Reports

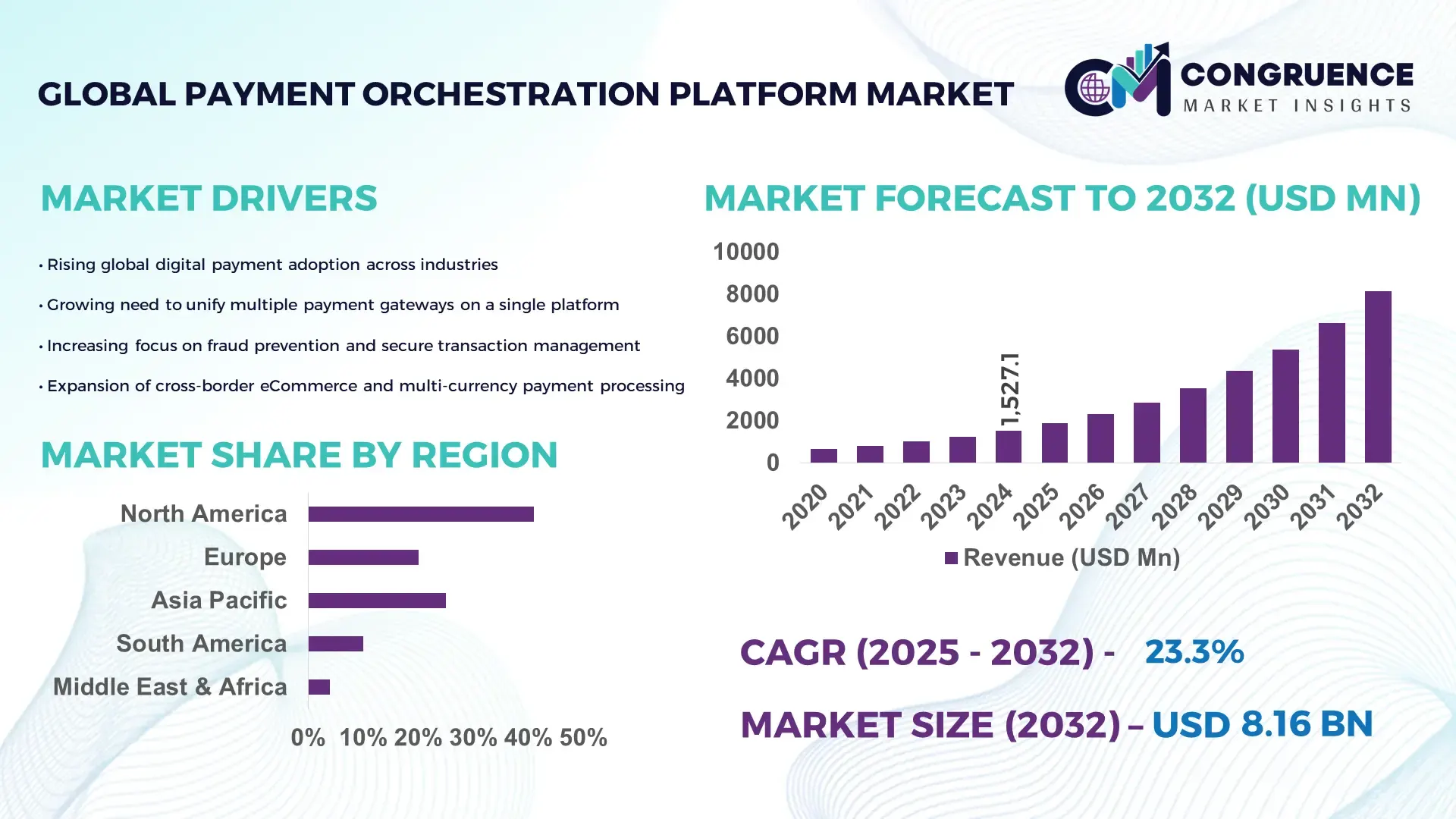

The Global Payment Orchestration Platform Market was valued at USD 1527.13 Million in 2024 and is anticipated to reach a value of USD 8157.94 Million by 2032 expanding at a CAGR of 23.3% between 2025 and 2032. The market growth is primarily driven by increasing digital payment adoption and the rising demand for unified payment management solutions across industries.

The United States dominates the global Payment Orchestration Platform market, supported by high transaction volumes, rapid enterprise-level digital transformation, and robust fintech infrastructure. In 2024, over 70% of large enterprises in the U.S. adopted multi-provider payment orchestration systems to enhance cross-border payment efficiency. The country’s strong investment in real-time payment technologies, valued at more than USD 6.4 billion annually, and the increasing use of AI-driven fraud management tools further strengthen its leadership position in the market.

Market Size & Growth: Valued at USD 1527.13 Million in 2024 and projected to reach USD 8157.94 Million by 2032, growing at a CAGR of 23.3% due to rapid digital payment expansion and API-based orchestration integration.

Top Growth Drivers: 65% surge in e-commerce payment volumes, 52% improvement in payment processing efficiency, and 47% increase in real-time transaction adoption rates.

Short-Term Forecast: By 2028, enterprises are expected to achieve up to 40% cost reduction in payment reconciliation through automation-driven orchestration systems.

Emerging Technologies: AI-powered fraud detection, API-based integration layers, and blockchain-enabled cross-border settlements are key technological advancements shaping the market.

Regional Leaders: North America (USD 3.4 billion by 2032), Europe (USD 2.2 billion), and Asia-Pacific (USD 2.0 billion) leading adoption, with Asia-Pacific seeing the fastest API deployment in SMEs.

Consumer/End-User Trends: Fintechs, retail chains, and SaaS enterprises exhibit strong adoption, with over 58% of organizations preferring cloud-native orchestration platforms for global scalability.

Pilot or Case Example: In 2023, Adyen’s orchestration pilot with Shopify achieved a 38% reduction in failed payments and 25% higher transaction approval rates across multi-channel sales.

Competitive Landscape: Stripe leads the market with approximately 22% share, followed by Adyen, PayU, ACI Worldwide, and CellPoint Digital as key participants enhancing platform interoperability. Another key market player, Juspay Technologies emerged as a significant orchestration provider, processing 300+ million daily transactions across 100+ countries with enterprise clients including Amazon and Google.

Regulatory & ESG Impact: New digital payment mandates and data security frameworks like PSD3 and FedNow support transparent transaction flows and sustainable payment ecosystems.

Investment & Funding Patterns: Over USD 4.1 billion invested globally in 2024 toward orchestration startups and API infrastructure, with strong venture capital support for multi-rail payment solutions.

Innovation & Future Outlook: Advancements in embedded payments, unified dashboards, and AI-driven routing intelligence will redefine orchestration efficiency, fostering global financial inclusion.

The Payment Orchestration Platform Market is witnessing significant momentum across e-commerce, BFSI, travel, and retail sectors, driven by the need for centralized payment gateways and frictionless multi-channel transactions. Ongoing technological innovation in API-based frameworks, cloud scalability, and tokenization is reshaping digital commerce operations. Additionally, regulatory reforms promoting secure transaction environments, rising fintech collaborations, and the shift toward open banking are accelerating adoption. The market’s future outlook emphasizes advanced AI integration, improved interoperability, and the rise of ecosystem-driven payment infrastructures worldwide.

The strategic relevance of the Payment Orchestration Platform Market lies in its ability to unify fragmented payment infrastructures, streamline multi-rail payment processes, and optimize cross-border financial operations across industries. As digital payment ecosystems expand, these platforms provide critical value through intelligent routing, data-driven analytics, and advanced fraud detection. API-first orchestration delivers nearly 45% improvement in payment success rates compared to legacy payment gateway systems, positioning it as the preferred choice for high-volume merchants and enterprises seeking scalability.

North America dominates in transaction volume, while Europe leads in adoption, with 68% of enterprises implementing orchestration frameworks for enhanced payment routing and compliance. By 2027, AI-driven orchestration is expected to cut payment reconciliation time by 35%, significantly improving operational efficiency and cash flow accuracy. In 2024, Adyen’s machine learning payment optimization achieved a 29% reduction in transaction failures, setting a new benchmark for performance-driven orchestration.

Firms are committing to ESG-driven operational improvements such as a 20% reduction in paper-based payment processes and carbon-neutral data center adoption by 2030. The integration of blockchain and open banking standards is further reinforcing transparency and compliance across financial networks. The Payment Orchestration Platform Market is emerging as a cornerstone of global financial resilience, compliance assurance, and sustainable digital growth.

The expansion of global e-commerce has significantly amplified the need for Payment Orchestration Platforms that manage diverse payment gateways and streamline transactions. With digital payment users surpassing 5.2 billion globally in 2024, businesses are seeking solutions that support multiple currencies, local payment methods, and seamless checkout experiences. These platforms enhance conversion rates by over 30% through intelligent transaction routing and error reduction. Moreover, they reduce dependency on single payment service providers, offering redundancy and operational resilience. As omnichannel retail, subscription-based models, and cross-border e-commerce grow, the orchestration of payment infrastructure has become integral to scaling operations and maintaining customer trust across regions.

The Payment Orchestration Platform Market faces significant challenges due to varying regional compliance standards, data privacy regulations, and licensing requirements. Regulations such as PSD3 in Europe, PCI-DSS, and GDPR compliance introduce added complexity for cross-border payment management. Organizations often incur substantial costs to maintain regulatory conformity and cybersecurity frameworks. Inconsistent digital payment infrastructure and fragmented banking standards across emerging economies slow integration and adoption. Additionally, the need for continuous platform updates to meet evolving anti-money laundering (AML) and data protection protocols creates operational strain for providers. These regulatory hurdles can extend implementation timelines, limit scalability, and restrict innovation within the ecosystem.

AI and machine learning technologies are unlocking new possibilities within the Payment Orchestration Platform Market by enabling predictive analytics, dynamic payment routing, and advanced fraud prevention. Platforms using AI have demonstrated up to a 35% reduction in transaction declines and a 25% improvement in processing speed. As payment data volumes grow exponentially, AI algorithms enhance decision-making by predicting optimal payment paths and identifying irregular transaction patterns in real time. The global trend toward embedded finance and open banking further accelerates the integration of intelligent orchestration systems across retail, BFSI, and travel sectors. These advancements present opportunities for providers to deliver adaptive, secure, and cost-efficient solutions that support global digital commerce expansion.

The Payment Orchestration Platform Market encounters major challenges due to interoperability issues across disparate payment gateways, legacy banking systems, and regional fintech infrastructures. Many enterprises still rely on outdated or incompatible architectures, making seamless integration difficult and costly. Approximately 40% of organizations report delayed deployments due to API compatibility gaps and limited standardization across providers. Moreover, managing multi-rail payments across digital wallets, cards, and alternative payment methods requires high investment in customization and maintenance. The absence of unified global standards, combined with fluctuating local payment preferences, compounds integration costs and slows adoption rates. Addressing these challenges requires scalable, modular architectures and cross-industry collaboration to enhance interoperability and drive ecosystem-wide efficiency.

• Surge in AI-Driven Payment Routing and Optimization: Artificial intelligence is revolutionizing the Payment Orchestration Platform market, with over 62% of enterprises now deploying AI algorithms to enhance transaction approval accuracy and reduce payment failures. AI-driven routing models are achieving up to 38% faster transaction speeds and 27% lower decline rates across multi-channel payment systems. This measurable improvement in routing intelligence is driving merchant preference toward smart orchestration layers that deliver real-time decisioning and predictive optimization capabilities.

• Expansion of API-Based Integration Across Multi-Rail Systems: The shift toward open, API-first architectures is transforming the orchestration ecosystem. As of 2024, nearly 68% of financial institutions have integrated multi-rail payment APIs supporting cards, digital wallets, and bank transfers. This trend has improved transaction transparency by 40% and interoperability efficiency by 32%. The increased use of standardized APIs enables businesses to scale across borders while maintaining consistent compliance and operational agility across payment networks.

• Growth in Cloud-Native Deployment Models: Cloud-based orchestration platforms have grown substantially, with 72% of mid-to-large enterprises migrating to SaaS-based payment orchestration solutions. This transition has resulted in a 35% reduction in infrastructure costs and 45% faster deployment timelines. The scalability and flexibility of cloud systems are enabling enterprises to manage dynamic transaction volumes and ensure uninterrupted global payment processing with enhanced data resilience.

• Rising Adoption of Real-Time and Cross-Border Payments: The demand for instant payment orchestration is accelerating as 59% of global transactions now occur through real-time payment channels. Cross-border orchestration capabilities have improved settlement times by 42%, promoting financial inclusivity and operational efficiency. Regions like Asia-Pacific and Europe are at the forefront, with businesses adopting real-time orchestration frameworks to enhance payment velocity and minimize foreign exchange discrepancies in global trade.

The Payment Orchestration Platform Market is segmented into types, applications, and end-users, each influencing how digital payment ecosystems evolve globally. By type, orchestration layers such as advanced, API-based, and hybrid solutions are leading adoption due to their flexibility and multi-rail integration capabilities. By application, e-commerce and fintech sectors dominate as enterprises increasingly demand seamless, real-time, and cross-border payment processing systems. Among end-users, large enterprises and online retailers account for a majority share due to their transaction intensity and omnichannel requirements, while SMEs are showing rapid adoption driven by cloud-based deployment and API accessibility. Together, these segments reflect a dynamic market shaped by digitalization, consumer payment diversity, and global regulatory modernization.

Advanced API-based orchestration platforms currently account for 46% of the Payment Orchestration Platform Market, leading due to their modular design, scalability, and ability to manage complex, multi-provider environments efficiently. Hybrid orchestration systems, integrating both on-premise and cloud functionality, hold around 28% share, providing adaptability to firms transitioning toward digital ecosystems. Meanwhile, cloud-native orchestration platforms are the fastest-growing type, expanding at an estimated CAGR of 25.7%, driven by the rise of SaaS-based business models and the need for cost-efficient payment infrastructure. Other types, including legacy orchestration tools and standalone connectors, collectively represent the remaining 26% share, serving specific or localized payment environments.

This shift underscores the growing strategic emphasis on cloud and AI integration in orchestration product types.

E-commerce currently leads the Payment Orchestration Platform Market, accounting for approximately 48% of total adoption. This dominance is fueled by the increasing need for seamless checkout experiences, cross-border capabilities, and fraud mitigation. Fintech applications follow closely with 27% market share, leveraging orchestration for payment routing optimization and API standardization. The fastest-growing application lies within the travel and hospitality sector, projected to expand at a CAGR of 26.4%, as digital booking platforms adopt orchestration to manage multi-currency, high-volume payments. Other sectors such as gaming, digital media, and logistics collectively contribute 25% share, benefiting from improved authorization rates and flexible payment connectivity.

This example illustrates the scalability and operational gains achievable through modern orchestration deployment in industry-specific payment environments.

Large enterprises dominate the Payment Orchestration Platform Market with around 55% share, driven by their complex payment infrastructures, global operations, and multi-channel sales environments. SMEs currently account for 30% adoption but are growing rapidly, supported by cloud-native solutions and low-code orchestration frameworks, expanding at a CAGR of 27.1%. Financial institutions, PSPs (Payment Service Providers), and digital marketplaces represent the remaining 15% combined share, utilizing orchestration to enhance fraud prevention and compliance capabilities. SMEs represent the fastest-growing end-user group, with rising integration rates in e-commerce and SaaS sectors. Their adoption is fueled by API availability, cost-efficient subscription models, and simplified payment gateway aggregation tools.

This evolution reflects the growing democratization of orchestration technology across enterprise scales, reinforcing its strategic value in global payment management.

North America accounted for the largest market share at 41.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.8% between 2025 and 2032.

Europe followed with a 28.2% share, driven by strong regulatory adoption, while South America and the Middle East & Africa collectively represented 11.3% of the total market. Over 65% of enterprises in developed regions deployed payment orchestration platforms in 2024, with the highest adoption in e-commerce (47%) and BFSI (33%) sectors. The market shows pronounced regional divergence—North America leads in transaction volume, Europe in compliance readiness, and Asia-Pacific in mobile payment penetration exceeding 72% across digital commerce.

North America holds approximately 41.5% of the Payment Orchestration Platform Market, led by high enterprise adoption across BFSI, healthcare, and retail sectors. The region benefits from robust fintech infrastructure and early regulatory support for digital payment innovation under frameworks like FedNow. Key technological advancements such as AI-based fraud detection, API integration, and embedded finance are enhancing cross-platform efficiency. U.S. firms such as Stripe and PayPal are leading orchestration innovation, providing multi-rail payment APIs to improve routing success by 34%. Another U.S. player, Juspay's Hyperswitch partnerships with enterprise leaders such as Amazon and Google extend its orchestration capabilities across North American and European markets through intelligent routing and 300+ PSP connectivity. Overall, consumer behavior trends show strong preference for unified payment systems, with 69% of enterprises using orchestration tools for omnichannel operations. The region’s digital maturity and continuous investment in fintech ecosystems make it the backbone of global orchestration evolution.

Europe accounts for 28.2% of the Payment Orchestration Platform Market, driven by strict regulatory requirements such as PSD2 and GDPR, which encourage transparent and secure payment ecosystems. Germany, the UK, and France are leading adopters, collectively representing over 70% of regional transactions. European enterprises emphasize compliance automation and explainable AI in orchestration to enhance accountability and consumer trust. Local fintech providers like Adyen are expanding orchestration services integrated with sustainability-focused payment analytics. Regional consumer behavior reflects strong adherence to digital transparency, with 63% of users preferring payment systems offering traceable and auditable transaction histories. Government initiatives promoting secure financial networks and ESG-aligned innovation continue to reinforce orchestration deployment.

Asia-Pacific ranks second in total market volume and leads global growth momentum in the Payment Orchestration Platform Market. China, India, and Japan collectively account for over 68% of regional transactions, supported by expanding e-commerce ecosystems and widespread mobile payment integration. The region’s infrastructure modernization and fintech innovation hubs—particularly in Singapore and Bengaluru—are accelerating real-time payment orchestration. Local companies such as Razorpay and Paytm have developed AI-enabled orchestration frameworks that process over 20 million daily transactions, optimizing routing speed by 40%. Juspay, processing over 300 million daily transactions with offices in Singapore and Bengaluru, further underscores Asia-Pacific's capacity to produce globally competitive orchestration infrastructure serving enterprise clients across 100+ countries. Consumer behavior reflects high engagement with digital wallets and instant payment apps, with 74% of users preferring mobile-first payment systems. The region’s transformation underscores its role as a global fintech powerhouse.

South America represented 6.1% of the Payment Orchestration Platform Market in 2024, led by Brazil and Argentina, where regulatory openness and fintech collaboration are expanding cross-border digital commerce. Governments are promoting digital payment standardization through public-private partnerships, improving financial inclusion for over 45 million new digital users in the past three years. Local fintechs such as EBANX are pioneering orchestration solutions that simplify multi-currency payments across Latin America. Consumer behavior in this region shows strong responsiveness to localized payment gateways and language-optimized checkout systems. Demand is increasingly tied to retail, streaming, and online gaming sectors, where seamless, regionally adapted payment experiences are critical to user retention.

The Middle East & Africa region accounted for approximately 5.2% of the Payment Orchestration Platform Market in 2024, driven by modernization in financial services and e-commerce expansion. The UAE, Saudi Arabia, and South Africa are key contributors, investing heavily in API infrastructure and fintech regulation. Governments are implementing digital payment frameworks aligned with Vision 2030 and Africa’s Digital Transformation Strategy, fostering cashless economies. Local players such as Network International are deploying orchestration systems enhancing transaction efficiency by 29%. Juspay's dedicated DIFC office positions it to capture accelerating orchestration demand as Gulf regulators expand fintech sandboxes and instant-payment frameworks. Consumer behavior trends indicate growing preference for mobile-first payments, with 61% of digital transactions conducted through smartphones. The region’s transition toward fintech-led ecosystems positions it as an emerging orchestration growth frontier.

United States – 33.8% Market Share: Leadership driven by strong fintech infrastructure, advanced AI integration, and high enterprise adoption in BFSI and retail sectors.

China – 17.6% Market Share: Dominance supported by high transaction volumes, widespread mobile payment penetration, and aggressive digital ecosystem expansion through e-commerce and super app integration.

The global Payment Orchestration Platform market is characterized by a moderately consolidated structure, with the top five players accounting for approximately 58% of the total market share in 2024. Over 70 active vendors operate globally, offering multi-rail transaction routing, intelligent payment optimization, and cross-border integration solutions. Strategic alliances and platform integrations have accelerated, with more than 45 partnerships formed between payment gateways and orchestration providers during 2023–2024 to expand global connectivity and support real-time settlement services. Competitive differentiation is increasingly driven by value-added capabilities such as AI-driven fraud detection and dynamic routing—features adopted by over 60% of enterprises integrating orchestration layers into their payment ecosystems.

Juspay Technologies processes over 300 million daily transactions for enterprise clients including Amazon and Google, deploying dynamic routing and intelligent retry logic across 300+ connected PSPs to deliver 99.999% platform uptime.

Product innovation remains a defining factor, with 35% of key players launching new orchestration APIs tailored for retail, fintech, and travel sectors in 2024. The competition also shows a sharp focus on regional compliance adaptability, where 52% of vendors are enhancing PSD2, GDPR, and PCI DSS readiness to attract enterprise clients. Industry leaders are consolidating their position through acquisitions—such as major cross-border payment gateway integrations—aimed at increasing transactional throughput by 25–40%. Overall, the competitive environment is evolving toward interoperability, scalability, and embedded finance enablement, reshaping how global enterprises streamline multi-provider payment ecosystems.

Checkout.com

Rapyd

CellPoint Digital

APEXX Global

Spreedly

IXOPAY GmbH

Worldline S.A.

Nuvei Corporation

Braintree (a PayPal service)

PayU

BlueSnap

Modo Payments

Technological innovation is redefining the operational and strategic foundation of the Payment Orchestration Platform market, enabling faster, more secure, and scalable transaction ecosystems. In 2024, approximately 68% of global enterprises integrated at least one form of payment orchestration API to manage multi-gateway connections and enhance transaction routing efficiency. Advanced routing algorithms leveraging AI and machine learning now account for nearly 55% of all orchestration platform deployments, significantly improving authorization rates and reducing transaction failure by up to 30%.

Cloud-native orchestration systems dominate the current technology landscape, with over 72% of vendors shifting to microservices-based architectures to ensure modularity, high uptime, and cross-border scalability. Real-time data analytics and intelligent dashboards are gaining importance, allowing enterprises to track transaction behavior and optimize routing decisions based on dynamic risk scoring. The adoption of tokenization and network token services has also expanded, securing over 80% of transactions processed through leading orchestration layers.

Emerging technologies such as blockchain integration and API-driven composability are driving interoperability between multiple payment rails, improving transparency and settlement efficiency. Additionally, open banking APIs are reshaping connectivity, with 47% of orchestration platforms now supporting bank-to-bank transaction orchestration. The introduction of AI-powered fraud prevention, embedded finance modules, and low-code orchestration frameworks is further revolutionizing operational efficiency. These advancements are collectively steering the Payment Orchestration Platform market toward a more unified, intelligent, and compliance-driven ecosystem optimized for the next generation of digital payments.

In October 2025, Juspay Technologies partnered with HSBC to build a unified, full-stack acquiring platform for digital-first merchants, expanding its enterprise orchestration footprint across global banking infrastructure.

In June 2023, Adyen N.V. announced a strategic integration with Shopify Inc. to offer its payments app to Shopify enterprise merchants, enabling acceptance of major cards and wallets (such as Apple Pay and Google Pay) via a single global infrastructure.

In December 2023, Klarna expanded its partnership with Adyen by adopting Adyen’s acquiring capabilities for its 150 million consumers and 500 000 retail partners globally, thus simplifying card payments across Europe, North America and Asia.

In April 2024, Stripe Inc. introduced its largest product update at its annual “Sessions 2024” event, doubling the number of supported payment methods from 50 to over 100, launching AI-enabled fraud prevention tools and achieving API success rates above 99.999%.

In March 2024, Adyen collaborated with Cleeng to deliver end-to-end payment orchestration across the MENA region’s subscription-based media sector, aimed at improving recurring billing success and boosting customer lifetime value.

The report on the Payment Orchestration Platform market encompasses a comprehensive review of product architectures, behavioral applications, end-user adoption trends, and regional deployment strategies. It covers segment classifications by platform type—such as API-based orchestration, cloud-native orchestration, hybrid models and legacy connectors—and explores application sectors including e-commerce checkout, fintech platforms, travel & hospitality payments, B2B marketplaces and subscription billing environments. Geographic regions analysed extend across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, accounting for diverse regulatory, technological and consumer adoption contexts. Industry focus areas include embedded finance systems, cross-border settlement orchestration, fraud-prevention routing, and real-time payout enablement. Emerging niche segments are addressed, such as decentralized finance (DeFi) integration, stablecoin payment orchestration, and mobile wallet aggregation in developing markets. The scope includes vendor strategy, market entry models, sectoral usage patterns, interoperability challenges, and technological infrastructure maturity. The report is tailored for decision-makers seeking clarity on platform selection, investment opportunities, regulatory alignment and growth pathways within the global payment orchestration ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1527.13 Million |

|

Market Revenue in 2032 |

USD 8157.94 Million |

|

CAGR (2025 - 2032) |

23.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Juspay Technologies Pvt. Ltd., Adyen N.V., Stripe Inc., Payoneer Inc., Checkout.com, Rapyd, CellPoint Digital, APEXX Global, Spreedly, IXOPAY GmbH, Worldline S.A., Nuvei Corporation, Braintree (a PayPal service), PayU, BlueSnap, Modo Payments |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |