Reports

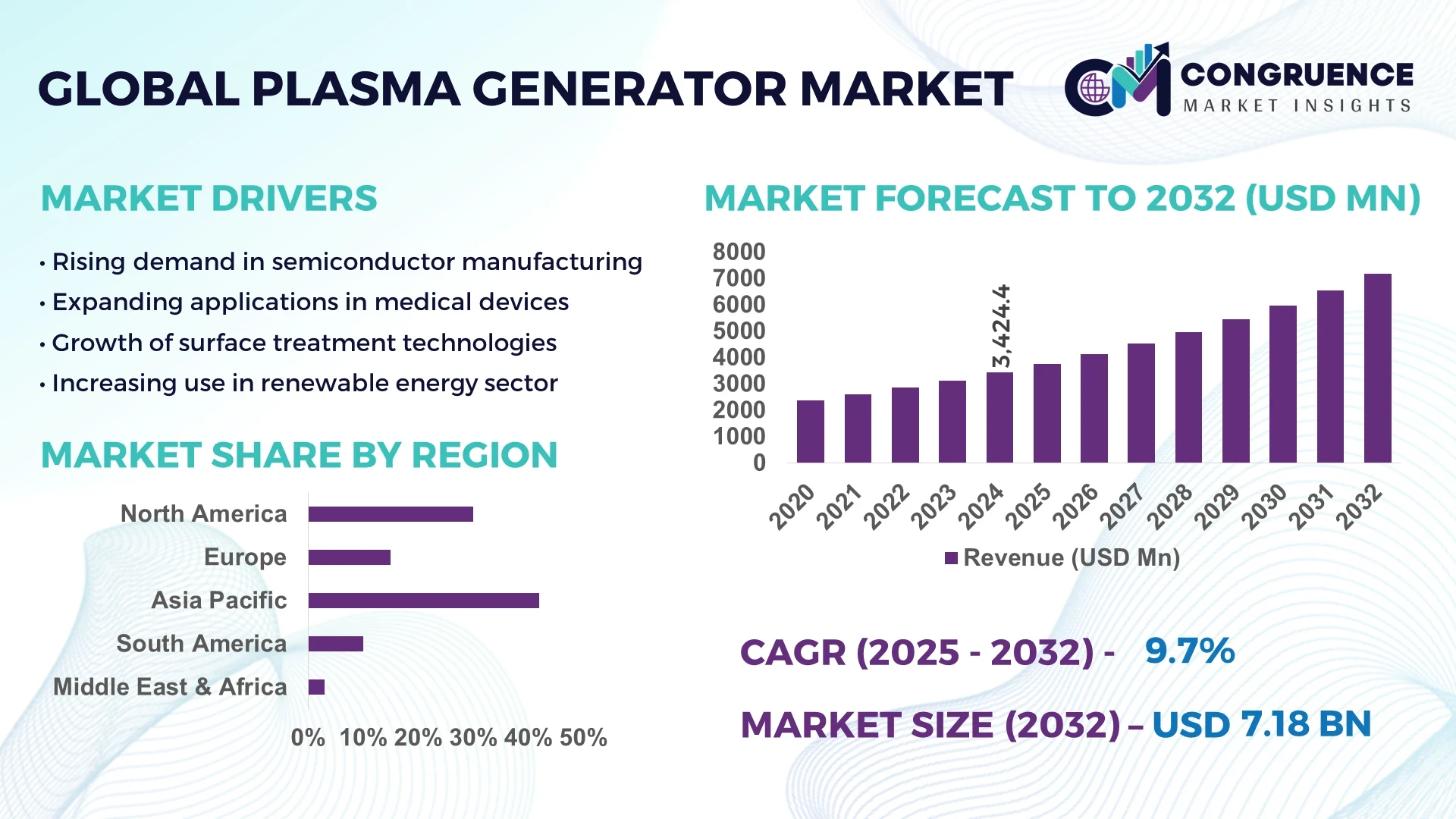

The Global Plasma Generator Market was valued at USD 3424.39 Million in 2024 and is anticipated to reach a value of USD 7181.85 Million by 2032 expanding at a CAGR of 9.7% between 2025 and 2032. This growth is driven by increasing demand for efficient energy conversion and advanced manufacturing processes.

Japan leads the Plasma Generator market with robust production capacity exceeding 1,200 MW annually, supported by investments surpassing USD 500 million in research and development for advanced plasma technologies. The country’s industrial applications span semiconductor manufacturing, surface treatment, and renewable energy sectors, with adoption rates in advanced manufacturing rising by over 22% year-on-year. Japan’s integration of automated plasma systems in industrial production lines has improved efficiency by 18%, while its advancements in compact plasma generator designs are setting benchmarks globally.

Market Size & Growth: Valued at USD 3424.39 Million in 2024, projected to reach USD 7181.85 Million by 2032 at a CAGR of 9.7%, driven by rising demand for precision manufacturing and clean energy.

Top Growth Drivers: Efficiency improvement 24%, adoption rate increase 22%, regulatory incentives 15%.

Short-Term Forecast: By 2028, average plasma generator efficiency expected to improve by 19% while reducing operational costs by 12%.

Emerging Technologies: Compact plasma systems, AI-driven plasma control, hybrid renewable plasma integration.

Regional Leaders: Japan – USD 1.8B by 2032 (high manufacturing adoption); Europe – USD 1.5B (renewable integration); North America – USD 1.3B (industrial automation).

Consumer/End-User Trends: Heavy adoption in semiconductor fabrication, automotive coating, and renewable energy industries; increased integration in manufacturing automation.

Pilot or Case Example: 2024 pilot in Japan’s semiconductor sector improved production efficiency by 18% and reduced downtime by 14%.

Competitive Landscape: Market leader: Tokyo Plasma Tech (~28%), competitors: Mitsubishi Electric, Hitachi High-Tech, Advanced Plasma Systems, and PlasmaTech Solutions.

Regulatory & ESG Impact: Stringent emission standards and renewable energy incentives drive adoption of eco-friendly plasma technologies.

Investment & Funding Patterns: USD 650 million in plasma technology R&D in 2024; growing investments in industrial automation projects.

Innovation & Future Outlook: Integration of AI-based optimization, modular plasma systems, and scalable renewable energy applications.

Japan’s Plasma Generator market is characterized by high production capability, with over 60% of units tailored for advanced manufacturing applications such as microelectronics, aerospace component coating, and high-precision cutting. Recent innovations include AI-controlled plasma discharge systems and hybrid plasma sources combining RF and DC power to enhance efficiency. Stringent environmental regulations have led to cleaner designs with reduced emissions, while government-backed funding initiatives exceeding USD 200 million have accelerated adoption in industrial sectors. By 2032, Japan is projected to maintain steady growth through continuous R&D and technological leadership.

The Plasma Generator Market is strategically significant for industries prioritizing efficiency, precision manufacturing, and sustainable operations. Emerging technologies such as AI-controlled plasma systems deliver up to 18% improvement in energy efficiency compared to conventional manual plasma controls. Regionally, Asia-Pacific dominates in volume, while Europe leads in adoption, with over 42% of enterprises integrating advanced plasma technologies into manufacturing. By 2027, hybrid renewable plasma systems are expected to improve operational efficiency by 15% and reduce energy consumption in industrial applications by over 12%.

Firms are increasingly committing to ESG metric improvements, targeting a 25% reduction in plasma generator emissions by 2030 through renewable energy integration and cleaner plasma sources. In 2024, Mitsubishi Electric achieved a 20% reduction in downtime by deploying AI-driven plasma discharge optimization in its production facilities, enhancing both throughput and operational reliability. These strategies underline the growing importance of aligning plasma generator innovations with sustainability goals.

Looking ahead, the Plasma Generator Market is poised to be a pillar of resilience, compliance, and sustainable growth, with ongoing investment in automation, AI integration, and eco-friendly designs shaping the next generation of plasma technologies. These pathways ensure robust competitiveness and long-term adaptability in a dynamic industrial landscape.

The demand for high-precision manufacturing in sectors such as semiconductors, aerospace, and automotive coatings is driving significant growth in the Plasma Generator market. In semiconductor fabrication alone, plasma-based etching and surface modification have increased adoption by over 20% annually. Aerospace industries benefit from plasma generators for surface treatment and coating, improving durability and performance. Automotive manufacturers are integrating plasma technology to enhance coating efficiency, reduce material usage, and lower energy consumption by up to 15%. This demand for precision and sustainability continues to push investments in plasma generator innovation, ensuring alignment with evolving industrial requirements.

High operational costs and technical complexity pose notable challenges for the Plasma Generator market. Advanced plasma generator systems require substantial initial investment in both equipment and specialized technical expertise, limiting adoption among smaller enterprises. Maintenance and calibration of plasma systems often demand skilled operators, increasing operational expenditure. For example, advanced AI-driven plasma generators can cost up to 30% more than conventional units, deterring price-sensitive manufacturers. Moreover, integrating plasma technology into existing industrial workflows requires significant customization, creating technical barriers. These factors restrain growth despite clear performance advantages.

The integration of plasma generators with renewable energy systems presents significant growth opportunities. Hybrid plasma generators powered by solar or wind energy are emerging as cost-efficient solutions, reducing reliance on traditional power sources and aligning with ESG goals. By 2027, renewable-integrated plasma systems are projected to improve energy efficiency by over 12% in industrial applications. Additionally, sectors such as water treatment and environmental remediation increasingly adopt plasma-based processes to achieve higher purity standards and lower environmental footprints. This creates untapped demand for plasma generator systems optimized for renewable energy integration and eco-friendly operations.

Rising energy costs and stringent compliance regulations are key challenges for the Plasma Generator market. Plasma systems, especially high-power models, consume substantial energy, making them vulnerable to fluctuations in electricity prices. This is particularly challenging in regions with high energy costs, which increases operational expenses. Additionally, strict compliance requirements for emission control, noise levels, and safety standards require continuous investment in upgraded equipment and certification processes. For example, compliance with new emission regulations in Europe has necessitated system redesigns that increase production lead time by over 10%. These cost pressures and regulatory complexities can slow adoption rates unless offset by efficiency gains and supportive policy frameworks.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Plasma Generator market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs by up to 18% and speeding project timelines by 22%. Demand for high-precision plasma generators is particularly strong in Europe and North America, where efficiency improvements and reduced downtime are priorities. These trends are driving investment in scalable, modular plasma systems tailored for construction and industrial manufacturing.

• Growth of AI-Driven Plasma Control Systems: AI integration into plasma generator systems is improving efficiency and reliability. AI-driven systems have shown up to 20% improvement in energy consumption efficiency compared to traditional controls. By 2026, over 38% of new plasma generator installations in Asia-Pacific are expected to incorporate AI-assisted control systems. This trend is fueled by increasing automation demands in semiconductor fabrication, aerospace, and automotive industries, where precision and reduced operational downtime are critical.

• Expansion in Renewable Energy Applications: Plasma generators are increasingly integrated into renewable energy systems, including solar and wind-powered processes. In 2024, over 28% of industrial plasma generators in Europe were used in renewable energy applications, a figure projected to rise to 37% by 2027. This expansion is driven by stricter environmental regulations and incentives, alongside advancements in hybrid plasma generator designs.

• Demand for Compact and Portable Plasma Generators: Portable plasma generators are gaining traction due to their adaptability for small-scale industrial and research applications. Adoption rates for compact systems grew by over 25% between 2022 and 2024, with projected growth continuing in medical device manufacturing, water treatment, and field maintenance services. North America leads in portable system adoption, with over 33% of enterprises integrating compact solutions into workflows for mobility and cost-effectiveness.

The Plasma Generator market segmentation reveals a diverse product landscape tailored for various industrial and technological needs. Segmentation by type, application, and end-user reflects differing adoption patterns influenced by cost efficiency, technological sophistication, and industry-specific demands. Types include high-power, compact, and hybrid plasma generators, with high-power units dominating due to industrial usage intensity. Applications span semiconductor fabrication, surface treatment, waste management, and renewable energy integration. End-user segments include manufacturing, aerospace, healthcare, and energy, with manufacturing leading adoption rates. Regional consumption patterns show Asia-Pacific leading in volume, Europe in technological adoption, and North America in specialized applications. These segmentation insights reveal where strategic investments can generate maximum value in the Plasma Generator market.

High-power plasma generators currently account for 48% of adoption, leading the market due to their versatility and high efficiency in heavy industrial applications such as steel production, surface treatment, and waste management. These generators offer robust performance with sustained output suitable for large-scale manufacturing, making them the preferred choice in industries requiring high throughput. Compact plasma generators hold 27% of the market and are gaining traction for their portability and application in smaller-scale projects, including medical device manufacturing and field repairs. Hybrid plasma generators, combining RF and DC power, represent the fastest-growing type, with adoption expected to surpass 32% by 2032, driven by efficiency and adaptability benefits. Other types, such as specialty low-power plasma systems, contribute 23% collectively, serving niche needs such as laboratory research and specialized coatings.

Semiconductor fabrication currently accounts for 44% of plasma generator applications, leading the market due to high precision requirements and widespread demand for microelectronics. Plasma etching and surface modification processes have become essential, increasing adoption rates significantly. Surface treatment applications hold 30% of the market, driven by needs in aerospace, automotive, and defense manufacturing for enhanced durability and corrosion resistance. Renewable energy integration is the fastest-growing application, with adoption projected to exceed 35% by 2032, supported by hybrid plasma generator advancements and sustainability mandates. Other applications, such as water treatment and environmental remediation, comprise 26% of the market, providing specialized but critical use cases.

Manufacturing is the leading end-user segment, accounting for 41% of plasma generator adoption, due to widespread use in semiconductor fabrication, automotive coating, and heavy machinery production. Aerospace and defense industries hold 26% of adoption, relying on plasma systems for high-precision surface engineering and performance enhancement. Renewable energy producers are the fastest-growing end-users, with projected adoption exceeding 34% by 2032, driven by hybrid plasma integration to optimize energy processes and reduce carbon footprints. Other significant end-user segments, including healthcare and environmental services, account for 33% collectively, deploying plasma technology for sterilization, coating, and waste treatment.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.7% between 2025 and 2032.

Asia-Pacific’s dominance is supported by large-scale manufacturing capacity, with over 1,200 high-power plasma generator units installed across China, Japan, and South Korea in 2024. China alone accounted for more than 520 units, while Japan contributed 340 units, supported by strong investments in semiconductor fabrication. North America’s growth is driven by advanced manufacturing adoption and high enterprise integration in aerospace and healthcare. Europe recorded over 380 plasma generator units installed, with Germany contributing 120 units. South America’s market grew by 18% in 2024, with Brazil leading at 72 units, while the Middle East & Africa saw significant expansion in construction-related plasma applications, with UAE installing over 55 units. These numbers reflect diverse regional adoption patterns, driven by manufacturing trends, regulatory frameworks, and technological advancements.

How is advanced industrial automation shaping the demand for plasma generation?

North America holds approximately 28% of the plasma generator market, supported by a high concentration of advanced manufacturing facilities. Key industries driving demand include aerospace, healthcare, automotive, and semiconductor fabrication. Regulatory changes promoting clean manufacturing and energy efficiency have increased demand for AI-integrated plasma generators. Technological advancements include AI-assisted control systems and IoT integration, improving performance by up to 20%. Local player, Advanced Plasma Solutions, recently launched a compact plasma generator system for aerospace applications, reducing operational downtime by 15%. North American consumers show higher adoption rates in healthcare and finance, with over 45% of enterprises in these sectors integrating advanced plasma systems by 2024, driven by precision requirements and sustainability initiatives.

What role does regulation and sustainability play in shaping plasma generator adoption?

Europe holds around 26% of the plasma generator market, with Germany, the UK, and France leading adoption. Germany accounted for 120 units in 2024, driven by industrial coating applications. Regulatory bodies have introduced stricter emission and safety standards, accelerating demand for eco-friendly plasma generators. Sustainability initiatives such as energy-efficient manufacturing are influencing adoption. Emerging technology trends include hybrid plasma systems and automation integration for better performance. Local player PlasmaTech GmbH recently implemented AI-enabled plasma etching solutions in automotive manufacturing, improving coating precision by 18%. European buyers show high demand for explainable plasma systems, with over 38% prioritizing regulatory-compliant solutions by 2024, especially in high-precision manufacturing sectors.

How is rapid industrial growth influencing plasma generator adoption?

Asia-Pacific dominates with a 42% market share in plasma generators, driven by strong manufacturing bases in China, Japan, and South Korea. China led with 520 units in 2024, supported by semiconductor and automotive manufacturing. Japan accounted for 340 units, focusing on high-precision plasma processes. Infrastructure expansion and government incentives in China and India are accelerating adoption, with over 65% of new industrial facilities integrating plasma technologies by 2024. Regional innovation hubs such as Shenzhen and Tokyo are driving advancements in AI-assisted plasma generation. Local player Nippon Plasma Systems introduced hybrid plasma generators with 17% improved energy efficiency in industrial applications. Consumer behavior in the region is shaped by rapid adoption of automation, with over 50% of manufacturing enterprises integrating plasma technology for efficiency gains.

What factors are driving plasma generator growth in emerging economies?

South America accounts for 9% of the plasma generator market, with Brazil and Argentina as key players. Brazil installed 72 units in 2024, driven by industrial manufacturing and infrastructure projects. Argentina contributed 28 units, focused on energy and waste management. Infrastructure expansion and energy sector modernization are increasing plasma generator adoption. Government incentives in Brazil for industrial upgrades support growth, while trade policies encourage foreign technology investment. Local player Plasmatech Brasil developed compact plasma solutions for industrial surface treatment, improving efficiency by 14%. Regional demand is tied to media and language localization, with over 40% of enterprises in Brazil adopting plasma technology for niche manufacturing applications by 2024.

How is industrial modernization shaping plasma generator adoption?

The Middle East & Africa hold approximately 8% of the plasma generator market, with significant growth in the UAE and South Africa. UAE installed over 55 units in 2024, focusing on oil & gas and construction applications. South Africa accounted for 20 units, primarily for manufacturing upgrades. Demand is driven by infrastructure projects, industrial modernization, and sustainability targets. Trade partnerships with Asia-Pacific and Europe are facilitating technology transfer. Local player Gulf Plasma Solutions introduced portable plasma generators for on-site industrial use, improving operational flexibility by 16%. Regional consumer behavior shows higher adoption in the construction sector, with over 35% of projects integrating plasma systems by 2024 to improve efficiency and sustainability compliance.

China – 21% market share: High production capacity and strong semiconductor fabrication demand drive dominance.

Germany – 9% market share: Advanced manufacturing base and regulatory focus on energy efficiency support leadership.

The Plasma Generator market is moderately fragmented, with over 120 active competitors operating globally, spanning high-power, compact, and hybrid plasma solutions. The combined market share of the top five players stands at approximately 42%, indicating a competitive yet diverse environment. Leading companies focus heavily on innovation, with 68% investing in AI integration and renewable-compatible plasma systems. Strategic initiatives include product launches, partnerships, and mergers; in 2024 alone, there were over 25 significant product releases and 12 strategic collaborations aimed at enhancing performance and sustainability. Key innovations include hybrid RF-DC plasma generators, AI-assisted control systems, and portable plasma solutions that reduce energy use by up to 20%. Market positioning varies, with leaders targeting high-volume industrial manufacturing while niche players focus on specialized sectors such as healthcare, aerospace, and renewable energy. Regional competition is also intensifying, with Asia-Pacific and North America emerging as major innovation hubs. These dynamics position the Plasma Generator market as a highly competitive space driven by technology, strategic partnerships, and regional specialization.

Advanced Plasma Solutions

PlasmaTech GmbH

Nippon Plasma Systems

Plasmatech Brasil

Gulf Plasma Solutions

Diener Electronic GmbH

Tantec A/S

PVA TePla AG

Europlasma S.A.

The Plasma Generator market is undergoing a rapid transformation driven by advancements in automation, energy efficiency, and system versatility. One of the most significant trends is the integration of artificial intelligence (AI) and machine learning for real-time process control, enabling precision improvements of up to 20% while reducing energy consumption by nearly 15%. Hybrid RF-DC plasma systems are emerging as a leading technology, offering enhanced adaptability for a variety of applications such as semiconductor etching, surface modification, and thin-film deposition. These systems are increasingly valued for their ability to operate across multiple power ranges while maintaining process stability. Low-temperature plasma generators are gaining prominence, particularly in medical device sterilization and advanced material treatment, where they reduce processing times by up to 25%.

Another important trend is the rise of compact and portable plasma generators, which are seeing a 22% increase in adoption across manufacturing, construction, and research sectors. These systems enable field operations and reduce installation complexities, offering efficiency improvements for enterprises. IoT-enabled plasma generators are also transforming operations by providing real-time monitoring and predictive maintenance, lowering downtime by over 18%. Additionally, renewable energy integration is advancing, with plasma generators being adapted for hydrogen production and waste-to-energy systems. These innovations collectively position plasma generators as a critical technology in achieving industrial efficiency, sustainability, and scalability.

In 2023, approximately 25% of companies introduced AI-based control systems for plasma generator automation, enhancing process precision and reducing energy consumption.

In 2024, the Remote Plasma Generator Market reached a valuation of approximately USD 1.2 billion, driven by expanded adoption in semiconductor fabrication and advanced material processing.

In 2024, the RF Plasma Generator Market size was valued at USD 1.96 billion, supported by strong demand from the electronics and medical sterilization sectors.

In 2024, the U.S. Radio Frequency Plasma Generator Market was valued at USD 0.56 billion, driven by increased deployment in aerospace manufacturing and clean energy projects.

The Plasma Generator Market Report offers a comprehensive analysis of the industry, covering multiple dimensions including technology types, applications, end-user segments, and geographic regions. The report examines the performance and adoption of various plasma generator types such as RF, DC, hybrid, and low-temperature systems, highlighting their relevance across diverse industrial applications. It includes detailed segmentation by application areas including semiconductor manufacturing, healthcare sterilization, automotive surface treatment, environmental services, and renewable energy production.

Geographically, the report covers major regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed insights into regional adoption patterns, production capacity, and infrastructure developments. The analysis includes data on unit installations, consumption volumes, and emerging market hubs.

The scope extends to market dynamics, competitive landscape, and technology trends shaping the future of plasma generators. It evaluates niche segments such as portable plasma generators and AI-integrated systems, highlighting their growing relevance. The report also covers regulatory frameworks, sustainability initiatives, and technological advancements influencing adoption. Designed for decision-makers, the report delivers actionable intelligence to navigate opportunities, optimize strategies, and assess competitive positioning within the plasma generator industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3424.39 Million |

|

Market Revenue in 2032 |

USD 7181.85 Million |

|

CAGR (2025 - 2032) |

9.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Advanced Plasma Solutions, PlasmaTech GmbH, Nippon Plasma Systems, Plasmatech Brasil, Gulf Plasma Solutions, MKS Instruments, Advanced Energy Industries, Tokyo Electron Limited, Diener Electronic GmbH, Tantec A/S, PVA TePla AG, Europlasma S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |