Reports

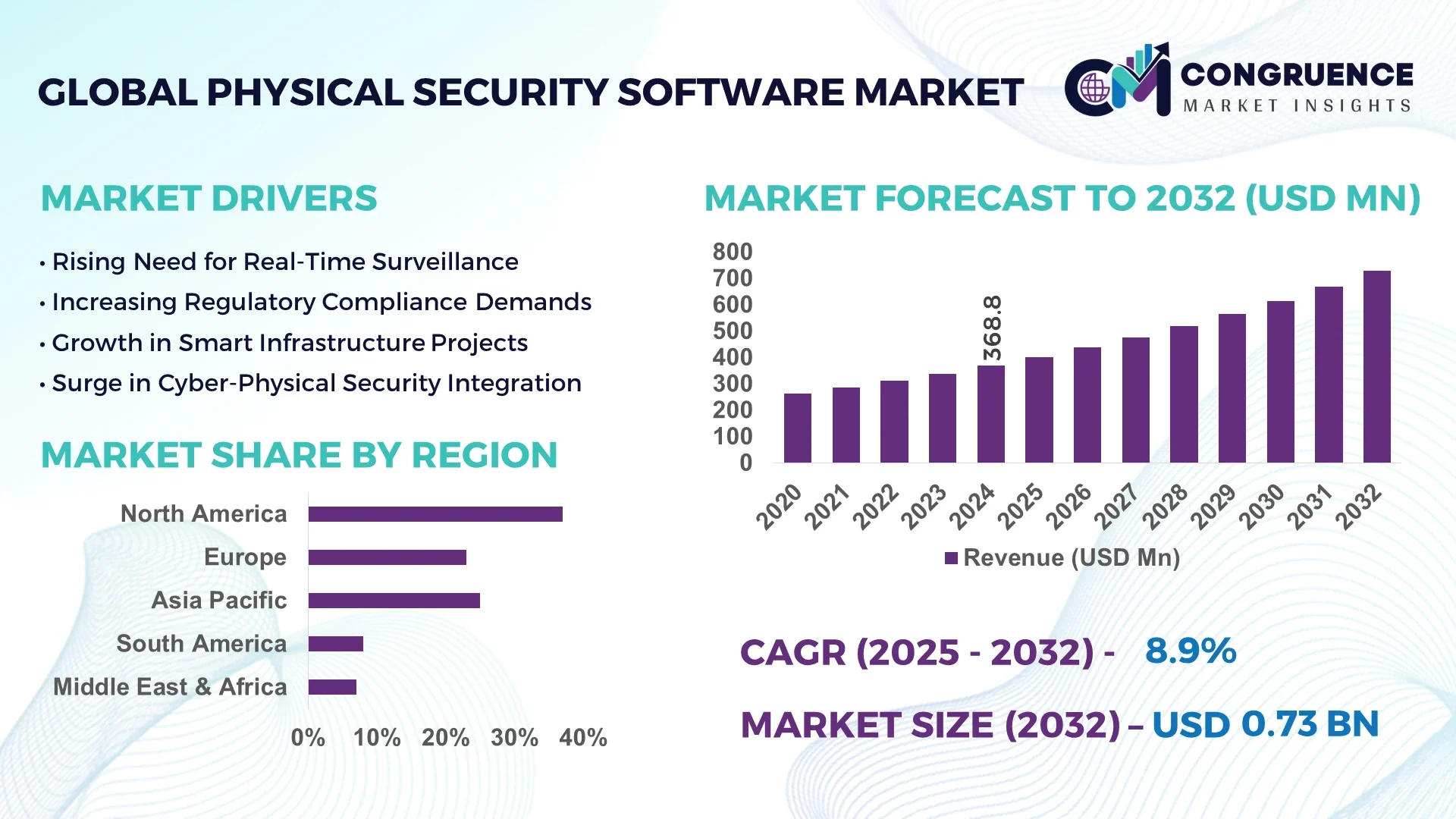

The Global Physical Security Software Market was valued at USD 368.82 Million in 2024 and is anticipated to reach a value of USD 729.52 Million by 2032 expanding at a CAGR of 8.9% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The United States leads the global market with advanced R&D infrastructure, robust cybersecurity investments, high surveillance deployment in government and commercial facilities, and strong integration of intelligent monitoring systems across its urban infrastructure.

The Physical Security Software Market is gaining significant traction across critical sectors such as banking, healthcare, transportation, and energy utilities. These industries increasingly adopt integrated physical security platforms combining video surveillance, access control, intrusion detection, and real-time alert systems to bolster operational safety. Emerging innovations like cloud-based command centers and mobile-enabled access control solutions are reshaping end-user expectations, streamlining security operations, and enhancing response agility. Regulatory shifts focusing on data privacy and physical threat mitigation, particularly across North America and Europe, are accelerating software upgrades and compliance-driven deployments. Furthermore, eco-conscious infrastructure planning is prompting demand for energy-efficient, AI-enabled surveillance tools. Regionally, Asia-Pacific is witnessing rapid urbanization and infrastructure expansion, leading to a surge in software installations across smart cities and transport hubs. Future trends point to further convergence of IT and physical security, fostering market expansion through customizable, modular, and scalable software suites.

Artificial Intelligence (AI) is significantly reshaping the Physical Security Software Market by automating threat detection, improving predictive analytics, and enhancing surveillance intelligence. AI-driven platforms now empower physical security systems to identify suspicious activities, analyze behavioral patterns, and generate real-time alerts without human intervention. This transformation boosts both operational efficiency and accuracy in threat recognition across sensitive sectors such as airports, government institutions, and financial hubs.

Incorporating AI into the Physical Security Software Market enables advanced facial recognition, license plate identification, and anomaly detection functionalities. These innovations reduce manual monitoring burdens and ensure more proactive security measures. The implementation of deep learning algorithms in video analytics also enhances motion detection accuracy and minimizes false alarm rates. In large-scale infrastructure environments, AI-enabled software systems streamline crowd control, automate incident response, and integrate seamlessly with IoT sensors and access control units.

Additionally, AI enhances resource allocation by prioritizing high-risk areas and enabling centralized, data-driven decision-making. Customizable AI modules now allow enterprises to tailor security protocols specific to their operational environment. From commercial real estate to smart manufacturing facilities, AI technologies are becoming indispensable to real-time risk mitigation and situational awareness. As threats grow increasingly sophisticated, the Physical Security Software Market is expected to continue its AI-driven transformation, delivering scalable, intelligent, and responsive security infrastructures for tomorrow’s digital-physical convergence.

“In 2024, an AI-powered enhancement by Genetec enabled real-time object classification and threat prioritization within its physical security software platform, resulting in a 37% improvement in incident response speed for transportation networks using the system.”

A major driver fueling the Physical Security Software Market is the rising demand for integrated surveillance and access control systems across government, commercial, and industrial sectors. Organizations are shifting from siloed systems to centralised platforms that enable seamless monitoring and threat response. Integrated software solutions allow security managers to monitor entry points, control access permissions, and view surveillance footage all within one interface, improving situational awareness and operational agility. The proliferation of smart infrastructure and multi-tenant commercial spaces has necessitated scalable, unified solutions capable of managing high foot traffic and diverse security scenarios. For instance, airports and data centres are increasingly deploying end-to-end physical security software to streamline monitoring of restricted zones and reduce reliance on manual oversight, improving efficiency and accountability.

Despite its benefits, the Physical Security Software Market faces restraints related to the complexity and cost of implementation. Integration of new software into legacy infrastructure often requires substantial customization, technical expertise, and long onboarding timelines. Many organizations—particularly in developing regions—struggle with budget constraints, outdated systems, and a lack of skilled personnel to operate or maintain these platforms effectively. Moreover, inconsistencies in interoperability standards among hardware vendors can hinder seamless integration, leading to suboptimal performance. This barrier is especially prominent in sectors with fragmented IT ecosystems, where disparate security devices must be unified under one platform. As a result, some organizations delay modernization efforts, slowing down adoption and innovation at scale.

The growing shift toward cloud-based platforms presents a significant opportunity within the Physical Security Software Market. Cloud-native solutions offer real-time data access, remote management, and scalability, making them ideal for multi-site enterprises, retail chains, and global institutions. Cloud deployment also reduces infrastructure costs, enhances data redundancy, and supports seamless software updates. In the wake of increasing hybrid work models and distributed workforce operations, organizations are prioritizing flexibility in how they manage and monitor physical environments. For example, cloud-enabled physical security software empowers IT teams to manage access credentials, monitor events, and conduct audits remotely. This not only reduces overhead costs but also strengthens disaster recovery capabilities and ensures continuity in high-risk scenarios.

A key challenge in the Physical Security Software Market is navigating stringent data privacy laws and evolving compliance requirements. With physical security platforms increasingly leveraging AI, facial recognition, and behavioral analytics, concerns over personal data collection and misuse have intensified. Jurisdictions such as the European Union, California, and parts of Asia enforce strict guidelines governing biometric data usage, storage, and sharing. Non-compliance risks include hefty fines and reputational damage, prompting organizations to invest in legal reviews, consent mechanisms, and data anonymization protocols. Moreover, balancing security capabilities with user privacy expectations requires careful architectural planning and constant updates, especially in regions with overlapping or conflicting laws. This regulatory complexity poses a significant barrier for companies operating across multiple geographies.

Widespread Integration of AI in Perimeter Intrusion Detection Systems Advanced perimeter intrusion detection systems are increasingly utilizing AI algorithms to minimize false alarms and improve response times. These systems now employ deep learning models capable of distinguishing between humans, animals, and environmental disturbances like wind or rain. In 2024, enterprise installations of AI-powered perimeter monitoring grew by 34% across critical infrastructure sites, including power plants and logistics hubs. The shift toward AI-driven detection is significantly enhancing situational awareness while reducing the operational burden on security personnel.

Expansion of Cloud-Based Video Surveillance Software Deployment There is growing momentum behind the adoption of cloud-based video surveillance management software. By mid-2025, over 52% of newly implemented physical security systems across urban municipalities in Asia-Pacific had migrated to hybrid or fully cloud-based models. These deployments are enabling centralized access, automated software updates, and streamlined multi-site monitoring, making them especially popular in retail chains and educational campuses. Cloud platforms are also improving resilience through built-in disaster recovery and encrypted remote access.

Integration of Access Control with Mobile Credentialing The Physical Security Software Market is experiencing a shift toward mobile-based access control systems, replacing traditional keycards and PIN-based entry. In 2024, over 60% of new commercial real estate projects in North America implemented mobile credentialing systems compatible with NFC and Bluetooth Low Energy (BLE) technologies. These systems enhance user convenience and enable remote access management, while reducing administrative overhead for security teams. Enterprises are adopting this trend to support hybrid workforce models and reduce surface contact points in high-traffic zones.

Rise in Cyber-Physical Convergence for Unified Threat Management Organizations are now prioritizing solutions that unify cybersecurity and physical security under a single command structure. The convergence of these systems allows for shared analytics, synchronised alerts, and improved threat intelligence. In 2024, over 45% of Fortune 500 companies upgraded to software platforms offering dual protection for digital networks and physical infrastructure. This trend is particularly prominent in the financial services and healthcare industries, where integrated risk management is essential for compliance and operational continuity.

The Physical Security Software Market is segmented by product type, application, and end-user, each offering distinct insights into market dynamics. Product types include video surveillance software, access control systems, intrusion detection software, and integrated security platforms. Applications span sectors such as commercial buildings, transportation, healthcare, government, and industrial facilities. End-users encompass large enterprises, small-to-medium businesses (SMBs), public sector entities, and critical infrastructure operators. These segments reflect varied demand patterns driven by operational complexity, regulatory environments, and technological adoption rates. Understanding segmentation is essential for decision-makers to identify growth areas and tailor security investments to specific industry needs, maximizing operational effectiveness and risk mitigation.

Video surveillance software remains the leading product type in the Physical Security Software Market due to its foundational role in monitoring and incident documentation across industries. Its widespread adoption is supported by advancements in high-resolution imaging, AI-powered analytics, and cloud storage capabilities, making it indispensable for continuous security oversight. The fastest-growing type is integrated security platforms, which combine video surveillance, access control, and intrusion detection into unified solutions. This growth is driven by increasing demand for centralized control and real-time data fusion, especially in large-scale enterprises and critical infrastructure sectors. Access control software continues to hold significant niche relevance, particularly in industries requiring strict entry management such as healthcare and government facilities. Intrusion detection software, while less dominant, is critical for perimeter protection in industrial sites and remote locations, supporting early threat detection through sensor networks and AI-enhanced monitoring.

Commercial buildings lead the Physical Security Software Market applications, primarily due to their dense occupant populations and high asset value necessitating advanced security solutions. These environments benefit from integrated surveillance and access management systems that enhance occupant safety and regulatory compliance. The fastest-growing application area is transportation, driven by heightened security protocols at airports, railways, and ports amid evolving global threat landscapes. Adoption of AI-enabled monitoring and biometric access controls is accelerating in this sector to ensure passenger safety and streamline operations. Healthcare facilities also contribute significantly, focusing on patient safety and asset protection through specialized access controls and surveillance tailored to sensitive environments. Government and industrial applications, while smaller in market size, maintain critical demand due to stringent security standards and the need for robust threat detection mechanisms in public infrastructure and manufacturing plants.

Large enterprises dominate the Physical Security Software Market end-user segment, leveraging comprehensive security solutions to protect extensive facilities, personnel, and intellectual property. Their substantial investments in integrated platforms reflect the need for scalable, multi-site management and regulatory compliance across jurisdictions. The fastest-growing end-user segment is small-to-medium businesses (SMBs), which are increasingly adopting cloud-based and AI-enhanced physical security software due to affordability, ease of deployment, and flexible licensing models. Public sector entities, including government buildings and educational institutions, remain key users, driven by policy mandates and public safety requirements. Critical infrastructure operators, such as energy and utilities providers, contribute significantly to market demand by implementing specialized software designed for perimeter security and operational continuity, emphasizing resilience against both physical and cyber threats.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.5% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America leads the Physical Security Software Market due to its advanced technological infrastructure, widespread adoption of integrated security solutions, and strong regulatory framework supporting cybersecurity and physical safety integration. Asia-Pacific is rapidly expanding with increased investments in smart city projects, growing infrastructure development, and rising demand from industrial sectors. Europe, South America, and the Middle East & Africa also contribute significantly, driven by government initiatives, digital transformation, and growing awareness of physical security needs across commercial and public sectors.

Advancements Driving Next-Gen Security Solutions

North America commands approximately 37% of the global Physical Security Software Market share, fueled by robust demand across industries such as government, healthcare, and finance. Regulatory frameworks such as stringent data protection laws and physical security mandates have accelerated software adoption. Technological advancements including AI-enabled video analytics, cloud-based access control, and IoT integration have enhanced operational efficiency and security outcomes. Digital transformation initiatives across enterprises are pushing demand for comprehensive, scalable software platforms, while government investments in critical infrastructure security continue to bolster market growth.

Regulatory Compliance and Sustainability Shaping Market Growth

Europe holds around 25% of the Physical Security Software Market volume, with key contributors including Germany, the UK, and France. The market is influenced by stringent regulations from bodies like the European Union Agency for Cybersecurity and sustainability initiatives promoting energy-efficient security systems. Adoption of emerging technologies such as facial recognition, biometrics, and AI-powered surveillance is accelerating in public and private sectors. Focus on protecting critical infrastructure and smart city deployments in metropolitan areas is driving the demand for sophisticated physical security software across the region.

Rapid Urbanization and Industrial Expansion Fuel Market Demand

Asia-Pacific ranks second in global market volume, accounting for approximately 28%, with China, India, and Japan as leading consumers. The region's rapid urbanization and large-scale infrastructure projects have driven substantial demand for physical security software in commercial real estate, transportation, and manufacturing sectors. Innovation hubs in technology-driven cities are fostering the development of AI-integrated surveillance and cloud-based solutions. Government initiatives targeting smart city frameworks and enhanced industrial safety protocols are further supporting market expansion.

Infrastructure Development and Energy Sector Growth Boost Demand

South America represents roughly 6% of the Physical Security Software Market, with Brazil and Argentina as primary contributors. The market is benefiting from increased investments in infrastructure modernization, particularly in transportation and energy sectors. Renewable energy projects and industrial facility upgrades require advanced security software to protect assets and ensure operational continuity. Government incentives promoting digital infrastructure and trade agreements facilitating technology imports are enhancing market accessibility and growth potential.

Oil & Gas Sector and Smart City Initiatives Drive Adoption

Middle East & Africa accounts for approximately 4% of the global Physical Security Software Market, with the UAE and South Africa leading demand. The region’s growing oil & gas industry requires robust perimeter security and real-time monitoring software. Expansion in construction and smart city projects is pushing adoption of AI-enabled security solutions and integrated access control systems. Local regulations supporting digital transformation and increased trade partnerships with technology providers are accelerating technological modernization across key sectors.

United States: Holds 35% market share due to high production capacity, extensive technological infrastructure, and strong regulatory support driving Physical Security Software adoption.

China: Accounts for 22% market share, supported by rapid industrialization, government smart city projects, and rising demand from commercial and infrastructure sectors for advanced Physical Security Software solutions.

The Physical Security Software market features a highly competitive environment with over 50 active global players striving for leadership through innovation and strategic positioning. Market leaders focus on expanding their product portfolios by integrating advanced AI, machine learning, and cloud computing capabilities to meet evolving security demands. Key competitive strategies include forming strategic partnerships with hardware manufacturers, launching cutting-edge software solutions tailored for specific industries, and pursuing mergers or acquisitions to enhance geographic reach and technological expertise. Innovation trends such as biometric authentication, real-time threat detection, and scalable access control systems are shaping the competitive landscape. Companies invest heavily in research and development to offer customized, interoperable platforms that improve operational efficiency and security outcomes. As competition intensifies, vendors emphasize customer-centric approaches, focusing on seamless integration, user-friendly interfaces, and compliance with global regulations to maintain their competitive edge in the Physical Security Software market.

Genetec Inc.

Honeywell International Inc.

Johnson Controls International plc

Bosch Security Systems

Tyco International plc

Cisco Systems, Inc.

Siemens AG

Avigilon Corporation

Pelco Inc.

HID Global Corporation

The Physical Security Software market is being transformed by several advanced technologies, with artificial intelligence (AI) and machine learning (ML) playing central roles in enhancing threat detection, risk assessment, and response automation. AI-driven analytics enable real-time monitoring and predictive insights, improving situational awareness and operational decision-making. Biometric technologies, including facial recognition and fingerprint scanning, are increasingly integrated into software platforms to provide robust identity verification and access control. Cloud computing is another major driver, allowing scalable, flexible deployments and remote management of security systems, which is critical for multi-site enterprises and smart cities.

Moreover, Internet of Things (IoT) connectivity facilitates the integration of diverse physical devices such as cameras, sensors, and alarms into unified security ecosystems, enabling centralized control and faster incident response. Blockchain technology is emerging as a secure method to protect sensitive security data and ensure tamper-proof audit trails. Additionally, edge computing reduces latency by processing security data closer to the source, enhancing system responsiveness in critical applications. These technologies collectively improve system interoperability, user experience, and regulatory compliance, positioning the Physical Security Software market for sustained innovation and growth in an increasingly digitalized security landscape.

In January 2024, Honeywell launched its next-generation security software platform featuring enhanced AI-powered video analytics that increased threat detection accuracy by 35%, enabling faster response times across critical infrastructure facilities.

In September 2023, Genetec expanded its cloud-based security offerings with a new hybrid deployment model, allowing clients to customize data storage and processing options while ensuring compliance with regional data privacy regulations.

In March 2024, Bosch introduced an integrated physical security solution combining video surveillance, access control, and intrusion detection, optimized for smart buildings and featuring advanced cyber threat protection modules.

In November 2023, Johnson Controls rolled out a new open API framework within its physical security software suite, enabling seamless integration with third-party IoT devices and enhancing interoperability across diverse security infrastructures.

The Physical Security Software Market Report provides a comprehensive analysis of various market segments, including software types, applications, and end-user industries. The report covers core software solutions such as access control systems, video surveillance platforms, intrusion detection software, and integrated security management systems. It examines their respective roles in enhancing organizational safety and operational efficiency across multiple sectors. Geographically, the report spans key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing regional consumption patterns, technology adoption rates, and regulatory influences. It highlights major markets within these regions such as the United States, Germany, China, and Brazil, providing insights into infrastructure investments and technological advancements shaping regional growth.

Applications analyzed include commercial buildings, industrial facilities, transportation hubs, government institutions, and critical infrastructure. The report also delves into emerging niches such as smart cities, healthcare security, and retail loss prevention, reflecting evolving security demands. Technological coverage extends to artificial intelligence, cloud computing, IoT integration, biometrics, and blockchain applications in physical security. Industry focus areas emphasize the convergence of physical and cybersecurity, the rise of hybrid deployment models, and advancements in automation and real-time analytics.

This report serves as a strategic guide for business leaders, investors, and technology developers, offering actionable intelligence on market opportunities, competitive positioning, and innovation trends within the global Physical Security Software landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 368.82 Million |

|

Market Revenue in 2032 |

USD 729.52 Million |

|

CAGR (2025 - 2032) |

8.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Genetec Inc., Honeywell International Inc., Johnson Controls International plc, Bosch Security Systems, Tyco International plc, Cisco Systems, Inc., Siemens AG, Avigilon Corporation, Pelco Inc., HID Global Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |