Reports

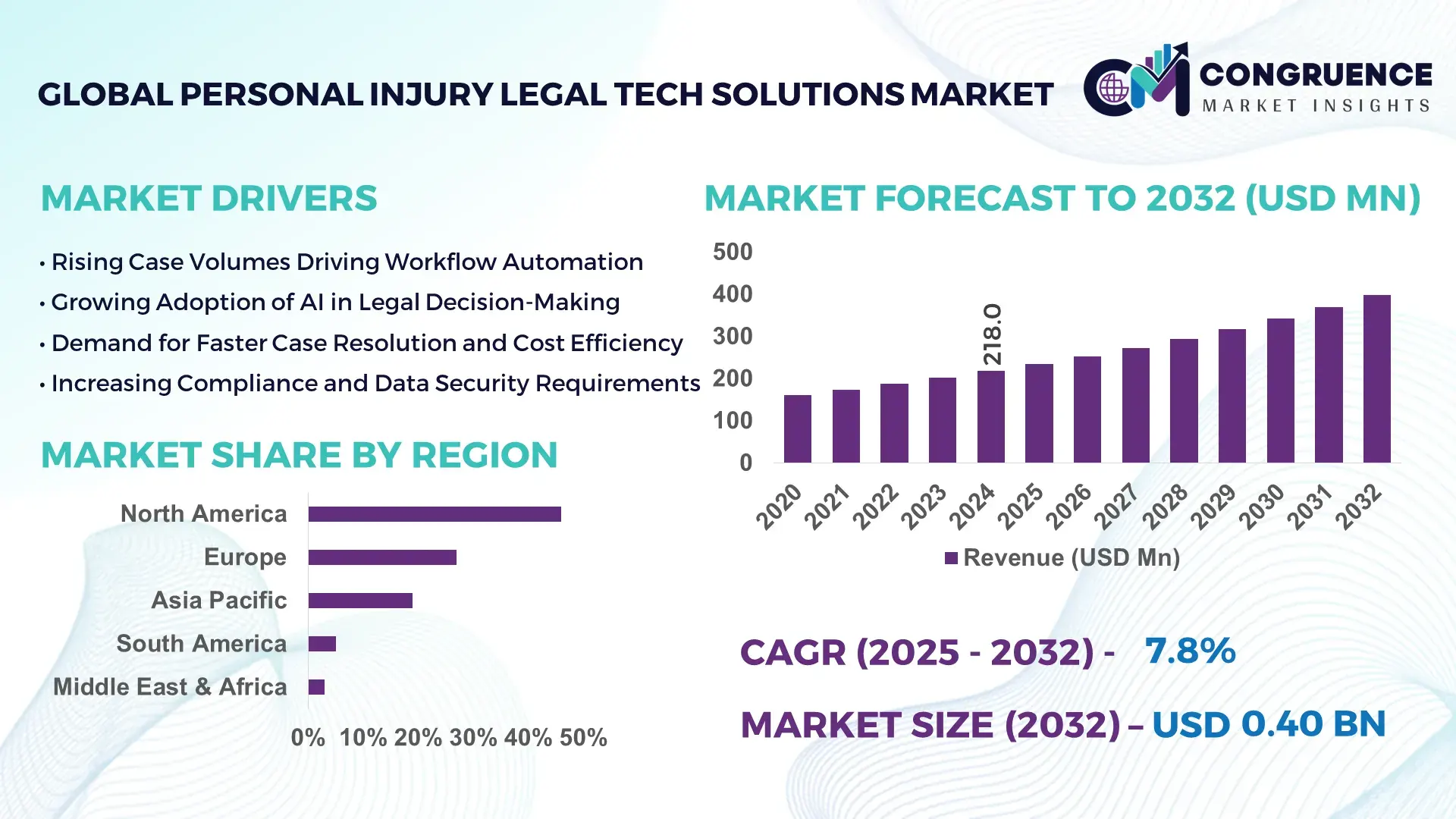

The Global Personal Injury Legal Tech Solutions Market was valued at USD 218.0 Million in 2024 and is anticipated to reach a value of USD 397.6 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is supported by rising digital transformation across personal injury law firms aimed at improving case efficiency, compliance accuracy, and client engagement outcomes.

The United States represents the dominant country in the Personal Injury Legal Tech Solutions Market, supported by advanced digital infrastructure, high legal service digitization, and strong enterprise-scale deployments. Over 78% of mid-to-large personal injury law firms in the U.S. actively use AI-enabled case management or analytics platforms, with cloud-based legal software penetration exceeding 70%. Annual legal tech investment in the U.S. surpassed USD 1.6 billion in recent years, supporting innovations such as predictive settlement analytics, automated evidence indexing, and AI-driven medical record analysis. The country also leads in SaaS-based legal platforms, hosting more than 60% of global personal injury-focused legal tech vendors, alongside extensive integration of e-discovery, billing automation, and litigation intelligence tools across state and federal jurisdictions.

Market Size & Growth: Valued at USD 218.0 Million in 2024, projected to reach USD 397.6 Million by 2032, expanding at a CAGR of 4.8%, driven by efficiency-led digital adoption across litigation workflows.

Top Growth Drivers: AI-assisted case review adoption at 42%, litigation cycle time reduction of 35%, administrative workload reduction of 48%.

Short-Term Forecast: By 2028, automated case processing is expected to reduce claim resolution timelines by 30%.

Emerging Technologies: Predictive legal analytics, NLP-based document review, AI-powered settlement modeling.

Regional Leaders: North America (USD 170.4 Million by 2032) with SaaS dominance; Europe (USD 112.6 Million) driven by compliance automation; Asia Pacific (USD 84.3 Million) led by cloud-first adoption.

Consumer/End-User Trends: Over 65% of personal injury firms prioritize mobile-accessible legal platforms for client engagement.

Pilot or Case Example: In 2023, a U.S.-based pilot reduced evidence review time by 38% using AI document tagging.

Competitive Landscape: Clio (~18%), followed by Filevine, SmartAdvocate, MyCase, and PracticePanther.

Regulatory & ESG Impact: Compliance automation aligned with GDPR and U.S. data privacy mandates accelerates adoption.

Investment & Funding Patterns: Over USD 900 Million invested globally in legal tech platforms over the last three years.

Innovation & Future Outlook: Integration of AI, analytics, and interoperable cloud platforms will define next-phase scalability.

Personal Injury Legal Tech Solutions Market adoption is concentrated across law firms (62%), legal service providers (21%), and insurance-linked litigation support services (17%). AI-enabled case analytics and automated documentation tools are driving faster litigation cycles, while regulatory data protection requirements are accelerating secure cloud adoption. North America leads consumption, followed by Europe’s compliance-driven uptake, with Asia Pacific showing rapid cloud-based expansion and long-term growth potential.

The Personal Injury Legal Tech Solutions Market holds strategic relevance as litigation complexity, data volumes, and compliance requirements intensify across global legal systems. Law firms are increasingly deploying AI-enabled platforms to enhance case accuracy, reduce administrative overhead, and improve client outcomes. For example, AI-based predictive settlement analytics deliver up to 32% faster case resolution compared to traditional manual case assessment models, enabling firms to optimize legal strategies and cost structures.

Regionally, North America dominates in deployment volume, while Europe leads in adoption intensity, with over 58% of personal injury firms using compliance-integrated legal platforms. Asia Pacific is emerging as a high-growth region due to cloud-native legal ecosystems and mobile-first client engagement tools. By 2027, AI-driven legal workflow automation is expected to reduce documentation errors by 40% while improving billable utilization rates by 25%.

From a compliance and ESG perspective, firms are committing to data minimization and digital documentation strategies, achieving up to 50% paper reduction by 2028. In 2024, a U.S.-based legal consortium achieved a 36% reduction in case processing time through AI-enabled evidence management platforms, demonstrating tangible operational gains. Looking forward, the Personal Injury Legal Tech Solutions Market is positioned as a pillar of legal sector resilience, regulatory compliance, and sustainable digital growth.

The Personal Injury Legal Tech Solutions Market is shaped by rapid digitalization within legal services, rising litigation caseloads, and increasing reliance on data-driven decision-making. Law firms are transitioning from manual case handling to integrated digital platforms to manage evidence, documentation, billing, and client communication. Cloud deployment, AI-assisted analytics, and workflow automation are redefining operational benchmarks. The market is further influenced by evolving data protection regulations, client demand for transparency, and pressure to reduce legal cycle times. Integration with insurance databases, healthcare records, and court systems continues to expand the functional scope of Personal Injury Legal Tech Solutions Market platforms.

Workflow automation is a key growth driver, with over 60% of personal injury firms reporting measurable productivity improvements after adopting legal tech solutions. Automated intake, document classification, and deadline tracking reduce administrative workloads by up to 45%. AI-powered tools enable faster evidence review, improving legal accuracy and reducing human error. These efficiencies allow firms to manage higher caseloads without proportional staffing increases, reinforcing sustained demand for Personal Injury Legal Tech Solutions Market platforms.

Despite strong adoption, data security concerns and integration challenges limit broader deployment. Personal injury cases involve sensitive medical and financial data, increasing compliance risks. Nearly 34% of firms report delays due to interoperability issues between legacy systems and modern platforms. Cybersecurity investments and regulatory compliance costs also raise deployment barriers, particularly for small and mid-sized firms, slowing uniform market penetration.

AI-powered litigation intelligence offers significant growth opportunities by enabling predictive case outcomes, settlement optimization, and risk assessment. Firms using AI-driven analytics report up to 28% improvement in case win probability. Expansion into insurance-linked claims analysis and medical data interpretation opens new application areas, while subscription-based SaaS models lower adoption thresholds for smaller firms.

Skill shortages in legal technology adoption and resistance to workflow changes remain key challenges. Nearly 41% of firms cite training requirements as a barrier to full platform utilization. Legacy operational cultures and limited technical expertise can delay ROI realization, requiring sustained investment in training and process reengineering.

Rapid Expansion of AI-Driven Case Analytics: AI-enabled case analytics adoption has reached 44% among personal injury law firms, enabling up to 37% faster evidence evaluation. Predictive models now analyze over 1 million historical case records annually, improving settlement accuracy by 29% and reducing litigation uncertainty.

Acceleration of Cloud-Based Legal Platforms: Cloud deployment accounts for 68% of new legal tech installations, offering scalability and remote accessibility. Firms using cloud platforms report 42% improvement in collaboration efficiency and 33% reduction in infrastructure maintenance workloads.

Increased Integration with Healthcare and Insurance Data Systems: Over 52% of platforms now support direct integration with medical record databases and insurance claim systems, reducing manual data entry errors by 46% and improving claim validation timelines by 31%.

Growing Focus on Client-Centric Digital Interfaces: Client portals and mobile-enabled dashboards are used by 61% of firms, improving client response times by 34% and increasing satisfaction scores by 27%, reinforcing long-term digital engagement strategies.

The Personal Injury Legal Tech Solutions Market is segmented based on type, application, and end-user, reflecting how digital tools are deployed across litigation workflows. By type, software-centric platforms dominate due to their scalability, automation depth, and integration with court, insurance, and medical data systems. Applications are primarily centered on case management and document automation, followed by analytics-driven litigation intelligence and client engagement tools. End-user adoption is led by mid-to-large personal injury law firms, while insurers and third-party legal service providers are rapidly increasing usage for claims validation and litigation support. Segmentation trends indicate a clear shift toward AI-enabled, cloud-native platforms that support multi-jurisdiction compliance, real-time collaboration, and data-driven legal decision-making.

Software platforms represent the leading type in the Personal Injury Legal Tech Solutions Market, accounting for approximately 56% of total adoption. These platforms integrate case management, document automation, billing, and analytics into unified environments, enabling firms to reduce administrative workloads and improve litigation efficiency. Cloud-based legal software dominates this category, supported by strong demand for scalability, remote access, and data security compliance. AI-powered analytics tools are the fastest-growing type, expanding at an estimated 6.9% CAGR, driven by predictive settlement modeling, evidence relevance scoring, and outcome forecasting. Adoption is fueled by measurable performance gains, including reductions in case resolution time and improved accuracy in claim valuation. Service-based offerings—such as implementation, customization, and managed legal tech services—along with niche tools like standalone e-discovery modules and digital intake systems collectively account for the remaining 44% share, serving firms with specialized or hybrid deployment needs.

Case management and workflow automation is the leading application segment, representing nearly 39% of overall adoption. These solutions streamline intake, deadline tracking, evidence organization, and task assignment, enabling firms to handle higher caseloads without proportional staff expansion. Their dominance is reinforced by strong integration with court calendars and insurance systems. Litigation analytics and predictive modeling is the fastest-growing application area, expanding at an estimated 7.2% CAGR, supported by rising demand for data-driven legal strategies. Firms increasingly rely on analytics to forecast settlement ranges, assess litigation risks, and optimize negotiation strategies. Other applications—including document automation, billing and time tracking, client portals, and compliance management—collectively contribute around 61% of market activity, addressing operational transparency and client engagement needs. From an adoption perspective, over 46% of personal injury law firms globally reported piloting AI-driven analytics tools in 2024 to enhance litigation planning, while more than 58% of digitally mature firms use client-facing portals to improve communication efficiency.

Personal injury law firms are the dominant end-user group, accounting for approximately 63% of total adoption. Mid-to-large firms lead usage due to higher case volumes, greater digital budgets, and strong emphasis on workflow optimization. These firms report widespread use of integrated platforms to manage evidence, medical records, and insurer communications within a single environment. Insurance-linked legal service providers represent the fastest-growing end-user segment, expanding at an estimated 6.5% CAGR, driven by the need for faster claim validation, fraud detection, and litigation cost control. Insurers increasingly deploy legal tech platforms to align claims handling with legal outcomes. Other end-users—including solo practitioners, third-party litigation support firms, and alternative legal service providers—collectively hold around 37% of adoption, often favoring modular or subscription-based solutions. Adoption trends show that over 52% of law firms with more than 20 attorneys use AI-assisted document review, while nearly 41% of insurers deploy legal analytics tools for dispute resolution optimization.

North America accounted for the largest market share at 46% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2025 and 2032.

North America’s dominance is supported by high digital maturity across legal services, with over 72% of mid-to-large personal injury law firms using cloud-based legal platforms and nearly 58% integrating AI-driven analytics into litigation workflows. Europe follows with an estimated 27% share, driven by compliance-focused legal digitization and strong adoption in the UK and Germany. Asia-Pacific holds approximately 19%, benefiting from rapid cloud penetration, mobile-first legal services, and expanding legal tech ecosystems in China and India. South America and Middle East & Africa together account for the remaining 8%, supported by gradual judicial modernization, cross-border litigation growth, and increasing investments in digital legal infrastructure.

The region holds approximately 46% of the global Personal Injury Legal Tech Solutions Market, making it the most mature regional ecosystem. Demand is primarily driven by personal injury law firms, insurance litigation units, and alternative legal service providers. Regulatory developments around electronic filing, digital evidence admissibility, and data privacy compliance have accelerated platform adoption. Over 65% of firms now rely on integrated case management and document automation systems. AI-driven settlement analytics and medical record digitization are key technological advancements, with automation reducing manual case preparation time by over 35%. Local players such as Filevine and Clio continue expanding AI modules focused on litigation analytics and client engagement. Regional consumer behavior shows higher enterprise-scale adoption, with large firms prioritizing workflow optimization and data-driven litigation strategies.

Europe represents nearly 27% of global market activity, with the UK, Germany, and France as key contributors. Strong regulatory frameworks and data protection mandates have driven demand for explainable, auditable legal tech platforms. More than 54% of personal injury firms in Western Europe use compliance-integrated legal software to manage documentation and cross-border cases. The region has seen increased adoption of AI-assisted document review and multilingual legal platforms, supporting litigation across diverse jurisdictions. Local legal tech providers focus on GDPR-aligned data handling and transparency-driven AI models. Consumer behavior reflects regulatory sensitivity, with firms prioritizing traceable decision logic and secure data storage over experimental automation.

Asia-Pacific accounts for approximately 19% of the Personal Injury Legal Tech Solutions Market and ranks as the fastest-expanding regional segment. China, India, and Japan are the top consuming countries, supported by rising litigation volumes and judicial digitization initiatives. Cloud-first legal platforms now account for over 62% of new deployments in the region. Legal tech adoption is closely tied to mobile platforms, with more than 48% of small and mid-sized firms using mobile-accessible case management tools. Innovation hubs in India and Southeast Asia are producing AI-driven intake and document automation tools tailored for high-volume litigation. Regional consumer behavior is strongly influenced by mobile usage and cost-efficient SaaS models.

South America contributes close to 5% of global market share, led by Brazil and Argentina. Judicial modernization programs and expanding digital court systems are increasing demand for legal workflow automation. Over 39% of law firms in Brazil now use basic digital case tracking tools, while advanced analytics adoption remains in early stages. Government initiatives supporting digital documentation and e-filing are improving platform acceptance. Regional players focus on language localization and integration with national court systems. Consumer behavior reflects price sensitivity, with firms favoring modular and subscription-based solutions over full-suite deployments.

The Middle East & Africa region accounts for approximately 3% of the global market, with growth concentrated in the UAE and South Africa. Legal tech demand is supported by broader digital government initiatives and judicial efficiency programs. More than 33% of law firms in the UAE use cloud-based legal software for case documentation and client communication. Technological modernization includes secure cloud hosting and bilingual legal platforms. Regional regulations emphasize data sovereignty and cross-border compliance. Consumer behavior shows increasing openness to digital tools, particularly among international law firms operating across multiple jurisdictions.

United States – 41% Market Share: Strong legal digitization, high enterprise adoption, and advanced AI-driven litigation platforms support leadership in the Personal Injury Legal Tech Solutions Market.

United Kingdom – 9% Market Share: Regulatory-driven adoption, high compliance requirements, and widespread use of explainable legal AI solutions reinforce market strength.

The Personal Injury Legal Tech Solutions Market exhibits a dynamic competitive environment shaped by a blend of established legal software firms and specialist AI-driven newcomers. The landscape includes 20+ active competitors, ranging from legacy practice management platforms to next-generation AI startups focused on plaintiffs’ workflows. Market dynamics are influenced heavily by strategic investments, product launches, partnerships, and acquisitions that underscore the drive toward automation, cloud adoption, and tailored personal injury capabilities. According to industry tracking, Clio, Filevine, PracticePanther, MyCase, CasePeer, and Litify are consistently cited among leading vendors offering personal injury-relevant software, forming a core competitive set actively enhancing capabilities for case management, document automation, lead intake, and AI-assisted drafting.

The competitive nature of the market is moderately fragmented, with top players collectively accounting for an estimated ~45–55% of total deployments in mature regions like North America, while numerous mid-tier providers and niche offerings serve specialized law firm needs. Litify’s acquisition of CasePeer and CasePeer’s partnership with Filevine illustrate consolidation and collaboration trends aimed at cross-platform interoperability and expanded feature depth. Emerging AI-focused entrants such as EvenUp and Eve enhance competition by targeting high-value workflows including demand letter automation, medical chronology generation, and predictive case evaluation. Venture capital influx into these startups underscores innovation traction, with combined funding rounds exceeding $350M+ in recent years, strengthening their competitive footing against incumbents. The result is a rich, innovation-driven market where players differentiate via AI integration, cloud scalability, workflow customization, and ecosystem partnerships — compelling firms to continuously innovate to maintain relevance across diverse legal practice sizes and geographies.

CasePeer

MyCase

PracticePanther

SmartAdvocate

Rocket Matter

Legal Files

Zola Suite

PainWorth

EvenUp

Eve

Supio

The technology landscape in the Personal Injury Legal Tech Solutions Market is characterized by rapid adoption of cloud-native platforms, artificial intelligence (AI), and machine learning (ML) to streamline core legal workflows and enhance outcomes for both law firms and their clients. Cloud-based practice management systems now dominate deployments, offering scalable access to case files, document repositories, calendaring, and client communications across distributed teams and remote work environments. These platforms support integration with legal research tools, billing systems, and third-party data sources to create cohesive ecosystems that reduce manual coordination overhead. AI and ML are central to current innovation strategies. Today’s systems leverage natural language processing (NLP) to automate document drafting, extract key details from medical and legal records, and summarize complex case inputs into structured formats that save attorneys significant time. For example, certain AI modules can generate medical chronologies and demand letters in minutes rather than hours, while predictive analytics tools estimate potential case outcomes based on historical data patterns. Real-time data parsing improves the accuracy of client intake assessments and supports smarter task prioritization by analyzing incoming leads and highlighting high-value opportunities.

Another key technological transformation is the integration of workflow automation, enabling lawyers to model case progression, assign tasks automatically, and trigger alerts based on deadlines or client communications. Automation accelerates repetitive processes like scheduling, document generation, and compliance checks — which are critical in personal injury cases involving tight statutory deadlines and high volumes of medical documentation. Blockchain and secure distributed ledger technologies are being explored for improved evidence integrity and chain-of-custody tracking, ensuring that digital files and evidence remain tamper-proof. Coupled with advanced encryption and compliance frameworks tailored to legal privacy requirements (e.g., HIPAA in the U.S.), these technologies enhance trust and security. Interoperability standards and APIs are increasingly important as firms integrate legal tech tools across ecosystems, allowing practice management platforms to sync with financial, calendaring, and research systems seamlessly. The proliferation of no-code/low-code customization options enables firms to tailor solutions without heavy IT investment, democratizing advanced technology adoption.

Collectively, these technology trends are transforming the operational fabric of the personal injury legal sector — shifting emphasis from manual case handling to intelligent, data-driven decision-making and integrated digital workflows that support competitive differentiation and improved client service.

Clio invests in EvenUp to expand personal injury tech ecosystem (2025): Clio announced a strategic investment in EvenUp, enabling integration of EvenUp’s AI-driven demand letter and case automation tools into Clio’s ecosystem — enhancing capabilities for over 200 law firms and processing more than 1,000 demands monthly for personal injury cases. Source: www.clio.com

EvenUp raises $150M to scale AI solutions in 2025: AI-focused startup EvenUp closed a $150 million funding round pushing its valuation above USD 2 billion, signaling strong investor confidence in AI tools that support personal injury case documentation and settlement automation. Source: www.journal.com

Filevine launches LeadsAI to enhance personal injury lead processing (2025): Filevine introduced an AI-powered feature, LeadsAI, capable of summarizing incoming personal injury leads and evaluating case suitability — initially deployed for motor vehicle accident practices with plans for broader rollout. Source: www.lawtechdaily.com

Four Legal Tech Firms Named in Forbes Cloud 100 (2025): In the Forbes Cloud 100 ranking, four legal tech companies earned placements, with two additional firms recognized as rising stars — highlighting accelerating adoption of cloud-native and AI-driven tech solutions in law practices including personal injury workflows. Source: www.lawnext.com

The scope of the Personal Injury Legal Tech Solutions Market Report comprehensively covers the competitive, technological, and operational aspects of legal tech tailored to personal injury law practices globally. This report evaluates product types spanning cloud-based and on-premises case management systems, AI-assisted automation modules, document drafting tools, client intake and lead qualification engines, and integrated analytics dashboards. It assesses deployment modes and software functionalities, including legal research integration, compliance support for privacy and security standards like HIPAA, and customizable workflow configurations that adapt to diverse firm sizes and practice specializations.

Geographically, the report analyzes key regions such as North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, benchmarking adoption levels, infrastructure support, regulatory landscapes, and end-user behavior patterns that shape technology uptake. It profiles market demand from a broad set of end users, including solo practitioners, small to mid-sized law firms, large multi-practice firms, insurance and claims departments, and corporate legal teams seeking specialized personal injury capabilities.

The report also highlights emerging niches such as AI-driven predictive litigation outcomes, blockchain-enhanced evidence chain-of-custody tracking, secure client communication tools, and low-code customization frameworks that allow firms to tailor solutions with minimal IT overhead. Strategic initiatives like mergers, partnerships, and funding flows further illuminate where competitive advantage is being forged, while technology trend analysis underscores how advancements in machine learning, NLP, and workflow automation are reshaping operations. This broad and detailed scope equips decision-makers with nuanced insights into market structure, innovation hotspots, and future growth vectors, enabling informed strategic planning and investment decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 218.0 Million |

| Market Revenue (2032) | USD 397.6 Million |

| CAGR (2025–2032) | 7.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Clio, Filevine, Litify, CasePeer, MyCase, PracticePanther, SmartAdvocate, Rocket Matter, Legal Files, Zola Suite, PainWorth, EvenUp, Eve, Supio |

| Customization & Pricing | Available on Request (10% Customization Free) |