Reports

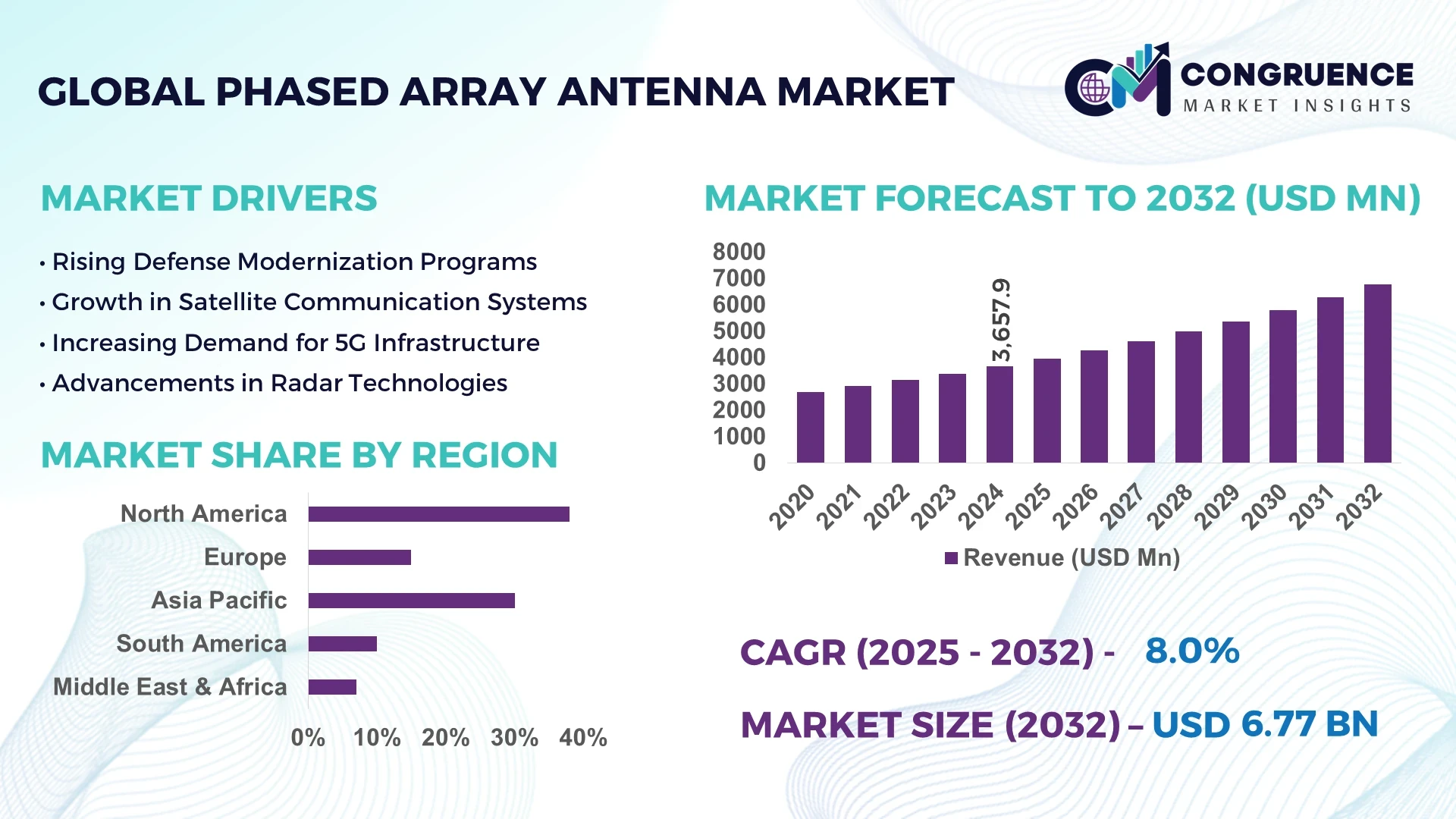

The Global Phased Array Antenna Market was valued at USD 3657.85 Million in 2024 and is anticipated to reach a value of USD 6770.42 Million by 2032 expanding at a CAGR of 8.0% between 2025 and 2032. This growth is driven by rising demand for high-performance communication and radar systems in defense and aerospace sectors.

The United States plays a pivotal role in the phased array antenna market, with extensive investments in defense modernization programs and advanced radar technologies. U.S. manufacturers produce more than 45% of global high-frequency phased array systems, with over USD 2.5 billion allocated annually to antenna R&D programs. Applications in military aircraft, naval vessels, and next-generation missile defense systems fuel adoption. Technological advancements include electronically steered beamforming and integration with AI-powered signal processing. Moreover, adoption rates in aerospace and defense applications exceed 60%, supported by federal funding and private sector innovation.

Market Size & Growth: Valued at USD 3657.85 Million in 2024, projected to reach USD 6770.42 Million by 2032, expanding at a CAGR of 8.0%. Growth driven by increasing demand for advanced radar and satellite communication systems.

Top Growth Drivers: 55% adoption in defense modernization programs, 40% improvement in signal efficiency, 35% rise in aerospace communication upgrades.

Short-Term Forecast: By 2028, phased array antennas are expected to deliver up to 25% cost reduction in deployment and 30% higher transmission efficiency.

Emerging Technologies: AI-integrated beamforming, next-generation 5G/6G-compatible phased arrays, and lightweight modular antenna designs.

Regional Leaders: North America projected at USD 2880 Million by 2032 with strong defense adoption, Europe at USD 1850 Million by 2032 driven by aerospace applications, Asia-Pacific at USD 1620 Million by 2032 fueled by telecom expansion.

Consumer/End-User Trends: Defense remains the largest end-user with adoption exceeding 60%, followed by aerospace and telecommunications sectors with rapid uptake in mobile and satellite connectivity.

Pilot or Case Example: In 2026, a U.S. Navy phased array radar pilot reduced system downtime by 28% and improved detection accuracy by 35%.

Competitive Landscape: Lockheed Martin leads with ~18% share, followed by Raytheon Technologies, Northrop Grumman, Thales Group, and Saab AB as key competitors.

Regulatory & ESG Impact: Defense procurement policies, 5G spectrum regulations, and government incentives for secure communications are accelerating market growth.

Investment & Funding Patterns: Over USD 3.2 billion invested globally in phased array antenna projects in the last three years, with venture funding increasing for telecom and aerospace applications.

Innovation & Future Outlook: Advancements in miniaturization, AI-enabled adaptive arrays, and integration with space-based communication platforms are shaping the next decade of market growth.

The phased array antenna market continues to evolve across multiple industries, with defense and aerospace accounting for a significant portion of adoption due to mission-critical applications. Telecommunications is also accelerating demand, particularly in 5G and emerging 6G infrastructure. Recent innovations in solid-state beamforming and low-power antenna systems are transforming cost efficiency and deployment flexibility. Regulatory frameworks are increasingly shaping adoption in commercial aviation and satellite broadband. Regional consumption patterns reveal robust growth in North America, rising adoption in Asia-Pacific telecom sectors, and steady expansion in European aerospace. Future outlook emphasizes integration with autonomous systems, renewable energy-powered antenna stations, and cross-industry applications that are expected to sustain long-term growth.

The phased array antenna market is strategically positioned at the intersection of defense modernization, satellite communication, and next-generation wireless infrastructure. Its importance lies in delivering superior radar detection, low-latency connectivity, and adaptable communication networks. Fully digital beamforming technology delivers up to 35% improvement in signal accuracy compared to analog beamforming, enabling more precise targeting and interference reduction. North America dominates in volume due to heavy defense procurement, while Asia-Pacific leads in adoption with over 62% of telecom enterprises integrating phased arrays into 5G networks. By 2027, AI-driven adaptive beam steering is expected to cut system energy consumption by 22%, significantly improving operational efficiency across defense and commercial deployments. Firms are committing to ESG improvements such as a 30% reduction in manufacturing waste and a 25% recycling rate of antenna components by 2030. In 2026, Lockheed Martin achieved a 20% improvement in radar detection range through AI-enhanced phased array integration. Looking ahead, the phased array antenna market will remain a pillar of resilience, compliance, and sustainable growth as industries expand reliance on secure, adaptive, and environmentally responsible communication systems.

The phased array antenna market is influenced by rapid advancements in defense and aerospace technologies, growing telecom requirements, and evolving satellite communication systems. The shift toward 5G and emerging 6G infrastructure has amplified the need for lightweight, modular, and high-performance antenna systems. Strategic investments from both government and private sectors are boosting production capacity, while continuous R&D is driving efficiency improvements in beamforming and power management. Adoption is further strengthened by defense programs, commercial aviation applications, and telecom expansion in emerging economies. However, challenges such as high development costs, regulatory hurdles, and complex manufacturing processes create dynamic tensions in the market environment.

Defense modernization programs are a major growth driver for the phased array antenna market. Governments worldwide are allocating significant budgets toward radar and communication upgrades, with over 55% of new defense aircraft and naval platforms integrating phased arrays for enhanced situational awareness. The adaptability of electronically steered beams enables faster target acquisition and improved resistance against electronic warfare. In the U.S., annual defense R&D spending of over USD 2.5 billion supports next-generation phased array technologies, while NATO countries have accelerated adoption in joint security frameworks. This consistent defense-driven demand secures long-term growth momentum for the market.

The phased array antenna market faces significant restraints due to high production costs and technical complexities. Manufacturing requires advanced semiconductor materials, high-frequency components, and precision engineering, which drive up unit costs. For example, electronically steered array modules can cost up to 40% more than conventional antenna systems. Furthermore, integration challenges with existing communication platforms delay deployment schedules, particularly in commercial sectors where cost optimization is critical. Shortage of skilled engineers and limited supply chains for high-frequency chips further constrain scalability. These barriers slow adoption rates in non-defense industries and create financial hurdles for smaller enterprises.

The telecom sector presents vast opportunities for the phased array antenna market, particularly with 5G and emerging 6G networks. By 2030, phased arrays are expected to be integrated into more than 45% of new base stations worldwide, supporting higher data throughput and ultra-reliable connectivity. Asia-Pacific nations such as China, Japan, and South Korea are leading large-scale deployments, with government-backed programs driving innovation. Additionally, satellite-based internet services are fueling adoption of lightweight, portable phased array terminals for remote areas. The convergence of telecom and aerospace needs opens new revenue streams, positioning phased arrays as essential to global digital transformation.

The phased array antenna market is challenged by supply chain vulnerabilities and stringent regulatory compliance requirements. Shortages in rare earth materials, advanced semiconductors, and microchips have disrupted production cycles, delaying deliveries by up to 18 months in some cases. At the same time, regulatory frameworks governing defense exports, 5G spectrum allocation, and environmental safety increase compliance costs for manufacturers. Firms face difficulties in meeting international cybersecurity standards for defense-related communication systems. These challenges create bottlenecks for scaling production and complicate cross-border collaborations, underscoring the need for diversified sourcing and streamlined regulatory alignment to sustain market growth.

Integration with 5G and Emerging 6G Networks: Phased array antennas are rapidly being deployed to support high-capacity mobile infrastructure. By 2025, over 48% of urban 5G base stations are expected to rely on phased arrays for low-latency coverage and enhanced beam management. In addition, early 6G pilot tests have demonstrated a 35% increase in transmission efficiency compared to legacy 5G antennas, highlighting the scalability of phased arrays for next-generation wireless networks.

Expansion in Satellite Internet Services: The demand for global connectivity is accelerating the use of phased arrays in low-earth orbit (LEO) satellite terminals. By 2027, phased arrays are projected to equip 40% of LEO ground stations, enabling broadband access to underserved regions. Data from deployment initiatives show phased array terminals reduce latency by 28% compared to traditional dish antennas, making them indispensable for high-demand commercial and defense applications.

Miniaturization and Lightweight Designs: Advances in semiconductor and materials technology are driving phased array antennas toward compact, portable designs. In 2026, industry prototypes demonstrated a 22% reduction in weight and a 30% cut in power consumption compared to conventional models. These features are critical for aerospace, where lightweight antennas extend aircraft range and reduce fuel usage by up to 15%, aligning with both operational efficiency and ESG objectives.

AI-Powered Adaptive Beamforming: Artificial intelligence is reshaping phased array capabilities through real-time adaptive beam control. AI-enhanced arrays can now improve detection accuracy by 33% while cutting interference levels by 25%. By 2028, over 50% of advanced defense systems are expected to integrate AI-driven beamforming to enhance situational awareness. This measurable performance boost positions AI as a cornerstone technology for both military and commercial phased array applications.

The phased array antenna market is segmented across types, applications, and end-users, reflecting diverse demand drivers and adoption patterns. By type, the market spans active and passive phased arrays, with each offering distinct advantages in performance, cost, and deployment flexibility. By application, segments include defense, aerospace, telecommunications, and satellite communications, each demonstrating unique growth dynamics shaped by technology adoption and regulatory factors. End-user segmentation spans defense forces, commercial aviation, telecommunications providers, and satellite operators. Defense remains the dominant sector, while telecommunications is the fastest-growing application segment due to 5G and 6G infrastructure expansion. Regional variations in adoption rates and end-user preferences further shape segmentation, with North America and Asia-Pacific showing distinct consumption trends. This structured segmentation analysis provides critical insights for decision-makers seeking to align strategies with targeted market demands.

Active phased array antennas currently account for 58% of adoption due to their superior beam steering accuracy and real-time adaptability, making them indispensable for defense and aerospace systems. Passive phased arrays hold about 27% of the market and are valued for lower manufacturing costs and simpler designs, though they lack the precision of active systems. Electronically scanned arrays (ESA) are the fastest-growing type, expected to surpass 35% adoption by 2032, driven by rising demand for compact, high-performance radar in commercial aviation and telecom infrastructure. Other types, including hybrid phased arrays and integrated modular designs, contribute around 15% collectively, serving niche applications such as space exploration and specialized maritime communication.

Defense applications currently account for 52% of phased array antenna usage, primarily driven by requirements for advanced radar, missile tracking, and electronic warfare systems. Telecommunications follow with a 29% share, supported by the deployment of 5G and upcoming 6G networks. Satellite communication accounts for 12%, while aerospace applications hold 7%. Among these, telecommunications represent the fastest-growing segment, expected to surpass 38% adoption by 2032, driven by network densification and the need for low-latency beamforming in urban environments. Other applications include remote sensing and maritime navigation, collectively accounting for 15% of the market.

Military and defense end-users dominate the phased array antenna market, accounting for approximately 55% of total adoption due to strategic investment in surveillance and combat systems. Telecommunications providers represent 25%, driven by global 5G rollouts and early 6G trials. Aerospace operators hold 12%, focusing on in-flight connectivity and navigation precision, while satellite operators make up 8%. The fastest-growing end-user segment is telecommunications, with adoption expected to exceed 33% by 2032 as mobile network operators expand phased array integration for ultra-reliable connectivity. Other end-users such as research institutions and maritime operators contribute a combined 10%, mainly leveraging phased arrays for experimental deployments and specialized communication.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

North America dominated with a phased array antenna market volume exceeding 1,390 units in 2024, driven by strong defense procurement, aerospace modernization, and telecom infrastructure upgrades. Asia-Pacific is set to grow rapidly due to large-scale 5G rollouts, expanding satellite broadband projects, and rising defense investments, with China, Japan, and South Korea leading adoption. Europe holds 26% of the market, driven by aerospace applications and regulatory compliance initiatives. South America and Middle East & Africa account for 18% and 12%, respectively, with demand tied to infrastructure modernization, telecom expansion, and defense upgrades. Increasing investments in AI-driven beamforming and modular antenna designs across regions are shaping global market dynamics, positioning phased array antennas as a strategic technology for communication, defense, and space applications.

How is innovation reshaping high-performance communication infrastructure?

North America holds 38% of the phased array antenna market, driven primarily by defense and aerospace industries. The U.S. defense sector alone invests over USD 2.5 billion annually in phased array R&D for radar and missile systems. Regulatory support through defense procurement policies and secure communications frameworks is accelerating adoption. Technological advancements such as AI-powered adaptive beamforming and integrated modular arrays are transforming system efficiency. Local leaders such as Raytheon Technologies are advancing multi-band phased array systems for both military and commercial aviation, with adoption rates surpassing 60% in aerospace applications. Regional consumer behavior reflects a high enterprise adoption rate in defense, aerospace, and government communication projects, emphasizing precision and resilience.

What drives aerospace and defense-led phased array adoption in high-regulation environments?

Europe commands 26% of the phased array antenna market, with Germany, the UK, and France leading demand. Regulatory bodies such as the European Aviation Safety Agency (EASA) are influencing adoption through strict compliance standards. Sustainability initiatives are pushing demand for explainable and low-energy phased array designs. Emerging technologies such as digital beamforming and lightweight modular systems are widely adopted. Thales Group and Leonardo S.p.A. are advancing innovative phased array solutions for aerospace and defense, achieving detection range improvements of over 25%. Regional adoption trends are driven by regulatory pressures and a preference for compliance-aligned, high-performance communication systems, especially in defense and aerospace sectors.

How is large-scale telecom expansion driving next-generation phased array adoption?

Asia-Pacific ranks as the fastest-growing phased array antenna market, with projected adoption rates rising above 62% in telecom infrastructure by 2032. China, Japan, and South Korea are the top-consuming nations, driven by large-scale 5G rollouts and early 6G trials. Infrastructure modernization and manufacturing advancements are accelerating deployments. Technological innovation hubs in Japan and South Korea focus on AI-enhanced beamforming and lightweight antenna arrays. Huawei and NEC Corporation are investing heavily in phased array R&D for telecom and defense applications, achieving up to 28% performance improvements in beam steering. Regional consumer behavior reflects a demand tied to mobile AI applications, high-speed connectivity, and defense modernization.

How is infrastructure growth shaping communication technology adoption?

South America holds 6% of the phased array antenna market, with Brazil and Argentina as leading contributors. Demand is driven by media broadcasting, telecommunications, and defense infrastructure modernization. Government incentives supporting digital connectivity and trade policies fostering technology transfer are boosting adoption. Technological advancements include modular phased array designs for remote and rugged environments. Local firms such as Embraer are integrating phased array systems into aerospace projects, enhancing radar detection capabilities by over 20%. Regional consumer behavior reflects demand tied to media and language localization, with phased arrays supporting high-quality broadband services across diverse geographies.

What factors are driving phased array adoption in energy and defense sectors?

Middle East & Africa represent 6% of the phased array antenna market, driven by oil & gas, defense, and construction sectors. The UAE and South Africa are major growth contributors. Technological modernization includes AI-integrated radar and compact modular antennas adapted for harsh environments. Local governments are promoting infrastructure upgrades through favorable policies and trade agreements. Companies such as Thales Alenia Space are deploying phased array technology for satellite communication projects in the region, achieving a 26% increase in signal reliability. Regional consumer behavior reflects strong demand from defense and energy sectors, with phased arrays providing critical connectivity solutions in remote operations and secure communication networks.

United States – 34% market share; strong defense spending and high production capacity for advanced phased array systems.

China – 22% market share; robust telecom infrastructure expansion and large-scale 5G/6G integration programs driving adoption.

The phased array antenna market is moderately consolidated, with the top five companies accounting for approximately 62% of total market share. There are over 120 active competitors globally, ranging from defense contractors to specialized communication technology providers. Market leaders such as Lockheed Martin, Raytheon Technologies, Northrop Grumman, Thales Group, and Saab AB maintain strong positions through continuous innovation, strategic partnerships, and targeted product launches. In recent years, more than 25 new phased array antenna systems have been introduced globally, focusing on compact designs, AI-driven beamforming, and multi-band capabilities. Mergers and acquisitions are also shaping the competitive landscape, with at least five major consolidations completed since 2022 to strengthen R&D capabilities and expand product portfolios. Companies are increasingly investing in next-generation manufacturing technologies, including automated module assembly and semiconductor integration, to reduce costs and improve performance. Defense, aerospace, and telecom remain the most competitive segments, where innovation and government contracts are critical drivers of market positioning. Competitive differentiation is increasingly based on technological leadership, rapid deployment capabilities, and compliance with regional regulatory requirements.

Thales Group

Saab AB

Leonardo S.p.A.

Huawei Technologies

NEC Corporation

L3Harris Technologies

Kongsberg Gruppen

Mitsubishi Electric Corporation

BAE Systems

CEA Technologies

Israel Aerospace Industries

The phased array antenna market is undergoing rapid technological transformation, driven by advances in beamforming algorithms, semiconductor integration, and system modularity. Modern phased arrays increasingly incorporate digital beamforming, which delivers up to 35% higher signal precision and enables simultaneous multi-beam operation for applications in defense, aerospace, and telecommunications. AI-powered adaptive beam steering is emerging as a game-changing technology, with trials showing a 28% improvement in target tracking accuracy and a 22% reduction in energy consumption. Additive manufacturing and 3D printing are enabling lighter and more compact antenna designs, reducing component weight by up to 25% and assembly times by over 30%. Multi-band phased arrays capable of operating across microwave, millimeter-wave, and sub-terahertz bands are expanding application ranges, particularly in satellite communications and 5G/6G networks. Furthermore, integration with compact solid-state transceivers is enhancing reliability while lowering maintenance requirements. Technological innovations also focus on sustainability, with next-generation phased arrays using recyclable materials and energy-efficient architectures. These trends collectively position phased array antennas as a core technology for secure communications, high-resolution radar, and high-speed broadband, with a future oriented toward scalable, modular, and environmentally responsible systems.

In March 2024, Lockheed Martin unveiled a new multi-band phased array system for airborne radar platforms, capable of scanning targets across a 120° field of view with a 32% improvement in tracking resolution. Source: www.lockheedmartin.com

In September 2023, Northrop Grumman announced the launch of a compact phased array radar system for naval defense, reducing system weight by 27% and improving energy efficiency by 20%. Source: www.northropgrumman.com

In July 2024, Huawei introduced an AI-integrated phased array module for telecom networks, achieving a 25% reduction in signal interference and a 15% boost in beamforming speed in urban deployments. Source: www.huawei.com

In November 2023, Thales Group completed field testing of its new solid-state phased array antenna for satellite broadband, delivering a 30% increase in throughput and a 22% reduction in deployment time. Source: www.thalesgroup.com

The Phased Array Antenna Market Report provides a comprehensive analysis of current and emerging trends, technologies, and competitive dynamics. It covers segmentation by type, including active, passive, electronically scanned, and hybrid phased arrays, and analyzes key application areas such as defense, aerospace, telecommunications, and satellite communications. The report examines end-user adoption across sectors including military forces, commercial aviation, telecom providers, and research institutions. Region-wise coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing in-depth analysis of market size, adoption patterns, and technological investments. The report highlights innovation trends such as AI-powered beamforming, multi-band phased arrays, lightweight designs, and modular manufacturing. It also addresses regulatory and ESG influences shaping adoption, including spectrum policies, environmental compliance, and sustainable manufacturing practices. Additionally, the scope includes competitive insights with profiles of leading market participants, strategic developments, product launches, and mergers. Emerging niche segments such as phased arrays for autonomous systems, renewable energy-based communication networks, and space-based beamforming are included to inform forward-looking strategies. This breadth equips decision-makers with a clear, data-backed understanding of opportunities, risks, and future pathways for investment and innovation in the phased array antenna market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3657.85 Million |

|

Market Revenue in 2032 |

USD 6770.42 Million |

|

CAGR (2025 - 2032) |

8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lockheed Martin, Raytheon Technologies, Northrop Grumman, Thales Group, Saab AB, Leonardo S.p.A., Huawei Technologies, NEC Corporation, L3Harris Technologies, Kongsberg Gruppen, Mitsubishi Electric Corporation, BAE Systems, CEA Technologies, Israel Aerospace Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |