potting materials. Local players are expanding capacity to meet industrial demand, and approximately 30% of regional electronics OEMs now integrate potting compounds into power modules and automation systems. Consumer behavior in the region leans toward cost-efficient, locally supplied materials, with emphasis on durability for hot and humid climates.

The Middle East & Africa market accounted for 6% in 2024, with major contributions from the UAE and South Africa. Regional demand is driven by oil & gas, construction, and renewable energy applications. Modernization of industrial plants and integration of automated dispensing systems are improving efficiency. Local regulations and trade partnerships are fostering the adoption of advanced and environmentally friendly potting compounds. Companies are increasingly using thermally conductive and UV-curable formulations to meet high-performance standards. Consumer preferences reflect prioritization of long-lasting, weather-resistant potting materials suitable for harsh operational environments.

China – 28% Market Share: High production capacity and strong electronics and EV manufacturing hubs support dominance.

United States – 18% Market Share: Strong end-user demand in automotive, aerospace, and renewable energy sectors drives market leadership.

The potting compound market is moderately consolidated, with more than 50 active competitors globally, but the top 5 companies together account for approximately 62% of the total market. Major players dominate through a combination of broad resin portfolios, global manufacturing footprints, and strong R&D capabilities. Henkel leads with a multi‑chemistry offering including epoxy, silicone, and polyurethane. Dow leverages its vertically integrated silicone production, while 3M brings fast-curing polyurethane and epoxy systems. H.B. Fuller emphasizes hybrid and low-VOC compounds, and Electrolube focuses on thermally conductive and flame-retardant formulations.

Strategic initiatives include Henkel’s expansion of automated potting lines and launches of UV‑curable compounds; Dow’s investment in new silicone capacity; and 3M’s patent filings around AI‑enabled dispensing. Innovation trends are centered on high-thermal-conductivity systems, bio-based resins, and dual‑cure technologies. Emerging challengers and specialty firms are also contributing to pressure: start‑ups are developing phase-change microparticle potting, self-healing encapsulants, and solvent-free hybrids.

Overall, the competitive environment is dynamic. Legacy chemical companies maintain scale advantages, while niche innovators push the envelope on sustainability and performance. The combined strength of the top firms means pricing and formulation advances are often set by a few leaders, but there's increasing disruption from agile, application-focused entrants.

Henkel AG & Co. KGaA

Wacker Chemie AG

PPG Industries, Inc.

H.B. Fuller Company

Momentive Performance Materials

Huntsman Corporation

LORD Corporation (Parker Hannifin)

Dymax Corporation

ACC Silicones Ltd.

The potting compound market is being transformed by several technology-driven trends. Thermally conductive formulations are a major focus: newly developed epoxy and silicone compounds now achieve thermal conductivities of up to 5 W/m·K, enabling better heat dissipation in power electronics and LED systems. The drive for fast-curing technologies is also strong, with dual-cure and UV-curable resins reducing cure times by up to 30% in high-throughput manufacturing environments, such as in automotive electronics and consumer devices.

Sustainability is another key technological frontier: bio‑based and low‑VOC potting compounds are gaining traction, with a growing number of formulations incorporating more than 40% renewable raw materials. Nanotechnology is making inroads as well: nano‑silica, nano-alumina, and other nano-fillers are being used to reinforce mechanical strength and improve thermal and dielectric performance. Some of these nano‑enhanced potting compounds boast 35% higher strength and up to 25% better heat dissipation, making them very attractive for demanding applications.

Automation and digitization also play a critical role. AI-driven dispensing systems are being deployed to optimize resin volume and cure parameters, reducing waste and improving precision. In parallel, smart potting lines equipped with real-time sensors monitor viscosity, temperature, and flow, providing feedback loops that tighten process control. These technologies help manufacturers scale without compromising quality.

On the frontier of innovation, self-healing potting compounds are emerging: these embed microcapsules or phase-change materials that repair micro-cracks or manage thermal stress dynamically. The integration of electrically conductive fillers (e.g., graphene or graphite-based) is also being explored, aiming to create potting systems that not only insulate but also carry current or act as thermal pathways.

For business decision-makers, this technological evolution underscores how potting compounds are no longer passive materials — they are becoming active enablers of performance, reliability, and sustainability in high-growth sectors like EVs, renewable energy, and miniaturized electronics.

In May 2024, Henkel launched three new potting solutions tailored for automotive electronics: Loctite SI 5035 (a one-part silicone sealant with UV + moisture cure), Loctite AA 5832 (a dual‑cure polyacrylate for sealing against transmission fluids), and Loctite PE 8086 AB, a thermally conductive two-component epoxy for powertrain module encapsulation. Source: www.henkel.in

In February 2024, PPG added two adhesives to its aerospace portfolio: PPG PR‑2940 ESPA (a lightweight epoxy syntactic paste potting compound) for filling honeycomb structures, and PPG PR‑2936 for sealing and bonding aircraft skins to internal panels. Source: www.ppg.com

In May 2024, Dow’s SILASTIC™ SST 2650 Self‑Sealing Silicone won two 2024 SEAL Business Sustainability Awards (Sustainable Product and Sustainable Innovation categories), recognizing its design for circularity: the silicone can be removed from tires at end-of-life, enabling efficient recycling. Source: www.dow.com

In June 2024, WACKER unveiled two new silicone potting compounds — ELASTOSIL CM 181 and ELASTOSIL CM 185 — at Battery Show Europe, designed specifically to improve safety in lithium-ion battery systems by preventing fire propagation during cell thermal runaway. Source: www.wacker.com

The Potting Compound Market Report offers a comprehensive assessment of global potting compound dynamics, covering all major resin types—epoxy, silicone, polyurethane, polyester, and other tailored chemistries—as well as curing techniques including thermal, UV, and dual-cure systems. The analysis spans key applications such as electronics, automotive power modules, aerospace structures, industrial machinery, renewable energy inverters, and medical devices, with quantitative segmentation by volume and share.

Geographically, the report spans North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa, highlighting regional market size, influencing trends, and competitive positioning. The analysis delves into emerging technologies such as thermally conductive and bio-based formulations, UV/dual cure systems, nano‑reinforced potting, and self-healing materials. It also examines industry focus areas, including the rising importance of EV encapsulation, high-reliability power electronics, sustainable materials, and automated manufacturing.

Additionally, the report addresses supply chain dynamics, raw-material cost pressures, ESG compliance, and regional investment flows. It provides a detailed competitive landscape, profiling leading and emerging players, strategic initiatives (like joint ventures and new product launches), and innovation trajectories. The scope further includes forecasting demand trends, technology adoption pathways, and risk‑opportunity analysis to inform decision-makers in manufacturing, R&D, and policy planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,432.0 Million |

| Market Revenue (2032) | USD 4,415.6 Million |

| CAGR (2025–2032) | 3.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Dow Inc., 3M Company, Electrolube, Henkel AG & Co. KGaA, Wacker Chemie AG, PPG Industries, Inc., H.B. Fuller Company, Momentive Performance Materials, Huntsman Corporation, LORD Corporation (Parker Hannifin), Dymax Corporation, ACC Silicones Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |