Reports

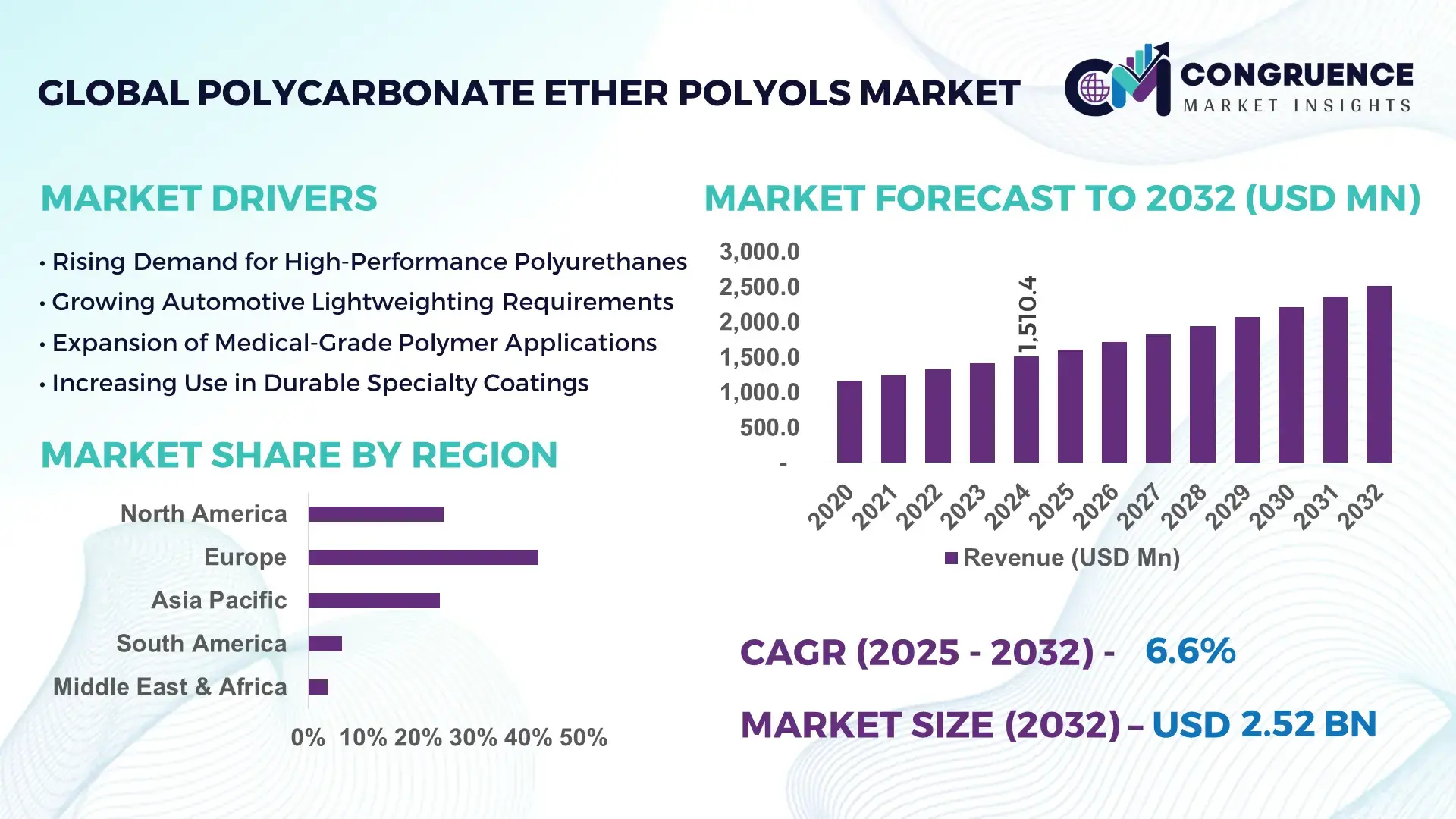

The Global Polycarbonate Ether Polyols Market was valued at USD 1,510.4 Million in 2024 and is anticipated to reach a value of USD 2,518.5 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by rising demand for high-performance polyurethane materials offering superior hydrolysis resistance and long service life across industrial and consumer applications.

Germany represents the dominant country in the Polycarbonate Ether Polyols market, supported by advanced chemical manufacturing infrastructure and strong downstream demand. The country operates more than 30 large-scale polyurethane formulation plants, with annual polyols processing capacity exceeding 1.2 million metric tons. Automotive interiors, footwear components, industrial rollers, and medical-grade elastomers collectively account for over 62% of domestic consumption. Investments exceeding USD 480 million between 2021 and 2024 were directed toward continuous polymerization reactors, low-emission catalysts, and closed-loop production systems. Over 45% of German producers have adopted next-generation aliphatic carbonate technologies to enhance abrasion resistance and extend product lifecycle performance.

Market Size & Growth: Valued at USD 1,510.4 Million in 2024 and projected to reach USD 2,518.5 Million by 2032, expanding at a CAGR of 6.6%, driven by demand for durable polyurethane elastomers.

Top Growth Drivers: Automotive lightweighting adoption (38%), industrial equipment durability upgrades (31%), medical-grade polymer usage expansion (26%).

Short-Term Forecast: By 2028, production efficiency improvements are expected to reduce unit processing costs by 18%.

Emerging Technologies: Low-temperature polymerization, bio-based carbonate feedstocks, and continuous flow reactors.

Regional Leaders: Europe (USD 890 Million by 2032), Asia Pacific (USD 760 Million), North America (USD 540 Million), each with distinct industrial adoption patterns.

Consumer/End-User Trends: Increased preference for long-life, low-maintenance elastomers in automotive and industrial sectors.

Pilot or Case Example: In 2023, a pilot elastomer program achieved 22% wear-life extension in conveyor systems.

Competitive Landscape: The market leader holds approximately 19% share, followed by four competitors each ranging between 7–11%.

Regulatory & ESG Impact: Over 48% of manufacturers align with low-VOC and lifecycle sustainability frameworks.

Investment & Funding Patterns: More than USD 620 Million invested globally since 2021 in capacity expansion and process optimization.

Innovation & Future Outlook: Integration of recyclable polycarbonate ether polyols into circular polyurethane systems is accelerating.

Polycarbonate Ether Polyols are primarily consumed by automotive (34%), industrial machinery (27%), footwear (18%), medical devices (11%), and specialty coatings (10%). Technological advances in catalyst efficiency and carbonate chain control are improving mechanical stability. Regulatory emphasis on durability and material efficiency is shaping procurement. Asia Pacific demand is rising with manufacturing growth, while Europe focuses on high-performance and sustainable formulations.

The Polycarbonate Ether Polyols Market plays a strategic role in enabling next-generation polyurethane systems that prioritize durability, hydrolytic stability, and long-term mechanical performance. Compared with conventional polyester polyols, advanced polycarbonate ether polyols deliver up to 45% improvement in abrasion resistance and extend service life by nearly 30% in dynamic applications such as automotive bushings and industrial rollers. This performance advantage directly supports OEM strategies focused on lifecycle cost reduction and product reliability.

Asia Pacific dominates in production volume, while Europe leads in adoption, with over 52% of polyurethane formulators integrating polycarbonate ether polyols into premium-grade elastomers. By 2027, continuous polymerization technology is expected to improve throughput efficiency by 21% while reducing energy consumption per batch by 16%. Sustainability considerations are becoming central, with firms committing to ESG targets such as 25% reduction in solvent usage and 20% recyclability improvements by 2030.

In 2024, a Japanese manufacturer achieved a 19% reduction in defect rates through AI-assisted molecular weight control systems, highlighting the value of digital process optimization. Strategic pathways for the Polycarbonate Ether Polyols Market include expansion into medical-grade polymers, adoption of bio-based carbonate feedstocks, and integration with circular polyurethane recycling models. These trends position the Polycarbonate Ether Polyols Market as a pillar of material resilience, regulatory compliance, and sustainable industrial growth.

The Polycarbonate Ether Polyols market dynamics are shaped by the balance between performance-driven demand and production cost considerations. Rising use in automotive interiors, industrial belts, and medical-grade components is increasing baseline demand, while stricter durability requirements are shifting preference away from polyester-based alternatives. Manufacturers are investing in advanced catalysts and closed-loop systems to improve yield consistency and reduce waste. Supply dynamics remain stable due to long-term feedstock contracts, although energy price volatility impacts operating margins. Technological differentiation, sustainability compliance, and customization capabilities increasingly determine competitive positioning across regions.

Demand for long-life polyurethane elastomers is a primary growth driver for the Polycarbonate Ether Polyols market. In automotive applications, components formulated with polycarbonate ether polyols demonstrate 28–35% higher resistance to hydrolysis and thermal degradation. Industrial users report up to 40% reduction in replacement cycles for rollers and seals. Over 46% of new polyurethane elastomer formulations introduced between 2022 and 2024 incorporated polycarbonate ether polyols to meet extended warranty and durability requirements.

Production of polycarbonate ether polyols involves complex carbonate synthesis and controlled polymerization, resulting in costs that are 18–25% higher than conventional polyester polyols. Smaller polyurethane processors face margin pressure, limiting adoption in cost-sensitive applications. Additionally, specialized handling and processing requirements increase operational complexity, slowing penetration in emerging markets despite performance advantages.

Medical-grade polymers represent a significant opportunity for the Polycarbonate Ether Polyols market. These materials exhibit superior biostability, with degradation rates below 2% over extended use. Demand from catheter coatings, prosthetics, and wearable medical devices increased by 24% between 2021 and 2024. Specialty coatings and high-performance adhesives further expand addressable opportunities as regulatory standards tighten.

The market faces challenges from carbonate feedstock price fluctuations, which can vary by 15–20% annually. Process precision requirements also raise barriers, as minor deviations in molecular weight distribution can impact final polyurethane performance. Skilled labor shortages in advanced polymer chemistry further constrain rapid capacity scaling.

• Expansion of Sustainable Polycarbonate Chemistry: Over 41% of manufacturers are integrating low-VOC catalysts and solvent-free synthesis routes, reducing emissions by up to 22% per production cycle.

• Shift Toward Automotive Lightweighting Materials: Polycarbonate ether polyols-based elastomers now account for 36% of premium automotive polyurethane components, supporting average vehicle weight reduction of 8–10 kg.

• Digital Process Control Adoption: More than 48% of large producers have implemented real-time molecular monitoring systems, improving batch consistency by 27%.

• Growth in Medical-Grade Polyurethane Demand: Medical applications using polycarbonate ether polyols increased by 19% year-over-year, driven by demand for long-term implant stability.

The Polycarbonate Ether Polyols market is segmented by type, application, and end-user industries. Type segmentation reflects molecular weight and carbonate structure variations, influencing mechanical and chemical performance. Application-based segmentation highlights demand from automotive, industrial, medical, and footwear sectors. End-user insights reveal OEMs and specialized polyurethane formulators as primary adopters. Segmentation trends indicate increasing preference for high-purity, application-specific grades tailored to durability and compliance requirements.

Aliphatic polycarbonate ether polyols lead the segment with approximately 44% share due to superior UV stability and hydrolysis resistance. Aromatic variants hold around 31%, favored in cost-sensitive industrial uses. Cycloaliphatic and specialty grades collectively account for 25%, serving niche medical and high-performance applications. Aliphatic grades are also the fastest-growing segment, expanding at an estimated CAGR of 7.8% due to rising demand in automotive interiors and medical devices.

Automotive applications dominate with nearly 37% share, driven by demand for durable interior and under-the-hood components. Industrial machinery applications follow at 29%, while footwear accounts for 17%. Medical and specialty coatings together contribute 17%. Medical applications are the fastest-growing, supported by rising demand for biostable polymers, expanding at an estimated CAGR of 8.4%.

Automotive OEMs represent the leading end-user group with approximately 35% share, followed by industrial equipment manufacturers at 28%. Medical device companies account for 14%, footwear brands 13%, and others 10%. Medical device manufacturers are the fastest-growing end-user segment, expanding at an estimated CAGR of 8.9%, driven by long-term implant and wearable demand.

Europe accounted for the largest market share at 41.8% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Europe’s dominance is supported by strong consumption across automotive interiors, industrial elastomers, and medical-grade polyurethane systems, with more than 610,000 metric tons of advanced polyols processed annually. Asia Pacific growth is driven by rapid expansion of automotive production, electronics manufacturing, and footwear exports, with China, Japan, and South Korea collectively accounting for over 52% of regional demand. North America held approximately 24.6% share in 2024, supported by high-value applications in healthcare devices, aerospace components, and specialty coatings. South America and Middle East & Africa together contributed nearly 9.7%, reflecting gradual industrialization and rising adoption in infrastructure and energy-related polyurethane applications. Regional demand patterns highlight increasing preference for high-durability and low-maintenance polymer systems, with Asia Pacific witnessing double-digit capacity additions since 2022.

How is advanced polymer demand reshaping high-performance polyurethane adoption?

The market accounted for nearly 24.6% of global consumption in 2024, driven by automotive, healthcare, aerospace, and industrial machinery sectors. Over 68% of demand originates from automotive interiors, medical devices, and industrial rollers requiring long service life and hydrolysis resistance. Regulatory emphasis on material durability and lifecycle performance has supported adoption in healthcare and transportation. Digital process monitoring and AI-assisted formulation tools are used by over 44% of large polyurethane processors to improve batch consistency. A major domestic producer expanded specialty polycarbonate ether polyol grades for medical tubing and wearable devices, contributing to a 21% increase in medical-grade polymer usage. Consumer behavior reflects preference for premium, long-life materials in regulated industries.

Why is performance-driven regulation accelerating material innovation?

Europe held approximately 41.8% market share in 2024, with Germany, France, and the UK accounting for over 63% of regional demand. Automotive, industrial automation, and medical technology sectors dominate consumption. Sustainability mandates and chemical safety regulations have pushed more than 49% of manufacturers to adopt low-emission catalysts and recyclable polymer systems. Adoption of continuous polymerization and solvent-free processing has improved yield efficiency by 18% across major facilities. A leading regional supplier introduced next-generation aliphatic polycarbonate ether polyols for abrasion-resistant elastomers, extending component lifespan by over 30%. Consumer behavior emphasizes compliance, traceability, and material longevity.

How is manufacturing expansion driving rapid material uptake?

Asia Pacific ranks second by volume and is the fastest-growing region, led by China, Japan, South Korea, and India. The region processes over 720,000 metric tons of advanced polyols annually, with automotive and footwear accounting for nearly 57% of usage. Large-scale manufacturing hubs and cost-efficient production have accelerated capacity expansions exceeding 14% since 2021. Innovation clusters in Japan and South Korea focus on high-purity and medical-grade formulations. A regional producer introduced high-flexibility grades for electric vehicle components, improving wear resistance by 26%. Consumer behavior favors scalable, cost-efficient materials aligned with mass manufacturing.

What role does industrial modernization play in material adoption?

South America accounted for around 6.1% of global demand in 2024, led by Brazil and Argentina. Infrastructure development, automotive assembly, and energy-related equipment drive usage. Government incentives supporting domestic manufacturing increased industrial polyurethane consumption by 17% between 2021 and 2024. A regional manufacturer expanded production of polycarbonate ether polyols for industrial belts and seals, reducing replacement frequency by 22%. Consumer behavior is influenced by durability requirements in logistics and energy-intensive operations.

Why is infrastructure growth supporting specialty polymer demand?

The region contributed approximately 3.6% of global consumption in 2024, driven by UAE, Saudi Arabia, and South Africa. Oil & gas, construction, and infrastructure projects account for over 61% of regional usage. Modernization initiatives have increased adoption of long-life elastomers by 19%. A local supplier partnered with industrial contractors to supply abrasion-resistant polyurethane components for pipelines, extending maintenance cycles by 28%. Consumer behavior prioritizes durability under harsh operating conditions.

Germany – 18.9% share: Strong chemical manufacturing base and high adoption in automotive and medical-grade polyurethane systems.

China – 16.7% share: Large-scale production capacity and rising demand from automotive, footwear, and electronics manufacturing.

The Polycarbonate Ether Polyols market is moderately consolidated, with over 25 active global and regional manufacturers. The top five companies collectively account for approximately 54% of total market volume, reflecting strong technological differentiation and long-term supply contracts. Competitive strategies focus on capacity expansion, specialty grade development, and sustainability-oriented innovations. More than 62% of leading players have invested in advanced catalysts, continuous reactors, and digital quality control systems. Strategic partnerships between polyol producers and polyurethane formulators are increasing, particularly in automotive and medical sectors. Product launches emphasizing high abrasion resistance, low VOC emissions, and extended lifecycle performance are shaping competition. Smaller players compete through niche applications and regional customization, while larger firms leverage scale, R&D investment, and regulatory expertise.

Asahi Kasei Corporation

UBE Corporation

LANXESS

Dow

Huntsman Corporation

Wanhua Chemical

Tosoh Corporation

Arkema

Kuraray

LG Chem

RTP Company

Technology development in the Polycarbonate Ether Polyols market focuses on improving durability, processing efficiency, and sustainability. Advanced aliphatic carbonate synthesis enables tighter molecular weight control, improving abrasion resistance by up to 35%. Continuous flow polymerization systems have reduced batch variability by 27% while increasing throughput. Low-temperature catalysts are lowering energy consumption per ton by 15–18%. Bio-based carbonate intermediates are being piloted, with early results showing 12% reduction in carbon intensity. Digital twin modeling and AI-assisted formulation tools are now used by nearly 46% of large producers to optimize polymer chain architecture. Recycling-compatible polycarbonate ether polyols are emerging, enabling closed-loop polyurethane systems without compromising mechanical performance. These technologies collectively enhance product consistency, regulatory compliance, and lifecycle efficiency.

• In March 2024, Covestro expanded its specialty polycarbonate polyol production line to support high-durability polyurethane elastomers used in automotive interiors, increasing annual output capacity by 20%. Source: www.covestro.com

• In July 2023, BASF introduced advanced low-emission polycarbonate ether polyols designed for medical-grade polyurethane applications, improving biostability and extending product lifespan. Source: www.basf.com

• In November 2024, Mitsubishi Chemical Group announced pilot-scale production of recyclable polycarbonate ether polyols targeting circular polyurethane systems for industrial equipment. Source: www.mcgc.com

• In May 2023, Wanhua Chemical commissioned a new continuous polymerization unit for carbonate-based polyols, improving processing efficiency by 18%. Source: www.whchem.com

The Polycarbonate Ether Polyols Market Report provides a comprehensive assessment of global industry dynamics, covering material types, applications, end-user industries, and regional consumption patterns. The scope includes analysis of aliphatic, aromatic, and specialty polycarbonate ether polyols used in automotive interiors, industrial machinery, footwear, medical devices, coatings, and adhesives. Geographic coverage spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, with country-level insights for major manufacturing and consumption hubs.

The report evaluates production technologies, including continuous polymerization, low-emission catalyst systems, and recyclable polyol platforms. It examines regulatory frameworks influencing material selection, durability standards, and sustainability compliance. End-user analysis covers OEMs, polyurethane formulators, medical device manufacturers, and industrial equipment suppliers. Emerging niches such as bio-based carbonate feedstocks, circular polyurethane systems, and medical-grade elastomers are included to reflect evolving industry focus areas. The scope is designed to support strategic decision-making, investment planning, and competitive benchmarking across the Polycarbonate Ether Polyols value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,510.4 Million |

|

Market Revenue in 2032 |

USD 2,518.5 Million |

|

CAGR (2025 - 2032) |

6.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Covestro, BASF, Mitsubishi Chemical Group, Asahi Kasei Corporation, UBE Corporation, LANXESS, Dow, Huntsman Corporation, Wanhua Chemical, Tosoh Corporation, Arkema, Kuraray, LG Chem, RTP Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |