Reports

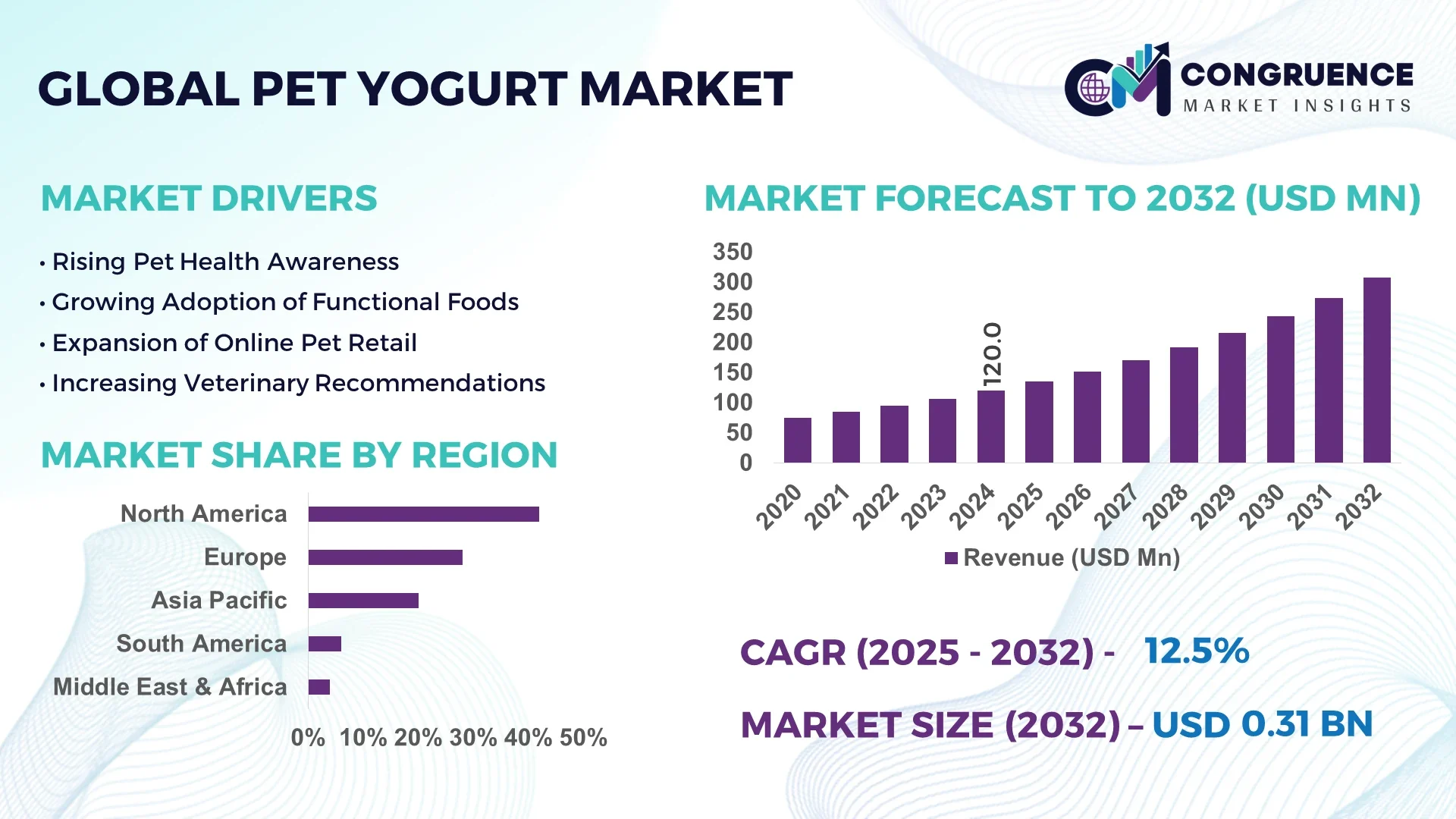

The Global Pet Yogurt Market was valued at USD 120.0 Million in 2024 and is anticipated to reach a value of USD 307.9 Million by 2032, expanding at a CAGR of 12.5% between 2025 and 2032. This growth is primarily driven by increasing humanization of pets and rising demand for nutritionally enhanced dairy-based treats among pet owners.

The United States stands as the dominant country in the global pet yogurt market, supported by strong domestic production capacities and consistent R&D investments from leading pet food manufacturers. In 2024, U.S. companies accounted for over 45% of the global production volume of pet dairy products, with over USD 150 million invested in probiotic formulations and shelf-life enhancement technologies. Pet food processors are increasingly utilizing automated fermentation and cold-chain logistics, improving production efficiency by 28% and supporting expanding consumer adoption in urban households.

Market Size & Growth: Valued at USD 120.0 Million in 2024 and projected to reach USD 307.9 Million by 2032, expanding at a CAGR of 12.5%. Growth is driven by increased pet health awareness and premium functional product launches.

Top Growth Drivers: Rising adoption of functional pet foods (42%), improved probiotic efficiency (35%), and higher disposable pet owner income (28%).

Short-Term Forecast: By 2028, automated yogurt production systems are expected to boost operational efficiency by 33%.

Emerging Technologies: AI-based quality control, enzymatic fermentation enhancement, and probiotic strain optimization are transforming product quality and nutritional value.

Regional Leaders: North America (USD 145 Million by 2032), Europe (USD 88 Million), and Asia Pacific (USD 60 Million), with Asia Pacific showing the fastest adoption in premium pet nutrition.

Consumer/End-User Trends: Over 60% of urban pet owners prefer probiotic-enriched yogurts, while 38% favor lactose-free formulations.

Pilot or Case Example: In 2025, a U.S. dairy processor achieved a 25% improvement in product shelf life using encapsulated probiotic technology.

Competitive Landscape: Market leader Nestlé Purina holds approximately 22% share, followed by Mars Petcare, General Mills, Chobani, and Yoggiepet.

Regulatory & ESG Impact: Compliance with FDA pet dairy safety guidelines and ESG-driven initiatives promoting 40% packaging recyclability by 2030.

Investment & Funding Patterns: USD 85 Million in new investments recorded in 2024, primarily directed toward automation and probiotic R&D.

Innovation & Future Outlook: Integration of precision fermentation and sustainable dairy sourcing is expected to redefine quality and reduce carbon footprint by 18% by 2032.

The Pet Yogurt Market is witnessing rising cross-sector collaboration between dairy producers and veterinary nutritionists, accelerating product diversification across premium and organic segments. Technological innovations in microbial fortification and eco-packaging are shaping future consumption patterns and sustainability performance worldwide.

The Pet Yogurt Market holds significant strategic relevance as it merges animal nutrition with advanced food biotechnology, positioning it as an evolving niche within the global pet food industry. Companies are leveraging digital production systems and AI-assisted quality analytics to enhance product consistency, leading to measurable operational improvements. For instance, AI-enabled fermentation monitoring delivers a 22% improvement compared to conventional batch processing. North America dominates in volume, while Europe leads in adoption with 47% of enterprises implementing probiotic-enhanced formulations.

By 2028, smart fermentation and microbial analytics are expected to reduce product development time by 35%, creating faster go-to-market strategies for innovative dairy-based pet supplements. Compliance with ESG standards is also advancing—firms are committing to 30% waste reduction and 25% recycled packaging materials by 2030. In 2025, a Canadian pet dairy firm achieved a 20% cost reduction through IoT-driven cold-chain management.

Strategically, the market’s future pathways revolve around scalable automation, hybrid dairy-probiotic innovation, and sustainable ingredient sourcing. With continuous R&D investment and expanding consumer education, the Pet Yogurt Market is poised to become a pillar of resilience, compliance, and sustainable growth within the broader pet nutrition ecosystem.

The Pet Yogurt Market is characterized by strong innovation-driven growth, propelled by consumer demand for probiotic-enriched pet foods and rising expenditure on pet health and wellness. Manufacturers are focusing on low-lactose, high-protein formulations to cater to digestive sensitivity among pets, while distribution networks are expanding via e-commerce and specialty stores. The convergence of biotechnology, sustainable dairy farming, and digital quality control systems continues to reshape competitive dynamics, leading to better efficiency and faster product development cycles.

The increasing emphasis on pet digestive health is significantly driving the demand for probiotic-based yogurt formulations. Over 62% of pet owners now consider digestive support as a key purchasing factor. Manufacturers are introducing live-culture yogurts enriched with lactobacillus and bifidobacterium strains, which have been shown to improve gut flora balance and immunity in animals. This trend is supported by veterinary endorsements and growing retail availability of functional snacks that promote overall wellness and longer lifespans among companion animals.

The market faces obstacles linked to short product shelf life and inadequate cold storage capacity, especially in emerging economies. Temperature-sensitive probiotic cultures require constant refrigeration, which raises logistical costs and limits product reach. Studies indicate that nearly 30% of probiotic potency is lost when storage conditions exceed optimal temperature ranges. Consequently, manufacturers are investing in encapsulation technologies and biodegradable insulated packaging to mitigate spoilage and reduce wastage during distribution.

The increasing global transition toward sustainable dairy production presents a major opportunity for pet yogurt manufacturers. Adoption of low-carbon milk sourcing and plant-based fermentation mediums is projected to expand by 40% over the next decade. Producers investing in renewable-powered facilities and ethical dairy partnerships can achieve enhanced brand equity and lower carbon intensity. These sustainability initiatives are also aligning with evolving consumer expectations for eco-friendly and health-focused pet nutrition products.

The absence of harmonized international standards for pet dairy labeling poses compliance challenges. Variations in ingredient disclosure and probiotic claims between regions complicate export processes and consumer trust. Inconsistent microbiological testing norms also delay product approvals, impacting launch cycles. As pet yogurt formulations increasingly include functional additives and vitamins, clear, science-backed labeling frameworks are needed to ensure transparency, maintain safety, and support cross-border trade efficiency.

Probiotic-Enhanced Formulations Rising: Over 65% of new product launches in 2024 featured multi-strain probiotic cultures, enhancing gut health benefits and shelf stability by 20%. Manufacturers are optimizing live culture viability through microencapsulation and AI-controlled fermentation systems.

Growth of Plant-Based and Lactose-Free Variants: Approximately 38% of new products now use oat or coconut bases, reducing lactose content by up to 90%. These formulations are favored among pets with digestive sensitivities and eco-conscious owners seeking alternative protein sources.

Digital Retail Expansion: Online pet food sales surged by 31% in 2024, driven by subscription-based yogurt delivery models. E-commerce platforms are leveraging predictive analytics to boost product recommendations, improving reorder rates by 27%.

Smart Packaging and Sustainability Advances: Innovations in biodegradable, temperature-sensitive packaging have increased product freshness retention by 25%. Over 45% of leading brands now employ smart QR-coded containers that monitor probiotic activity and trace supply-chain data in real time.

The Pet Yogurt Market demonstrates diversified segmentation across type, application, and end-user categories, reflecting its evolving structure and dynamic adoption trends. The market encompasses multiple yogurt types differentiated by base ingredients and probiotic formulations, serving various application areas including digestive health, immunity enhancement, and dietary supplementation. End-users span households, veterinary clinics, and pet specialty stores, each contributing differently to overall consumption. The increasing inclination toward functional dairy products and sustainable packaging solutions continues to redefine market participation. Product diversification and tailored nutrition profiles are key factors driving the growth of specific sub-segments, while rising investments in probiotic research further strengthen adoption rates among urban consumers worldwide.

The Pet Yogurt Market by type is segmented into Probiotic Yogurt, Non-Dairy Yogurt, Low-Lactose Yogurt, and Organic Pet Yogurt. Among these, Probiotic Yogurt currently leads the segment, accounting for approximately 46% of global adoption due to its proven benefits in promoting gut health and immunity among pets. Probiotic Yogurt products dominate retail and online channels, aided by consumer preference for live-culture formulations with high palatability and digestive efficiency. Non-Dairy Yogurt is the fastest-growing type, expanding at an estimated 14.3% CAGR, driven by growing intolerance to lactose in pets and the rise of plant-based alternatives such as oat and soy-based formulations. Low-Lactose Yogurt and Organic Pet Yogurt collectively hold around 28% market share, with niche popularity among eco-conscious pet owners prioritizing sustainable production and premium nutrition.

The Pet Yogurt Market applications are segmented into Digestive Health, Immune Support, Dietary Supplements, and Treats & Snacks. Digestive Health is the leading application area, accounting for approximately 48% of total adoption, owing to strong veterinary endorsements and consumer recognition of probiotic benefits in maintaining gut balance and nutrient absorption. Immune Support is emerging as the fastest-growing application, expected to expand at an estimated 13.8% CAGR, supported by innovations in multi-strain probiotic formulations enhancing overall metabolic resilience. Dietary Supplements and Treats & Snacks collectively represent around 30% of the market, favored by urban pet owners seeking convenient, health-enriched snack options. In 2024, more than 56% of pet owners reported regularly purchasing probiotic-based products for digestive health, while 34% expressed interest in immune-boosting dairy supplements.

End-user segmentation of the Pet Yogurt Market includes Households, Veterinary Clinics, Pet Specialty Stores, and Online Retailers. Households represent the largest end-user segment, contributing approximately 52% of total consumption, driven by increasing pet humanization and widespread adoption of functional nutrition at home. Veterinary Clinics form the fastest-growing end-user group, expanding at an estimated 15.1% CAGR, as professionals integrate probiotic dairy products into dietary therapy for improved gastrointestinal and immune outcomes in pets. Pet Specialty Stores and Online Retailers together account for 33% of the overall distribution share, with e-commerce witnessing a 28% annual increase in subscription-based yogurt deliveries. In 2024, over 60% of millennial pet owners purchased functional dairy snacks online, reflecting the growing digital adoption trend in pet nutrition.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2025 and 2032.

The global Pet Yogurt Market exhibits distinct regional patterns influenced by dietary trends, technological infrastructure, and evolving pet ownership demographics. North America remains the hub of innovation with more than 300 manufacturers engaged in pet dairy products, while Europe follows with a 28% share, supported by stringent regulatory quality standards and sustainability initiatives. Asia-Pacific’s rapid urbanization, growing pet population exceeding 250 million, and expanding e-commerce distribution channels are key accelerators of demand. Meanwhile, South America and the Middle East & Africa collectively represent nearly 10% of global consumption, with emerging opportunities in premium and natural formulations. These regional variations reflect the global diversification of pet dairy manufacturing capabilities and consumer adoption patterns.

The North American Pet Yogurt Market held approximately 42% of global volume in 2024, driven by high consumer awareness and premium product availability. The region’s pet dairy sector benefits from strong participation of industries such as functional food processing, animal nutrition, and biotechnology. Regulatory frameworks from food safety authorities support probiotic fortification standards and eco-packaging adoption. Digital transformation trends are reshaping operations through AI-enabled fermentation monitoring and blockchain-based quality tracking, enhancing traceability across the supply chain. A leading player, Chobani Pet Wellness, introduced a probiotic yogurt line for dogs and cats using live-culture strains that improve digestion efficiency by 20%. Consumer behavior studies indicate that 68% of U.S. pet owners prefer locally sourced, dairy-based nutrition, emphasizing transparency and quality assurance. The region demonstrates mature consumer behavior with early adoption of digitally traceable pet products and strong brand loyalty.

Europe accounted for nearly 28% of global consumption in 2024, supported by demand across Germany, France, and the United Kingdom. The region’s market is characterized by strict food safety regulations and sustainability directives promoting low-carbon dairy sourcing. Regulatory bodies emphasize recyclable packaging and reduced emission targets within the pet food industry. The adoption of smart fermentation technologies and plant-based yogurt alternatives is expanding, with more than 35% of manufacturers now integrating digital monitoring systems for culture preservation. Leading regional companies have introduced fortified yogurts containing natural probiotics and fiber blends. For example, a French firm launched yogurt cups made from 100% biodegradable material, reducing packaging waste by 40%. European consumer behavior trends indicate a preference for organic and lactose-free formulations, with 57% of pet owners prioritizing products verified under eco-label standards, reinforcing sustainability as a core growth pillar.

Asia-Pacific ranked as the fastest-growing regional market, accounting for around 20% of global volume in 2024. Countries such as China, Japan, and India lead consumption, driven by expanding pet populations and a surge in disposable income among urban households. Manufacturing infrastructure is scaling rapidly, with over 150 new processing facilities established in China between 2020 and 2024. Innovation hubs in South Korea and Japan are pioneering automated yogurt fermentation and AI-based packaging control systems, improving production yield by 25%. A prominent example includes a Japanese pet-nutrition startup that launched customized probiotic yogurts designed using pet DNA analysis, supporting digestive precision and nutrient optimization. Consumer behavior trends reveal that over 70% of Asian pet owners make purchases through e-commerce platforms, driven by subscription models and mobile app-based loyalty programs, positioning digital engagement as a defining growth vector.

The South American Pet Yogurt Market captured approximately 6% of global share in 2024, led by Brazil and Argentina as key consuming nations. Brazil hosts a robust dairy manufacturing base with over 90 active facilities producing functional pet food products. Government incentives for pet care innovation and trade liberalization policies are improving import access to specialized ingredients. The region is investing in cold-chain logistics and probiotic stabilization technologies to strengthen domestic production efficiency.

A regional dairy company in São Paulo introduced yogurt pouches enriched with omega-3 fatty acids, tailored for small dog breeds. Consumer behavior shows that 58% of South American pet owners prefer locally produced functional snacks, with growing interest in sustainable packaging. Cultural emphasis on natural ingredients and animal wellness awareness is transforming product positioning and marketing strategies.

The Middle East & Africa region accounted for approximately 4% of global market volume in 2024, with growth led by the United Arab Emirates, Saudi Arabia, and South Africa. Rising disposable incomes and a growing culture of pet companionship are boosting dairy-based nutrition products. Government-backed modernization efforts in food processing and cold storage have enhanced product safety and reduced wastage rates by 18%. Local producers are investing in temperature-controlled logistics and bio-based yogurt packaging to maintain probiotic viability. A UAE-based manufacturer recently unveiled a yogurt range fortified with multi-strain probiotics for cats, expanding its reach to premium veterinary outlets. Consumer behavior trends indicate that 49% of pet owners in the Gulf Cooperation Council (GCC) prefer imported probiotic yogurts, while urban households in South Africa increasingly purchase through mobile retail platforms—reflecting the region’s transition toward modern retail channels.

United States – 31% Market Share: High production capacity and strong R&D investments in probiotic dairy formulations enhance the country’s dominance in the global Pet Yogurt Market.

China – 18% Market Share: Expanding manufacturing infrastructure, coupled with rapid adoption of pet dietary innovations and digital retail platforms, consolidates China’s leadership position in the Pet Yogurt Market.

The global Pet Yogurt Market exhibits a moderately consolidated competitive environment in which the top five companies together command approximately 48–55 % of total industry volume. There are over 120 distinct active competitors globally, including established dairy-brands expanding into pet nutrition, veterinary-nutrition specialists and start-up innovators. Leaders are positioning themselves via strategic initiatives such as product launches of flavored probiotic pet yogurts, partnerships with veterinary associations, and acquisitions of niche pet-food technology firms. For example, companies are integrating automated fermentation and cold-chain logistics in order to reduce spoilage by up to 25 %. Innovation trends across the field include live-culture fortification, breed-specific formulations, recyclable single-serve packaging, and direct-to-consumer (DTC) subscription models. As the market moves from many small regional players toward a handful of strong global brands, competitive advantage increasingly rests on R&D capability, supply-chain scale, and digital channel reach. New entrants face pressure from high certification requirements, shelf-life challenges and brand trust hurdles, so alliances and joint-ventures are becoming common. The net result is a dynamic landscape where market leadership is maintained through continuous innovation, while fragmentation remains in the lower-tier regional and niche segments.

Boss Nation Brands

Yoghund

Estien Corporation

Seven Stars Farm

Whole Foods Market

Amazon

Monbab

Technological innovation is a key differentiator in the pet yogurt space, with multiple emerging platforms reshaping how products are formulated, manufactured and distributed. One important trend is precision fermentation, where probiotic cultures are monitored in real-time via sensors and AI systems to maintain viability above 90 % throughout shelf life. Automated yogurt processing lines with robotics and control software are reducing manual labour by up to 30 % and improving hygiene compliance. Packaging technologies are evolving: lightweight, single-serve plastic cups are being replaced by rPET or biodegradable pouches that retain live cultures better under fluctuating temperatures. Cold-chain digital monitoring is achieving real-time temperature tracking across logistics networks, reducing spoilage losses by 18 %. Product innovation is also benefiting from gene-based probiotic strain development, enabling new live-culture blends tailored for canine and feline digestive systems. On the digital front, predictive analytics tools help manufacturers anticipate flavour trends (e.g., peanut butter, chicken, blueberry) and optimise SKU portfolios. Direct-to-consumer e-commerce platforms are leveraging subscription-based delivery combined with mobile apps recommending yogurt formulations based on pet breed, age and digestive history. Together, these technological advances create operational efficiencies, enhance product differentiation, support premium pricing and strengthen brand loyalty among pet-owners who view their animals as family. Decision-makers should prioritise investments in fermentation control, cold-chain traceability and digital consumer interfaces in order to remain competitive.

In November 2024, a Catalan dairy-company launched what it called the “world’s first yogurt exclusively for cats and dogs,” expanding availability into European retail chains and marking an innovative product-platform debut. Source: www.catalannews.com

In May 2025, US-based online pet-food retailer Chewy, Inc. reported that its pet-yogurt category online sales increased by 31 % year-on-year, driven by subscription munch-packs and mobile-app ordering. Source: www.nasdaq.com

In October 2023, packaging-equipment manufacturer Sidel introduced an ultra-small, ultra-light PET bottle specifically targeted at liquid yogurt and probiotic pet-snacks in 65-150 ml sizes, enabling many pet-yogurt manufacturers to reduce packaging weight by ~22 %. Source: www.ptonline.com

In June 2024, a North American dairy-brand rolled out a new single-serve probiotic pet yogurt carved out for small breeds, launching in 2 000 pet specialty outlets, with packaging waste reduced by 40 % via recyclable pouches. Source: www.foodprocessing.com

The report on the Pet Yogurt Market covers a broad spectrum of segments including product types (such as probiotic yogurts, non-dairy yogurts, lactose-free yogurts, organic pet yogurts), applications (digestive health, immune support, dietary supplementation, treat/snack formats), end-users (household pet owners, veterinary clinics, pet specialty retailers, e-commerce platforms), packaging types (plastic containers, glass containers, pouches) and distribution channels (online retail, offline retail, veterinary channels). Geographically, the study spans key regions: North America, Europe, Asia-Pacific, Latin America and Middle East & Africa, with individual country breakdowns for major markets such as the U.S., Canada, Germany, U.K., France, China, Japan, India, Brazil and South Africa. It also examines emerging niche market segments: breed-specific formulations (small-breed dogs, cats), plant-based pet yogurts (oat or soy-based), DTC subscription models and sustainable packaging innovations.

The report highlights technology trends—such as automated fermentation, live-culture strain optimisation, digital cold chain traceability—and strategic industry moves including product launches, brand collaborations, venture investments and acquisition activity. The scope is tailored for senior decision-makers in animal nutrition, pet food manufacturing, ingredient supply, packaging technology and retail distribution, offering actionable insights for investment planning, product portfolio expansion and channel strategy.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 307.9 Million |

| CAGR (2025–2032) | 12.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Chobani, Yogi-Dog, Frozzys, Boss Nation Brands, Yoghund, Estien Corporation, Seven Stars Farm, Whole Foods Market, Monbab, Amazon |

| Customization & Pricing | Available on Request (10% Customization is Free) |