Reports

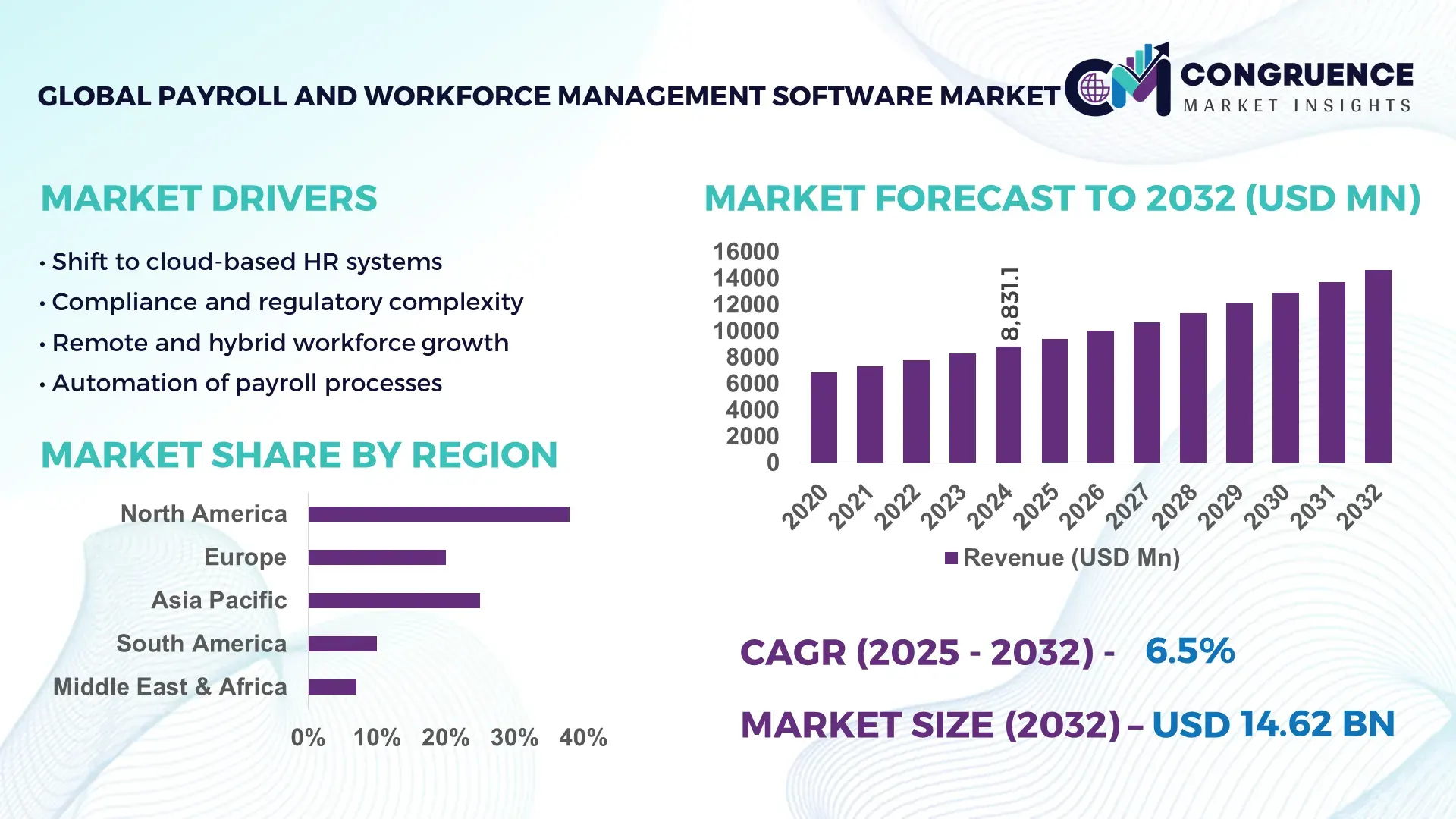

The Global Payroll and Workforce Management Software Market was valued at USD 8831.07 Million in 2024 and is anticipated to reach a value of USD 14615.39 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032. This growth is supported by increasing enterprise demand for automation, compliance accuracy, and real-time workforce analytics across distributed work environments.

The United States represents the most prominent country in the global Payroll and Workforce Management Software ecosystem, supported by a mature enterprise IT infrastructure and high digital HR adoption. In 2024, over 78% of mid-to-large enterprises in the U.S. deployed cloud-based payroll platforms, with more than 62 million employees managed through integrated workforce systems. Annual enterprise HR software spending exceeded USD 18 billion, driven by large-scale deployments across BFSI, healthcare, IT services, and retail sectors. Advanced capabilities such as AI-driven payroll error detection, real-time tax compliance engines, and predictive labor analytics are increasingly embedded, with over 55% of U.S.-based solutions supporting multi-country payroll processing and automated regulatory updates.

Market Size & Growth: Valued at USD 8831.07 Million in 2024 and projected to reach USD 14615.39 Million by 2032 at a CAGR of 6.5%, driven by cloud adoption and increasing workforce digitization.

Top Growth Drivers: Cloud payroll adoption at 71%, payroll error reduction up to 45%, and HR operational efficiency improvements of approximately 38%.

Short-Term Forecast: By 2028, enterprises are expected to achieve payroll processing cost reductions of nearly 32% through automation and AI-enabled compliance tools.

Emerging Technologies: AI-based payroll anomaly detection, API-driven HR ecosystem integration, and blockchain-enabled payroll security.

Regional Leaders: North America projected at USD 5100 Million by 2032 with AI-first adoption; Europe at USD 4100 Million driven by compliance automation; Asia-Pacific at USD 3600 Million fueled by SME cloud migration.

Consumer/End-User Trends: Large enterprises lead adoption, while SMEs show fastest growth due to subscription-based SaaS pricing and mobile-first payroll access.

Pilot or Case Example: In 2023, a multinational IT services firm implemented AI-driven workforce management software, achieving a 41% reduction in payroll cycle time.

Competitive Landscape: ADP holds approximately 18% share, followed by Workday, SAP, Oracle, UKG, and Paychex.

Regulatory & ESG Impact: Increased adoption driven by data protection regulations, automated tax compliance mandates, and workforce transparency reporting.

Investment & Funding Patterns: Over USD 4.2 billion invested globally between 2022–2024, with strong venture funding in AI-powered HR platforms.

Innovation & Future Outlook: Growth in unified HCM platforms, real-time payroll analytics, and cross-border compliance engines shaping long-term market evolution.

The Payroll and Workforce Management Software market serves critical sectors including BFSI, IT & telecom, healthcare, manufacturing, and retail, collectively accounting for over 70% of enterprise deployments. BFSI alone contributes approximately 24% due to stringent payroll accuracy and compliance requirements. Recent innovations include AI-enabled wage forecasting, automated statutory reporting, and employee self-service payroll portals. Regulatory drivers such as evolving labor laws, data privacy frameworks, and digital tax reporting mandates continue to influence adoption patterns. Regionally, North America and Europe demonstrate high per-employee software spend, while Asia-Pacific shows accelerated growth from SME digitalization. Looking forward, embedded analytics, cross-border payroll integration, and sustainability-linked workforce reporting are expected to define future market expansion.

The Payroll and Workforce Management Software Market holds growing strategic relevance as organizations increasingly align workforce operations with cost optimization, regulatory accuracy, and business resilience objectives. Enterprises with over 1,000 employees report up to 42% improvement in payroll accuracy and a 35% reduction in manual processing time following full-scale payroll digitalization initiatives. Cloud-native payroll platforms combined with AI-driven workforce analytics deliver measurable operational advantages; for instance, AI-based payroll automation delivers 48% improvement compared to spreadsheet-driven legacy payroll systems.

From a regional perspective, Asia-Pacific dominates in volume due to large employee bases and expanding SME digitalization, while North America leads in adoption with nearly 78% of enterprises using integrated payroll and workforce management platforms. Europe follows closely, driven by strict labor compliance frameworks and multi-country payroll standardization requirements. By 2027, AI-powered predictive workforce scheduling is expected to improve labor utilization efficiency by approximately 30%, directly supporting margin optimization and service continuity.

Compliance and ESG considerations are becoming embedded within payroll strategies. Firms are committing to workforce transparency and sustainability reporting improvements, including a 25% reduction in paper-based payroll documentation by 2026 through digital payslip adoption. In 2023, a U.S.-based multinational enterprise achieved a 39% reduction in payroll processing errors by deploying machine-learning-based compliance engines across 18 countries. Looking ahead, the Payroll and Workforce Management Software Market is positioned as a core pillar supporting organizational resilience, regulatory alignment, and sustainable workforce growth, particularly as hybrid work models and cross-border employment structures continue to expand.

Cloud-based workforce platforms are driving significant momentum in the Payroll and Workforce Management Software Market by enabling centralized payroll operations across multiple geographies. Over 70% of enterprises now prefer cloud deployment due to faster implementation cycles and reduced IT maintenance requirements. Organizations report up to 40% improvement in payroll cycle efficiency when migrating from on-premise systems. The scalability of cloud platforms supports rapid workforce expansion, particularly for companies managing remote and hybrid employees. Additionally, automatic regulatory updates and integrated tax engines reduce compliance risk, strengthening adoption across regulated industries such as BFSI and healthcare.

Data security concerns remain a key restraint in the Payroll and Workforce Management Software Market, as payroll systems handle sensitive employee and financial data. Enterprises report that nearly 34% of delayed payroll system deployments are linked to integration challenges with legacy HR, ERP, and finance systems. Cross-border payroll further complicates compliance due to varying data residency laws. Cybersecurity investments associated with payroll platforms can increase implementation timelines, particularly for large organizations operating across jurisdictions with strict data protection regulations.

The rapid expansion of global and contingent workforces presents major opportunities for the Payroll and Workforce Management Software Market. Multinational companies increasingly seek unified platforms capable of handling multi-country payroll, local tax compliance, and currency conversion within a single interface. Over 60% of enterprises with international operations plan to consolidate payroll vendors to improve visibility and control. Growth in employer-of-record services and gig employment models further drives demand for flexible, API-driven payroll solutions tailored to diverse employment structures.

Regulatory fragmentation poses a persistent challenge to scalability in the Payroll and Workforce Management Software Market. Labor laws, tax regulations, and reporting standards vary significantly across countries, requiring continuous system updates. Enterprises operating in more than ten jurisdictions report up to 28% higher payroll administration workloads compared to domestic-only operations. Failure to adapt systems quickly to regulatory changes can lead to compliance penalties and operational disruptions, increasing pressure on vendors to maintain highly localized and continuously updated payroll engines.

• Accelerated Adoption of Modular, API-Driven Payroll Platforms: Enterprises are increasingly deploying modular payroll architectures that allow organizations to activate specific workforce functions on demand. Around 58% of large enterprises now use modular payroll components for time tracking, compliance, and benefits, achieving implementation time reductions of nearly 35%. API-based integration enables faster interoperability with ERP and finance systems, improving payroll processing accuracy by approximately 42% while supporting scalable workforce expansion across regions.

• AI-Led Automation Transforming Payroll Accuracy and Cycle Time: Artificial intelligence is rapidly redefining payroll operations through automated anomaly detection, tax validation, and workforce forecasting. Nearly 47% of organizations report payroll error reductions exceeding 40% after adopting AI-enabled payroll engines. Automated payroll reconciliation tools have shortened processing cycles by 33%, while predictive scheduling algorithms improve labor allocation efficiency by close to 29%, particularly in sectors with shift-based workforces.

• Expansion of Real-Time Compliance and Regulatory Intelligence: Continuous regulatory monitoring is emerging as a core capability within payroll and workforce platforms. Approximately 63% of multinational employers now rely on real-time compliance engines to manage statutory changes across jurisdictions. These systems have reduced compliance-related payroll adjustments by 31% and audit preparation workloads by 28%. Automated alerts and rule-based payroll validation are increasingly standard in regions with complex labor regulations.

• Growth in Mobile-First and Employee Self-Service Payroll Usage: Workforce expectations are driving rapid growth in mobile-accessible payroll solutions. Over 69% of employees now access payslips, tax documents, and attendance data through mobile platforms, resulting in a 37% decline in HR support queries. Organizations deploying mobile self-service payroll tools report employee satisfaction improvements of 26% and faster issue resolution timelines by nearly 34%, reinforcing adoption across both enterprise and SME segments.

The Payroll and Workforce Management Software Market is segmented across type, application, and end-user categories, reflecting diverse enterprise needs and deployment priorities. Product types range from core payroll processing platforms to fully integrated workforce management suites combining time tracking, compliance, analytics, and employee self-service. Applications span payroll automation, workforce scheduling, attendance management, benefits administration, and compliance reporting, with demand intensity varying by industry and workforce scale. End-user adoption differs significantly between large enterprises, SMEs, and sector-specific users such as BFSI, healthcare, manufacturing, and retail. Increasing regulatory complexity, hybrid work models, and cross-border employment structures continue to influence segmentation trends, with enterprises favoring flexible, scalable solutions aligned to operational size, geographic footprint, and compliance exposure.

The Payroll and Workforce Management Software Market by type is led by integrated payroll and workforce management suites, which account for approximately 46% of total adoption. These platforms consolidate payroll processing, time and attendance, compliance, and analytics into a unified system, reducing data silos and improving operational visibility. Cloud-based payroll-only solutions represent around 28%, primarily adopted by SMEs seeking simplified compliance and cost efficiency. However, AI-enabled workforce analytics modules are the fastest-growing type, expanding at an estimated CAGR of 11.2%, driven by demand for predictive labor planning, overtime optimization, and real-time performance insights. Standalone time and attendance systems, along with benefits administration tools, collectively contribute about 26%, maintaining relevance in niche deployments and legacy environments.

By application, payroll processing remains the leading segment, accounting for nearly 39% of overall usage, as accurate salary calculation, tax filing, and statutory reporting are mission-critical across all industries. Workforce scheduling and time management follow with approximately 27%, reflecting growing demand from retail, healthcare, and manufacturing sectors operating shift-based labor models. Employee self-service and benefits administration applications are growing fastest, with an estimated CAGR of 10.6%, supported by rising employee expectations for mobile access and transparency. Other applications, including compliance reporting and workforce analytics, together represent about 34%, increasingly embedded as standard features within broader platforms.

Large enterprises are the dominant end-users in the Payroll and Workforce Management Software Market, accounting for approximately 52% of total adoption due to complex workforce structures and multi-jurisdiction compliance needs. SMEs represent around 31% and are the fastest-growing end-user group, expanding at an estimated CAGR of 12.1%, driven by cloud-based subscription models and simplified implementation. Among industries, BFSI and IT services show adoption rates exceeding 68%, while healthcare and retail follow closely due to scheduling intensity and compliance requirements. Manufacturing and logistics contribute steadily, together accounting for nearly 17% of usage.

North America accounted for the largest market share at 38.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

North America continues to lead due to high enterprise software penetration, with over 78% of large organizations using integrated payroll and workforce platforms. Europe followed with a 27.4% share, driven by regulatory complexity across more than 40 labor jurisdictions. Asia-Pacific represented 24.1%, supported by a workforce base exceeding 2.3 billion employees and rapid SME digitization. South America and the Middle East & Africa jointly accounted for 9.9%, where adoption is rising due to formalization of labor markets, digital tax frameworks, and cloud infrastructure expansion. Cross-border payroll demand increased by 34% globally in 2024, reflecting workforce globalization and reinforcing regional demand variations.

How are enterprise-scale digital payroll transformations reshaping operational efficiency?

North America holds approximately 38.6% of the Payroll and Workforce Management Software Market, supported by widespread adoption across healthcare, BFSI, IT services, and retail. Over 72% of enterprises with more than 1,000 employees use cloud-native payroll systems. Regulatory developments around wage transparency and data protection have accelerated upgrades to AI-enabled compliance tools. Digital transformation trends include real-time payroll analytics and predictive workforce scheduling, now used by nearly 46% of large employers. A prominent regional player has expanded AI-driven payroll compliance engines to support multi-state tax automation, reducing payroll audit workloads by over 30%. Consumer behavior shows higher adoption in healthcare and finance, where payroll accuracy and compliance are mission-critical.

Why is regulatory complexity accelerating intelligent payroll adoption?

Europe accounts for roughly 27.4% of the Payroll and Workforce Management Software Market, led by Germany, the UK, and France, which together represent over 60% of regional demand. Strict labor laws, GDPR compliance, and multi-country payroll requirements drive enterprise adoption. More than 68% of multinational firms operating in Europe rely on automated statutory reporting tools. Sustainability initiatives and digital payslip mandates have reduced paper payroll usage by approximately 29%. Regional vendors are focusing on explainable AI payroll engines to meet transparency requirements. Consumer behavior reflects strong demand for compliance-driven, auditable payroll systems rather than purely cost-focused solutions.

How is workforce scale combined with digital acceleration shaping adoption patterns?

Asia-Pacific ranks as the fastest-expanding region by growth rate and contributes 24.1% of the global Payroll and Workforce Management Software Market. China, India, and Japan collectively manage over 55% of the regional workforce volume. SME cloud payroll adoption exceeds 61%, driven by mobile-first platforms and subscription pricing. Manufacturing, IT services, and e-commerce are major demand drivers as companies scale rapidly. Regional technology hubs are integrating AI payroll chatbots and mobile attendance tools. A leading local provider recently expanded multi-language payroll support across Southeast Asia, improving onboarding efficiency by 34%. Consumer behavior shows strong reliance on mobile apps and automation to manage large, distributed teams.

How is workforce formalization influencing digital payroll demand?

South America represents approximately 6.2% of the Payroll and Workforce Management Software Market, with Brazil and Argentina accounting for nearly 70% of regional usage. Infrastructure, energy, and manufacturing sectors are key adopters as governments strengthen labor compliance enforcement. Digital tax filing mandates have increased payroll software adoption among mid-sized enterprises by 41%. Trade agreements and cloud adoption policies support regional software deployment. A regional payroll provider has introduced automated tax reporting aligned with national labor systems, reducing filing delays by 28%. Consumer behavior emphasizes localization, language support, and regulatory alignment.

Why are modernization and workforce nationalization driving adoption?

The Middle East & Africa account for around 3.7% of the Payroll and Workforce Management Software Market, with demand led by UAE, Saudi Arabia, and South Africa. Oil & gas, construction, and government sectors dominate adoption due to large expatriate workforces. Digital government initiatives have increased payroll system usage by over 36% in public-sector entities. Technological modernization includes cloud migration and biometric attendance integration. A regional software firm has partnered with government agencies to deploy centralized payroll platforms covering over 500,000 workers. Consumer behavior varies, with higher demand for multi-currency, multilingual payroll capabilities.

United States – 32.1% market share: High enterprise software adoption, advanced compliance requirements, and large-scale workforce digitization drive dominance in the Payroll and Workforce Management Software Market.

Germany – 9.4% market share: Strong regulatory frameworks, high industrial employment, and demand for compliant, auditable payroll systems support leadership within the Payroll and Workforce Management Software Market.

The Payroll and Workforce Management Software market exhibits a moderately consolidated competitive structure, with global leaders coexisting alongside a large base of regional and niche providers. More than 120 active vendors operate globally, addressing varying enterprise sizes, regulatory environments, and industry-specific requirements. The top five companies collectively account for approximately 55–58% of total market activity, reflecting strong brand equity, global delivery capabilities, and deep compliance expertise, while the remaining share is distributed among mid-tier SaaS vendors and localized payroll specialists.

Competition is primarily driven by product breadth, regulatory coverage, cloud scalability, and AI-enabled automation depth. Over 64% of leading vendors now offer unified HCM platforms that integrate payroll, workforce scheduling, compliance, analytics, and employee self-service. Strategic initiatives remain intense: between 2023 and 2024, more than 35 partnerships and integrations were announced globally to enhance ERP interoperability, tax automation, and cross-border payroll coverage. Mergers and acquisitions are focused on expanding geographic compliance libraries and acquiring AI-driven payroll intelligence capabilities.

Innovation trends shaping competition include machine-learning-based payroll anomaly detection, now deployed by over 48% of top-tier vendors, and real-time statutory update engines, reducing compliance lag by up to 30%. The market also shows increasing investment in mobile-first payroll experiences and API-driven ecosystems, enabling faster deployment across distributed workforces. Overall, competitive intensity is expected to remain high as vendors race to differentiate through automation depth, global compliance accuracy, and platform extensibility.

ADP

Workday

SAP

Oracle

UKG

Paychex

Ceridian

Dayforce

Paycom

Rippling

Technology evolution is a primary force shaping the Payroll and Workforce Management Software Market, with enterprises increasingly adopting intelligent, cloud-native, and automation-centric platforms. Cloud deployment has become the dominant architecture, with more than 74% of new payroll implementations delivered through multi-tenant SaaS models due to scalability, rapid updates, and reduced infrastructure dependency. These platforms support real-time payroll processing for workforces exceeding 100,000 employees across multiple jurisdictions, enabling centralized governance with localized compliance.

Artificial intelligence and machine learning are now embedded across payroll workflows. Approximately 49% of enterprise-grade payroll platforms use AI-driven validation engines to detect anomalies in wage calculations, tax deductions, and overtime rules, reducing payroll discrepancies by up to 43%. Predictive analytics tools leverage historical workforce data to forecast absenteeism, overtime trends, and labor demand, improving workforce planning accuracy by nearly 31%. Natural language processing is increasingly applied to employee self-service portals, with AI chatbots resolving over 60% of payroll-related queries without HR intervention.

API-driven architectures are transforming system interoperability. More than 68% of organizations integrate payroll software with ERP, accounting, and time-tracking systems through standardized APIs, reducing data reconciliation workloads by 36%. Blockchain-based payroll security is gaining early traction, particularly for cross-border payroll, enhancing transaction traceability and reducing payment settlement times by 25%. Additionally, mobile-first payroll applications now support biometric attendance and geo-fencing, adopted by over 45% of shift-based enterprises, improving time capture accuracy and regulatory compliance. Together, these technologies are redefining payroll operations as strategic, data-driven workforce management functions.

• In August 2024, Workday announced Global Payroll Connect, a unified solution enabling organizations to manage payroll, HR, and workforce functions through seamless integrations with existing payroll providers. The platform aims to reduce implementation costs by up to 50% and offers a single access point for global payroll status and workforce insights, improving visibility and compliance across multi-country operations. (Newsroom | Workday)

• In Q3 2024, Paylocity expanded its global payroll footprint through the acquisition of Avionté, enhancing payroll capabilities for staffing and seasonal workforce management and enabling broader functionality for clients handling contingent labor.

• In 2024, UKG introduced UKG One View, a real-time payroll data synchronization and AI validation solution. It consolidates payroll information from disparate systems into a unified global view, enabling instant reporting and improved accuracy for multinational payroll operations.

• In Q1 2025, Ceridian launched Dayforce Assist, an AI-powered automation tool integrated into its cloud payroll platform. The feature automates exception handling, payroll corrections, and regulatory reporting in real time, enhancing accuracy and reducing manual intervention for complex payroll environments.

The Payroll and Workforce Management Software Market Report provides a comprehensive analysis of the systems and solutions that enable organizations to manage payroll processing, workforce scheduling, time and attendance, benefits administration, and compliance reporting. It covers an extensive set of product segments, including cloud-native payroll platforms, integrated workforce suites, AI-enabled analytics modules, and mobile self-service applications tailored to enterprise and SME needs. The report examines deployment models such as SaaS, on-premise, and hybrid systems, and evaluates the relevance of emerging technologies like AI, machine learning, API-driven interoperability, blockchain security, and real-time compliance engines in shaping market capabilities and adoption patterns.

Geographically, the study analyzes region-specific insights for North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing workforce digitization levels, regulatory influences, enterprise adoption behavior, and local innovation hubs. It segments the market by application areas such as core payroll processing, workforce scheduling, compliance automation, and employee self-service, outlining how each supports organizational efficiency and strategic HR decision-making. The report also includes industry focus areas—with specific attention to sectors like BFSI, healthcare, retail, manufacturing, IT services, and government—highlighting sector-specific payroll operational challenges and solution requirements.

In addition to traditional market assessments, the report addresses niche segments such as gig economy payroll integration, cross-border payroll orchestration, and contingent workforce management tools. It presents quantitative and qualitative insights into vendor competitiveness, technological differentiators, and strategic initiatives including partnerships, product enhancements, and ecosystem expansions. Designed for business leaders, HR technology executives, and investment professionals, the report offers actionable intelligence to evaluate current capabilities, forecast technology trajectories, and inform strategic investment and implementation decisions across the global payroll and workforce management landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 8831.07 Million |

Market Revenue in 2032 | USD 14615.39 Million |

CAGR (2025 - 2032) | 6.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | ADP, Workday, SAP, Oracle, UKG, Paychex, Ceridian, Dayforce, Paycom, Rippling |

Customization & Pricing | Available on Request (10% Customization is Free) |