Reports

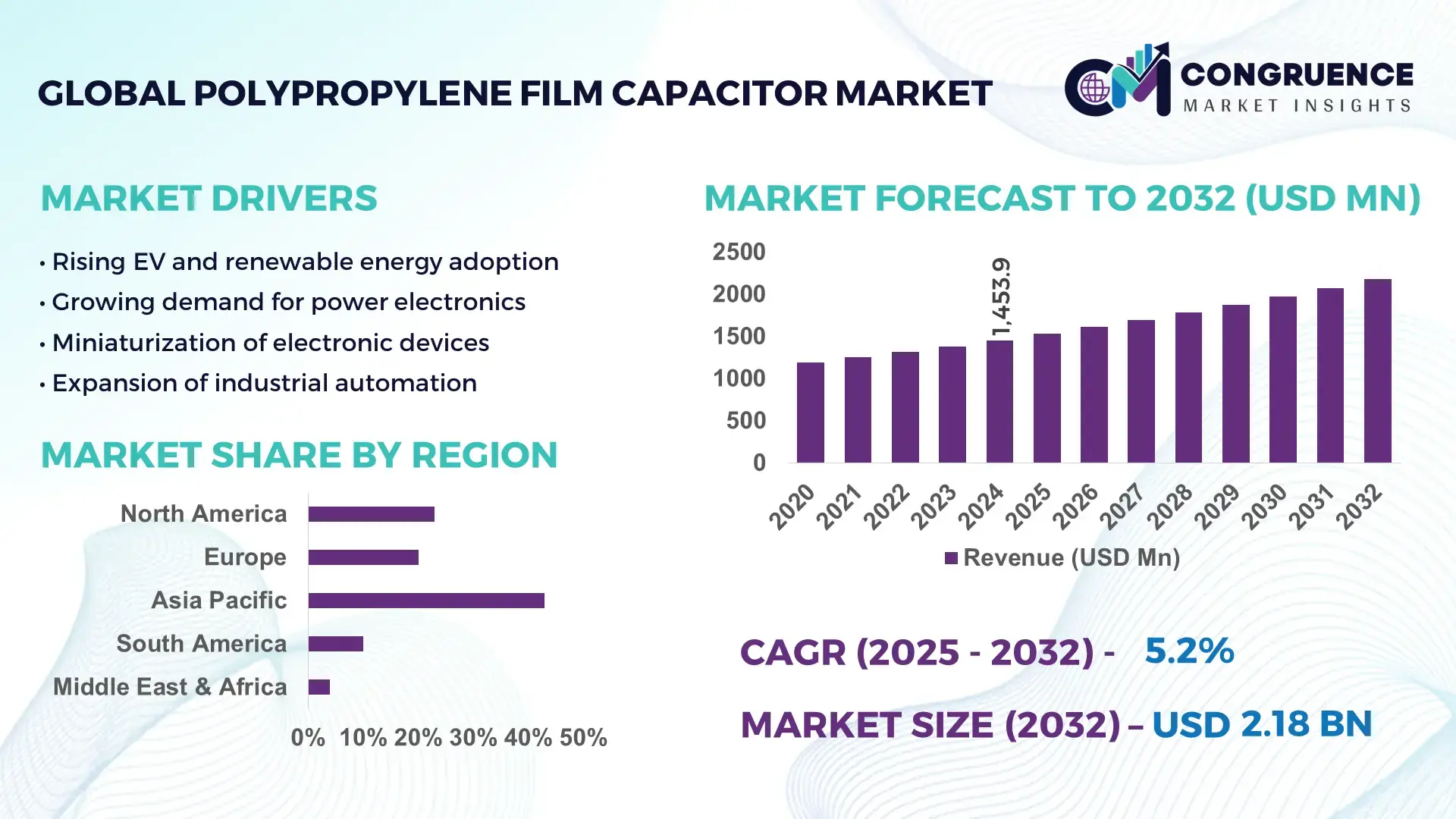

The Global Polypropylene Film Capacitor Market was valued at USD 1453.87 Million in 2024 and is anticipated to reach a value of USD 2180.98 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032. This growth is driven by rising demand for high-reliability passive components across power electronics, renewable energy systems, and electric mobility applications.

China currently represents the dominant country in the polypropylene film capacitor market, supported by its large-scale electronics manufacturing ecosystem and advanced capacitor production infrastructure. The country hosts over 40% of global polypropylene film capacitor manufacturing facilities, with annual production capacity exceeding 18 billion units across industrial, automotive, and consumer electronics segments. Capital investments in capacitor and dielectric film manufacturing surpassed USD 2.1 billion between 2021 and 2024, focused on high-voltage DC capacitors and metallized polypropylene technologies. Polypropylene film capacitors are extensively deployed in China’s electric vehicle inverters, solar PV inverters, and industrial motor drives, with renewable energy applications accounting for approximately 32% of domestic demand. Technological advancements include large-scale adoption of ultra-thin dielectric films below 4 microns and automated winding processes, improving volumetric efficiency by nearly 18% while enhancing thermal stability and lifespan.

Market Size & Growth: Valued at USD 1453.87 Million in 2024, projected to reach USD 2180.98 Million by 2032 at a CAGR of 5.2%, driven by increased electrification and demand for high-efficiency power conditioning components.

Top Growth Drivers: Electric vehicle penetration growth at 28%, renewable energy inverter installations rising 24%, and industrial automation efficiency gains of 15%.

Short-Term Forecast: By 2028, average capacitor energy density is expected to improve by 12%, while unit manufacturing costs decline by approximately 9%.

Emerging Technologies: Ultra-thin metallized polypropylene films, self-healing dielectric structures, and high-temperature polypropylene variants for automotive-grade applications.

Regional Leaders: Asia-Pacific projected at USD 980 Million by 2032 with EV-driven demand; Europe at USD 610 Million supported by renewable integration; North America at USD 420 Million driven by grid modernization.

Consumer/End-User Trends: Automotive OEMs and renewable energy integrators account for over 55% of new installations, with rising preference for long-life, maintenance-free capacitors.

Pilot or Case Example: In 2024, a utility-scale solar inverter project in Asia achieved a 14% reduction in inverter downtime using advanced polypropylene film capacitors.

Competitive Landscape: TDK holds approximately 18% share, followed by KEMET, Vishay Intertechnology, Panasonic, and Nichicon.

Regulatory & ESG Impact: Energy efficiency standards and carbon reduction policies are accelerating adoption of low-loss capacitors in power electronics.

Investment & Funding Patterns: Recent global investments exceeded USD 1.6 billion, focused on capacity expansion and advanced dielectric film technologies.

Innovation & Future Outlook: Integration with wide-bandgap semiconductors and development of recyclable polypropylene films are shaping next-generation capacitor solutions.

The polypropylene film capacitor market serves key industry sectors including automotive electronics, renewable energy, industrial automation, power transmission, and consumer electronics, with automotive and energy applications jointly contributing nearly 48% of total demand. Recent innovations such as high-temperature polypropylene dielectrics, enhanced self-healing metallization, and compact high-voltage designs are improving reliability and lifespan while reducing component size. Regulatory drivers include stricter energy efficiency norms for power electronics and environmental mandates encouraging recyclable and low-loss materials. Regionally, Asia-Pacific leads consumption due to large-scale electronics manufacturing, while Europe shows strong growth from renewable integration and electrified transport infrastructure. Emerging trends include increased use in DC-link applications, compatibility with silicon carbide power devices, and growing focus on sustainable capacitor materials, positioning the market for steady, technology-led expansion through the next decade.

The Polypropylene Film Capacitor Market holds strong strategic relevance within global power electronics and energy management value chains due to its role in ensuring electrical stability, low-loss performance, and long operational life across mission-critical applications. Polypropylene film capacitors are increasingly prioritized in electric vehicles, renewable energy inverters, smart grids, and industrial automation systems where failure tolerance and thermal reliability are non-negotiable. From a technology benchmarking perspective, metallized polypropylene film capacitor technology delivers nearly 22% lower dielectric loss compared to traditional polyester film capacitors, enabling higher efficiency under high-frequency and high-voltage conditions.

Regionally, Asia-Pacific dominates in volume due to large-scale electronics manufacturing and power infrastructure deployment, while Europe leads in adoption with approximately 46% of industrial power electronics enterprises integrating polypropylene film capacitors into renewable energy and electrified transport systems. Strategic pathways are increasingly shaped by digitization and automation. By 2028, AI-enabled process optimization in capacitor winding and metallization is expected to improve yield efficiency by 15% while reducing defect rates by nearly 12%.

Compliance and ESG priorities are also redefining procurement strategies. Firms are committing to material efficiency and circularity improvements, including up to 30% reduction in polymer waste and increased recyclability of dielectric films by 2030. In a measurable micro-scenario, in 2024, Japan-based capacitor manufacturers achieved a 17% reduction in energy consumption per production batch through smart factory upgrades and predictive maintenance platforms. Looking ahead, the Polypropylene Film Capacitor Market is positioned as a structural pillar supporting system resilience, regulatory compliance, and sustainable growth across electrified and decarbonized economies.

Electrification of transportation, industrial processes, and power infrastructure is a primary driver of the Polypropylene Film Capacitor Market. Electric vehicles require multiple high-voltage DC-link capacitors per drivetrain, with average capacitor content per EV increasing by over 35% compared to internal combustion platforms. Renewable energy systems such as solar and wind inverters rely heavily on polypropylene film capacitors for voltage smoothing and harmonic suppression, with utility-scale installations consuming thousands of units per megawatt. Industrial automation further amplifies demand as variable frequency drives and servo systems increasingly operate at higher switching frequencies. These applications collectively favor polypropylene film capacitors due to their low dielectric losses, high ripple current tolerance, and operational lifetimes exceeding 100,000 hours under rated conditions.

The Polypropylene Film Capacitor Market faces restraints related to material cost fluctuations and manufacturing complexity. Polypropylene resin pricing remains sensitive to petrochemical feedstock volatility, impacting production planning and margin stability. Additionally, the fabrication of ultra-thin dielectric films below 4 microns requires high-precision extrusion and metallization equipment, increasing capital intensity. Yield losses during winding and self-healing calibration can exceed 6% in less automated facilities, raising unit costs. Compliance with stringent automotive and grid standards further extends qualification timelines, limiting rapid scalability for new entrants and constraining short-term supply flexibility.

Grid modernization and adoption of silicon carbide and gallium nitride power devices present significant opportunities for the Polypropylene Film Capacitor Market. Wide-bandgap semiconductors operate at higher switching frequencies and temperatures, increasing demand for capacitors with superior thermal stability and low inductance. Polypropylene film capacitors are increasingly specified in next-generation solid-state transformers and fast-charging infrastructure. Smart grid investments are also expanding deployment of power quality equipment, where polypropylene film capacitors improve voltage regulation and reduce harmonic distortion by over 20%. These developments open opportunities for customized, high-performance capacitor designs with premium technical specifications.

Regulatory and qualification requirements present a persistent challenge for the Polypropylene Film Capacitor Market. Automotive-grade capacitors must comply with multiple international standards covering endurance, humidity resistance, and vibration tolerance, often requiring testing cycles exceeding 18 months. Grid-connected applications face additional certification related to fire safety and long-term reliability. These extended validation timelines delay commercialization of new designs and increase development costs. Furthermore, differences in regional compliance frameworks complicate global product harmonization, forcing manufacturers to maintain parallel specifications and testing protocols, which adds operational complexity and slows time-to-market.

• Expansion of Modular and Prefabricated Power Infrastructure Applications: The rise in modular and prefabricated construction is reshaping demand dynamics in the Polypropylene Film Capacitor market, particularly for power distribution panels, containerized substations, and prefabricated EV charging units. Around 55% of newly commissioned industrial and energy projects report measurable cost and time benefits from modular practices. Prefabricated power modules increasingly integrate polypropylene film capacitors for voltage stabilization and harmonic filtering, reducing on-site assembly time by nearly 30%. Demand growth is most pronounced in Europe and North America, where over 48% of new smart infrastructure projects now specify factory-assembled electrical systems using standardized capacitor modules.

• Shift Toward High-Temperature and High-Frequency Capacitor Designs: There is a measurable shift toward polypropylene film capacitors capable of operating above 105°C and at switching frequencies exceeding 50 kHz. These designs are increasingly required in electric vehicle traction inverters and silicon carbide-based power electronics. Adoption of high-temperature polypropylene films has increased by approximately 26% over the last three years, while dielectric thickness reductions of 18% have improved volumetric efficiency. This trend supports compact system architectures and reduces cooling system dependency by nearly 12%, directly improving overall system reliability.

• Accelerated Automation and Digital Quality Control in Manufacturing: Manufacturers are increasingly deploying automated winding, metallization, and inline inspection systems to improve consistency and throughput. Smart manufacturing adoption has resulted in defect rate reductions of up to 14% and yield improvements nearing 16% in advanced facilities. Digital quality monitoring using real-time capacitance and insulation resistance tracking is now implemented in over 40% of large-scale production lines, supporting tighter tolerance requirements for automotive and grid-grade polypropylene film capacitors.

• Growing Emphasis on Sustainability and Material Efficiency: Sustainability-driven design changes are emerging as a key trend, with manufacturers targeting thinner dielectric films and reduced aluminum metallization usage. Material optimization initiatives have lowered raw material consumption per unit by approximately 11% while maintaining electrical performance. Additionally, nearly 35% of producers have introduced recyclable or low-waste polypropylene film variants, supporting internal ESG targets that aim for polymer waste reduction of 25% by the end of this decade.

The Polypropylene Film Capacitor Market segmentation reflects diversified demand across product types, application environments, and end-user industries driven by electrification, efficiency standards, and system reliability requirements. By type, metallized and film/foil configurations address distinct voltage, lifespan, and self-healing needs across industrial and automotive systems. Application-wise, power electronics dominates deployment due to widespread use in inverters, converters, and DC-link circuits, while renewable energy and electric mobility are emerging as high-growth application clusters. From an end-user perspective, industrial manufacturing and automotive OEMs remain primary consumers, supported by rising adoption from utilities and infrastructure operators. Segmentation trends indicate increasing customization, tighter tolerance requirements, and differentiated growth trajectories across mature and emerging use cases, offering decision-makers clarity on demand concentration and future investment pathways.

The Polypropylene Film Capacitor Market by type is primarily segmented into metallized polypropylene film capacitors, polypropylene film/foil capacitors, and other specialized variants including segmented film and hybrid designs. Metallized polypropylene film capacitors currently account for approximately 62% of total adoption due to their self-healing properties, compact size, and suitability for high-volume applications such as DC-link circuits and power factor correction units. In comparison, film/foil polypropylene capacitors represent about 21% of adoption, favored in high-current and pulse applications requiring superior mechanical robustness. However, adoption of segmented and advanced hybrid polypropylene film capacitors is rising fastest, supported by demand in high-voltage DC transmission and traction systems, with this segment expanding at an estimated CAGR of 7.1% due to improved fault isolation and extended operational life. The remaining specialized capacitor types collectively contribute around 17% of market usage, addressing niche requirements such as extreme temperature stability and precision signal conditioning.

By application, the Polypropylene Film Capacitor Market is led by power electronics, which accounts for nearly 44% of total usage due to extensive integration in inverters, converters, motor drives, and uninterruptible power systems. Renewable energy systems and electric vehicles together represent around 31% of applications, reflecting the growing reliance on polypropylene film capacitors for voltage stabilization and harmonic suppression. Industrial automation applications hold approximately 15% share, driven by rising deployment of variable frequency drives and robotics. While power electronics remains the largest segment, electric mobility and fast-charging infrastructure are the fastest-growing applications, expanding at an estimated CAGR of 8.4% as global EV charger installations increase and higher switching frequencies demand low-loss capacitors. The remaining applications, including consumer electronics and rail traction, collectively account for about 10% of demand, serving stable but technically specialized use cases.

End-user segmentation in the Polypropylene Film Capacitor Market is dominated by industrial manufacturers, which account for approximately 39% of total demand due to extensive use in factory automation, power conditioning equipment, and heavy machinery. Automotive OEMs and tier-one suppliers collectively represent around 28% of adoption, reflecting growing capacitor content per vehicle in electric and hybrid platforms. Utilities and energy infrastructure operators contribute close to 18%, driven by investments in grid stability, renewable integration, and power quality systems. Among these, automotive and charging infrastructure operators constitute the fastest-growing end-user segment, expanding at an estimated CAGR of 9.0% as EV production volumes and fast-charging networks scale rapidly. The remaining end-users, including consumer electronics manufacturers and rail system integrators, together account for about 15% of usage, characterized by steady replacement demand and long qualification cycles.

Asia-Pacific accounted for the largest market share at 48.6% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Asia-Pacific’s leadership is supported by high-volume manufacturing capacity exceeding 18 billion capacitor units annually, strong electronics exports, and large-scale deployment in electric vehicles and renewable energy systems. Europe’s accelerated growth trajectory is driven by regulatory-led electrification, grid modernization programs, and sustainability mandates targeting reduced electrical losses and extended component lifecycles. North America held approximately 23.4% share in 2024, supported by industrial automation and EV charging infrastructure, while South America and the Middle East & Africa collectively represented around 11.2%, reflecting emerging investments in energy, transport, and industrial power systems. Regional demand variations highlight higher penetration of polypropylene film capacitors in automotive and grid-scale applications in developed markets, while emerging regions are seeing increased uptake in industrial drives and power conditioning equipment.

How is advanced electrification shaping demand across mature industrial ecosystems?

The North America Polypropylene Film Capacitor Market accounted for approximately 23.4% of global demand in 2024, driven primarily by industrial automation, electric mobility, renewable energy integration, and data center power management. Automotive electrification and fast-charging infrastructure are key demand generators, with over 62% of newly installed DC fast chargers utilizing polypropylene film capacitors in DC-link and filtering circuits. Regulatory support includes grid resilience funding and incentives for domestic manufacturing under clean energy and infrastructure programs. Technological advancements focus on digital power management, silicon carbide–based inverters, and automated capacitor quality inspection. Local players such as KEMET are expanding high-reliability capacitor production and introducing automotive-grade polypropylene film capacitors with extended temperature ratings. Regional consumer behavior shows higher enterprise adoption in automotive manufacturing, energy storage, and data center power systems, prioritizing long lifecycle and low-loss performance.

Why is compliance-driven electrification accelerating component adoption?

The Europe Polypropylene Film Capacitor Market represented around 21.8% of global demand in 2024, with Germany, France, and the UK collectively accounting for more than 58% of regional consumption. Demand is strongly influenced by renewable energy expansion, rail electrification, and industrial efficiency upgrades. Regulatory frameworks focused on energy efficiency, carbon reduction, and equipment lifecycle transparency are accelerating adoption of high-performance polypropylene film capacitors. Emerging technologies include wide-bandgap semiconductor integration and smart grid power electronics. European manufacturers such as TDK Europe are investing in low-loss, recyclable dielectric film designs aligned with sustainability targets. Regional consumer behavior reflects strong regulatory pressure, leading to preference for highly reliable, standards-compliant polypropylene film capacitor solutions in industrial and energy applications.

How does large-scale manufacturing sustain global supply leadership?

The Asia-Pacific Polypropylene Film Capacitor Market ranked first globally by volume in 2024, accounting for approximately 48.6% of total demand. China, Japan, and India are the top consuming countries, together representing over 72% of regional usage. The region benefits from dense electronics manufacturing clusters, advanced metallized film production, and high investments in EVs, solar inverters, and industrial drives. Manufacturing trends include automated winding lines, ultra-thin dielectric film extrusion, and vertically integrated capacitor supply chains. Companies such as Panasonic and Nichicon continue to expand high-voltage and automotive-grade capacitor portfolios. Regional consumer behavior emphasizes cost-efficiency, rapid scalability, and adoption driven by mass electrification and industrial expansion.

What role does energy infrastructure expansion play in regional demand?

The South America Polypropylene Film Capacitor Market accounted for approximately 6.5% of global demand in 2024, led by Brazil and Argentina. Growth is linked to power transmission upgrades, renewable energy installations, and industrial modernization projects. Wind and solar energy systems increasingly deploy polypropylene film capacitors for voltage stabilization, with renewable projects accounting for nearly 38% of new installations. Government incentives supporting clean energy and regional manufacturing are improving component localization. While local production remains limited, regional assemblers are increasing procurement volumes to support infrastructure reliability. Consumer behavior reflects demand tied closely to energy access expansion and industrial electrification rather than consumer electronics.

How is industrial and energy diversification influencing adoption?

The Middle East & Africa Polypropylene Film Capacitor Market represented approximately 4.7% of global demand in 2024, driven by oil & gas electrification, infrastructure construction, and grid reliability initiatives. The UAE and South Africa are the primary growth countries, together accounting for over 54% of regional usage. Technological modernization includes adoption of advanced power conditioning equipment in desalination plants, transport systems, and industrial facilities. Regional regulations emphasize equipment durability in high-temperature environments, favoring polypropylene film capacitors. Consumer behavior shows preference for robust, low-maintenance components capable of long service life under harsh operating conditions.

China – 34.2% market share: Dominance supported by large-scale production capacity, strong EV and renewable energy demand, and vertically integrated electronics manufacturing.

Germany – 12.6% market share: Leadership driven by advanced industrial automation, renewable integration, and stringent efficiency and compliance requirements across power electronics systems.

The Polypropylene Film Capacitor market exhibits a moderately consolidated competitive structure, characterized by the presence of over 45 active manufacturers globally, ranging from large multinational electronics companies to specialized capacitor producers. The top five companies collectively account for approximately 52–55% of global demand, reflecting strong brand positioning, extensive production capacity, and long-standing relationships with automotive, industrial, and energy-sector customers. Market leaders compete primarily on product reliability, dielectric innovation, volumetric efficiency, and compliance with automotive and grid-grade standards.

Strategic initiatives increasingly focus on capacity expansion, automation, and technology differentiation. More than 60% of leading players have invested in advanced metallized film processing, ultra-thin dielectric technologies below 4 microns, and automated winding systems to improve yield by 12–16%. Product launches targeting high-temperature (≥125°C) and high-frequency (>50 kHz) applications have intensified competition, particularly in EV traction inverters and renewable energy converters. Partnerships with automotive OEMs, inverter manufacturers, and power electronics integrators are common, with multi-year supply agreements covering volumes exceeding 100 million units annually. The market remains innovation-driven, with competition shaped by lifecycle performance, sustainability credentials, and the ability to scale production while maintaining tight tolerance and low defect rates.

TDK Corporation

Panasonic Corporation

Vishay Intertechnology, Inc.

KEMET Corporation

Nichicon Corporation

AVX Corporation

WIMA GmbH & Co. KG

Cornell Dubilier Electronics

EPCOS AG

Taiyo Yuden Co., Ltd.

Technological advancement in the Polypropylene Film Capacitor Market is centered on improving energy efficiency, thermal stability, miniaturization, and operational lifespan to meet the rising demands of power-dense applications. One of the most impactful developments is the large-scale adoption of ultra-thin metallized polypropylene films with dielectric thickness reduced to 3–4 microns, enabling volumetric efficiency improvements of up to 18% while maintaining high insulation resistance. These thinner films support higher capacitance per unit volume and are increasingly deployed in electric vehicle traction inverters and fast-charging infrastructure. Self-healing metallization technology continues to evolve, with optimized zinc–aluminum alloy layers improving fault isolation speed by nearly 25%, significantly reducing catastrophic failure risks in high-voltage environments. Advanced winding and segmentation techniques are also being implemented to enhance ripple current handling, allowing polypropylene film capacitors to operate reliably at switching frequencies exceeding 50 kHz. This capability aligns with the growing integration of silicon carbide and gallium nitride power semiconductors, which demand low equivalent series resistance and minimal dielectric losses.

On the manufacturing side, automation and digitalization are reshaping production efficiency. Automated winding systems combined with inline optical and electrical inspection have reduced defect rates by approximately 14% and improved yield consistency across large production runs. Predictive analytics and AI-driven process control are being used to optimize metallization uniformity and thermal curing cycles, resulting in endurance life extensions of 10–15% under rated operating conditions. Sustainability-driven technologies are also gaining traction. Material optimization has reduced aluminum metallization usage by around 12%, while new recyclable polypropylene film formulations are being introduced to support circular manufacturing goals. High-temperature polypropylene variants rated up to 125°C are expanding application potential in automotive and industrial power electronics, reinforcing the market’s technological trajectory toward reliability, efficiency, and long-term system resilience.

• In January 2024, TDK Electronics AG expanded production flexibility for key film capacitor series by qualifying its Gavatai, Brazil factory alongside existing facilities in China and India for standard B3292H and B3292J polypropylene film capacitors, enhancing delivery options and customer lead-time responsiveness.

• In early 2024, Panasonic Corporation commissioned a new high-volume production line in Jiangsu Province, China, adding capacity for approximately 2.2 billion polypropylene film capacitors annually with advanced automatic winding systems to support automotive and renewable energy demand.

• In May 2023, AVX Corporation qualified a series of 1 250 V polypropylene snubber capacitors tailored for silicon carbide (SiC) charger applications, achieving an exceptionally low failure rate of 11 FIT after 2,000 hours at 135 °C, underscoring reliability under high-stress conditions.

• In August 2023, Nichicon Corporation initiated expansion of its Fukushima manufacturing site to add capacity for an additional 620 million polypropylene film capacitor units and enhance film recycling initiatives, strengthening output for industrial and automotive sectors.

The scope of the Polypropylene Film Capacitor Market Report encompasses comprehensive analysis across product segments, geographic regions, end-use applications, and technological frontiers essential for industry planning and investment strategies. It evaluates segmentation by capacitor types—including metallized polypropylene, film/foil configurations, and specialized high-voltage or high-temperature variants—highlighting specific dielectric designs, volumetric efficiencies, and operational tolerances relevant to modular power systems, EV traction inverters, and industrial drives. Type evaluation includes volumetric penetration rates, dielectric thickness distributions, and comparative performance metrics across design families. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing consumption volumes, production capacities, regulatory and compliance landscapes, infrastructure investment trends, and regional manufacturing ecosystems. The report maps over 6.5 billion units consumed in Asia-Pacific in recent years, shifting regional demand patterns, and the strategic positioning of supply hubs in China, Japan, and India versus adoption nuances in regulatory-driven Western markets.

Application coverage dissects deployment in power electronics, renewable energy systems, electric mobility, industrial automation, and consumer power supplies, with emphasis on technical requirements such as high-frequency operation, low equivalent series resistance, and thermal endurance. It also identifies emerging niches such as DC-link systems for SiC/GaN platforms, fast charging networks, and smart grid components. Technology insights consider manufacturing automation, ultra-thin film processes, self-healing metallization, and sustainability trends including recyclable polypropylene formulations and energy-efficient processing. Industry focus areas address supply chain resilience, material cost dynamics, and innovation pipelines for next-generation capacitor architectures. The report serves decision-makers with actionable intelligence on competitive positioning, segment performance, and strategic growth drivers shaping the polypropylene film capacitor landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1453.87 Million |

Market Revenue in 2032 | USD 2180.98 Million |

CAGR (2025 - 2032) | 5.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | TDK Corporation, Panasonic Corporation, Vishay Intertechnology, Inc., KEMET Corporation, Nichicon Corporation, AVX Corporation, WIMA GmbH & Co. KG, Cornell Dubilier Electronics, EPCOS AG, Taiyo Yuden Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |