Reports

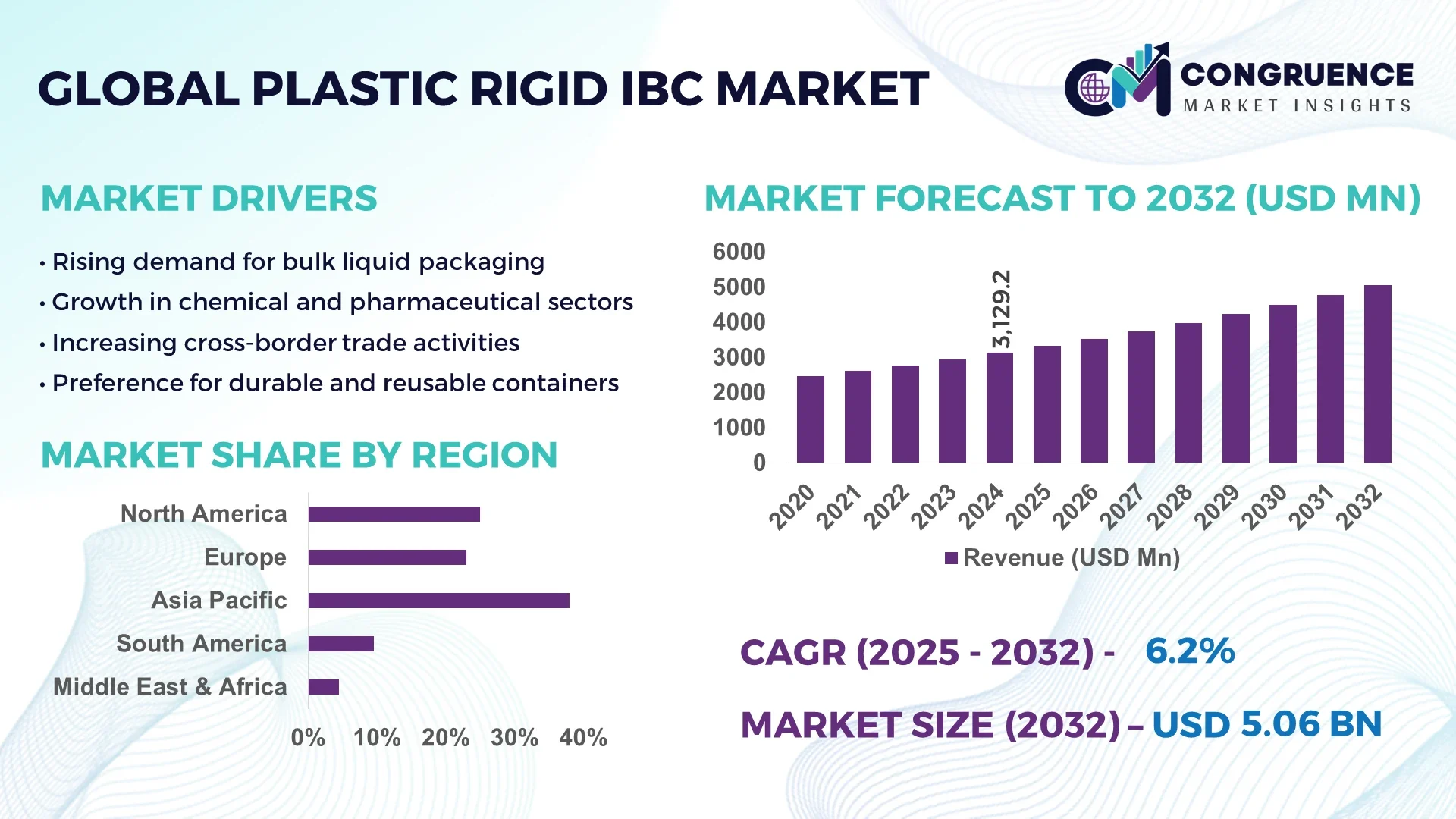

The Global Plastic Rigid IBC Market was valued at USD 3129.18 Million in 2024 and is anticipated to reach a value of USD 5063.22 Million by 2032 expanding at a CAGR of 6.2%% between 2025 and 2032.

China leads as the dominant country in the Plastic Rigid IBC Market, distinguished by its expansive production capacity and substantial investments in advanced manufacturing facilities. Cutting-edge extrusion and molding technologies, integrated with automation, enable rapid scaling of IBC output. Strategic capital allocation toward R&D has driven innovations in container durability, chemical resistance, and lightweight designs, reinforcing China’s pivotal role in shaping industry benchmarks.

Across industry sectors, industrial chemicals, petroleum and lubricants, food and beverages, paints, inks and dyes, and pharmaceuticals stand out as the principal end-users of plastic rigid IBCs. Within industrial chemicals and petroleum sectors, high-density polyethylene (HDPE) containers are extensively used for their robustness. In food and beverage and pharmaceuticals, stringent hygiene and regulatory compliance have spurred demand for food-grade materials and aseptic, tamper-evident designs. Recent innovations include UV-stabilized polyethylene formulations extending product lifecycle and multi-layer container walls enhancing barrier performance. Environmental regulations and rising sustainability mandates have increased interest in recycled polymers and monomaterial designs conducive to circular workflows. Economically, cities in Asia-Pacific exhibit surging consumption, fueled by rapid industrialization and rising logistics needs, while Europe’s moderate yet steady demand reflects focus on compliance and lifecycle efficiency. Emerging trends include smart IBCs equipped with RFID tracking, sensor-enabled fill-level monitoring, and modular nesting designs enabling space-efficient transport. Decision-makers and industry professionals are prioritizing innovation investments, aligning product evolution with regulatory dynamics, regional consumption patterns, and shifting economic drivers.

Artificial intelligence (AI) is revolutionizing the Plastic Rigid IBC Market by optimizing manufacturing efficiency, elevating quality assurance, and streamlining supply chain logistics in ways tailored for decision-makers and industry professionals. AI-driven robotics deployed on production lines reduce manual intervention and boost throughput while decreasing material waste and human error. High-precision AI-enabled quality control systems perform automated inspections of Plastic Rigid IBC containers, detecting micro-defects and ensuring consistent structural integrity. Supply chain operations leverage AI-powered predictive analytics to forecast inventory needs, aligning production scheduling with demand fluctuations and reducing holding costs. Integration of machine learning models with sensor data enables predictive maintenance of extrusion and molding machines, recognizing potential malfunctions early and minimizing unplanned downtime. These AI-based advancements support sustainable operations by reducing energy consumption through smart process control and resource allocation. In summary, AI implementation across manufacturing, inspection, logistics, and maintenance is materially enhancing efficiency, performance, and cost-effectiveness in the Plastic Rigid IBC Market without relying on speculative figures.

“In June 2025, an AI-Maglev conveyor system was piloted within a rigid plastic container plant, reducing conveyor maintenance downtime by over 30 and improving throughput by about 20 through frictionless, real-time adaptive material transport.”

The Plastic Rigid IBC Market is influenced by a combination of regulatory pressures, material innovations, and shifting consumption trends across diverse end-use industries. Increasing demand from sectors such as industrial chemicals, food and beverages, and pharmaceuticals is reinforcing the market’s steady growth trajectory. Environmental compliance is a central factor shaping container design, with stricter policies accelerating the transition toward recyclable polymers and eco-friendly materials. Logistics and global trade expansion are boosting adoption, given IBCs’ ability to handle bulk liquids efficiently and safely. Technological advancements, including smart sensors and RFID integration, are elevating supply chain visibility and efficiency. Furthermore, regional dynamics highlight rising adoption in Asia-Pacific due to rapid industrialization, while Europe continues to prioritize compliance and sustainable production standards. Together, these factors create a balanced landscape of opportunities and constraints that decision-makers must navigate.

The increasing global trade of hazardous and non-hazardous chemicals is a significant driver for the Plastic Rigid IBC Market. With industrial chemical exports crossing trillions of dollars annually, industries are emphasizing reliable and compliant packaging solutions. Plastic rigid IBCs constructed from high-density polyethylene (HDPE) provide superior chemical resistance, impact durability, and secure liquid containment. This makes them indispensable for transporting acids, solvents, and petroleum derivatives across international supply chains. Additionally, strict international standards such as UN/DOT approvals have accelerated adoption of IBCs in chemical logistics. By minimizing leakage risks and ensuring safety during long-haul transportation, plastic rigid IBCs are becoming the preferred choice for chemical manufacturers, distributors, and logistics providers worldwide.

One of the major restraints in the Plastic Rigid IBC Market is the volatility in prices of raw materials, particularly polyethylene and polypropylene. Global resin prices are heavily influenced by crude oil fluctuations, trade tariffs, and supply chain disruptions. For instance, polymer price surges of over 25 percent in some years have directly impacted production costs for container manufacturers. This creates unpredictability for businesses relying on stable cost structures, affecting profitability and investment planning. In addition, smaller manufacturers face challenges in sustaining competitiveness when raw material spikes occur, often leading to consolidation within the industry. These fluctuations not only increase procurement costs but also pressure companies to explore alternative materials and recycled inputs, which may not always meet stringent performance standards.

The Plastic Rigid IBC Market is witnessing significant opportunities through the integration of smart technologies such as IoT sensors, RFID tracking, and predictive analytics. These innovations allow real-time monitoring of fill levels, container integrity, and location across global supply chains. For example, RFID-enabled IBCs can reduce inventory discrepancies by over 40 percent while improving asset utilization efficiency. IoT-based solutions also enhance safety by providing alerts on potential leaks or temperature variations, making them highly attractive for sensitive industries like food and pharmaceuticals. As companies shift toward digitalized logistics networks, the adoption of smart IBCs is anticipated to rise, opening new revenue streams for manufacturers while supporting sustainability initiatives through improved lifecycle management and reduced product wastage.

Environmental legislation presents a complex challenge for the Plastic Rigid IBC Market. Increasing restrictions on single-use plastics and stricter recycling mandates are compelling manufacturers to redesign products for circular economy models. Compliance requires investment in advanced recycling processes and sourcing of high-quality recycled polymers, which often come with supply shortages and higher costs. Moreover, differing regulatory frameworks across regions complicate international trade, as containers approved in one jurisdiction may not meet requirements in another. For businesses operating globally, this creates additional certification costs and delays in market entry. Meeting both safety and sustainability criteria simultaneously remains a costly and technically demanding task, making regulatory compliance one of the most persistent challenges facing the industry.

• Growing Adoption of Sustainable Polymers: The Plastic Rigid IBC market is experiencing a significant shift toward sustainable materials, with over 35 percent of manufacturers in Europe integrating recycled high-density polyethylene into container production by 2024. This trend is fueled by strict environmental regulations and increasing demand from industries prioritizing low-carbon logistics solutions. Sustainable polymers not only reduce environmental footprints but also provide competitive advantages for suppliers securing contracts with eco-conscious industries.

• Integration of IoT-Enabled Smart Containers: Smart technologies are rapidly penetrating the Plastic Rigid IBC market, with RFID and IoT-based tracking solutions becoming mainstream. Companies using IoT-enabled IBCs have reported inventory error reductions of nearly 40 percent and transport efficiency gains of more than 20 percent. These advancements allow real-time monitoring of container conditions, fill levels, and geolocation, enhancing safety and reliability across supply chains. Adoption is strongest in food, beverage, and pharmaceutical logistics, where traceability is critical.

• Expansion of Cross-Border Chemical Trade: Global trade in specialty chemicals exceeded USD 2 trillion in 2024, driving increased demand for durable and compliant rigid IBCs capable of transporting hazardous materials across international routes. Plastic rigid IBCs designed with multilayer walls and chemical-resistant HDPE formulations have become standard solutions. Their compliance with UN/DOT regulations is accelerating uptake among chemical exporters and importers, especially in Asia-Pacific, where industrial expansion is intensifying container utilization.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is reshaping demand in the Plastic Rigid IBC market. In North America and Europe, prefabricated elements requiring safe storage and transportation of liquid adhesives, coatings, and construction chemicals are driving usage. Automated off-site assembly processes are increasing demand for high-capacity IBCs capable of ensuring quality retention of sensitive construction inputs. With modular construction projects reducing labor needs and cutting project timelines by up to 30 percent, IBC demand in this sector is witnessing measurable growth.

The Plastic Rigid IBC market segmentation reflects diverse product types, applications, and end-users that collectively shape its growth dynamics. By type, high-density polyethylene-based containers dominate due to their chemical resistance and durability, while composite variants are gaining momentum with innovations in lightweight structures. Applications range from chemicals, food and beverages, pharmaceuticals, paints, and lubricants, each contributing distinctly to demand. Chemicals lead due to bulk transport needs, while pharmaceuticals are expanding rapidly with heightened regulatory focus. In terms of end-users, industrial chemical manufacturers remain the largest adopters, but food and beverage companies are increasingly driving growth by prioritizing hygienic, recyclable, and traceable packaging solutions. This segmentation underscores how product differentiation and sector-specific requirements are influencing market expansion.

The Plastic Rigid IBC market is primarily categorized into high-density polyethylene (HDPE), composite, and other specialty container types. HDPE-based rigid IBCs lead the segment owing to their exceptional resistance to chemicals, impact strength, and compatibility with hazardous and non-hazardous liquids. They are widely adopted in chemical and petroleum industries for bulk handling. Composite IBCs are the fastest-growing type, driven by rising demand for lightweight designs that provide structural reinforcement and reduced transport costs. These containers often combine polyethylene with steel cages, delivering superior durability and safety in long-haul logistics. Other types, including specialized barrier-coated IBCs, cater to niche applications in food-grade and pharmaceutical packaging where contamination control is critical. The dominance of HDPE and rapid adoption of composite structures highlight the market’s dual emphasis on reliability and cost efficiency.

Applications of plastic rigid IBCs span chemicals, food and beverages, pharmaceuticals, lubricants, paints, coatings, and agrochemicals. Chemicals represent the leading application segment due to stringent safety requirements and the sheer scale of international trade in industrial liquids. The fastest-growing application is pharmaceuticals, as rising production of vaccines, biologics, and liquid drugs requires sterile, tamper-proof, and traceable storage solutions. Food and beverages also play a significant role, with demand increasing for food-grade IBCs capable of storing edible oils, juices, and flavor concentrates. Lubricants and coatings rely on rigid IBCs for consistent bulk storage and transport, while agrochemicals utilize these containers for fertilizers and liquid pesticides. Collectively, these applications highlight the adaptability of rigid IBCs to varying industry needs, with growth strongest in high-compliance and sensitive sectors.

The leading end-user of plastic rigid IBCs is the industrial chemical sector, where the large-scale need for safe transportation and storage of hazardous liquids drives substantial container utilization. Chemical producers and exporters prefer rigid IBCs due to their compliance with international safety standards and cost-effectiveness in bulk movement. The fastest-growing end-user is the food and beverage industry, where demand for hygienic, reusable, and food-grade certified IBCs is accelerating. Rising global consumption of processed foods and beverages has intensified container adoption in this segment. Pharmaceuticals are another expanding end-user, where strict sterility and traceability standards encourage the use of advanced, smart-enabled IBCs. Other notable contributors include paints, coatings, and agrochemical industries that depend on IBCs for efficient handling of specialized liquid products. Together, these end-user dynamics emphasize the versatility and industry-wide reliance on rigid plastic IBC solutions.

Asia-Pacific accounted for the largest market share at 41.7 percent in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.3 percent between 2025 and 2032.

Asia-Pacific benefits from strong industrial output, large-scale chemical exports, and rising demand in the food and beverage sector. Meanwhile, Middle Eastern and African markets are increasingly investing in infrastructure and energy projects, which significantly boost the adoption of durable bulk storage and transport solutions. The combination of high consumption and expanding industrial ecosystems makes these regions central to the global outlook for plastic rigid IBC adoption.

Technological integration driving packaging efficiency

North America accounted for 23.5 percent of the global Plastic Rigid IBC market in 2024, with demand led by industries such as chemicals, pharmaceuticals, and processed food. Stringent government regulations around hazardous materials handling have encouraged broader use of certified high-density polyethylene IBCs. Notably, regulatory frameworks like OSHA compliance standards and FDA-approved food-grade packaging requirements have influenced product adoption. Technological integration, including RFID-enabled IBCs and IoT-driven monitoring systems, is improving operational efficiency for logistics companies. The region’s manufacturing base is adopting automation to enhance durability and reduce production time, which positions North America as a significant contributor to innovation in this market.

Eco-innovation shaping industrial logistics solutions

Europe represented 21.4 percent of the Plastic Rigid IBC market in 2024, with Germany, France, and the UK emerging as major contributors. Strict sustainability mandates driven by the European Commission and national regulatory bodies are propelling demand for recyclable polymers in rigid IBC production. Green packaging initiatives and the circular economy framework are encouraging the adoption of monomaterial designs that simplify recycling. Advanced technologies, such as RFID-enabled smart tracking and UV-stabilized polymer innovations, are gaining traction in logistics. With its strong focus on compliance and eco-innovation, the region is at the forefront of transitioning the rigid IBC sector toward sustainable and digitally optimized solutions.

Expanding manufacturing capacity supporting high-volume consumption

Asia-Pacific accounted for 41.7 percent of the Plastic Rigid IBC market in 2024, making it the largest regional contributor. China, India, and Japan are the top consumers, with China holding the most significant share due to massive chemical and industrial liquid exports. Infrastructure expansion projects and rising food processing industries in India and Southeast Asia are further driving container demand. The region is also home to innovation hubs focused on advanced molding techniques and recyclable material applications, ensuring scalable production. High-volume manufacturing capacity, coupled with rising regional trade flows, continues to strengthen Asia-Pacific’s leadership in this market.

Infrastructure and energy projects boosting bulk packaging adoption

South America held 6.8 percent of the Plastic Rigid IBC market in 2024, with Brazil and Argentina emerging as primary consumers. The demand is driven by the chemical, agricultural, and energy sectors, which require reliable bulk transport solutions. Brazil’s oil and gas sector is adopting durable IBCs to streamline liquid handling, while Argentina is witnessing rising demand from agrochemicals and food processing industries. Infrastructure development projects and government trade incentives are further supporting regional growth. This combination of sectoral demand and policy support positions South America as an emerging contributor to the global market.

Energy-driven demand fueling industrial container adoption

The Middle East & Africa accounted for 6.6 percent of the Plastic Rigid IBC market in 2024, with countries such as the UAE, Saudi Arabia, and South Africa leading consumption. Demand is driven primarily by the oil and gas sector, alongside rapid infrastructure and construction growth. Local regulations encouraging safe transport of hazardous materials are pushing adoption of certified high-density polyethylene containers. Technological modernization, including IoT integration for transport monitoring, is gaining traction in logistics hubs like Dubai. Trade partnerships and diversification of regional economies are further boosting market opportunities, establishing the region as the fastest-growing globally between 2025 and 2032.

China 28.9 % Dominance driven by large-scale chemical exports and expansive manufacturing capacity.

United States 18.4 % Strong demand from pharmaceuticals, chemicals, and food industries combined with advanced regulatory compliance frameworks.

The Plastic Rigid IBC market is characterized by a moderately consolidated competitive landscape, with more than 35 active global and regional players shaping industry dynamics. Large multinational corporations dominate through extensive product portfolios and established distribution networks, while regional manufacturers compete by offering cost-efficient and locally customized solutions. Strategic partnerships and collaborations with chemical, pharmaceutical, and logistics companies are becoming increasingly common, allowing manufacturers to expand market presence and enhance customer value. In recent years, innovation trends such as the integration of IoT-enabled smart IBCs, the development of recyclable polymer solutions, and modular design advancements have intensified competition. Several players are also investing in acquisitions to strengthen supply chain resilience and extend geographic reach, particularly in emerging markets. Competitive positioning is now increasingly defined not only by durability and compliance but also by sustainability performance and digital integration, with companies aligning strategies to meet evolving global regulatory and customer requirements.

Greif Inc.

SCHÜTZ GmbH & Co. KGaA

Mauser Packaging Solutions

Time Technoplast Ltd.

Snyder Industries LLC

Hoover Ferguson Group

Schoeller Allibert Services B.V.

Berry Global Inc.

IPL Plastics Inc.

Werit Kunststoffwerke W. Schneider GmbH & Co. KG

Technological advancements are significantly transforming the Plastic Rigid IBC market, with innovations focused on durability, sustainability, and digital integration. High-density polyethylene (HDPE) continues to dominate container production, but manufacturers are increasingly adopting multi-layer wall designs that enhance barrier protection against aggressive chemicals while reducing overall material weight. UV-stabilized polymers are being incorporated to extend service life, particularly for containers stored outdoors in extreme climates. Another critical innovation is the development of recyclable and bio-based polymers, with several producers integrating up to 30 percent recycled content without compromising structural integrity.

Digitalization is also reshaping the competitive landscape. RFID-enabled IBCs and IoT-integrated monitoring systems now allow companies to track fill levels, location, and integrity in real time. These smart solutions improve supply chain transparency, reduce losses from leakage, and optimize container utilization rates by more than 20 percent. Predictive maintenance supported by AI-driven analytics is reducing downtime in manufacturing lines by identifying equipment issues before they cause failures.

In addition, automation technologies in blow molding and extrusion processes are enhancing production efficiency, lowering defect rates, and enabling large-scale customization. Modular cage designs and foldable structures are being developed to improve space optimization during return logistics. Collectively, these emerging technologies are driving efficiency, sustainability, and customer value, aligning the market with future regulatory and operational requirements.

• In March 2023, Mauser Packaging Solutions introduced a new generation of rigid IBCs with enhanced multilayer HDPE walls designed to reduce material use by 15 percent while improving chemical resistance for industrial liquids.

• In July 2023, SCHÜTZ GmbH expanded its production facilities in the United States, increasing capacity by 20 percent to meet growing demand from the chemical and food sectors for high-volume plastic rigid IBCs.

• In February 2024, Greif Inc. launched an IoT-enabled smart IBC platform that integrates RFID and sensor technologies, enabling real-time monitoring of liquid levels, location tracking, and leak detection to support digitalized supply chains.

• In May 2024, Time Technoplast Ltd. announced the development of recyclable rigid IBCs made with 35 percent post-consumer recycled plastic, aligning with circular economy practices and reducing carbon emissions across logistics operations.

The Plastic Rigid IBC Market Report provides a comprehensive assessment of the industry’s structure, covering product types, applications, end-users, and geographic markets. The report examines rigid IBCs manufactured from high-density polyethylene, composite materials, and specialty barrier-coated polymers, offering insights into their adoption across multiple industries. It further analyzes applications spanning chemicals, pharmaceuticals, food and beverages, lubricants, agrochemicals, paints, and coatings, each segment evaluated for its contribution to overall demand. Geographically, the report covers five key regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Detailed insights highlight top contributing countries, including China, the United States, Germany, India, and Brazil, with emphasis on consumption patterns, industrial investments, and regulatory frameworks.

The report also explores technological innovations, from IoT-enabled smart IBCs and RFID-based tracking systems to bio-based polymers and recyclable designs. Industry professionals will find in-depth coverage of regulatory influences, sustainability initiatives, and trade dynamics that are shaping competitive strategies. Niche segments, such as foldable and modular IBCs designed for space optimization, are also addressed, reflecting emerging opportunities. By combining insights on market dynamics, regional growth, technological innovation, and end-user adoption, the report equips decision-makers with a strategic overview of the current landscape and the future trajectory of the Plastic Rigid IBC industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3129.18 Million |

|

Market Revenue in 2032 |

USD 5063.22 Million |

|

CAGR (2025 - 2032) |

6.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Greif Inc., SCHÜTZ GmbH & Co. KGaA, Mauser Packaging Solutions, Time Technoplast Ltd., Snyder Industries LLC, Hoover Ferguson Group, Schoeller Allibert Services B.V., Berry Global Inc., IPL Plastics Inc., Werit Kunststoffwerke W. Schneider GmbH & Co. KG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |