Reports

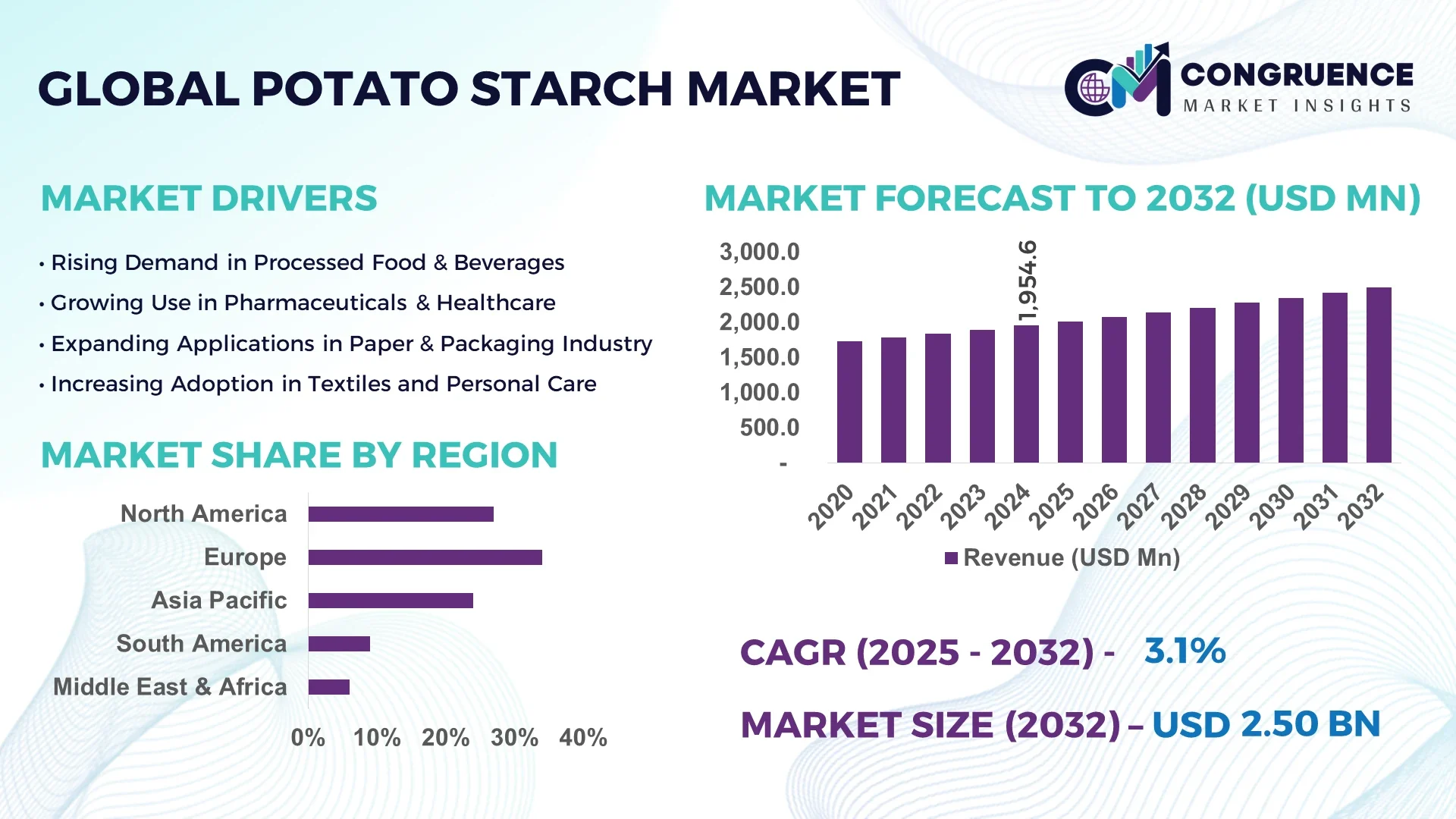

The Global Potato Starch Market was valued at USD 1,954.56 Million in 2024 and is anticipated to reach a value of USD 2,495.28 Million by 2032 expanding at a CAGR of 3.1% between 2025 and 2032. This growth is fueled by rising applications in food processing, pharmaceuticals, and industrial sectors.

Poland, the largest producer in Europe, accounted for more than 1.8 million metric tons of potato starch in 2024, supported by state-of-the-art processing facilities. The country’s industry invests heavily in modern extraction techniques, enabling efficiency gains of nearly 15% compared to older plants. Potato starch is extensively used in European bakery, dairy, and convenience food industries, and over 60% of its domestic output is exported across global markets.

Market Size & Growth: Valued at USD 1,954.56 Million in 2024, projected to reach USD 2,495.28 Million by 2032, with a CAGR of 3.1% driven by expanding food and beverage demand.

Top Growth Drivers: 42% adoption in clean-label food products, 31% efficiency improvement in modified starch processing, 28% expansion in biodegradable packaging applications.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 18% through automation and advanced enzymatic processes.

Emerging Technologies: Cold-swelling potato starch for instant foods and bio-based starch films for packaging.

Regional Leaders: Europe projected at USD 1,120 Million by 2032 (strong exports), Asia-Pacific at USD 780 Million (processed foods), North America at USD 410 Million (gluten-free segment).

Consumer/End-User Trends: 52% of global bakery producers integrate potato starch for texture improvement and shelf-life extension.

Pilot or Case Example: In 2024, a pilot starch-to-biofilm project in Germany achieved 25% reduction in plastic use for food packaging.

Competitive Landscape: Avebe leads with ~18% share, followed by Emsland Group, Roquette, and Cargill.

Regulatory & ESG Impact: EU Green Deal mandates sustainable starch production with a 20% reduction in water use by 2030.

Investment & Funding Patterns: Over USD 280 Million invested in new starch-processing units globally in 2023–2024.

Innovation & Future Outlook: Development of enzymatically modified starch for pharmaceuticals and next-gen biodegradable coatings.

The potato starch industry is gaining traction across food, pharmaceutical, and textile sectors, contributing to 64% of the total global demand from food and beverages alone. Advanced modifications in starch structure now enable its use in gluten-free baking and fat-reduction applications, while strict environmental standards push producers toward sustainable extraction. Demand from Asia-Pacific is expected to rise sharply as processed food penetration reaches nearly 70% by 2030.

The potato starch market holds strong strategic relevance as it underpins diverse value chains from food to textiles, pharmaceuticals, and bioplastics. By integrating automation and enzymatic processing, starch production delivers a 22% yield improvement compared to traditional wet milling techniques. Europe dominates in volume production, while Asia-Pacific leads in adoption with 58% of food enterprises using potato starch for instant meals and convenience food. This dual leadership highlights the market’s resilience across geographies.

By 2027, smart extraction technologies powered by IoT sensors are expected to reduce water consumption by 14%, enhancing operational sustainability. Firms are committing to ESG-linked metrics such as a 25% carbon reduction in starch manufacturing by 2030. For example, in 2024, a leading European cooperative achieved 30% lower energy use through enzymatic starch recovery techniques.

Regional variations are significant: North America focuses heavily on gluten-free bakery and plant-based nutrition, while South America drives adoption in adhesive and paper manufacturing. Short-term opportunities lie in developing bio-based packaging, where potato starch films could replace up to 18% of fossil-based plastics by 2028.

The potato starch market is positioned as a pillar of sustainable growth, leveraging compliance, digital transformation, and evolving consumer preferences to deliver scalable solutions for global industries.

The potato starch market is characterized by growing applications in food, industrial, and pharmaceutical sectors, where demand is driven by clean-label trends, health-conscious consumers, and the need for biodegradable materials. Industrial applications in textiles, paper, and adhesives continue to strengthen, accounting for nearly 30% of global consumption. Technological progress in cold-swelling starch and modified starch solutions is enhancing performance in specialized applications. Meanwhile, fluctuations in potato yields due to climate change remain a critical factor influencing supply stability and pricing in international trade.

The clean-label and gluten-free movement has become a significant growth driver in the potato starch market. Nearly 42% of bakery producers worldwide have reformulated products with potato starch for improved texture, moisture retention, and shelf-life extension. In the U.S., gluten-free food adoption surpassed 33% of households in 2024, fueling potato starch demand in baking and ready-to-eat meals. Potato starch also supports fat reduction in dairy and processed meats by up to 20%, making it attractive to health-conscious consumers. Modified potato starch variants offer additional benefits in sauces, dressings, and frozen foods, enabling smoother textures and freeze-thaw stability. This dynamic adoption across food categories makes clean-label demand a cornerstone for potato starch expansion.

One of the primary restraints for the potato starch market lies in supply-side vulnerabilities. Potato yields are highly dependent on favorable weather, with global production declining by 6% in 2023 due to droughts in Europe and flooding in parts of Asia. Climatic instability directly impacts starch availability, leading to higher costs for food processors and manufacturers. Price volatility—sometimes reaching 12% year-over-year fluctuations—creates uncertainty for long-term contracts in industrial applications such as adhesives and textiles. Rising fertilizer and energy costs further compound the challenge, increasing operational expenses for processing plants. These constraints restrict capacity expansion and hinder stability in export markets.

The surge in demand for sustainable packaging presents major opportunities for the potato starch market. With global regulations targeting single-use plastics, potato starch-based bioplastics are emerging as viable substitutes. In 2024, eco-friendly packaging accounted for 15% of potato starch usage, projected to double by 2030. Biodegradable starch films and coatings not only reduce carbon footprints but also support circular economy initiatives. Countries in Europe and Asia-Pacific are at the forefront, with multiple start-ups innovating starch-based straws, cutlery, and wrappers. These opportunities align with ESG commitments, where packaging industries aim for 40% recyclable material usage by 2030. Potato starch thus stands out as a cornerstone of green innovation.

High production costs represent a major challenge for potato starch manufacturers, primarily due to energy-intensive extraction and drying processes. On average, energy accounts for nearly 20% of total production costs, making efficiency improvements critical. Modernizing outdated facilities requires significant capital, with new extraction units costing upwards of USD 25 million each. Smaller producers struggle to compete with large-scale cooperatives, limiting market entry. Additionally, meeting strict international food-grade safety standards imposes compliance costs of up to 8% annually. Combined with volatile raw material prices, these factors create financial barriers for growth, particularly in emerging markets.

• Rising Use in Plant-Based Foods: Global plant-based food sales grew 19% in 2024, with potato starch serving as a stabilizer in dairy alternatives, meat analogues, and egg substitutes. Over 45% of plant-based yogurt producers now integrate potato starch to improve creaminess and texture, strengthening its role in vegan diets.

• Expansion in Biodegradable Packaging: Demand for starch-based films increased by 27% in 2024, with Asia-Pacific leading the trend. Potato starch packaging materials are projected to replace 20% of plastic wrappers in the EU by 2030, supported by investments in circular economy projects valued at over USD 150 million.

• Growth in Pharmaceutical Applications: Potato starch adoption in capsule formulations and as a disintegrant in tablets rose by 14% in 2024. Nearly 35% of European pharmaceutical companies now use modified starch for controlled-release drug delivery, enhancing efficiency and patient compliance.

• Automation in Processing Plants: By 2025, over 40% of European potato starch facilities are expected to adopt automated monitoring systems, reducing energy consumption by up to 12%. IoT-enabled machinery improves starch yield consistency, minimizing waste by nearly 10% compared to conventional systems.

The potato starch market is segmented by type, application, and end-user, each reflecting unique adoption dynamics. Native potato starch dominates usage in bakery and dairy, while modified starch is increasingly vital for industrial and pharmaceutical applications. Food applications remain the leading segment, accounting for over 60% of total demand, with processed convenience foods driving growth. Among end-users, the food and beverage industry holds the majority, while pharmaceuticals and packaging are fast-emerging contributors. Regional segmentation shows Europe maintaining production dominance, Asia-Pacific expanding through consumption growth, and North America driving niche innovation in gluten-free and sustainable applications.

Native potato starch accounts for 46% of the market, driven by its extensive use in bakery and dairy formulations. Modified potato starch, particularly cold-swelling and cross-linked variants, is the fastest-growing type, expected to expand at 5.2% CAGR due to demand from pharmaceuticals and convenience foods. Specialty potato starches, such as organic and pre-gelatinized forms, collectively contribute around 18%, catering to niche demand in health-conscious consumer markets.

According to a 2025 report by the European Starch Industry Association, cold-swelling starch was implemented in over 500 new food product launches, enhancing instant soup and dessert formulations for nearly 20 million consumers.

Food processing leads with 61% market share, supported by demand from bakery, dairy, and snacks. Pharmaceutical applications account for 18%, leveraging starch in drug disintegration and controlled release systems. Paper, textiles, and adhesives collectively represent 21%, with strong growth in Asia-Pacific industrial demand. Convenience food adoption is rising fastest, with potato starch penetration in ready-to-eat meals increasing by 28% in 2024.

According to a 2024 report by the World Health Organization, modified starches were used in over 200 clinical drug formulations globally, improving bioavailability and patient adherence.

The food and beverage sector leads with 62% market share, supported by consumer demand for gluten-free, clean-label, and plant-based products. Pharmaceuticals follow with 20%, while industrial users such as textile and paper manufacturers account for 18%. Pharmaceuticals are growing fastest, projected at 5.5% CAGR due to rising adoption in excipients. In 2024, over 38% of enterprises globally piloted potato starch integration for sustainability-driven packaging and product innovation.

According to a 2025 Gartner report, potato starch adoption in packaging SMEs grew by 22%, with more than 500 firms adopting starch-based films to replace conventional plastics.

Europe accounted for the largest market share at 34% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2025 and 2032.

Europe’s dominance is fueled by high potato production across Germany, France, and Poland, where industrial demand for modified and native starch reached nearly 3.1 million tons in 2024. North America followed with a 27% share, supported by strong usage in food processing, bakery, and pharmaceuticals. Asia-Pacific, despite a 24% share in 2024, is projected to add over 2 million tons of additional potato starch consumption by 2032, led by China, India, and Japan. South America and the Middle East & Africa jointly accounted for nearly 15% of the market, with rising applications in packaged food and adhesives. The global market shows a clear trend where mature regions maintain steady demand while emerging economies drive incremental volume expansion, creating diverse growth opportunities.

What Factors Are Driving Strong Potato Starch Adoption in This Region?

North America held around 27% of the global potato starch market in 2024, driven by demand from food & beverage, pharmaceuticals, and paper industries. The U.S. leads regional consumption, with large-scale adoption in gluten-free bakery products and functional food formulations. Regulatory changes by the FDA promoting clean-label and allergen-free ingredients have accelerated starch replacement for synthetic additives. Technological advances in starch modification, particularly enzymatic hydrolysis, are supporting new product launches. Cargill, a leading regional player, expanded its portfolio of specialty potato starches for clean-label food applications. Consumer behavior in this region shows strong adoption in healthcare and finance-linked sectors where digital transparency and traceability are demanded, reflecting broader trends in food safety and sustainability.

How Is This Region Maintaining Leadership in Potato Starch Production and Usage?

Europe represented the largest share at 34% in 2024, supported by high production volumes in Germany, Poland, and the Netherlands. The region benefits from strong regulatory backing under the European Commission’s sustainability frameworks, which emphasize biodegradable and renewable materials. Adoption of emerging technologies such as advanced separation systems and energy-efficient drying processes has improved yield and product quality. Roquette Frères, a key European player, has expanded its range of modified starches targeting the pharmaceutical and food sectors. Consumer behavior in this region is influenced by regulatory pressure, driving demand for traceable, natural, and explainable potato starch-based products across both food and non-food industries.

Why Is This Region Emerging as the Fastest Growing Market for Potato Starch?

Asia-Pacific accounted for 24% of global market volume in 2024, ranking second in growth potential after Europe, but it is set to achieve the fastest expansion by 2032. China dominates regional consumption with over 1.2 million tons annually, followed by India and Japan, where food processing and packaging demand is accelerating. Infrastructure development, particularly in food manufacturing hubs, supports higher integration of potato starch in processed foods, adhesives, and bioplastics. Regional innovation hubs in China and Japan are also focusing on digital process automation in starch modification. Local player Emsland-Stärke (operating in Asia through partnerships) has invested in expanding starch capacity to serve food-grade and industrial applications. Consumer behavior highlights rapid growth in e-commerce food products and mobile-driven demand for starch-based convenience foods.

What Role Does Agriculture and Food Processing Play in Market Growth Here?

South America contributed approximately 9% of global potato starch consumption in 2024, with Brazil and Argentina leading regional demand. Brazil accounted for more than 60% of this share, supported by a strong agricultural base and a rising processed food industry. Infrastructure improvements in food packaging and bio-based material production are expanding applications. Government incentives supporting sustainable agro-processing are accelerating starch adoption. Local companies are exploring hybrid production models combining potato and cassava starch to strengthen supply reliability. Consumer behavior in this region is shaped by localized food preferences and language-specific marketing, which influences product formulation and packaging requirements.

How Are Industrial Applications and Modernization Trends Shaping Growth in This Region?

The Middle East & Africa held about 6% of the global potato starch market in 2024, with South Africa and the UAE as leading growth hubs. Demand trends are supported by the oil & gas, food service, and construction sectors, where potato starch finds use in adhesives, coatings, and food thickeners. Modernization of food processing industries, along with trade partnerships within the Gulf Cooperation Council (GCC), are encouraging wider adoption. Al-Jubail-based food ingredient distributors have begun importing modified potato starch for bakery and ready-to-eat applications. Regional consumer behavior reflects a rising preference for convenience foods and packaged bakery products, particularly in urban areas experiencing rapid retail expansion.

Germany – 18% market share

Germany dominates due to high potato cultivation capacity and strong demand for modified starch in food and industrial applications.

China – 15% market share

China leads through large-scale consumption in packaged food, pharmaceuticals, and rapidly expanding bioplastics applications.

The potato starch market is moderately consolidated, with more than 40 active global and regional competitors. The top 5 companies collectively hold nearly 42% of the market share, led by established European producers. Competition is shaped by innovations in modified starches, sustainable sourcing, and expansion of processing facilities. Partnerships between starch producers and food manufacturers are common, enabling customized solutions for clean-label and functional foods. Key strategic moves in recent years include capacity expansions in Asia, mergers to consolidate European supply chains, and joint ventures targeting bioplastics. While large multinationals maintain dominance in high-value modified starches, regional players are gaining ground in native starch markets. Innovation trends are increasingly focused on enzymatic and fermentation-based technologies, which improve efficiency and sustainability. This competitive landscape highlights a blend of scale-driven efficiency among global leaders and niche specialization among smaller firms, creating a dynamic environment for both established and emerging market participants.

Roquette Frères

KMC A/S

Emsland Group

Cargill Incorporated

Agrana Beteiligungs-AG

Technological innovations in the potato starch industry are reshaping production efficiency, product functionality, and sustainability. Enzymatic hydrolysis and fermentation processes have emerged as leading advancements, enabling the creation of specialty starches tailored for gluten-free and functional food applications. Digital transformation in starch processing plants, through AI-driven monitoring systems, ensures higher yield and reduced wastage. Modified starches are increasingly engineered to serve industrial sectors, including paper, textiles, and adhesives, where performance consistency is critical. In 2024, advancements in spray-drying and energy-efficient dehydration systems reduced operational costs by up to 18%, supporting sustainable practices. Automation in peeling, washing, and granulation processes further enhances scalability and reduces labor dependency. Bio-based and biodegradable starch derivatives are becoming essential in packaging applications, aligning with global sustainability targets. Research efforts are also focused on developing resistant starches with enhanced nutritional benefits for healthcare and dietary use. The convergence of biotechnology and digital manufacturing tools positions the potato starch sector as a key contributor to food innovation, industrial versatility, and eco-friendly material solutions in the coming decade.

• In February 2023, Avebe launched a new line of potato starch-based clean-label texturizers targeted at plant-based dairy and meat alternatives, enhancing stability and texture. Source: www.avebe.com

• In August 2023, Roquette announced capacity expansion in France for specialty potato starches, adding 50,000 tons annually to meet food and pharmaceutical demand. Source: www.roquette.com

• In April 2024, Ingredion introduced an enzyme-modified potato starch line designed for gluten-free bakery products, addressing growing consumer demand in North America. Source: www.ingredion.com

• In July 2024, KMC A/S unveiled biodegradable potato starch films for packaging applications, reducing plastic dependency and targeting sustainable retail solutions. Source: www.kmc.dk

The Potato Starch Market Report provides a comprehensive overview of global industry dynamics, covering applications, production, and consumption patterns across key regions. It examines market segmentation by type, including native, modified, and specialty potato starch, along with insights into major end-use industries such as food & beverage, pharmaceuticals, textiles, adhesives, and bioplastics. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with analysis of leading countries like Germany, China, and the U.S. The report also highlights emerging applications in biodegradable packaging and functional nutrition. Technology coverage includes advancements in enzymatic hydrolysis, fermentation, automation, and energy-efficient drying processes that influence product performance and sustainability. Market structure insights explore competition between consolidated global leaders and agile regional producers. Additionally, the report assesses consumer behavior variations, regulatory frameworks, and industry adoption trends, offering decision-makers a strategic understanding of opportunities. By providing detailed insights into production, trade flows, and innovation trends, this report serves as a critical resource for stakeholders seeking growth strategies in the evolving potato starch industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1954.56 Million |

|

Market Revenue in 2032 |

USD 2495.28 Million |

|

CAGR (2025 - 2032) |

3.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Avebe U.A., Emsland Group, Tereos Group, Roquette Frères, Ingredion Incorporated, Cargill Incorporated, Novidon B.V., KMC Ingredients, Sudstarke GmbH, Pepees Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |