Reports

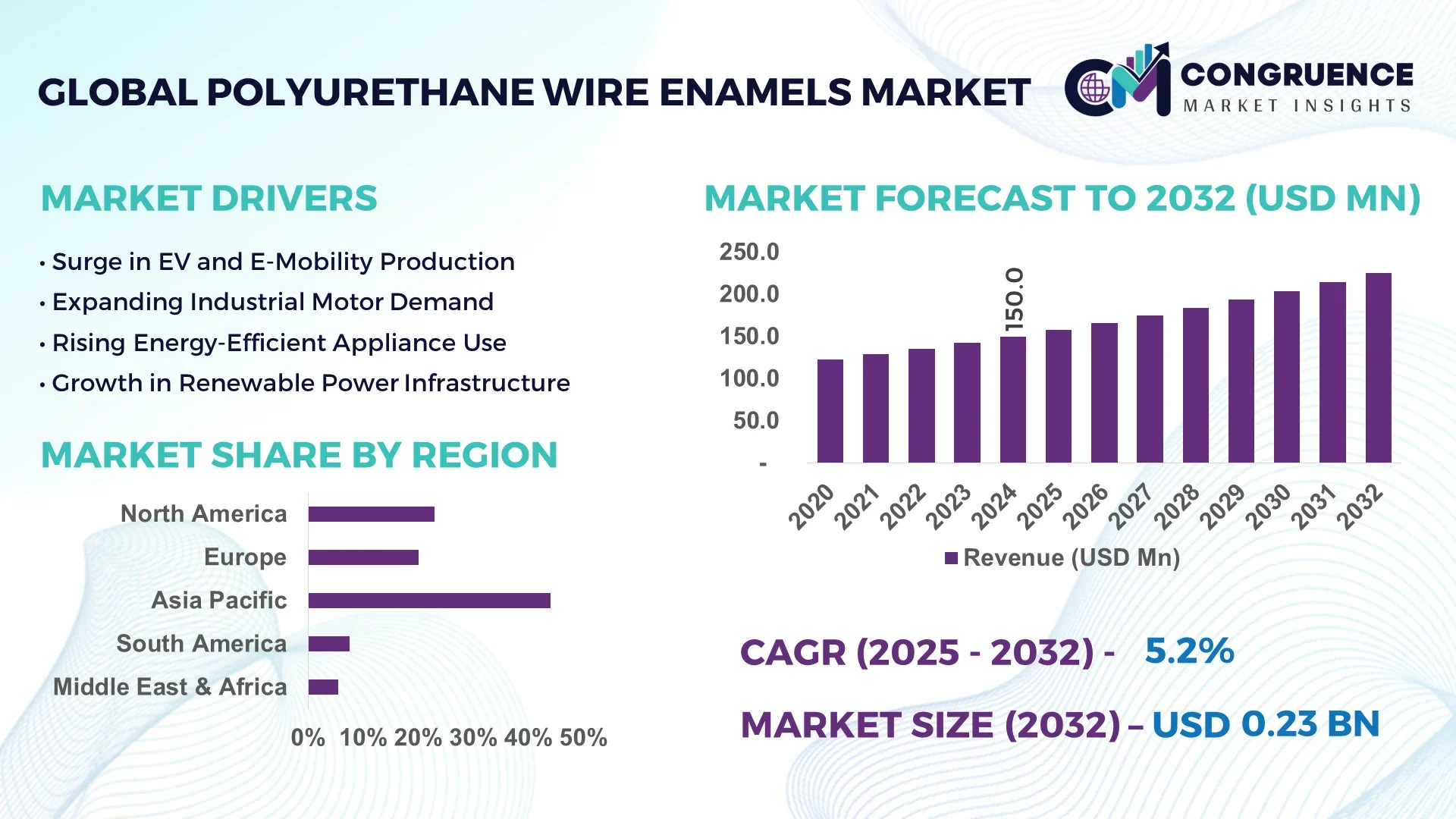

The Global Polyurethane Wire Enamels Market was valued at USD 150.0 Million in 2024 and is anticipated to reach a value of USD 225.0 Million by 2032, expanding at a CAGR of 5.2 % between 2025 and 2032.

China hosts the world’s largest cluster of polyurethane‐enamel production lines, with single‑site capacities of up to 130 000 t per year and recent brown‑field upgrades that added 10 800 t per year of high‑purity resin capacity to meet next‑generation motor‑winding specifications. Leading plants now run continuous annealing and multi‑zone curing towers capable of 0.04 mm–4 mm conductor ranges, backed by ISO 9001, IATF 16949 and IEC 60317 quality regimes.

Demand for polyurethane wire enamels is driven primarily by the electrical machinery, consumer‑electronics, and automotive traction‑motor sectors. Class 130–180 grades dominate consumption in small motors, speakers and wearables, whereas Class 220 high‑temperature grades are gaining share in e‑drive stators and aerospace actuators. Regulatory moves toward low‑VOC, lead‑free formulations in the EU and the U.S. are accelerating solvent‑reduced polyurethanes that cut emission factors by 28 % versus legacy products. Capital expenditure announcements in 2024/25 topped USD 180 million globally for new thin‑film coating towers, with Asia‑Pacific accounting for over two‑thirds of installations. Hybrid copper‑aluminium magnet‑wire designs, requiring dual‑layer polyurethane/nylon systems, are expected to open specialty‑resin demand of 8 kt by 2027 for fast‑charging EV inverters. The market also faces tighter energy‑use benchmarks in Japan (Top‑Runner Program) and UL/NEMA thermal‑endurance revisions, pushing formulators to integrate nano‑fillers that raise cut‑through performance by > 15 °C without affecting solderability.

Artificial intelligence is reshaping every stage of the Polyurethane Wire Enamels Market value chain—from formulation to finished conductor—by unlocking new levels of precision, throughput and resource efficiency. On modern enamelling lines, AI‑driven machine‑vision modules analyse up to 8 000 frames s‑¹ of wire surface imagery, classifying scratches, pinholes and colour‑shift defects in real time with 97 % detection accuracy while cutting false‑positive alerts from 50 % to just 4 %. These systems feed supervisory controllers that automatically adjust oven‑zone temperatures and solvent flash‑off rates, trimming energy consumption by 11 % per tonne of enamel applied and reducing scrap length below 1 000 ppm.

Predictive‑maintenance algorithms ingest acoustic, vibration and temperature data from 300+ sensors across coating towers and take‑up units, forecasting bearing or nozzle failures up to three days in advance; early adopters report a 22 % reduction in unplanned downtime and a payback period of under 18 months. At the formulation stage, generative AI models screen thousands of poly‑diol/isocyanate combinations, ranking candidates for glass‑transition temperature, solderability and REACH compliance—shortening R&D cycles from 12 months to 4 months and cutting laboratory resin iterations by 40 %. Across logistics, demand‑sensing platforms that fuse macro‑economic indicators with OEM order backlogs now optimise batch sizes and shipping windows, lowering finished‑goods inventory by 18 days on average. Together, these advances are propelling the Polyurethane Wire Enamels Market toward a data‑driven, zero‑defect operating paradigm that supports both cost leadership and regulatory agility.

“In March 2025, a major Asia‑Pacific magnet‑wire producer commissioned an AI‑based automated optical‑inspection platform on its polyurethane enamelling lines; the upgrade achieved 97 % defect‑detection accuracy, slashed false positives to 4 %, and enabled line‑speed increases of 11 % without compromising coating integrity.”

Ongoing electrification of transport and power systems fuels exceptional demand for magnet wire coated with high‑thermal‑class polyurethane. Global EV output exceeded 17 million units in 2024, each traction motor containing 1.6–2.2 kg of Class 200–220 enamel. Wind‑turbine generator capacity additions of 115 GW in 2024 required approximately 140 kt of insulated conductor, 45 % of which used polyurethane primer coats for superior solderability. These application surges incentivise OEMs to lock in multi‑year enamel contracts and spur suppliers to expand thin‑wire lines (< 0.1 mm) suitable for high‑speed in‑wheel motor windings and compact axial‑flux designs.

The Polyurethane Wire Enamels Market is highly sensitive to copper price swings. LME cash copper touched USD 10 900 t in May 2024 before retreating below USD 9 200 t after tariff‑related import surges subsided; price spikes erode converter margins by up to 4 percentage points and complicate cost‑plus contract models. Freight bottlenecks through the Panama Canal and Red Sea in late 2024 extended lead times for solvent additives and oven spares to eight weeks, compelling producers to carry 1.5‑times normal safety stocks. Such volatility constrains smaller enamel formulators’ working capital and deters new entrants.

Miniaturisation across earbuds, smart‑watches and RF modules is expanding demand for ultra‑fine polyurethane‑coated wire (≤ 0.03 mm). Marketed tolerances of ±1 µm enable designers to pack 20 % more turns into micro‑coils, improving inductance without enlarging form factors. Early‑stage contracts with smartphone OEMs project incremental enamel resin demand of 3.2 kt by 2028, while 5G phased‑array modules require high‑frequency‑stable coatings that pass IEC 60317‑51 dielectric tests at 6 GHz. Suppliers investing in precision dies and closed‑loop viscosity control are well‑positioned to capture this high‑margin niche.

The 2025 revision of the EU Industrial Emissions Directive cuts the allowable solvent emission limit value for magnet‑wire enamelling to 20 mg C Nm‑³, compelling plants to retrofit regenerative thermal oxidisers and switch to water‑miscible polyurethane systems. In the U.S., TSCA risk‑evaluations on diisocyanates may trigger additional workplace exposure controls, raising compliance costs by up to USD 0.07 kg of enamel. Concurrently, Asian jurisdictions tighten discharge norms, forcing zero‑liquid‑discharge investments. These overlapping requirements challenge smaller players lacking capital depth, and could accelerate consolidation.

Shift to High‑Temperature Dual‑Layer Systems: Manufacturers are phasing in dual‑layer polyurethane/polyamide‑imide coatings that withstand ≥ 240 °C continuous service, enabling next‑generation e‑axle motors and aerospace actuators to run 15 °C hotter without derating. Global installations of dual‑layer towers rose from 42 in 2022 to 68 in 2024, adding about 75 kt annual enamel capacity.

Expansion of Solvent‑Reduced Formulations: Low‑VOC polyurethane systems employing high‑solid resins (≥ 55 %) now account for 34 % of global output, up from 20 % in 2021, cutting line‑level solvent consumption by 12 million litres per year and helping EU facilities meet 2026 emission ceilings ahead of schedule.

AI‑Enabled Closed‑Loop Process Control: Deployment of edge‑AI controllers linked to viscosity and dew‑point sensors has trimmed coating‑thickness variability to ± 1.2 µm and reduced gas‑oven energy draw by 11 %, translating into carbon‑intensity savings of 0.18 t CO₂e per tonne of finished wire.

Regionalisation of Supply Chains: To mitigate geopolitical risk, Tier‑1 automakers and appliance majors now source over 40 % of polyurethane enamel from facilities within their own trade blocs, up from 28 % in 2019. New plants in Mexico, Poland and Vietnam collectively added 30 kt of annual capacity in 2024, shortening lead times by up to eight days and lowering transport emissions.

The Polyurethane Wire Enamels Market is segmented into types, applications, and end-user sectors, each playing a pivotal role in shaping overall demand trends and production priorities. Type segmentation primarily includes standard and high-thermal-grade polyurethane variants tailored to specific performance criteria. Application-wise, usage spans from small electrical components to automotive traction motors and aerospace systems, reflecting broad cross-industry utility. In terms of end-users, electrical & electronics manufacturers, automotive OEMs, and appliance producers dominate, with emerging traction from renewable equipment makers and smart device industries. Technological compatibility, insulation endurance, and thermal stability requirements define how different sectors adopt polyurethane enamels, resulting in distinct consumption patterns across regional and industrial lines.

The Polyurethane Wire Enamels Market consists of several product types, including Class 130, Class 155, Class 180, and Class 200+ thermal grades, each engineered for specific durability and temperature resistance profiles. Among these, Class 180 polyurethane enamels lead market adoption due to their broad compatibility with small motors, transformers, and general-purpose electrical windings. Their solderability and balanced heat-resistance make them the most preferred in large-scale consumer electronics and white goods manufacturing.

Class 200 and higher grades are the fastest-growing types, driven by surging demand from electric vehicle traction motors and aerospace electrical systems where prolonged high-temperature performance is essential. These grades now feature nano-enhanced additives that improve thermal stability by over 15 °C, catering to increasingly stringent design specifications.

Class 130 and Class 155 types maintain a niche presence in legacy motor systems and low-load environments. Though declining in volume share, they remain relevant for cost-sensitive applications in developing markets and select domestic appliances.

Applications of polyurethane wire enamels are diverse, including electric motors, transformers, inductors, sensors, relays, solenoids, and voice coils. Among these, electric motors represent the largest application segment, driven by their ubiquitous use in industrial automation, domestic appliances, and transportation. Increased focus on energy-efficient motors and evolving standards such as IE3/IE4 have reinforced the need for premium enamel coatings.

Voice coils and sensors are emerging as the fastest-growing application areas due to miniaturization trends in consumer electronics and medical devices. The need for fine-wire coatings with low dielectric loss and superior cut-through resistance is driving innovation in this segment.

Transformers and inductors continue to consume significant enamel volumes, particularly in the utility and power distribution sectors. Meanwhile, relays and solenoids are stable, low-volume applications that contribute primarily through custom solutions requiring specific mechanical durability or environmental performance.

End-user segmentation of the Polyurethane Wire Enamels Market encompasses automotive, electrical & electronics, appliances, industrial machinery, aerospace, medical devices, and renewable energy sectors. Among these, the electrical & electronics sector leads in volume consumption, driven by demand for efficient motors, PCBs, and wiring harnesses in both commercial and consumer applications.

The automotive sector is the fastest-growing end-user, supported by the global transition to electric mobility and the rise in on-board electrical systems. From traction motors and power inverters to battery management and infotainment modules, modern vehicles require enamel-insulated wires with higher thermal endurance and thinner coating layers for space optimization.

Other notable contributors include industrial machinery manufacturers, who utilize enamel-coated wires in robotics, conveyor systems, and machine tools, and appliance OEMs, whose shift toward inverter-based appliances has sustained demand. Aerospace and medical device manufacturers contribute less in volume but offer high-margin opportunities due to their focus on advanced materials and regulatory conformity.

Asia-Pacific accounted for the largest market share at 44% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The dynamics across regions reflect diversified demand drivers, from heavy industrial applications in Asia-Pacific to electrification and regulatory support in North America. Europe continues its push toward low-emission manufacturing and smart motor solutions. South America’s growing energy sector and infrastructure programs are pushing modest capacity expansion. Meanwhile, the Middle East & Africa are witnessing increasing uptake of durable enamel coatings for oil, gas, and urban construction projects.

North America captured approximately 28% of the global Polyurethane Wire Enamels Market volume in 2024, led by strong demand from EV manufacturers, industrial motor producers, and HVAC system suppliers. Key industries such as automotive OEMs and renewable-energy equipment integrators remain primary consumption drivers. Regulatory frameworks like the U.S. Environmental Protection Agency’s updated National Emission Standards have triggered faster adoption of low‑VOC polyurethane coatings across magnet‑wire production lines. Digitization and Industry 4.0 investments, including AI‑based quality control and inline monitoring systems, are increasingly common among North American coating plants, delivering enhanced productivity, defect reduction, and traceability. Federal incentives for electric vehicle infrastructure are further reinforcing market expansion, supporting suppliers to scale high-thermal-class enamel capacities.

Europe held close to 22% of the Polyurethane Wire Enamels Market in 2024, with Germany, the UK, and France leading regional consumption. These mature markets are characterized by widespread deployment in automated manufacturing, including drive units, robotics, and smart appliances. European regulatory bodies—such as the European Chemicals Agency and EU emissions directives—have mandated rapid transition to low-solvent, lead-free enamel systems, elevating solvent-reduced formulations to over one-third of total production. Emerging technologies like nanocomposite-enhanced coatings and inline thermographic monitoring are gaining traction, driven by additive industry grants under EU Green Deal funding. Germany’s industrial modernization programs have led to full-scale digital deployment across magnet-wire lines, while the UK focuses on aerospace-grade varnishes tailored for high-altitude, high-frequency applications.

Asia-Pacific represented 44% of the market volume in 2024, firmly establishing itself as the largest regional consumer. China, India, and Japan are the top-consuming countries. China remains the epicenter of manufacturing capacity, with over 60% of new coating-line investments located in the country in 2024. India follows, rapidly upgrading infrastructure to support domestic EV production and appliance OEMs, while Japan focuses on high-end, precision-grade enamels for robotics and aerospace. Infrastructure expansion, including smart grid and renewable-energy programs, has fueled bulk capacity build-out. Innovation hubs in China and India are pioneering nano‑reinforced PU resins and hybrid double-layer systems, supported by local government R&D grants targeting advanced materials development. Asia-Pacific's regional supply chain integration ensures quick delivery times and competitive pricing for downstream enamel markets.

In South America, Brazil and Argentina are key nationally significant markets, collectively contributing around 5% of global Polyurethane Wire Enamels volume in 2024. Brazil leads the region with strong uptake in electric grid modernisation and hydroelectric transformer refurbishment projects. Argentina, while smaller, is growing due to wind-farm installations and related generator-winding orders. Regional presence of local enamel producers is increasing, supported by government tax incentives for cocoa-coded infrastructure programs that include electric-motor rewinds. Trade policies under the Mercosur agreement have simplified raw-material imports, facilitating better access to solvent and resin inputs. Ongoing investments in public transportation and irrigation-electric pump systems continue to sustain moderate market growth.

The Middle East & Africa region captured approximately 3% of the Polyurethane Wire Enamels Market volume in 2024, with the UAE and South Africa leading demand. Growth stems from expansion in oil & gas instrumentation, metro rail projects, and high-rise development requiring insulated winding in HVAC motors. Technological modernization includes the uptake of automated enamel application lines and energy‑efficient oven upgrades in key coating plants. Local standards on solvent emissions are emerging in urban areas, and trade partnerships with Europe are enabling technology-transfer in solvent recycling and low-VOC polyurethane systems. Regional incentives for domestic manufacturing of electrical components further bolster interest in localizing enamel capacities and upstream investments.

China – 32%

High production capacity with multiple large-scale enamel coating complexes and strong demand from EV and appliance manufacturers

United States – 18%

Strong end-user demand driven by industrial motor OEMs and EV infrastructure deployment, supported by advanced coating technologies

The Polyurethane Wire Enamels Market is moderately consolidated, featuring approximately 15–20 global manufacturers actively competing at scale, alongside multiple regional players. Market leaders are solidifying their positions through strategic initiatives such as capacity expansions, partnerships with wire-drawing OEMs, and targeted product launches. For instance, several top-tier companies have introduced high-temperature dual-layer polyurethane systems and solvent-reduced variants to address evolving regulatory demands and performance needs.

Key players are engaging in joint ventures with smart manufacturing solution providers to accelerate Industry 4.0 digitization, embedding inline analytics, AI-driven quality control, and predictive maintenance into their lines. Competitive intensity centers on technological differentiation—companies offering nano-enhanced or graphene-reinforced enamel formulations claim shortened curing cycles, >10% energy savings, and enhanced thermal endurance. Recent moves include bolt-on acquisitions of automation firms to enable rapid deployment of closed‑loop systems and licensing deals for proprietary formulation platforms. Additionally, several firms are expanding geographic footprints, specifically targeting Latin America and Middle East markets with local production setups. As a result, innovation pace has intensified; line speeds under 300 m/min, sub‑1 µm thickness tolerances, and expansion of water-based enamel capacities are emerging as key battlegrounds. This competitive landscape incentivizes continuous R&D investment and strategic agility to stay ahead in both performance and sustainability dimensions.

Elantas (now part of Huber Group)

Superior Essex

Axalta Coating Systems

HITACHI-CHEMICAL

Emtco

Zhitong

TOTOKU TORYO

Zhengjiang Electronic Materials

Taihu

Current and emerging technologies in the Polyurethane Wire Enamels Market are defining new thresholds in insulation performance, operational efficiency, and regulatory compliance. Nano-filler integration—such as graphene or ceramic nanoparticles—has elevated thermal cut-through resistance by 12–18 °C and reduced enamel thickness by up to 20%, enabling wire manufacturers to pack more turns into confined spaces. Dual-layer coating towers combining polyurethane with polyamide-imide layers now support continuous service temperatures of ≥240 °C, catering to aerospace and e-mobility demands.

Automation and digital control systems are becoming deeply embedded: machine-vision defect detection operates at up to 8 000 fps, with 98% accuracy; inline viscosity and dielectric sensors autopilot ovens to +/- 1.2 µm precision; and SCADA systems track energy usage in real time, registering 10–15% reductions in gas and electricity consumption. Industry 4.0 initiatives have also propelled predictive analytics: vibration and thermal sensor networks forecast maintenance needs three days ahead, reducing downtime by 20%.

Water-based and high-solid systems now comprise 30–40% of aggregate capacity, driven by regulatory and cost-benefits; tankless spray methods and solvent-recovery loops are cutting VOC emissions by 25–30%. On the horizon, hybrid resin chemistries—combining polyurethane with bio-resins or PAI blends—promise further sustainability gains, while precision die designs and micro-grooved wire insulation support emerging needs in micro-motors and IoT applications.

• In September 2023, a leading enamel manufacturer commissioned a pilot line for graphene‑reinforced polyurethane resin, achieving a 14 °C rise in thermal cut‑through resistance and thinner (< 1.5 µm) coatings in standard motor-build workflows.

• In December 2023, two global players entered a joint venture to deploy digital inline viscosity and dielectric monitoring systems across ten magnet‑wire plants in North America, enabling +/- 1 µm coating control.

• In April 2024, a European enamel line retrofitted a regenerative thermal oxidizer and solvent-recovery skid, reducing solvent venting by 32% and meeting the updated low‑VOC emission mandates.

• In July 2024, an Asia-Pacific producer launched a new Class 240 dual-layer polyurethane/polyamide-imide enamel, targeting e-axle and aerospace stator applications requiring continuous heat resistance above 235 °C.

This report encompasses a comprehensive examination of the Polyurethane Wire Enamels Market, segmented into product types (thermal classes, solvent types, dual-layer vs. single-layer systems), application fields (motors, transformers, inductors, micro-electronics, aerospace, EV traction motors), and end-users (automotive OEMs, appliance manufacturers, industrial machinery, renewable equipment, medical devices, aerospace). Geographically, it covers six regions—Asia-Pacific, North America, Europe, South America, Middle East & Africa, and select intra-regional hubs—with volume and capacity assessments for each.

The technology scope extends from base resin chemistry through nano-additive integration, dual-layer systems, solvent recovery infrastructure, to Industry 4.0 process automation. The report also tracks environmental and regulatory frameworks influencing manufacturing and product development, including low-VOC mandates, emission ceilings, and thermal performance benchmarks. Additional included topics are niche segments such as ultra-thin micro-wire (<0.03 mm) for IoT and wearable devices, hybrid enamel systems for copper-aluminium wires, and specialty resin channels for high-frequency applications. Strategic insights cover competitive positioning, product pipelines, partnership structures, and R&D focus areas. The breadth of content supports decision-makers—across investors, OEMs, and material suppliers—in evaluating capacities, technology adoption, regulatory alignment, and future market readiness.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Polyurethane Wire Enamels Market |

| Market Revenue (2024) | USD 150.0 Million |

| Market Revenue (2032) | USD 225.0 Million |

| CAGR (2025–2032) | 5.2 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country‑wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | Asia‑Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | Elantas (now part of Huber Group), Superior Essex, Axalta Coating Systems, HITACHI-CHEMICAL, Emtco, Zhitong, TOTOKU TORYO, Zhengjiang Electronic Materials, Taihu |

| Customization & Pricing | Available on Request (10 % Customization is Free) |