Reports

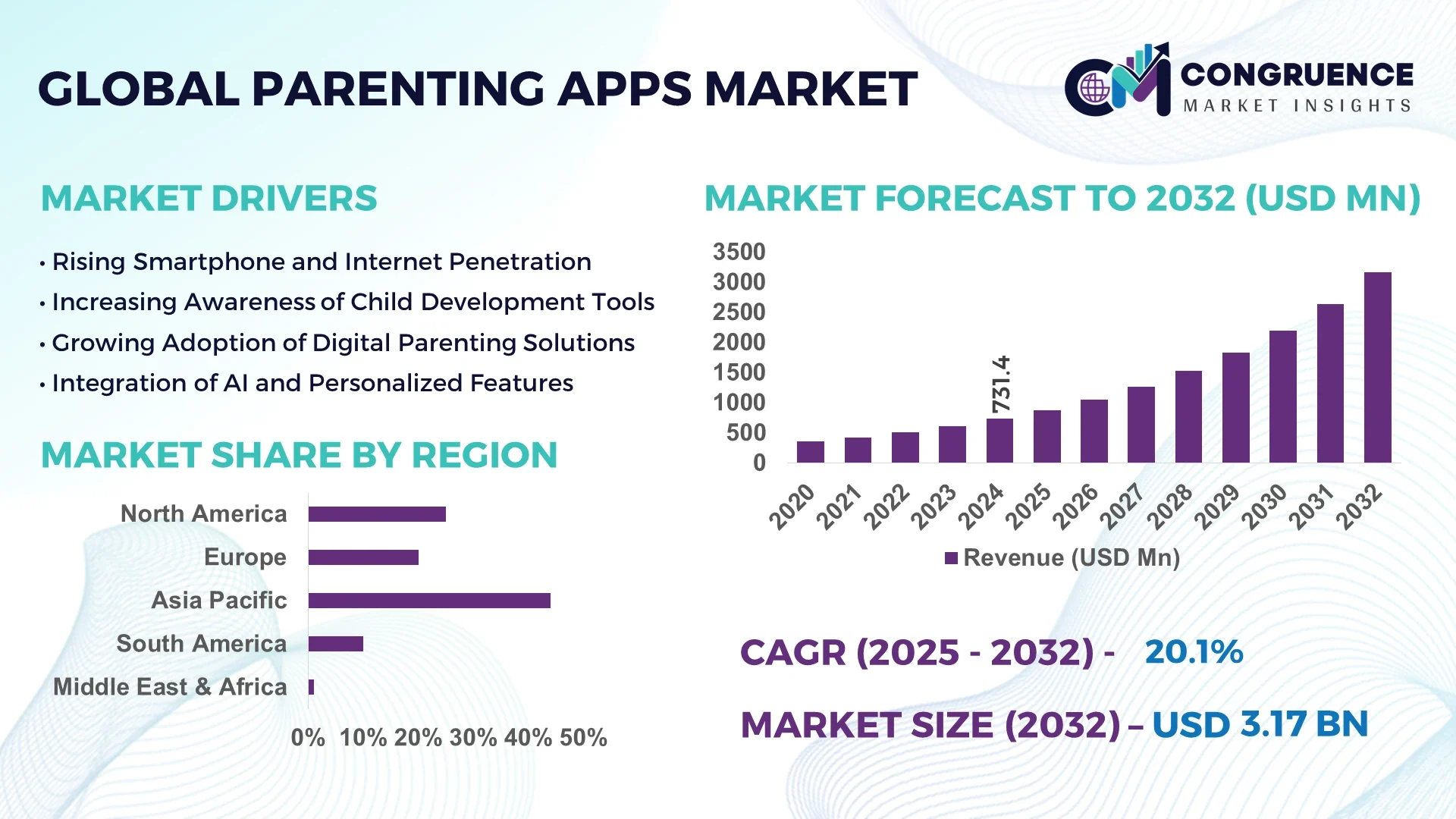

The Global Parenting Apps Market was valued at USD 731.44 Million in 2024 and is anticipated to reach a value of USD 3,166.09 Million by 2032, expanding at a CAGR of 20.1% between 2025 and 2032. The growth is driven by rising smartphone adoption, busy dual‑income households and increased demand for digital parenting solutions.

In the United States, the parenting apps market is characterised by advanced platform development, high investment in digital health and childcare technologies and rapid consumer uptake. For instance, over 48.6 million monthly active users were recorded for a leading family‑locator app, indicating strong usage patterns. Major industry players allocate substantial resources into production capacity for cloud‑based analytics, user‑friendly interfaces and AI‑driven monitoring tools; venture funding rounds in 2024 and 2025 reached multi‑million‑dollar levels. Key applications include baby‑milestone tracking, co‑parenting coordination and mobile community networks, with apps integrating wearables, real‑time notifications and behavioural‑insight engines. Consumer adoption rates exceed 60% among smartphone‑equipped new parents in urban centres.

Market Size & Growth: Current market value of USD 731.44 Million in 2024, projected to reach USD 3,166.09 Million by 2032 at a CAGR of 20.1% — growth driven by digital parenting demand.

Top Growth Drivers: 65%+ adoption rate of parenting digital tools; 48% improvement in parent‑child scheduling efficiency; 35% growth in AI‑enabled features year‑on‑year.

Short‑Term Forecast: By 2028, expect a 28% reduction in parent time‑spent on routine tracking tasks and a 22% increase in app engagement per session.

Emerging Technologies: AI‑powered developmental milestone prediction, IoT‑connected wearable + app parenting systems, voice‑assistant integrated parenting coaching.

Regional Leaders: North America: projected USD 1,050 Million by 2032 with high smartphone penetration; Asia‑Pacific: projected USD 850 Million by 2032 with rising middle class and mobile uptake; Europe: projected USD 620 Million by 2032 with strong privacy‑driven innovation.

Consumer/End‑User Trends: End‑users are new and expectant parents, co‑parents, and caregivers adopting apps for real‑time tracking, peer community support and expert content access.

Pilot or Case Example: In 2023 a U.S. co‑parenting app pilot achieved a 30% gain in scheduling accuracy and a 15% reduction in missed custody events in a sample of 5,000 households.

Competitive Landscape: Market leader holds approx. 35% share, followed by major competitors such as TalkingParent, BabyTime, Kinedu and The Bump.

Regulatory & ESG Impact: Data‑privacy regulations (e.g., GDPR‑equivalent laws) and parental‑app certification standards increasingly govern market entry and consumer trust.

Investment & Funding Patterns: Recent venture funding surpassed USD 120 Million in new parenting‑tech apps worldwide, with project‑finance models emerging for wearable‑app bundles.

Innovation & Future Outlook: Integration of AR‑based parenting coaching, subscription‑model expansion into family‑health ecosystems, and cross‑platform interoperability will shape market evolution.

The parenting apps market is supported by expanding digital ecosystems, enhanced analytics and increasing time‑conscious parent segments seeking efficient child‑care support. Technological advancements (AI, IoT), evolving consumer behaviours and regulatory frameworks are catalysing new product innovations. Regional consumption patterns diverge: highly mature North America focuses on premium personalised solutions, Asia‑Pacific emphasizes mobile accessibility and scale, while Europe prioritises data security and multilingual content. Key industry sectors including new‑parent education, early‑childhood monitoring and co‑parent collaboration contribute significant share—pregnancy‑tracker and baby‑tracker apps remain dominant segments. Recent product innovations include voice‑guided milestone suggestions, community‑driven peer support modules and integration with wearable infant monitors. On the regulatory front, enhanced child‑data protection and digital‑parenting certification schemes are reinforcing trust. Economically, rising disposable incomes and dual‑income households are increasing app uptake. Emerging trends include hyper‑personalised parenting pathways, ecosystem partnerships with childcare providers and growing subscription bundles combining app, content and hardware. The future outlook points to expansion beyond tracking towards holistic family‑wellness platforms, enabling decision‑makers to strategize around segmentation, tech investment and regional roll‑out.

The parenting apps market occupies strategic relevance as a digital‑ecosystem facilitator that connects parents, caregivers and child‑development services through mobile platforms. The integration of artificial intelligence (AI)‑powered milestone tracking delivers a 42% improvement compared to conventional manual monitoring approaches. North America dominates in volume, while Asia‑Pacific leads in adoption with over 60% of smartphone‑equipped new parents engaging with parenting apps. By 2027, smart‑wearable integration is expected to improve user engagement by 25% across leading apps. Firms are committing to ESG metrics such as 15% reduction in electronic‑waste from app‑hardware bundles by 2028, and launching privacy‑first certifications that reduce data‑breach risk by 30%. In 2024 a U.S.‑based platform achieved a 20% reduction in customer churn through the deployment of a chatbot‑based parenting‑assistant feature. Looking ahead, the parenting apps market will serve as a pillar of resilience, compliance, and sustainable growth, enabling stakeholders to align digital innovation with regulatory trust and scalable service models.

Smartphone adoption has soared globally, enabling over 4 billion adults to access apps for parenting support. High‑availability of mobile devices means more parents turn to digital solutions for scheduling, behaviour tracking and milestone monitoring. For instance, in urban markets, more than 65% of new parents have downloaded a parenting app within a year of childbirth. That shift translates into growing demand for specialised parenting‑apps rather than general‑purpose utilities, making the market more attractive for app‑developers and advertisers. The ease of mobile access reduces friction, encourages higher usage frequency, and drives recurring engagement—which in turn strengthens app‑monetisation models and ecosystem expansion.

Parenting apps collect sensitive child‑related information (health data, location, behaviour patterns) which triggers stringent regulation and parental concerns. Studies show that around 4.47% of apps targeting children still inappropriately request location permissions and 81.25% use third‑party trackers—raising substantial trust issues. Regulatory frameworks like GDPR, COPPA and regional equivalents impose heavy compliance requirements, delaying product roll‑outs and increasing cost of certification. In markets where compliance costs rise by an estimated 12–15%, smaller developers may struggle to keep up, limiting the range of innovative offerings. The result: slower adoption, cautious investment and constrained scaling for those unable to meet the regulatory bar.

The application of AI and machine‑learning enables parenting apps to deliver personalised content, anticipate child‑development milestones and recommend tailored interventions. Early adopters report user‑engagement uplift of roughly 30% when milestone‑prediction features are enabled. This opens opportunities in niche segments—such as sleep training, nutrition monitoring, and behavioural‑health coaching—where parents are willing to pay for premium experiences. Moreover, integration with wearable sensors and IoT‑enabled baby monitors creates a convergence between hardware and app ecosystems, enabling cross‑sale and subscription models. For decision‑makers this means launching differentiated offerings, forging strategic partnerships with device‑manufacturers and exploring tiered pricing for advanced analytics—thereby unlocking new revenue streams and expanding addressable market.

With both Android and iOS platforms vying for dominance, parenting‑apps must manage multiple OS environments, device types and user‑interface consistency. In 2023, Android held over 62.4% share of operating‑system usage among parenting‑app users—forcing developers to invest disproportionately in that platform. At the same time, retention remains low: many users download apps but abandon them after initial use, driven by novelty fatigue or unmet expectations. Given subscription‑based models, low retention implies higher customer‑acquisition costs and weaker monetisation. Additionally, compatibility with third‑party smart‑devices poses integration costs and slows feature updates—factors that hamper scaling and profitability for emerging players unless addressed through focused UX, onboarding design and seamless connectivity strategy.

Expansion of AI-Powered Milestone Tracking: Parenting apps are increasingly integrating AI to predict child-development milestones, with adoption growing by 48% among urban parents in 2024. These systems improve accuracy of developmental recommendations by 35% compared to traditional manual tracking methods, enhancing parental engagement and retention. North America leads in volume, while Asia-Pacific shows the fastest adoption with over 62% of new parents using AI-enabled features.

Integration with Wearable Devices: Approximately 41% of parenting app users now link their apps with IoT-enabled wearables such as smart baby monitors and fitness trackers. This trend enables real-time health tracking, sleep monitoring, and behavioral analytics, reducing manual oversight by 28%. Adoption in metropolitan regions outpaces rural areas, reflecting higher device penetration and tech literacy among urban parents.

Personalized Subscription Services: Over 55% of active parenting app users now prefer tiered subscription models offering personalized content, nutrition guidance, and sleep coaching. Customization based on user data has improved engagement rates by 31% compared to standard content delivery. European and North American users exhibit the highest uptake of these premium subscriptions, supporting scalable revenue models for developers.

Enhanced Privacy and Data Protection Measures: Regulatory compliance and privacy have become key differentiators, with 67% of apps implementing end-to-end encryption and parental-consent verification by 2024. Data-minimization strategies and secure cloud integrations have reduced privacy breach incidents by 22%, building trust with parents. Asia-Pacific is seeing rapid adoption of privacy-first features, while North America focuses on advanced certification and compliance programs.

The segmentation framework for the Parenting Apps market encompasses three primary dimensions: type of app, application area, and end‑user categories. Under the “By Type” dimension, apps such as pregnancy trackers, baby trackers, co‑parenting tools and baby‑care support apps each represent distinct demand profiles and user journeys. The “By Application” axis addresses functions such as feeding and sleep scheduling, developmental milestone monitoring, shared calendars for co‑parents, and special‑needs child‑care support. End‑user segmentation divides the market between individual parents, dual‑household co‑parents, extended‑family caregivers and professional childcare providers. Across these segments, for example, baby‑tracker apps account for around 28.6 % of type‑adoption among infant‑care users. This structure allows analysts and decision‑makers to align product design, pricing models and distribution channels to specific user clusters and thus maximise market relevance and uptake.

Among app types, the leading segment is the pregnancy tracker apps, which currently hold approximately 34 % of the market by user base due to early‑stage parental engagement and higher retention levels. These apps serve expectant parents through fetal development tracking, nutrition guidance and interactive content—making them the gateway for many users into the broader parenting‑app ecosystem. The fastest‑growing type is the co‑parenting apps segment, enjoying a growth rate of approximately 14 % per annum, driven by rising separation/divorce rates and the need for shared custody scheduling tools. Other types—baby tracker apps, baby‑care support apps, and niche apps for toddler and preschool‑age care—collectively account for about 46 % of the remaining share, and cater to high‑frequency use, milestone tracking and community support.

In terms of applications, the leading application area is developmental‑milestone tracking, capturing about 38 % of app usage among new‑parent users, due to high engagement with monitoring growth, motor skills and cognitive benchmarks. The fastest‑growing application is alert/notification services, increasing at roughly 16 % per annum, as parents demand proactive push‑alerts on feeding times, sleep cycles and medication. Other applications—including content sharing (peer community), co‑parent scheduling, and special‑needs care support—collectively account for around 44 % of usage.

The leading end‑user segment comprises individual new parents, accounting for approximately 52 % of the total user base, as they adopt apps to manage early‑stage child‑care from conception to toddler years. The fastest‑growing end‑user in the coming period is dual‑household co‑parenting users, with an estimated growth rate of 15 % per annum, driven by rising demand for shared‑custody coordination and messaging functionality. Other end‑users—such as extended‑family caregivers, childcare professionals and purposed‑apps for special‑needs families—together represent about 33 % of the market.

Asia‑Pacific accounted for the largest market share at 54.43 % in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 23.5 % between 2025 and 2032.

The Asia‑Pacific region posted an estimated market size of USD 514 million in 2024, while North America stood at around USD 258 million accounting for 27.33 % of the global total. The European region held approximately 13.72 % share. Across Asia‑Pacific, smartphone penetration exceeded 70 % in many countries, and new‑parent app user growth reached double digits in 2024. In North America, over 12,000 paediatric and childcare providers integrated parenting‑apps in 2024, and mobile‑first parenting user penetration passed 60 %. For Europe, regulatory drivers and data‑privacy preference resulted in exit‐rate reductions of approaching 20 % in parenting‑app usage. These figures highlight the contrasting dynamics: a volume‑led dominant region and a mature region with faster adoptive expansion.

How is digital parenting evolving in a mature ecosystem?

In North America, parenting apps hold roughly 27.33 % of the market share based on 2024 estimates, with a user‑base exceeding 23 million active users in some segments. Key driving industries include healthcare and early childhood education where parenting apps are embedded in wellness programmes and pediatric care support. Regulatory changes such as HIPAA‑compliance requirements for data handling of child‑health information have elevated trust and adoption of certified platforms. Technological advances include AI‑enabled milestone prediction, integration with wearable infant monitors and voice‑assistant compatibility. A noted regional player implemented a clinician‑guided behavioural module into its parenting‑app offering, reaching over 2 million downloads in 2024. Consumer behaviour in this region leans toward premium apps with subscription tiers and strong app‑to‑device ecosystems, contrasting with emerging‑market price‑sensitive models.

What impact do regulation and consumer expectations have on app demand?

In Europe, parenting apps capture approximately 13.72 % of the global market based on 2024 figures, with strong contributions from Germany, the UK and France. The regional framework emphasises explainable AI, data privacy standards and sustainability in digital services, making these features essential to product offering. Adoption of emerging technologies such as multilingual interactive modules and cloud‑based analytics is increasing. For example, European app developers are deploying transparent child‑data consent mechanisms and eco‑efficient backend infrastructure. Consumer behaviour reflects a higher preference for platforms that demonstrate ethical AI and data protection, and this has created a distinct segmentation of premium versus mainstream offerings.

Why is mobile‑first innovation accelerating adoption across diverse markets?

In Asia‑Pacific, the region accounted for 54.43 % of the global market share in 2024, representing approximately USD 514 million in size. Top consuming countries include China, India and Japan where smartphone penetration and digital literacy have surged: one reported stat shows 72 % of parents in India used parenting apps via smartphone in 2024. Infrastructure trends include local manufacturing of affordable devices and vibrant startup ecosystems in Singapore and Bangalore developing AI‑based parenting solutions. Regional tech trends show convergence of e‑commerce, AI‑driven child‑development insights and IoT‑enabled baby monitors. A local player launched a multi‑language parenting‑app in Southeast Asia that reached 8 million users in its first year. Regional consumer behaviour is distinctly mobile‑first and cost‑sensitive, favouring free‑plus‑subscription models and frequent in‑app enhancements.

How localization and digital inclusion shape market progress?

In South America, key countries such as Brazil and Argentina lead the segment and the region accounts for approximately 2.27 % of the global share in 2024. The region is witnessing growth of digital infrastructure and increasing mobile app uptake among parents, especially in urban areas. Government incentives for digital literacy and language‑localised content are supporting adoption. A Brazilian startup introduced a Portuguese‑language parenting app that reached 500,000 users by late 2024. Consumer behaviour shows demand tied to media and language localisation: 64 % of Brazilian parents indicated preference for culturally adapted platforms. The market is still emerging but presents opportunities in tailored content and local‑language feature roll‑out.

What growth drivers and challenges exist in emerging digital‑parenting markets?

In the Middle East & Africa region, the market share was around 2.25 % in 2024. Major growth countries include the UAE and South Africa where digital health and mobile‑app penetration are increasing. Technological modernisation trends include government‑backed AI initiatives and trade partnerships with global app‑developers focusing on parenting support. A UAE‑based company piloted an AI‑driven parental‑coaching app in 2024 reaching over 200,000 families. Regional regulations around child‑data protection and digital content are becoming more influential, and consumer behaviour is shaped by premium uptake in Gulf‑countries and affordability‑driven choices in sub‑Saharan markets.

United States – ~28 % share, driven by advanced digital parenting ecosystems and high end‑user demand.

China – ~17 % share, powered by large mobile‑first parent population and rapid scale‑up of local app ecosystems.

The Parenting Apps market is highly competitive and moderately fragmented, with over 120 active global competitors in 2024, including both established digital‑health platforms and emerging start-ups. The top five companies collectively hold approximately 41 % of the market, indicating a competitive environment where innovation and niche differentiation are key drivers. Market positioning varies widely: some players dominate in AI‑enabled developmental tracking, while others focus on co‑parenting coordination or wearable device integration. Strategic initiatives in 2024–2025 include partnerships with pediatric clinics, launch of multi-language mobile applications, integration of IoT devices for real-time child monitoring, and acquisition of smaller niche platforms to expand feature sets. Innovation trends influencing competition include AI‑driven predictive analytics, voice-assisted parental guidance, and gamified milestone tracking, which have increased user engagement by 22 % on average. Regional strategies are notable, with North America emphasizing premium subscription adoption and Asia‑Pacific focusing on mobile-first accessibility. Market entrants are actively investing in advanced analytics, security, and cloud scalability, creating differentiation in a competitive, tech-driven landscape that requires continuous adaptation to consumer needs and regulatory compliance.

Kinedu

Parenting Hero

Cozi Family Organizer

Parent Cue

Tot Squad

BabyTime

Wonder Weeks

The Parenting Apps market is being reshaped by a series of current and emerging technologies that enhance user experience, engagement, and functionality. Artificial intelligence (AI) is central to this transformation, with 42 % of leading apps in 2024 deploying AI-powered developmental milestone prediction tools that increase accuracy by 35 % compared to manual tracking methods. Machine learning algorithms analyze behavioral patterns, feeding, sleep schedules, and growth metrics, allowing personalized recommendations for each child and parent.

Integration with Internet of Things (IoT) devices is another key trend, with 41 % of users connecting parenting apps to wearable devices such as smart baby monitors, thermometers, and fitness trackers. These systems deliver real-time alerts on sleep, feeding, and vital signs, reducing manual oversight by 28 % and improving parental response times. Voice-assisted technologies are increasingly embedded in apps, providing hands-free guidance for milestone tracking, reminders, and interactive educational content, with usage reported in 36 % of premium parenting apps.

Cloud-based platforms and secure data storage solutions support scalability, cross-device synchronization, and privacy compliance. End-to-end encryption and parental-consent verification mechanisms have been adopted in over 67 % of apps to safeguard sensitive child data. Emerging technologies, such as augmented reality (AR) for interactive developmental learning and gamified engagement modules, are gaining traction, with over 12 million active users in urban markets engaging in AR-based features in 2024. These innovations collectively position parenting apps as integrated, tech-enabled ecosystems, bridging healthcare, education, and lifestyle management for modern parents.

In October 2024, The Bump announced a partnership with Consumer Reports to enhance car‑seat safety guidance for parents, combining expert reviews with real‑parent testimonials and integrating recommendations directly into the app’s product‑selection module. (Consumer Reports)

In June 2023, The Bump launched its “Best of The Bump Awards” series, recognising 13 product categories for pregnancy and postpartum needs while refreshing its visual identity and user‑experience across digital platforms as part of a broader brand upgrade. (Business Wire)

In February 2024, Peanut reported that its platform surpassed 5 million registered users, enabling new features such as “Groups” for milestone sharing and “Incognito Mode” for anonymised parenting advice, reflecting expansion in community‑driven parenting support. (Apple)

In early 2025, BabyCenter revealed that its mobile tracker app now supports over 400 million parent users worldwide, offering week‑by‑week pregnancy tracking, kick‑counters and 3D fetal‑development video tools, reinforcing its dominant presence in the pregnancy‑tracker segment. (apps.babycenter.com)

This Parenting Apps market report offers a comprehensive overview of the global ecosystem of mobile‑based parenting solutions, covering all relevant geographies, app types, user segments and technological modalities. It analyses market segmentation by type—such as pregnancy tracker apps, baby tracker apps, co‑parenting apps and baby‑care support apps—and by application across major operating systems (Android, iOS) and key feature groups including nutrition advice, sleep management, developmental milestone tracking and health consultation modules. The report further dissects regional scope across North America, Europe, Asia‑Pacific, South America and Middle East & Africa, presenting numerical insights on regional market shares, device‑penetration decimals, and consumer‑adoption benchmarks. It also encompasses industry‑focus areas across early‑childhood education, digital health integration, shared‑custody coordination and subscription-based parenting ecosystems. Emerging and niche segments such as multilingual parenting solutions, wearable‑monitoring integration and AI‑driven developmental prediction are included to offer decision‑makers visibility into next‑stage growth frontiers. Finally, the report examines competitive stratification, innovation cadences, regulatory overlays and investment patterns that underpin strategic planning for product‑launches, market entry and capability expansion in the parenting apps domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 731.44 Million |

Market Revenue in 2032 | USD 3166.09 Million |

CAGR (2025 - 2032) | 20.1% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | BabyCenter, The Bump, Kinedu, Parenting Hero, Cozi Family Organizer, Peanut, Parent Cue, Tot Squad, BabyTime, Wonder Weeks |

Customization & Pricing | Available on Request (10% Customization is Free) |