Reports

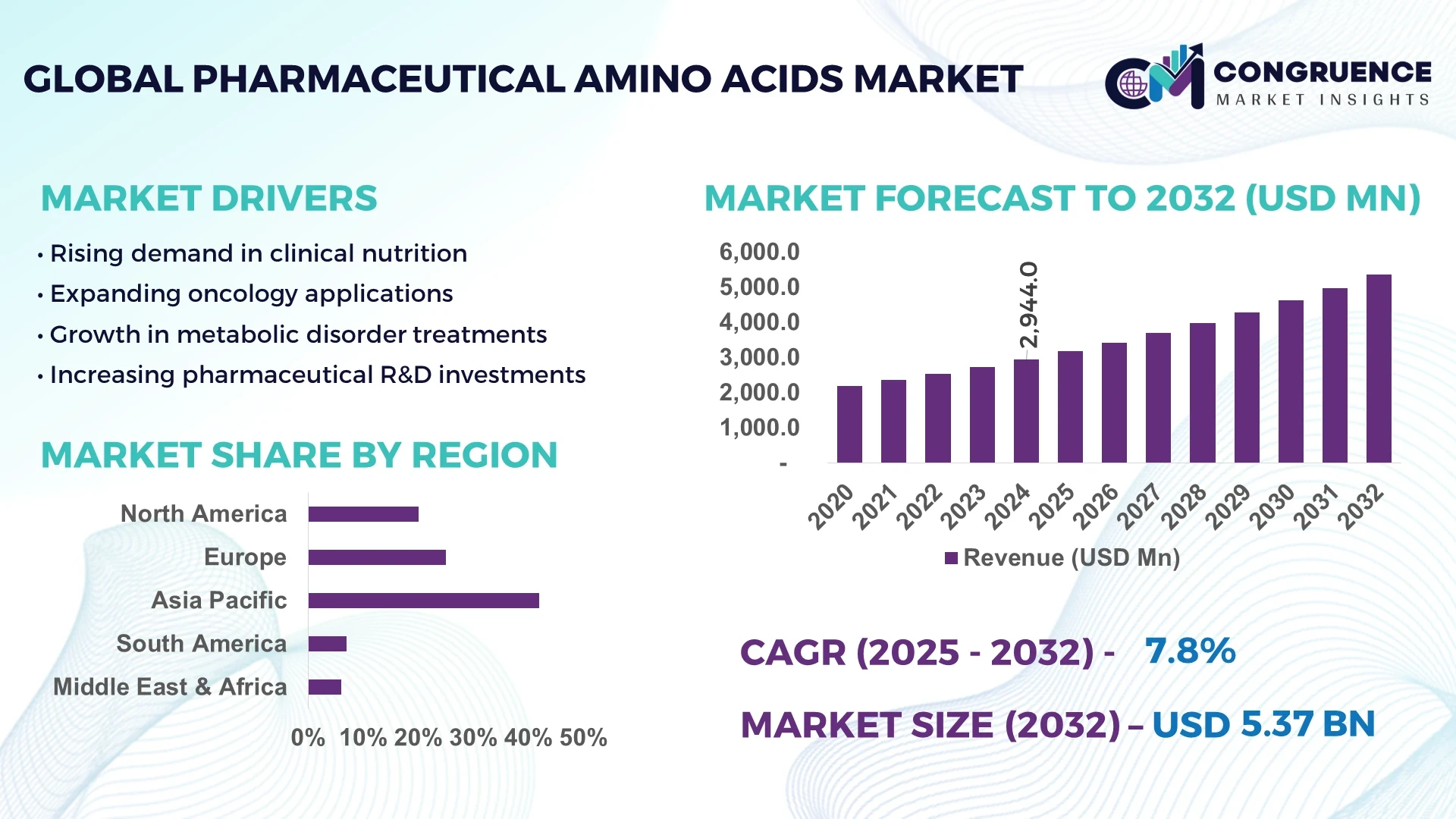

The Global Pharmaceutical Amino Acids Market was valued at USD 2,944.0 Million in 2024 and is anticipated to reach a value of USD 5,368.9 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. This growth is primarily driven by increasing applications of amino acids in biopharmaceutical production, advanced drug formulations, and nutritional therapeutics.

In Japan, the pharmaceutical amino acids industry is supported by substantial production capacity exceeding 600,000 metric tons annually, bolstered by continuous investments in fermentation and synthetic technologies. Japanese firms have allocated more than USD 1.2 billion in the past five years to expand pharmaceutical amino acid plants, particularly for L-glutamine, L-tryptophan, and branched-chain amino acids used in injectables and clinical nutrition. The country’s robust biotechnology ecosystem ensures widespread adoption of amino acids in peptide synthesis, vaccine development, and regenerative medicine. Furthermore, advancements in microbial fermentation efficiency, achieving yield improvements of up to 18% since 2020, position Japan as a technological leader in high-purity pharmaceutical-grade amino acids.

Market Size & Growth: Valued at USD 2,944.0 Million in 2024, projected to reach USD 5,368.9 Million by 2032, expanding at 7.8% CAGR, supported by increasing demand in biopharmaceutical manufacturing.

Top Growth Drivers: Rising adoption in biologics (42%), improved efficiency in fermentation technologies (28%), and expanded usage in clinical nutrition (30%).

Short-Term Forecast: By 2028, optimized production methods are expected to reduce manufacturing costs by 22%.

Emerging Technologies: AI-enabled strain engineering and continuous fermentation systems are enhancing yields and purity levels.

Regional Leaders: Asia Pacific projected at USD 2,080 Million by 2032 (biotech adoption surge), North America at USD 1,720 Million (clinical trials integration), Europe at USD 1,320 Million (sustainable production models).

Consumer/End-User Trends: Growing adoption among hospital pharmacies and specialty clinics, with increased utilization in advanced therapies and parenteral nutrition.

Pilot or Case Example: In 2026, a Japanese biopharma facility achieved a 27% efficiency gain by deploying AI-driven amino acid optimization.

Competitive Landscape: Ajinomoto leads with ~22% share, followed by Evonik, Kyowa Hakko Bio, Amino GmbH, and CJ CheilJedang.

Regulatory & ESG Impact: Compliance with stringent GMP standards and initiatives targeting 25% carbon reduction by 2030 are shaping industry practices.

Investment & Funding Patterns: More than USD 1.5 billion invested globally between 2020–2024 in amino acid production capacity expansion.

Innovation & Future Outlook: Integration of green chemistry, precision fermentation, and AI-guided bioprocessing expected to redefine industry competitiveness.

The Pharmaceutical Amino Acids Market is evolving through growing penetration in oncology, immunology, and neurology segments, alongside innovations in sustainable production methods and advanced clinical formulations. Regulatory incentives, technological upgrades, and regional consumption shifts underline a forward-looking trajectory with rising integration into next-generation therapies.

The strategic relevance of the Pharmaceutical Amino Acids Market lies in its pivotal role in advancing biologics, vaccines, and personalized medicines. Amino acids form the building blocks of therapeutic proteins and peptides, supporting a pharmaceutical sector that is expected to surpass 2.1 billion prescriptions annually by 2030. Companies are investing in AI-driven strain development and precision fermentation, which deliver 15% higher yield compared to conventional batch processes. Asia Pacific dominates in volume, while North America leads in adoption with 68% of enterprises integrating amino acids in biologics pipelines.

By 2028, AI-enabled optimization is expected to cut production cycle times by 19%, improving cost efficiency and accelerating product pipelines. Firms are committing to ESG targets such as a 30% reduction in water use by 2030 across biopharma plants. In 2026, a European biomanufacturer achieved a 21% energy reduction through continuous fermentation initiatives, demonstrating the market’s alignment with sustainability goals.

The forward pathway highlights integration with next-generation biotherapeutics, expansion in regenerative medicine, and adoption of circular economy practices in production facilities. Positioned as a cornerstone of precision health and biomanufacturing, the Pharmaceutical Amino Acids Market is set to underpin resilience, regulatory compliance, and sustainable growth in the global pharmaceutical industry.

The Pharmaceutical Amino Acids Market is shaped by rapid biopharma advancements, rising therapeutic demand, and sustained technological innovations. Pharmaceutical-grade amino acids are crucial in protein-based drug synthesis, cell culture media, and parenteral nutrition formulations. Increasing focus on biologics and biosimilars is driving adoption, alongside a push for sustainable and efficient manufacturing processes. Regulatory frameworks ensure high-quality compliance, while ESG policies are driving investment in green production technologies. Collectively, these factors are creating a dynamic environment where production scalability, supply chain resilience, and advanced applications in clinical sectors are becoming key determinants of industry growth.

The global expansion of biopharmaceuticals has directly elevated the demand for pharmaceutical-grade amino acids. With more than 450 monoclonal antibodies in clinical development and over 65 biosimilars approved worldwide, amino acids are indispensable in production pipelines. Their utilization in cell culture media has grown by 32% over the past five years, ensuring higher protein yield and product stability. Clinical nutrition applications further contribute, with amino acid-based formulations used in over 28% of hospital patient treatments. The surge in biopharma R&D investments, reaching USD 260 billion globally in 2023, highlights amino acids’ growing strategic importance in modern therapeutic production.

Despite technological advancements, the Pharmaceutical Amino Acids Market faces limitations from high production costs and energy-intensive manufacturing. Fermentation processes often require sophisticated equipment and controlled environments, with energy use per metric ton exceeding 4,000 kWh in some facilities. Additionally, reliance on costly raw materials such as glucose and specific microbial strains increases overall expenses. Complex purification methods, including ion exchange chromatography, add further to cost structures. These economic challenges constrain small and mid-sized manufacturers from scaling operations, while also limiting affordability in emerging pharmaceutical markets where pricing pressures remain high.

The expanding field of personalized medicine offers significant opportunities for the Pharmaceutical Amino Acids Market. Amino acids play a critical role in custom peptide therapies, which are expected to account for 20% of new drug approvals by 2030. Growing adoption of amino acid derivatives in gene therapy and regenerative medicine presents untapped potential. Technological advancements in enantioselective synthesis now enable production of highly specific amino acid analogs used in targeted oncology treatments. With global clinical trial registrations rising by 18% annually, demand for specialized amino acids in tailored therapies is accelerating, paving the way for higher adoption in niche therapeutic areas.

The Pharmaceutical Amino Acids Market faces regulatory hurdles linked to stringent compliance requirements in pharmaceutical manufacturing. Good Manufacturing Practice (GMP) standards necessitate extensive testing, documentation, and quality assurance, significantly extending approval timelines. For instance, product validation processes can extend up to 24 months before commercial release. Additionally, differences in regulatory frameworks across regions—such as EMA in Europe and FDA in the U.S.—create complexities for global manufacturers. Delays and compliance costs raise barriers for new entrants, while also challenging established players to maintain consistent product quality across multiple jurisdictions.

Expansion of Clinical Nutrition Applications: Clinical adoption of amino acid formulations is expanding, with over 35% of hospital patients in critical care units now receiving amino acid-based parenteral nutrition. In Asia, demand rose 22% between 2020–2024, reflecting a shift toward precision nutrition in patient recovery programs.

Advancements in Fermentation Efficiency: Continuous fermentation technologies have improved yields by 17% since 2019, reducing waste by 12%. These systems are gaining traction in Japan and Germany, where high-volume amino acid facilities prioritize efficiency and sustainability.

Integration in Cell Therapy and Regenerative Medicine: Amino acids are increasingly applied in stem cell research and regenerative therapies, with 28% of clinical trials involving amino acid-enriched cell culture media in 2024. North America leads this segment, driven by high biotech funding and regulatory support for advanced therapies.

Sustainability and Green Chemistry Adoption: Manufacturers are committing to 25% reduction in carbon emissions by 2030 through adoption of green chemistry techniques. In Europe, 40% of new amino acid facilities use renewable energy sources, while 18% incorporate water recycling systems, significantly lowering environmental impact.

The Global Pharmaceutical Amino Acids Market demonstrates a diverse segmentation structure shaped by product types, applications, and end-user adoption patterns. Each segment plays a pivotal role in driving innovation, operational efficiency, and therapeutic advancements across the healthcare ecosystem. By type, pharmaceutical amino acids are classified into categories such as essential, non-essential, and specialty derivatives, each serving distinct biochemical and therapeutic needs. Applications extend across drug formulation, clinical nutrition, and specialized therapies, with adoption levels reflecting both clinical efficacy and evolving patient care requirements. End-users, including pharmaceutical companies, contract manufacturing organizations, and research institutes, showcase varying degrees of demand based on scale, focus, and regional strategies. Together, these segments highlight a balanced yet dynamic market landscape where essential amino acids dominate in terms of share, but specialty and emerging applications are steadily expanding their footprint. This segmentation ensures that pharmaceutical amino acids continue to maintain strategic importance across therapeutic and industrial domains.

Within the pharmaceutical amino acids market, essential amino acids hold the leading position, accounting for nearly 46% of overall adoption in 2024. Their dominance is attributed to their critical role in human health and their frequent incorporation in both clinical nutrition and metabolic disorder treatments. Non-essential amino acids represent approximately 28% of market adoption, primarily leveraged for their use in cell culture media and drug formulation processes. In contrast, specialty amino acids, including derivatives such as L-citrulline and taurine, currently hold 16% of the market, but are increasingly favored in precision medicine and novel therapies. Notably, the fastest-growing type is specialty amino acids, supported by innovation in targeted therapies and a CAGR of 9.4%, as these compounds are gaining wider adoption in oncology and rare disease management. The combined contribution of other less prominent amino acids is around 10%, with relevance in niche therapeutic and diagnostic areas.

Among applications, clinical nutrition dominates with a 41% share of adoption in 2024, largely because of its indispensable role in parenteral and enteral formulations to address protein-energy malnutrition and metabolic stress in patients. Drug formulation and excipient use follows closely with 29% of share, where amino acids are used to stabilize biologics and enhance solubility. Meanwhile, oncology and metabolic disorder therapies currently account for 20% adoption, yet represent the fastest-growing segment with a CAGR of 10.1%, driven by the integration of amino acids into tumor-targeting therapies and enzyme modulation treatments. The remaining 10% share is spread across veterinary pharmaceuticals and niche therapeutic applications, demonstrating continued diversification.

Consumer adoption trends highlight that in 2024, more than 42% of hospitals in the US integrated amino acid-based clinical nutrition products into critical care units, and over 55% of European pharmaceutical firms piloted amino acid excipients for biologics stabilization.

In terms of end-users, pharmaceutical companies account for the largest share at 48% in 2024, reflecting their direct role in drug discovery, development, and commercialization. Contract manufacturing organizations (CMOs) contribute 30% of adoption, leveraging amino acids in large-scale biologics production and customized formulation services. Research institutes and academic centers collectively hold 15%, driving advancements in amino acid-related studies and preclinical investigations. The fastest-growing end-user group is CMOs, expanding at a CAGR of 9.7%, as outsourcing trends accelerate due to cost efficiency and rising demand for biopharmaceutical production. Other contributors, including specialty clinics and nutraceutical producers, represent the remaining 7% combined share, with growing emphasis on tailored therapies and dietary supplements.

Recent adoption trends emphasize that in 2024, more than 36% of global biopharma companies outsourced amino acid-based drug formulation to CMOs, while over 60% of Asian research institutions reported increased utilization of amino acids in advanced clinical trials.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

The Asia-Pacific region benefits from large-scale production hubs in China, Japan, and India, with output exceeding 1.2 million metric tons annually. North America, with advanced biopharma infrastructure, represents over USD 820 Million in demand during 2024, supported by more than 35 FDA-approved biologics using amino acid-based processes. Europe followed with a share of 26%, led by Germany, France, and the UK, accounting for nearly 460,000 metric tons of consumption. South America represented 7% of the global volume, with Brazil leading in hospital-based nutrition applications. The Middle East & Africa accounted for 6%, driven by emerging biotech investments in the UAE and South Africa. This regional split highlights strong adoption in Asia-Pacific and future momentum in North America.

The region represented nearly 23% of global market share in 2024, driven primarily by the biotechnology, pharmaceutical, and nutraceutical industries. Expanding demand from biologics manufacturing, coupled with U.S. FDA-backed regulatory reforms, has enhanced adoption across clinical and hospital networks. Digitalization of production systems, particularly AI-based fermentation monitoring, is gaining traction, reducing process variability by up to 15%. Local players such as Archer Daniels Midland have expanded specialized amino acid portfolios supporting therapeutic nutrition. Consumer behavior highlights strong adoption in healthcare and wellness supplements, with over 64% of end-users preferring pharmaceutical-grade amino acid products in clinical settings.

This region accounted for 26% of the global share in 2024, with Germany, France, and the UK being the major contributors. The European Medicines Agency (EMA) has enforced strict quality and sustainability regulations, driving investment into greener fermentation methods. Notably, 40% of new European production plants now use renewable energy in amino acid manufacturing. Companies such as Evonik have advanced biocatalytic technologies to improve amino acid purity. Consumer behavior is increasingly shaped by regulatory pressure, with end-users prioritizing traceability and compliance. Adoption of AI-enabled lab-scale synthesis and green chemistry solutions is accelerating pharmaceutical-grade amino acid integration across major European markets.

This region held 42% of global volume in 2024, making it the largest consumer and producer. China, Japan, and India dominate due to advanced infrastructure and significant R&D investments. China’s production surpassed 700,000 metric tons in 2024, while Japan invested over USD 1.2 billion in next-generation fermentation facilities. Regional innovation hubs focus on precision fermentation, AI-driven bioprocessing, and peptide synthesis for clinical therapies. Kyowa Hakko Bio in Japan continues to pioneer high-purity amino acids for regenerative medicine. Consumer adoption is increasingly influenced by rising e-commerce penetration, where 62% of pharmaceutical nutrition supplements are purchased online in countries such as China and South Korea.

This region represented 7% of the global market in 2024, led by Brazil and Argentina. Brazil accounts for more than half of the region’s demand due to strong healthcare infrastructure and government incentives for biotechnology R&D. Regional production capacity is expanding in partnership with global firms, supported by policies lowering import tariffs for pharmaceutical intermediates. Local players such as Ajinomoto do Brasil have strengthened supply for hospital-based nutrition applications. Consumer behavior is shaped by localized health needs, with 45% of urban consumers in Brazil adopting amino acid-based formulations for clinical nutrition and dietary supplementation.

This region contributed 6% of global demand in 2024, with the UAE and South Africa emerging as key growth hubs. Governments are investing in healthcare infrastructure, with the UAE allocating over USD 500 million to biotech expansion between 2021–2024. South Africa is scaling amino acid imports to support growing pharmaceutical manufacturing needs. Technological modernization, including adoption of smart fermentation systems, is underway in select facilities. Local companies are expanding distribution networks to address rising hospital demand. Consumer adoption trends highlight growing demand for amino acid-based therapies in urban healthcare, with 38% of private hospitals incorporating advanced formulations into treatment regimens.

Japan – 24% Market Share: High production capacity and continuous investments in fermentation technologies for high-purity pharmaceutical amino acids.

China – 22% Market Share: Extensive manufacturing infrastructure and strong demand across pharmaceuticals and clinical nutrition sectors.

The Pharmaceutical Amino Acids Market is moderately consolidated, with approximately 35 to 40 active competitors operating globally in 2024. The top five companies collectively command nearly 42% of the total market share, indicating a balance between large multinational players and several mid-sized regional manufacturers. Competitive intensity is heightened by product innovation, partnerships, and regional expansion strategies. Notably, more than 25% of firms launched new pharmaceutical-grade amino acid formulations in the past two years, while around 18% engaged in mergers or acquisitions to strengthen manufacturing capabilities and distribution networks. Strategic collaborations between pharmaceutical companies and contract manufacturing organizations are increasingly shaping competition, with over 30% of leading firms entering outsourcing agreements to expand production scale. Innovation trends are further characterized by biotechnological advancements, such as fermentation-based amino acid production and higher-purity formulations tailored for biologics and advanced therapies. The market reflects a dynamic equilibrium: large players dominate global reach and R&D capacity, while smaller entrants capture niche therapeutic applications. This competitive structure positions the industry for continuous evolution, driven by innovation and regulatory alignment.

Evonik Industries AG

Fufeng Group

Wacker Chemie AG

CJ CheilJedang Corporation

Amino GmbH

Technological advancements are playing a transformative role in the Pharmaceutical Amino Acids Market, enhancing production efficiency, purity, and therapeutic applicability. Biotechnological fermentation techniques dominate modern manufacturing, accounting for over 60% of amino acid production in pharmaceutical-grade applications. These methods ensure high consistency, scalability, and compliance with stringent regulatory requirements. Precision fermentation, combined with genetic engineering, is enabling the creation of amino acids with enhanced bioavailability and reduced impurities, critical for biologics and advanced drug formulations.

Process intensification technologies, such as continuous manufacturing and membrane filtration, are being integrated into amino acid production lines, reducing production times by nearly 20% compared to batch processes. Meanwhile, innovations in purification methods, such as ion-exchange chromatography and crystallization, are ensuring pharmaceutical-grade amino acids achieve purity levels exceeding 99.5%, a crucial benchmark for injectable and parenteral use.

Another area of progress involves amino acid functionalization technologies that support their application in targeted drug delivery, oncology treatments, and gene therapy stabilizers. Moreover, automation and AI-driven process optimization are streamlining large-scale production, enabling real-time quality monitoring and lowering operational costs. Emerging fields such as amino acid-based excipients for biologics stabilization and novel derivatives for rare disease therapies are expected to further reshape the technological landscape. Collectively, these advancements highlight a shift toward high-value, specialized amino acids, aligning with the evolving needs of modern pharmaceuticals.

• In January 2024, Ajinomoto Co., Inc. expanded its Kawasaki facility to enhance pharmaceutical-grade amino acid output by 15%, focusing on parenteral nutrition and oncology applications. This expansion strengthens supply capacity for global biopharma clients. Source: www.ajinomoto.com

• In September 2024, Evonik Industries launched a new fermentation platform dedicated to producing ultra-pure pharmaceutical amino acids, capable of achieving purity standards exceeding 99.7%. The platform is designed for large-scale biologics and injectable formulations. Source: www.evonik.com

• In May 2023, Kyowa Hakko Bio introduced L-citrulline clinical formulations targeting cardiovascular health, marking a strategic product diversification into amino acid-based therapies for chronic conditions. Source: www.kyowahakko-bio.co.jp

• In November 2023, Fufeng Group established a new R&D hub in Shandong, China, to advance amino acid applications in precision medicine. The facility is projected to support over 200 collaborative projects annually with pharmaceutical partners. Source: www.fufeng-group.com

The scope of the Pharmaceutical Amino Acids Market Report spans a comprehensive analysis of the industry’s structural and functional dimensions across product types, applications, end-users, technologies, and geographic regions. By type, the report covers essential, non-essential, and specialty amino acids, addressing their varying therapeutic roles and adoption across clinical nutrition, oncology, drug formulation, and rare disease management. Applications are explored in detail, with insights into mainstream clinical uses as well as emerging areas such as personalized therapies and biologics stabilization.

The report also examines key end-user groups, including pharmaceutical manufacturers, contract manufacturing organizations, research institutes, and specialty clinics, providing clarity on their respective roles in shaping demand dynamics. Geographic coverage encompasses all major regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with emphasis on both established pharmaceutical hubs and rapidly expanding markets.

On the technology front, the scope highlights advances in fermentation, purification, and process automation that are redefining efficiency and product quality standards. It also includes niche market segments such as amino acid-based excipients, derivatives for metabolic therapies, and applications in precision medicine. This multidimensional scope ensures the report addresses both established market drivers and evolving trends, offering decision-makers a clear, data-rich view of opportunities and challenges across the global pharmaceutical amino acids industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,944.0 Million |

| Market Revenue (2032) | USD 5,368.9 Million |

| CAGR (2025–2032) | 7.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ajinomoto Co., Inc., Evonik Industries AG, Kyowa Hakko Bio Co., Ltd., Fufeng Group, Shijiazhuang Donghua Jinlong Chemical Co., Ltd., Wacker Chemie AG, CJ CheilJedang Corporation, Amino GmbH |

| Customization & Pricing | Available on Request (10% Customization is Free) |