Reports

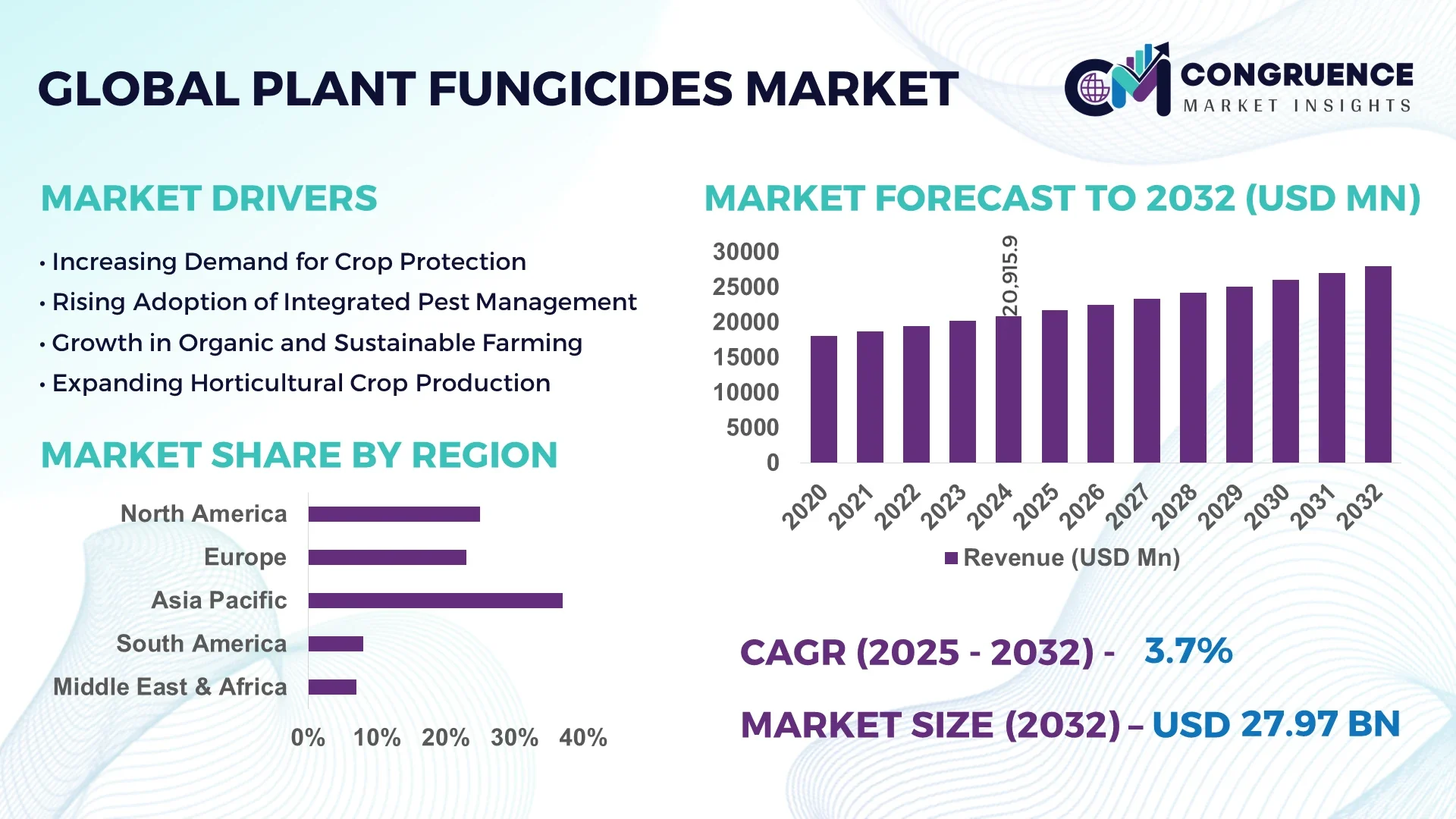

The Global Plant Fungicides Market was valued at USD 20915.92 Million in 2024 and is anticipated to reach a value of USD 27970.94 Million by 2032 expanding at a CAGR of 3.7% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The United States plays a crucial role in this market, with substantial production capacity supported by advanced agrochemical research facilities and robust investment in sustainable fungicide formulations. The country's agriculture sector extensively applies plant fungicides to protect high-value crops such as corn, soybeans, and wheat, leveraging technological innovations such as precision application systems and biofungicide developments.

The Plant Fungicides Market spans several key industry sectors including cereal crops, fruits & vegetables, and ornamentals, each contributing significantly to the market's expansion. Innovations such as nanoparticle-based fungicides and environment-friendly biofungicides are reshaping product portfolios, enhancing efficacy while minimizing ecological impact. Regulatory frameworks emphasizing residue limits and sustainable practices are driving manufacturers to innovate safer, more efficient products. Regional consumption patterns highlight increased demand in Asia-Pacific due to expanding agricultural activities and growing awareness of crop protection. Emerging trends include integrated disease management systems and climate-resilient fungicide solutions, positioning the market for steady growth driven by evolving agronomic needs and environmental stewardship.

Artificial intelligence is increasingly revolutionizing the Plant Fungicides Market by enhancing product development, precision agriculture, and operational efficiencies. AI-powered predictive analytics enable agronomists and manufacturers to anticipate fungal outbreaks with greater accuracy, allowing timely and targeted fungicide applications that reduce waste and increase crop protection efficiency. Machine learning algorithms analyze vast datasets from weather patterns, soil conditions, and plant health metrics, optimizing fungicide dosing schedules and formulations to maximize effectiveness and minimize environmental impact.

In manufacturing, AI-driven automation streamlines the production of plant fungicides, improving quality control and reducing production downtime through real-time monitoring and predictive maintenance. This boosts operational performance, lowers costs, and enhances product consistency. Additionally, AI integration in supply chain management improves inventory forecasting and distribution efficiency, ensuring fungicides reach high-demand regions promptly. Digital platforms powered by AI also facilitate farmer education and decision support, increasing adoption rates of advanced fungicide solutions. These AI advancements collectively drive innovation, sustainability, and profitability in the Plant Fungicides Market, positioning stakeholders for improved competitiveness in a rapidly evolving agricultural landscape.

“In 2024, a leading agrochemical company implemented an AI-based fungal disease prediction system across over 500,000 hectares, resulting in a 25% reduction in fungicide usage and a 15% increase in crop yield, demonstrating AI's tangible impact on the Plant Fungicides Market.”

The escalating global population continues to increase food demand, intensifying the need for effective crop protection solutions such as plant fungicides. This demand drives agricultural producers to adopt advanced fungicides to safeguard yields against fungal infections that threaten staple crops like wheat, rice, and maize. Additionally, expanding cultivation of high-value fruits and vegetables heightens reliance on plant fungicides to maintain quality and reduce post-harvest losses. Technological progress in fungicide formulation enhances disease control efficiency, encouraging wider adoption. Investment in precision agriculture further supports optimal fungicide use, reducing crop losses and improving food security worldwide, thus fueling growth within the Plant Fungicides Market.

The Plant Fungicides Market faces significant constraints due to increasingly strict regulatory policies governing chemical residues in food and environmental safety. Governments worldwide are imposing tighter residue limits and approving fewer synthetic fungicides, which restricts the availability of certain products. Compliance with complex registration procedures and lengthy approval timelines increases costs and delays product launches. Furthermore, public and consumer pressure for eco-friendly and residue-free produce limits fungicide options, necessitating reformulation and innovation. These regulatory challenges compel manufacturers to invest heavily in research and sustainable solutions, potentially slowing market growth and limiting product diversity in the Plant Fungicides Market.

The rising demand for environmentally friendly agricultural inputs creates significant opportunities in the Plant Fungicides Market, particularly in biofungicide development. Biological fungicides derived from natural microorganisms and plant extracts offer safer alternatives with minimal ecological impact, aligning with organic farming and sustainability goals. Increasing consumer preference for residue-free produce encourages growers to integrate biofungicides into crop protection programs. Additionally, advances in microbial fermentation and biotechnology facilitate scalable production of effective biofungicides, enhancing market availability. Emerging markets in Asia-Pacific and Latin America also present growth potential due to expanding organic agriculture and supportive government initiatives promoting sustainable farming practices.

Developing new and effective plant fungicides involves substantial costs and technical complexity, posing challenges to market players. The process of discovering, testing, and registering fungicides requires extensive field trials, toxicological studies, and compliance with stringent safety regulations, demanding significant financial and time investments. Additionally, the complexity of fungal pathogens, including resistance development, necessitates continuous innovation to maintain efficacy. Application challenges such as ensuring uniform coverage, avoiding runoff, and minimizing environmental impact require sophisticated delivery technologies and training for end-users. These factors increase operational costs and slow product introduction, impacting competitiveness and growth within the Plant Fungicides Market.

• Increasing Adoption of Biofungicides in Commercial Agriculture: The Plant Fungicides market is witnessing a marked increase in the use of biofungicides as farmers seek sustainable crop protection solutions. In 2024, biofungicide applications grew by over 18% in key agricultural regions such as Europe and Asia-Pacific, driven by regulatory restrictions on synthetic chemicals and rising consumer demand for residue-free produce. This shift has prompted manufacturers to invest in microbial and plant-extract-based formulations, enhancing product diversity and efficacy in controlling fungal diseases without harming beneficial soil organisms.

• Integration of Precision Agriculture Technologies: Precision agriculture tools, including drone-assisted spraying and sensor-based disease monitoring, are transforming fungicide application within the Plant Fungicides market. These technologies improve targeting accuracy and reduce chemical usage by up to 30%, optimizing input costs while maximizing disease control. The growing use of AI-powered predictive models further supports timely fungicide deployment, minimizing crop losses in large-scale farms, particularly in North America and Europe.

• Development of Nano-Enabled Fungicides: Nanotechnology is becoming increasingly prominent in the Plant Fungicides market, with nano-formulations offering improved solubility, controlled release, and enhanced penetration into plant tissues. In 2024, several manufacturers launched nano-enabled fungicide products that demonstrated a 20-25% increase in disease suppression efficiency compared to conventional formulations, driving adoption in both cereal and horticultural sectors.

• Emphasis on Climate-Resilient Fungicide Solutions: The Plant Fungicides market is adapting to shifting climate patterns by developing fungicides effective under diverse environmental stressors. Products engineered to maintain efficacy amid rising temperatures and humidity fluctuations are gaining traction, especially in tropical and subtropical regions. This trend supports farmers’ efforts to mitigate yield losses caused by climate-related fungal outbreaks and strengthens the market’s resilience to global environmental changes.

The Plant Fungicides Market is segmented into types, applications, and end-users, providing a comprehensive framework for understanding market dynamics. Product types range from synthetic fungicides to biofungicides and nano-formulations, each catering to specific agricultural needs. Application segments cover diverse crop categories such as cereals, fruits & vegetables, and ornamentals, reflecting varied disease control requirements across farming practices. End-user analysis highlights commercial agriculture, organic farming, and greenhouse operations, illustrating the broad spectrum of fungicide utilization. This segmentation helps industry professionals and decision-makers tailor strategies according to evolving crop protection demands and technological advancements, optimizing market penetration and innovation efforts.

Synthetic fungicides remain the dominant product type in the Plant Fungicides Market, favored for their broad-spectrum efficacy and well-established use in large-scale crop protection. Their reliable performance against common fungal pathogens in cereal and vegetable crops sustains their market leadership. Meanwhile, biofungicides are the fastest-growing segment, propelled by increasing environmental regulations and consumer demand for organic produce. These biological products offer targeted action with minimal ecological impact, making them increasingly popular among sustainable farming practices. Nano-formulations, though still niche, are gaining traction due to their enhanced delivery and controlled-release properties, improving efficacy while reducing chemical load. Other types, such as copper-based fungicides and systemic fungicides, serve specialized crop applications and maintain relevance in integrated pest management systems.

Cereal crops constitute the leading application segment in the Plant Fungicides Market, driven by the high prevalence of fungal diseases affecting staple grains such as wheat, rice, and maize. The need to protect yields and maintain food security underscores this segment’s importance. Fruits and vegetables represent the fastest-growing application area, fueled by rising consumer demand for quality produce and increased adoption of advanced fungicide solutions to combat fungal infections in perishable crops. Ornamentals and turfgrass applications also contribute to the market, with specialized fungicide formulations addressing aesthetic and commercial landscaping requirements. Additionally, pulses and oilseed crops form niche application segments supported by targeted disease management practices.

Commercial agriculture is the leading end-user segment for plant fungicides, reflecting the extensive use of fungicides in large-scale crop production systems aimed at maximizing yield and quality. The growth of precision farming techniques and mechanized application methods further reinforces this segment’s dominance. Organic farming stands out as the fastest-growing end-user segment, driven by increasing consumer preference for organic food and stricter residue regulations, boosting demand for biofungicides and natural disease control solutions. Greenhouse and protected cultivation also form significant end-user categories, relying on tailored fungicide applications to maintain disease-free environments in controlled conditions. Smallholder farms contribute regionally, especially in developing countries, through the adoption of accessible and cost-effective fungicide options.

Asia-Pacific accounted for the largest market share at 37% in 2024; however, Latin America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The Asia-Pacific region leads due to its extensive agricultural activities, high fungicide consumption for crops such as rice and wheat, and rapid adoption of innovative plant protection technologies. Latin America’s growth is fueled by expanding arable land, increasing investment in crop protection, and supportive government policies aimed at boosting agricultural exports. Other regions, including North America and Europe, maintain stable demand driven by regulatory frameworks and technological advancements in fungicide formulations.

Innovative Crop Protection Meets Regulatory Advancements

North America holds approximately 25% of the global Plant Fungicides Market volume, with strong demand from commercial grain, fruit, and vegetable production sectors. The region benefits from stringent regulatory oversight by agencies promoting safe chemical use and sustainable farming. Technological advancements such as drone-assisted fungicide application and AI-driven disease prediction models are transforming operational efficiency. Government incentives supporting precision agriculture and reduced environmental impact have further boosted adoption rates. Digital transformation in supply chain management and real-time crop monitoring contribute to North America’s prominent position in the Plant Fungicides Market.

Balancing Sustainability and Technological Innovation

Europe accounts for nearly 20% of the Plant Fungicides Market volume, with Germany, France, and the UK as leading contributors. Regulatory bodies emphasize stringent sustainability mandates, driving a shift toward biofungicides and reduced chemical residues. Initiatives such as the European Green Deal encourage eco-friendly plant protection practices. Europe is at the forefront of integrating smart agriculture technologies, including sensor-based disease detection and automated spraying systems. These advances support improved crop yields while aligning with regional environmental goals, reinforcing Europe’s strategic role in the evolving Plant Fungicides Market landscape.

Agricultural Expansion and Technology Adoption Fuel Demand

Asia-Pacific commands the largest Plant Fungicides Market volume globally, with China, India, and Japan leading consumption. The region’s expanding agricultural infrastructure and modernization of farming practices have significantly increased fungicide demand. Local manufacturers are investing in product innovation tailored to regional crop types and climatic conditions. Technology hubs in countries like China foster the development of advanced formulations, including nano-enabled fungicides and biological products. Growing government focus on food security and export-driven agriculture underpins the robust market size, positioning Asia-Pacific as the most critical player in the Plant Fungicides Market.

Strategic Agricultural Growth Supported by Policy Incentives

South America accounts for around 10% of the Plant Fungicides Market, with Brazil and Argentina as key contributors. Both countries possess vast arable land and export-oriented agriculture, driving consistent fungicide usage. Infrastructure development, particularly in logistics and storage, enhances market efficiency. Government incentives aimed at sustainable agriculture and favorable trade policies promote the adoption of innovative fungicide solutions. Energy sector investments and modernization in rural areas support enhanced distribution networks, further expanding market reach. These factors collectively position South America as a promising region within the Plant Fungicides Market.

Emerging Demand Amidst Technological and Regulatory Shifts

The Middle East & Africa represent about 8% of the Plant Fungicides Market volume, with the UAE and South Africa as major growth centers. Demand growth aligns with expanding agriculture and construction sectors requiring effective crop protection. Technological modernization, including the introduction of precision spraying and remote monitoring, is gaining momentum. Local regulations are evolving to support sustainable farming and reduce chemical overuse. Trade partnerships and regional cooperation facilitate fungicide availability and innovation adoption. These dynamics contribute to a gradually increasing footprint for the Plant Fungicides Market in this region.

China: 18% market share due to its vast agricultural production capacity and rapid adoption of advanced fungicide technologies.

United States: 15% market share supported by strong end-user demand in large-scale commercial farming and proactive regulatory frameworks promoting safe fungicide use.

The Plant Fungicides market is characterized by a highly competitive environment with over 50 active global and regional players vying for market share. Leading companies are strategically focusing on innovation, expanding their product portfolios, and enhancing sustainability through biofungicide development. Partnerships and collaborations between agrochemical firms and biotechnology companies are increasing, driving advances in precision agriculture technologies. Recent product launches emphasize eco-friendly formulations and digital integration to improve application efficiency and crop protection outcomes. Mergers and acquisitions are also shaping the landscape, enabling firms to consolidate R&D capabilities and expand geographic reach. Innovation trends such as nano-formulations and AI-powered disease detection systems are critical factors influencing competition. Companies prioritize regulatory compliance and responsiveness to evolving environmental standards, further intensifying rivalry as they seek to align with global sustainability goals. Overall, the Plant Fungicides market’s competition landscape is dynamic, marked by strategic investments and continuous technological evolution aimed at meeting diverse agricultural demands worldwide.

BASF SE

Syngenta AG

Bayer AG

FMC Corporation

Corteva Agriscience

UPL Limited

ADAMA Agricultural Solutions Ltd.

Sumitomo Chemical Co., Ltd.

Nufarm Limited

Ishihara Sangyo Kaisha, Ltd.

The Plant Fungicides market is experiencing significant transformation driven by advances in technology that enhance efficacy, sustainability, and application precision. Innovations such as nano-formulations are enabling more effective delivery of active ingredients, improving absorption rates, and reducing chemical usage. Precision agriculture technologies, including drone-based spraying systems and AI-driven disease detection platforms, are increasingly integrated into fungicide application processes. These advancements allow for targeted treatment, minimizing environmental impact and optimizing crop health monitoring. Additionally, biotechnology plays a pivotal role, with the development of biofungicides derived from natural microbial agents gaining traction as eco-friendly alternatives to synthetic chemicals. Digital farming solutions powered by big data analytics facilitate real-time decision-making and supply chain optimization. Automation in manufacturing processes improves production consistency and scalability. Furthermore, advancements in formulation technologies ensure longer residual effects and resistance management against evolving plant pathogens. Regulatory frameworks are driving innovation toward sustainable and less toxic fungicides, influencing R&D investments. Together, these technological insights highlight a future-forward Plant Fungicides market prioritizing efficiency, environmental stewardship, and technological integration.

In February 2024, Syngenta launched a novel biofungicide targeting powdery mildew in cereal crops, incorporating natural microbial strains that improve crop resistance while reducing synthetic chemical dependency by 35%.

In October 2023, BASF expanded its fungicide portfolio with the introduction of a multi-site action product that enhances resistance management, now adopted in over 15 countries with regulatory approval.

In August 2023, Corteva Agriscience implemented drone-assisted fungicide application trials across India, demonstrating a 20% increase in application precision and a 15% reduction in chemical waste.

In May 2024, FMC Corporation announced a strategic partnership with a leading AI technology firm to develop predictive models for early fungal disease outbreak detection, improving preventive fungicide application timing.

The Plant Fungicides Market Report provides a comprehensive analysis covering multiple dimensions critical for informed business decision-making. The report encompasses detailed segmentation by product types, including synthetic fungicides, biofungicides, and nano-formulations, addressing their unique applications across various crop categories such as cereals, fruits, vegetables, and ornamental plants. It evaluates end-user segments, ranging from commercial agriculture enterprises to organic farming operations, highlighting differing demand patterns and usage behaviors.

Geographically, the report spans key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional consumption volumes, infrastructure developments, and regulatory environments. Technological advancements are examined extensively, focusing on innovations like precision spraying systems, drone-assisted applications, and AI-enabled disease forecasting tools that are shaping the market landscape.

The report also delves into emerging niches such as environmentally sustainable biofungicides and integrated pest management solutions, emphasizing growing trends in eco-friendly agricultural practices. Industry focus areas include analysis of supply chain dynamics, manufacturing capabilities, and investment trends, alongside policy impacts influencing market trajectories. Collectively, this broad yet detailed scope equips stakeholders with a strategic understanding of market drivers, challenges, opportunities, and competitive positioning in the evolving Plant Fungicides industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 20915.92 Million |

|

Market Revenue in 2032 |

USD 27970.94 Million |

|

CAGR (2025 - 2032) |

3.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Syngenta AG, Bayer AG, FMC Corporation, Corteva Agriscience, UPL Limited, ADAMA Agricultural Solutions Ltd., Sumitomo Chemical Co., Ltd., Nufarm Limited, Ishihara Sangyo Kaisha, Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |