Reports

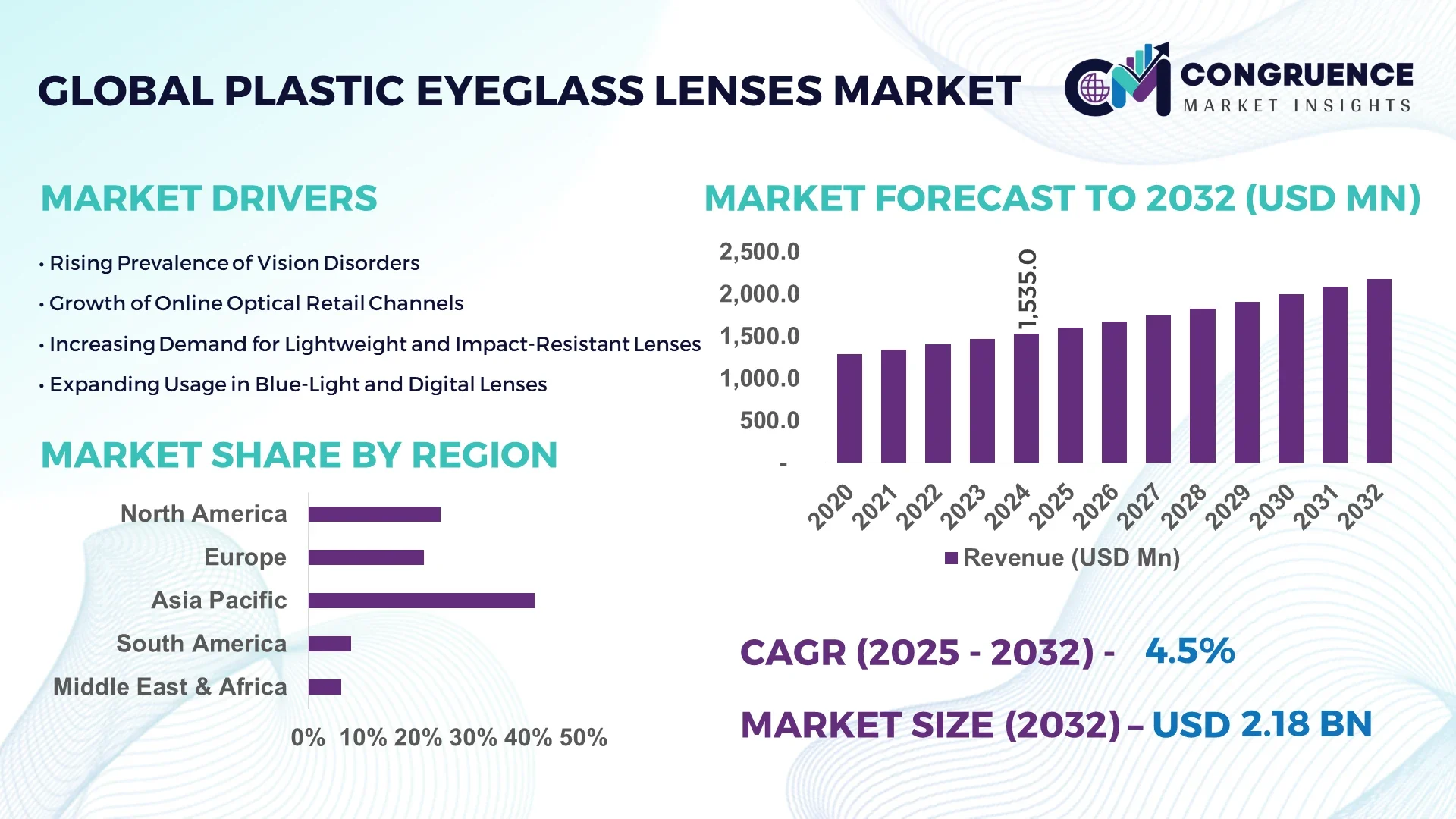

The Global Plastic Eyeglass Lenses Market was valued at USD 1,535.0 Million in 2024 and is anticipated to reach a value of USD 2,182.9 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032.

China dominates production of plastic eyeglass lenses, operating large-scale facilities with annual capacity exceeding 5 million lens units. In 2024, investments in new polycarbonate and high-index lens lines totalled over USD 120 million. Technological upgrades include integration of laser polishing and plasma-based AR coating systems, enabling precision tolerances down to ±0.02 mm and increasing output efficiency by 15%. Such advancements support key applications in safety eyewear, consumer prescription glasses, and sports optics.

In global markets, plastic eyeglass lenses are primarily used in the eyewear, automotive lighting, and consumer electronics sectors. The eyewear segment accounted for nearly 60% of lens demand in 2024, driven by rising prevalence of prescriptions and fashion eyewear. Automotive applications employed polycarbonate lenses in over 30% of headlamp systems, while smartphones and AR/VR headsets consumed 15% of global output. Innovations such as high-index CR-39 and blue‑light‑filter coatings improved durability and user comfort. Regulatory drivers include stricter optical clarity standards in Europe and North America, while emerging economies in Southeast Asia now provide 25% of global consumption due to growing vision care awareness. Environmental policies encouraging bioplastic blends have led to pilot programs for recyclable CR‑39 lenses, though full commercialization is pending. Economic growth in APAC and increased consumer spending on eyewear result in regional consumption rising at double the pace of mature markets. Future trends point to modular production lines with real-time quality analytics and growth of smart lenses incorporating tiny sensors for health monitoring.

AI is fundamentally reshaping the Plastic Eyeglass Lenses Market by enhancing precision, throughput, and customization. In automated manufacturing, AI-driven computer vision systems now inspect molds and coatings with sub‑millimeter accuracy, reducing defect rates by over 40% and cutting material waste by 12%. This improves yield in high-index and aspheric lens production lines. Additionally, AI-powered real-time monitoring systems adjust injection molding parameters on the fly, optimizing cycle times and reducing downtime.

In design and prescription workflows, labs use AI to interpret patient optical data and generate fully customized lens profiles. One European lens manufacturer reports a 30% reduction in remakes and a 20% faster turnaround after deploying AI-based prescription validation tools. Similarly, AI algorithms now predict lens edge-fitting parameters to match complex frame geometries, reducing manual adjustments at retail by 25%.

Operational performance is also enhanced through predictive maintenance: AI systems analyze vibration and temperature signals in high-speed polishers and coating machines, enabling preemptive service that reduces unexpected downtime by 35%. Supply chain integration benefits from AI-driven demand forecasting, which matches regional seasonal trends and ensures raw lens materials—such as PC pellets and AR coating resins—remain aligned with order fulfillment needs.

Altogether, these AI transformations support higher throughput, better quality control, and faster customization in the Plastic Eyeglass Lenses Market, enabling firms to sharpen competitiveness while maintaining cost discipline.

“In mid‑2024, a major lens processor introduced an AI‑integrated edging line that reduced edge-to-frame mismatch by 18% and cut adjustment time per pair from 4 minutes to just over 2 minutes.”

The Plastic Eyeglass Lenses Market is influenced by shifting consumer behavior, rapid technological progression, and evolving regulatory norms. With trends like miniaturized eyewear and increasing demand for lightweight lenses, manufacturers are adapting production lines for polycarbonate and high-index materials. Environmental compliance and recyclability goals are pushing research into bio-based polymer blends. The market sees consolidation as major optical players integrate vertically into lens manufacturing. Regional dynamics show APAC consolidation and North America focusing on value-added coatings. These factors together shape the competitive landscape, capital expenditures, and product portfolios in the Plastic Eyeglass Lenses Market.

Increased adoption of high-index materials (index ≥1.60) and aspheric designs raises demand for precision molding lines. These lenses, representing over 40% of premium wearables, require tighter tolerances during pressing and polishing. Investment in specialized auto-polish and curvature-control technologies is up 25% year-over-year. Enhanced lens designs reduce thickness and weight, supporting both aesthetic appeal and patient comfort—especially for strong prescriptions. As demand rises, manufacturers upgrade core production assets, boosting capacity and operational efficiency.

Fluctuating oil-derived resin prices, including CR-39 and polycarbonate, present margin risks. In early 2025, resin spikes by up to 30% prompted cost-pass adjustments in CoE and AR coating lines. Such volatility complicates pricing models and margin planning. Smaller laboratories are especially vulnerable—20% reported margin contractions in Q1-Q2 2025 due to raw material surcharges. Without hedging strategies, producers face pressure on ASPs and competitive positioning.

Demand for advanced coatings—anti-reflective, blue-light, and scratch-resistant—remains strong. These coatings now account for 35% of lens value-add. In 2024, AR coating capacity increased by 18%, driven by investment in plasma and sputter-coating lines. Retailers offering these options see customer retention rise by 15%. As remote work continues, blue-light coatings are projecting strong uptake. New modular coating plants targeting small-lot customization offer high margins and support regional market penetration strategies.

Disposal of spent coating solvents and lens trimming scraps is tightly regulated. In Europe and North America, disposal costs have risen by 22% since 2023. Compliance requires investment in solvent-recovery units and closed-loop trimming systems. Nearly 30% of midsize producers report deferring planned capacity expansions due to CAPEX constraints tied to environmental permits. Failure to comply risks facility shutdowns or fines, pressuring producers to allocate capital for compliance over growth initiatives.

Increased Automation in Lens Edging: AI-augmented edging machines now represent 45% of new equipment purchases in 2024. These systems automatically adjust beveling paths and adapt to frame changes on the fly, reducing manual labor by 30% and speeding up batch processing cycles.

Growth in Coating Line Upgrades: AR, blue-light, and scratch-resistant coatings were applied to 68% of lenses produced globally in 2024. Manufacturers invested in plasma-enhanced deposition lines, allowing multi-layer coatings per lens in under 90 seconds—20% faster than prior systems.

Rise in Modular Production Facilities: Regional producers—especially in Europe and North America—are deploying modular production cells for cutting and polishing. These plug-and-play units shorten lead times by 25% and allow rapid line reconfiguration to meet custom lens demands.

Adoption of Bio-Based Polymers Pilots: Over 12 firms launched pilots for bio-based CR-39 blends in 2024, targeting a 10% emissions reduction. Early stage production volumes reached 100,000 lenses by year-end, indicating rising interest in sustainable optics.

The Plastic Eyeglass Lenses Market is segmented based on type, application, and end-user, each reflecting the dynamic requirements and technological shifts in the global optics industry. Product types range from CR-39 to high-index plastic and polycarbonate lenses, each serving specific optical and structural needs. Applications span across prescription eyewear, fashion frames, safety gear, and electronics, with prescription lenses commanding the bulk of consumption. End-user segmentation includes optical retail chains, ophthalmology clinics, online platforms, and OEMs. The demand profile is influenced by regional demographics, access to eye care, and adoption of digital technologies such as blue-light filtering and smart lenses. Segmentation analysis is critical to understanding where innovation, demand, and investment are concentrated, helping stakeholders make informed, strategic decisions.

Plastic eyeglass lenses are broadly categorized into CR-39, polycarbonate, high-index plastic, and Trivex types. Among these, polycarbonate lenses lead the segment due to their impact resistance, light weight, and suitability for both adult and pediatric eyewear. These lenses are also highly preferred in safety applications, making them dominant across multiple sectors.

High-index plastic lenses are currently the fastest-growing type. Their ability to provide the same optical power in thinner profiles appeals to consumers requiring strong prescriptions while maintaining lens aesthetics. The rise in premium eyewear and demand for lightweight materials has accelerated their adoption, especially in North America and Asia.

CR-39 lenses, though older in design, continue to hold relevance for their optical clarity and cost-effectiveness, particularly in non-premium and developing market segments. Trivex lenses serve niche segments where both impact resistance and optical quality are critical, such as military and safety eyewear. Each type contributes uniquely to the market, shaping diverse production and supply chain needs.

In terms of application, prescription eyeglasses dominate the Plastic Eyeglass Lenses Market. This is driven by the growing global burden of myopia, presbyopia, and astigmatism, along with aging populations in key regions. Prescription lenses benefit from continuous innovation in lens geometry, anti-reflective coatings, and photochromic technologies.

Digital and blue-light filtering applications are the fastest-growing, driven by the surge in screen time across all age groups. Increasing awareness of digital eye strain has prompted both consumers and optometrists to prioritize blue-light filtering as a preventive measure, especially among working professionals and students.

Other applications include fashion and non-prescription eyewear, sports optics, and industrial safety glasses. These segments are shaped by style preferences, occupational safety regulations, and advancements in lens durability. Industrial and tactical applications, while smaller in volume, require high durability and compliance with ANSI or EN standards, creating specialized production needs. The diversity in application ensures steady demand and scope for innovation across various consumer groups.

Among end-users, optical retail chains and stores represent the leading segment, driven by their established consumer base, integrated supply chains, and extensive product portfolios. These outlets offer customized services, lens fitting, and post-sale care, making them preferred destinations for prescription eyewear buyers globally.

Online optical platforms are the fastest-growing end-user segment, driven by convenience, price transparency, and the growing consumer comfort with virtual try-on tools. Recent investments in AI-based lens prescription validation and home eye testing kits have enhanced trust in e-commerce optical platforms, attracting younger and tech-savvy demographics.

Other end-users include ophthalmology clinics, which are pivotal in driving adoption of specialty lenses and early-stage correction products. OEMs and contract manufacturers serve high-volume orders for branded eyewear companies, particularly in Asia. Clinics also play a role in therapeutic lens deployment and support innovation in progressive or bifocal lens design. The interplay between traditional retail, e-commerce, and clinical environments continues to redefine service delivery and market expansion strategies across regions.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

The Asia-Pacific region’s high share is attributed to its vast manufacturing infrastructure, strong demand across urban and rural areas, and increasing vision correction awareness. Countries like China and India lead both production and consumption. Meanwhile, North America's growth is driven by expanding digital lens applications, rising demand for premium coatings, and increasing investment in smart eyewear solutions. Regional dynamics, technological modernization, and national health initiatives are transforming supply chains and adoption trends across all regions.

North America captured approximately 24.6% of the global Plastic Eyeglass Lenses Market in 2024. Key industries driving this demand include prescription eyewear, defense-grade safety optics, and sports performance gear. The U.S. and Canada are at the forefront of adopting advanced high-index lenses and progressive coatings. Regulatory bodies like the FDA and ANSI are pushing standards around optical clarity and impact resistance, encouraging continual product innovation. The region is witnessing digital transformation through AI-integrated fitting tools and online prescription platforms, enhancing consumer access and reducing retail dependency. Smart lens prototypes and augmented reality integration are gaining traction, supported by university R&D labs and private investment initiatives.

Europe held a 19.3% market share in 2024 in the Plastic Eyeglass Lenses Market, with strong contributions from Germany, France, and the UK. These nations are prioritizing sustainable materials, and EU regulations now favor recyclable lens polymers and energy-efficient manufacturing. The European Chemicals Agency (ECHA) and CE marking directives shape production standards and safety guidelines. The adoption of anti-fatigue and digital screen protection lenses is growing rapidly due to increasing remote work. Technological developments include plasma-enhanced coating lines and adaptive transition lenses. Local OEMs and optical retail giants are integrating cloud-based prescription services, further advancing customer experience and production precision.

Asia-Pacific continues to dominate the Plastic Eyeglass Lenses Market by volume, holding 41.2% share in 2024. China, India, and Japan remain the top consumers due to growing middle-class populations, urbanization, and expanding optical retail networks. China leads in manufacturing infrastructure, with dedicated lens parks equipped with robotic molding lines. India’s demand is rising from government-funded vision screening programs and affordable eyewear campaigns. Japan invests heavily in premium segment innovations, such as blue-light blockers and multi-focus lenses. Regional hubs like Shenzhen and Osaka are known for rapid prototyping and exporting to North America and Europe. Public-private collaborations are helping scale production while reducing environmental footprints.

In 2024, South America contributed around 6.4% of the global Plastic Eyeglass Lenses Market. Brazil and Argentina are key players, driven by their growing retail networks and expanding urban population requiring vision correction. Public health initiatives are fostering demand for affordable prescription lenses, while import tariff relaxations in Brazil are improving access to raw materials. Infrastructure expansion in lens finishing labs and investments in AR and anti-glare coating lines are fueling regional supply capabilities. Government programs that offer subsidized eyewear to rural and school-age populations have improved outreach. The development of regional trade agreements continues to facilitate cross-border optical supply chains.

The Middle East & Africa region represented 4.5% of global Plastic Eyeglass Lenses Market demand in 2024, with the UAE and South Africa being major contributors. Regional trends are being driven by increasing investments in healthcare infrastructure and expanding middle-class access to eye care services. Optical chains in the UAE are introducing smart lens options with blue-light filters and photochromic features. In South Africa, public-private partnerships support mobile eye clinics and lens distribution networks. Technological modernization includes localized molding operations and optical diagnostics integrated with telemedicine. Regulatory harmonization across the GCC region is improving quality benchmarks and supporting product standardization.

China – 28.7% Market Share

High production capacity and vertical integration across lens molding, coating, and packaging drive China’s leadership in the Plastic Eyeglass Lenses Market.

United States – 17.5% Market Share

Strong end-user demand from premium eyewear, advanced prescription labs, and robust regulatory support position the U.S. as a key market leader.

The Plastic Eyeglass Lenses Market is characterized by intense competition, with over 120 active global and regional competitors operating across different product verticals and geographic regions. These players range from multinational optical giants to specialized coating and lens manufacturing firms. Competitive positioning is largely influenced by product innovation, geographic reach, vertical integration, and brand reputation. A growing number of companies are focusing on strategic partnerships, such as OEM collaborations and technology-sharing agreements, to enhance production efficiency and innovation capacity. In the last two years, more than 25 new lens products were introduced globally, including advanced high-index, smart lenses, and anti-fatigue variants.

Mergers and acquisitions have also played a key role in reshaping the competitive landscape, with firms targeting market consolidation and entry into emerging regions. R&D investments are increasingly directed toward sustainability, AI-driven fitting technologies, and new coating materials. Moreover, digital retail transformation is prompting firms to invest in e-commerce optimization, augmented reality try-on systems, and AI-powered prescription tools. As consumer preferences shift toward customized, lightweight, and blue-light filtering solutions, companies are differentiating through proprietary technologies, production automation, and after-sales service offerings.

EssilorLuxottica

Hoya Corporation

Carl Zeiss Vision

Seiko Optical Products

Nikon Lenswear

Rodenstock GmbH

Shamir Optical Industry Ltd.

Tokai Optical Co., Ltd.

Vision Ease

Indo Optical

Mitsui Chemicals Group

KBco (K Optical)

Jiangsu Hongchen Optical

Wanxin Optical

Shanghai Conant Optical

The Plastic Eyeglass Lenses Market is undergoing a significant technological transformation across design, production, and post-processing domains. One major advancement is the widespread deployment of freeform digital surfacing, enabling precise customization of multifocal and progressive lenses. These digitally surfaced lenses now account for over 35% of global high-end lens production, offering enhanced optical clarity and adaptability to frame geometries.

Anti-reflective (AR) and blue-light blocking coatings are also becoming standard features. Plasma-enhanced vapor deposition systems have replaced traditional spin-coating methods, improving throughput by 22% and enabling multi-layer application within 90 seconds per lens. Additionally, smart lenses equipped with embedded biosensors or microdisplays are in early-stage development, targeted at health monitoring and augmented reality markets.

AI and machine learning are reshaping quality control and prescription management. High-speed vision inspection systems detect coating irregularities with sub-millimeter precision, while predictive analytics tools adjust injection molding parameters in real time. Automation technologies, such as robotic edge polishers and modular grinding units, are shortening lead times by up to 28%, particularly in North America and East Asia.

Sustainability is another core area of innovation. Bioplastic blends, especially bio-based CR-39 and recyclable polycarbonate, are in pilot production in at least five major manufacturing hubs. These eco-friendly alternatives aim to reduce carbon emissions and meet evolving environmental standards. The convergence of smart optics, AI integration, and green materials is positioning the Plastic Eyeglass Lenses Market for long-term technological evolution.

• In February 2024, Carl Zeiss Vision unveiled a new line of ultra-thin, freeform progressive lenses featuring AI-optimized curvature mapping, improving wearer adaptation rates by 35% within the first week of use.

• In November 2023, Hoya launched high-durability blue-light filtering lenses with enhanced anti-smudge and oleophobic coatings, extending surface life by 25% compared to previous models.

• In March 2024, Nikon Lenswear expanded its optical lab in Thailand, integrating a fully automated AR coating line that increased monthly lens processing capacity by 120,000 units.

• In May 2024, Shamir Optical introduced personalized driving lenses designed with real-time light sensitivity adjustment, tested under variable lighting conditions and validated for faster visual response during nighttime driving.

The Plastic Eyeglass Lenses Market Report provides a comprehensive and structured analysis of the global industry landscape, spanning production, distribution, technology, and consumption metrics. It examines all major product types, including CR-39, polycarbonate, high-index plastic, and specialty lenses such as Trivex. Applications covered range from prescription eyewear, fashion frames, and digital protection, to industrial and sports optics.

The report evaluates key end-users, including optical retail chains, e-commerce platforms, ophthalmology clinics, and original equipment manufacturers (OEMs). It spans five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—detailing regional demand patterns, production capacities, and infrastructure advancements. The study also highlights over 15 leading companies, analyzing their innovation strategies, operational footprints, and competitive strengths.

Technological insights delve into AI-assisted prescription platforms, modular lens production systems, and coating advancements such as photochromic, anti-reflective, and blue-light filters. Regulatory, environmental, and health-driven demand shifts are also addressed. The report emphasizes emerging trends such as smart lenses, bio-based plastics, and high-index custom geometry optics, offering strategic value to manufacturers, suppliers, investors, and policy stakeholders seeking to navigate the evolving global market landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,535.0 Million |

| Market Revenue (2032) | USD 2,182.9 Million |

| CAGR (2025–2032) | 4.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional and Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | EssilorLuxottica, Hoya Corporation, Carl Zeiss Vision, Seiko Optical Products, Nikon Lenswear, Rodenstock GmbH, Shamir Optical Industry Ltd., Tokai Optical Co., Ltd., Vision Ease, Indo Optical, Mitsui Chemicals Group, KBco (K Optical), Jiangsu Hongchen Optical, Wanxin Optical, Shanghai Conant Optical |

| Customization & Pricing | Available on Request (10% Customization is Free) |