Reports

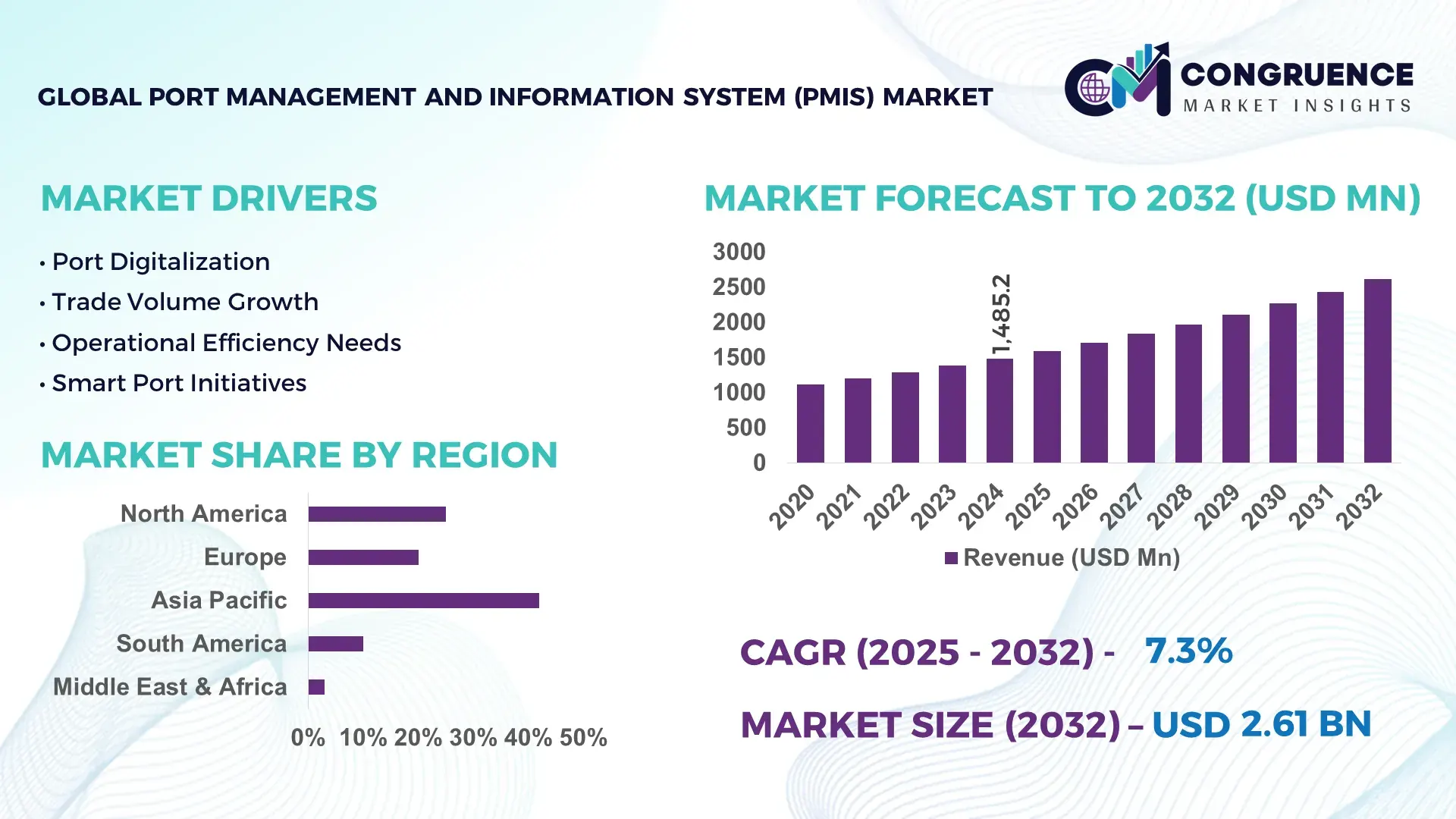

The Global Port Management and Information System (PMIS) Market was valued at USD 1485.21 Million in 2024 and is anticipated to reach a value of USD 2609.67 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032. Growth is primarily driven by accelerated digitalization of port operations and rising investments in smart port infrastructure.

China represents the dominant national market for PMIS deployments in terms of scale and implementation intensity. The country operates over 2,000 port terminals, including 16 of the world’s top 50 container ports, and handled more than 300 million TEUs of container traffic in 2023. Government-backed investments exceeding USD 20 billion have been allocated toward port automation, digital twins, AI-based vessel traffic management, and blockchain-enabled customs clearance platforms. PMIS platforms in China are heavily applied across container handling, bulk cargo management, port security, berth scheduling, and environmental monitoring. Over 75% of major Chinese ports have implemented integrated PMIS platforms, while 60% have adopted AI-driven berth optimization and predictive maintenance modules, positioning China as the largest PMIS deployment environment globally.

• Market Size & Growth: USD 1.49 billion in 2024, projected to reach USD 2.61 billion by 2032 at a CAGR of 7.3%, driven by automation adoption and trade volume digitization

• Top Growth Drivers: Terminal automation adoption +38%, port efficiency improvement +27%, regulatory digital compliance +22%

• Short-Term Forecast: By 2028, average vessel turnaround time is expected to decline by 18% across digitally enabled ports

• Emerging Technologies: AI-based berth optimization, IoT-enabled asset tracking, blockchain for cargo documentation

• Regional Leaders: Asia-Pacific USD 1.18 billion by 2032 with high automation uptake, Europe USD 0.78 billion with ESG-driven digitization, North America USD 0.65 billion with cybersecurity-focused PMIS upgrades

• Consumer/End-User Trends: Container terminals and logistics operators show fastest adoption, followed by port authorities and customs agencies

• Pilot or Case Example: A 2024 smart port PMIS pilot reduced cargo dwell time by 21% and improved crane utilization by 16%

• Competitive Landscape: Market leader holds approximately 18% share, followed by Navis, ABB, Siemens, TCS, and IBM

• Regulatory & ESG Impact: IMO emissions reporting rules and digital customs mandates are accelerating PMIS deployment

• Investment & Funding Patterns: Over USD 6.5 billion invested globally since 2022, with growth in PPP and infrastructure tech financing

• Innovation & Future Outlook: Strong shift toward integrated port ecosystems, predictive analytics, and real-time trade visibility platforms

The Port Management and Information System (PMIS) market serves key industry sectors including container terminals contributing roughly 42% of demand, bulk and liquid cargo terminals at 28%, port authorities at 18%, and logistics service providers at 12%. Recent innovations include AI-based vessel traffic optimization, digital twin port simulations, and carbon footprint monitoring modules. Regulatory drivers include IMO decarbonization targets, digital customs mandates, and cybersecurity compliance frameworks. Asia-Pacific leads consumption, followed by Europe and North America, while Latin America and the Middle East show rising adoption driven by port expansion projects. Future growth is expected from autonomous port operations, integrated trade platforms, and increased focus on ESG-aligned digital port infrastructure.

The Port Management and Information System (PMIS) Market has become strategically critical as ports evolve from infrastructure assets into data-driven logistics platforms. PMIS now underpins berth planning, vessel traffic management, cargo flow optimization, customs clearance, billing, safety monitoring, and emissions tracking within a single digital ecosystem. AI-based berth optimization delivers 18% improvement in vessel turnaround time compared to manual planning systems, while IoT-enabled asset tracking reduces container misplacement incidents by approximately 25% versus barcode-only identification standards. Asia-Pacific dominates in cargo handling volume, while Europe leads in digital port adoption with approximately 64% of large ports operating integrated PMIS platforms across terminals, authorities, and logistics operators. By 2028, predictive analytics and machine learning embedded in PMIS are expected to cut unplanned equipment downtime by 22% and improve crane utilization by 15% across automated terminals. Firms are committing to ESG improvements such as 30% reduction in port-related emissions by 2030 through energy monitoring, shore power management, and green vessel prioritization modules embedded in PMIS platforms. In 2024, the Port of Rotterdam achieved a 20% reduction in vessel waiting times and a 12% cut in fuel consumption through AI-driven traffic flow optimization integrated into its PMIS environment. Strategically, PMIS is shifting from an operational tool into a governance and resilience layer, supporting regulatory compliance, cyber risk management, climate reporting, and trade transparency. The Port Management and Information System (PMIS) Market is therefore positioned as a structural pillar for operational resilience, regulatory alignment, and sustainable growth across global maritime and logistics ecosystems.

Global container vessel capacity has more than doubled over the past decade, with ultra-large container ships exceeding 24,000 TEUs now operating on major routes, intensifying congestion at large ports. Average vessel waiting times at congested ports can exceed 30 hours, creating significant operational and cost pressures. PMIS platforms address this by enabling dynamic berth allocation, predictive arrival management, and automated crane scheduling, reducing berth conflicts by up to 20% and improving yard utilization by approximately 15%. As shipping alliances consolidate cargo flows into fewer mega-hubs, ports require advanced digital coordination to avoid bottlenecks. PMIS also supports real-time coordination with hinterland transport, improving truck and rail slot planning and reducing gate congestion by around 10–12%. These efficiency gains make PMIS a strategic investment for ports facing rising throughput without proportional physical expansion capacity.

PMIS deployments require integration with legacy terminal operating systems, customs platforms, vessel traffic services, billing systems, and national trade portals, often across multiple vendors and data standards. Integration projects can extend beyond 18 months and require substantial change management, delaying realization of operational benefits. Cybersecurity risks further restrain adoption, as ports are classified as critical infrastructure and increasingly targeted by cyberattacks, with reported incidents in maritime systems rising by over 40% in recent years. Compliance with data protection, sovereignty, and critical infrastructure regulations also increases implementation complexity. Smaller and mid-sized ports often lack internal IT and cybersecurity capabilities, limiting their ability to adopt advanced PMIS platforms despite operational need.

Smart port initiatives and green shipping corridors are generating new demand for PMIS modules that monitor energy use, emissions, and vessel environmental performance. More than 100 ports globally are participating in smart port or digital port programs, creating opportunities for AI-driven traffic management, digital twins, and carbon accounting solutions. PMIS platforms can integrate shore power management, alternative fuel tracking, and emission reporting, enabling ports to support cleaner shipping and meet climate targets. As regulators introduce mandatory emissions disclosure and environmental performance benchmarks, ports increasingly require PMIS for automated reporting and compliance. This creates growth opportunities in software upgrades, analytics modules, and integration services aligned with sustainability and smart infrastructure agendas.

The transition from manual or semi-digital port operations to fully integrated PMIS platforms requires new skills in data analytics, system administration, cybersecurity, and process engineering. Many ports face workforce shortages in these areas, increasing reliance on external vendors and raising operational risk. Resistance to organizational change among operational staff can slow adoption and reduce utilization of advanced features. Training programs, system customization, and process redesign add to project timelines and costs. Without adequate change management, ports may underutilize PMIS capabilities, limiting efficiency gains and weakening return on digital investment despite growing operational pressures.

• Rapid expansion of AI-driven operational optimization across global ports: Over 62% of large commercial ports have integrated AI modules into their Port Management and Information System (PMIS) platforms to support berth allocation, vessel sequencing, and yard planning. These systems are delivering 17% to 23% reductions in vessel waiting times and improving crane productivity by approximately 14%. Predictive maintenance algorithms embedded in PMIS reduce unplanned equipment failures by around 19%, while AI-based traffic forecasting improves peak-hour gate throughput by nearly 12%. Asia-Pacific ports account for over 45% of active AI-enabled PMIS deployments, reflecting high throughput requirements and rising automation investments.

• Shift toward modular and configurable PMIS architectures: Approximately 58% of new PMIS deployments now use modular, cloud-native architectures rather than monolithic on-premise platforms. Modular PMIS reduces implementation time by 30% and lowers integration costs by around 22% by allowing ports to deploy berth management, billing, security, and environmental monitoring modules independently. European and North American ports account for nearly 60% of modular PMIS adoption, driven by the need for faster upgrades, regulatory compliance flexibility, and integration with smart port and national trade platforms.

• Integration of ESG, emissions monitoring, and green port analytics into PMIS: More than 48% of ports implementing PMIS in 2024 included carbon tracking, energy monitoring, and environmental reporting modules. These tools enable ports to monitor vessel emissions in real time and support 20% to 30% reductions in port-related emissions through shore power optimization and green vessel prioritization. Over 35% of ports are now using PMIS to automate environmental reporting and compliance, reducing manual reporting workloads by approximately 25% while improving regulatory accuracy.

• Growing use of PMIS for end-to-end supply chain visibility and stakeholder integration: Around 52% of PMIS platforms now integrate shipping lines, freight forwarders, customs agencies, and hinterland transport into a single data environment. This integration reduces cargo dwell time by approximately 16% and improves customs clearance speed by 21%. Digital documentation and blockchain-enabled cargo tracking within PMIS have cut documentation errors by nearly 28%, while real-time data sharing has improved customer satisfaction scores among logistics users by roughly 15%, reinforcing PMIS as a core platform for trade transparency and operational resilience.

The Port Management and Information System (PMIS) market is segmented by system type, application scope, and end-user group, reflecting the diverse operational needs across global port ecosystems. By type, the market is shaped by the shift from traditional on-premise software toward cloud-native and modular platforms that support scalability, interoperability, and remote access. By application, operational optimization and terminal management remain core, while environmental compliance, security, and trade facilitation functions are gaining importance. End-user adoption varies across container terminals, port authorities, logistics operators, and government agencies, each prioritizing different functionalities within PMIS platforms. High-volume ports emphasize automation and real-time analytics, while regulatory bodies focus on reporting, safety, and compliance capabilities. This segmentation highlights how PMIS demand is no longer uniform, but driven by differentiated operational priorities, regulatory requirements, and digital maturity levels across the maritime and logistics landscape.

On-premise PMIS currently accounts for approximately 41% of active deployments, driven by data sovereignty requirements, cybersecurity concerns, and the classification of ports as critical infrastructure in many countries. Cloud-based PMIS represents about 34% of adoption and is growing fastest at an estimated 11.8% CAGR, supported by faster deployment cycles, lower infrastructure burden, and easier integration with external stakeholders such as shipping lines and customs authorities. Hybrid PMIS platforms account for roughly 17%, combining local control with cloud analytics and remote access capabilities, particularly favored by large ports transitioning from legacy systems. Other niche types, including edge-computing PMIS and private blockchain-enabled platforms, collectively represent around 8% of adoption, mainly in technologically advanced pilot ports.

Operational and terminal management functions account for around 46% of PMIS usage, as berth planning, yard optimization, and equipment scheduling remain the core value drivers for ports handling high cargo volumes. Environmental monitoring and emissions reporting account for approximately 21% of applications and are the fastest-growing area at about 13.2% CAGR, supported by regulatory mandates and decarbonization targets. Security, safety, and access control applications represent roughly 18%, while trade facilitation, billing, and documentation management together contribute about 15%.

Container terminals represent the leading end-user group with approximately 44% of PMIS adoption, driven by the need to manage high throughput, large vessels, and complex yard operations. Port authorities account for about 29% of usage, focusing on governance, safety, and regulatory reporting, while logistics and freight operators contribute roughly 17%, using PMIS primarily for visibility and coordination. Government agencies, including customs and maritime safety authorities, account for the remaining 10%.

Logistics and freight operators are the fastest-growing end-user group with an estimated 12.5% CAGR, supported by rising demand for end-to-end cargo visibility and digital documentation.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

Asia-Pacific handled over 60% of global container throughput with more than 370 million TEUs processed annually, driving high PMIS adoption across terminals and port authorities. Europe hosts over 1,200 commercial ports, of which approximately 65% have implemented digital port platforms for traffic management, customs integration, and emissions reporting. North America contributes around 23% of total PMIS deployments, driven by automation investments and cybersecurity mandates. The Middle East & Africa region represents roughly 9%, supported by greenfield port projects and logistics corridor investments, while South America accounts for about 6%, driven by port expansion in Brazil and Argentina. Across regions, more than 58% of large ports globally now operate integrated PMIS platforms, compared to only 34% five years ago, reflecting accelerated digital transformation in maritime infrastructure.

This region accounts for approximately 23% of global Port Management and Information System (PMIS) adoption, supported by strong investments in automation, cybersecurity, and data governance. Demand is driven by container terminals, energy exports, automotive logistics, and agricultural bulk shipping. Regulatory frameworks on critical infrastructure cybersecurity and digital trade compliance are accelerating PMIS upgrades. Advanced analytics, AI-driven traffic forecasting, and cloud-hybrid architectures are widely adopted, with over 55% of large ports operating predictive maintenance and berth optimization modules. A leading terminal operator has implemented AI-enabled PMIS to reduce vessel waiting time by 19% and improve crane utilization by 14%. Enterprise users show higher adoption among logistics, energy, and government agencies, prioritizing system reliability, compliance, and real-time reporting capabilities.

Europe represents around 27% of PMIS deployments, with high adoption in Germany, the Netherlands, France, and the UK. More than 64% of major ports in this region operate integrated digital port platforms, driven by strict emissions reporting rules, digital customs requirements, and climate targets. Sustainability initiatives have increased demand for PMIS-based emissions tracking and energy optimization modules, now used by over 48% of large ports. A major port authority has deployed digital twins and traffic optimization systems to reduce vessel idle time by 18% and fuel consumption by 11%. Enterprise users prioritize compliance, transparency, and interoperability, with regulatory pressure driving demand for explainable and auditable PMIS platforms.

This region ranks first globally in PMIS volume with approximately 42% of active deployments, led by China, Japan, South Korea, and India. The region operates over 2,500 commercial ports and accounts for more than 60% of global container handling volume. Infrastructure investments in smart ports, automated terminals, and logistics corridors are accelerating PMIS demand. AI-based berth planning, IoT-enabled equipment tracking, and blockchain documentation are widely deployed. A major terminal operator implemented automated PMIS scheduling to improve throughput by 21% and reduce truck gate congestion by 17%. Adoption is driven by high trade volumes, industrial exports, and rapidly expanding e-commerce logistics ecosystems.

This region represents approximately 6% of the global PMIS market, led by Brazil, Argentina, and Chile. Growth is supported by agricultural exports, mining logistics, and infrastructure modernization programs. Governments are investing in port expansions and digital customs platforms to reduce trade friction and improve competitiveness. PMIS adoption focuses on cargo tracking, customs integration, and billing automation. A regional port authority implemented digital cargo visibility modules, reducing clearance delays by 22% and improving shipment reliability. Enterprise users prioritize affordability, regulatory compliance, and integration with national trade systems.

This region accounts for approximately 9% of PMIS adoption, driven by logistics hub development, energy exports, and large-scale infrastructure projects. The UAE, Saudi Arabia, and South Africa are key growth countries. Smart port initiatives and trade corridor programs are accelerating PMIS implementation across new and upgraded terminals. Digital platforms are used to support vessel traffic control, customs automation, and security monitoring. A regional operator implemented integrated PMIS platforms to improve berth utilization by 16% and reduce vessel waiting time by 14%. Users prioritize reliability, multilingual support, and integration with regional trade and customs systems.

• China Port Management and Information System (PMIS) Market — 26% share, driven by large-scale port automation, high cargo throughput, and strong government-backed smart port programs

• United States Port Management and Information System (PMIS) Market — 18% share, supported by advanced digital infrastructure, cybersecurity mandates, and high enterprise adoption across logistics and government agencies

The Port Management and Information System (PMIS) market is moderately fragmented, with approximately 35 to 40 active global and regional solution providers competing across terminal operations, vessel traffic management, customs integration, and analytics layers. The top five providers together account for roughly 52% of total deployments, indicating a balance between dominant enterprise vendors and a long tail of specialized regional and niche technology firms. Leading companies are differentiating through AI-enabled berth optimization, cloud-native modular platforms, cybersecurity certifications, and ESG reporting functionality. Over 60% of competitive product launches in the past two years focused on predictive analytics, digital twins, and integration with national single window and customs platforms. Strategic partnerships between PMIS vendors and port authorities, cloud providers, and logistics platforms now account for nearly 45% of major market initiatives, reflecting a shift from standalone software toward ecosystem-based solutions. Mergers and acquisitions activity represents around 12% of strategic actions, mainly targeting niche firms with strengths in IoT, cybersecurity, or environmental monitoring. Competition is also intensifying around implementation speed and interoperability, with modular platforms reducing deployment times by up to 30% compared to legacy systems. Innovation cycles are shortening, with major vendors releasing platform updates every 6 to 9 months to incorporate AI models, regulatory changes, and cybersecurity enhancements, reinforcing the technology-driven nature of competitive positioning.

Navis

ABB

Siemens

IBM

Tata Consultancy Services (TCS)

Accenture

Wipro

Oracle

SAP

Kaleris

Navis

Siemens

ABB

The Port Management and Information System (PMIS) market is being reshaped by a combination of artificial intelligence, Internet of Things (IoT), cloud computing, digital twins, and cybersecurity frameworks that collectively transform how ports operate, monitor, and optimize their assets. AI-driven analytics are now embedded in more than 60% of large-scale PMIS deployments to support berth allocation, crane scheduling, traffic flow forecasting, and predictive maintenance. These tools enable ports to reduce vessel waiting time by 15–25%, improve equipment utilization by around 14%, and cut unplanned downtime by nearly 20%. Machine learning models continuously refine operational decisions based on historical and real-time data, supporting adaptive planning in high-traffic environments.

IoT plays a critical role through the deployment of smart sensors on cranes, gates, yards, and vessels. Over 45% of ports use IoT-enabled PMIS modules to monitor asset condition, energy consumption, and cargo movement, improving yard accuracy by approximately 18% and reducing container misplacement incidents by 22%. Real-time environmental sensors integrated into PMIS also support emissions monitoring, noise tracking, and water quality management, enabling ports to meet tightening regulatory and ESG requirements.

Cloud and hybrid architectures now support about 58% of new PMIS installations, enabling scalable data processing, faster deployment, and integration with external stakeholders such as shipping lines, customs agencies, and inland transport providers. Modular cloud platforms reduce implementation time by roughly 30% and facilitate frequent system updates aligned with regulatory and operational changes. Digital twin technology is being used by approximately 28% of advanced ports to simulate berth operations, traffic flows, and infrastructure upgrades, improving capital planning accuracy and reducing project risk. Cybersecurity technologies are also integral, as ports are classified as critical infrastructure. Around 52% of PMIS platforms now include embedded cybersecurity monitoring, intrusion detection, and access control modules to protect operational technology and data exchanges. Together, these technologies position PMIS as a strategic digital backbone for resilient, efficient, compliant, and sustainable port operations worldwide.

• In March 2024, Tidalis secured a major Port Management Information System (PMIS) contract with Forth Ports, the UK’s third-largest port operator, to implement an advanced PMIS solution across nine key terminals, enhancing end-to-end vessel management, billing, and scheduling capabilities. (Materials Handling World)

• In November 2024, Navis launched a cloud-native version of its N4 Terminal Operating System, featuring a new analytics module designed to expand PMIS capabilities for global ports, improving unified data management and real-time decision support across terminals.

• In August 2024, ABB entered a strategic partnership with Kalmar to deliver integrated electrified port equipment and digital optimization solutions, combining PMIS data integration with energy-efficient terminal operations to reduce energy use and enhance throughput in container handling.

• In April 2025, the Gambia Ports Authority completed the rollout of a comprehensive PMIS system across its operations, incorporating berth scheduling, pilotage, cargo operations, billing, and analytics, with modular design enabling future integration with ERP and vessel traffic systems. (Maritime Review)

The scope of the Port Management and Information System (PMIS) Market Report encompasses a comprehensive analysis of software and digital technologies that support maritime terminal operations, cargo management, vessel scheduling, customs integration, safety monitoring, and environmental reporting. It covers all major deployment models including on-premise, cloud, and hybrid PMIS architectures, detailing their functional differences, deployment patterns, and adoption drivers among terminals, port authorities, logistics operators, and government agencies. The report segments the market by type, application, and end-user, offering measurable insights into system usage trends such as predictive maintenance, AI-driven berth optimization, IoT-based asset tracking, and compliance modules.

Geographically, the report analyzes regional dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, including market presence, infrastructure trends, technology penetration, regulatory environment, and consumer behavior variations. It benchmarks key application areas such as operational optimization, environmental monitoring, trade facilitation, and security, identifying how high-volume container ports differ from bulk and multipurpose terminals in PMIS requirements. Emerging niche segments like digital twin simulation, blockchain for supply chain visibility, and smart port community platforms are also detailed, highlighting innovation pathways and competitive differentiation. Additionally, the report profiles major vendors, strategic alliances, technology partnerships, implementation case studies, and integration challenges. Designed for business decision-makers and industry professionals, it provides a precise, data-oriented view of the competitive landscape, technology impact, and market expansion opportunities, equipping stakeholders with actionable insights for strategic planning and investment prioritization.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1485.21 Million |

Market Revenue in 2032 | USD 2609.67 Million |

CAGR (2025 - 2032) | 7.3% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed |

|

Customization & Pricing | Available on Request (10% Customization is Free) |