Reports

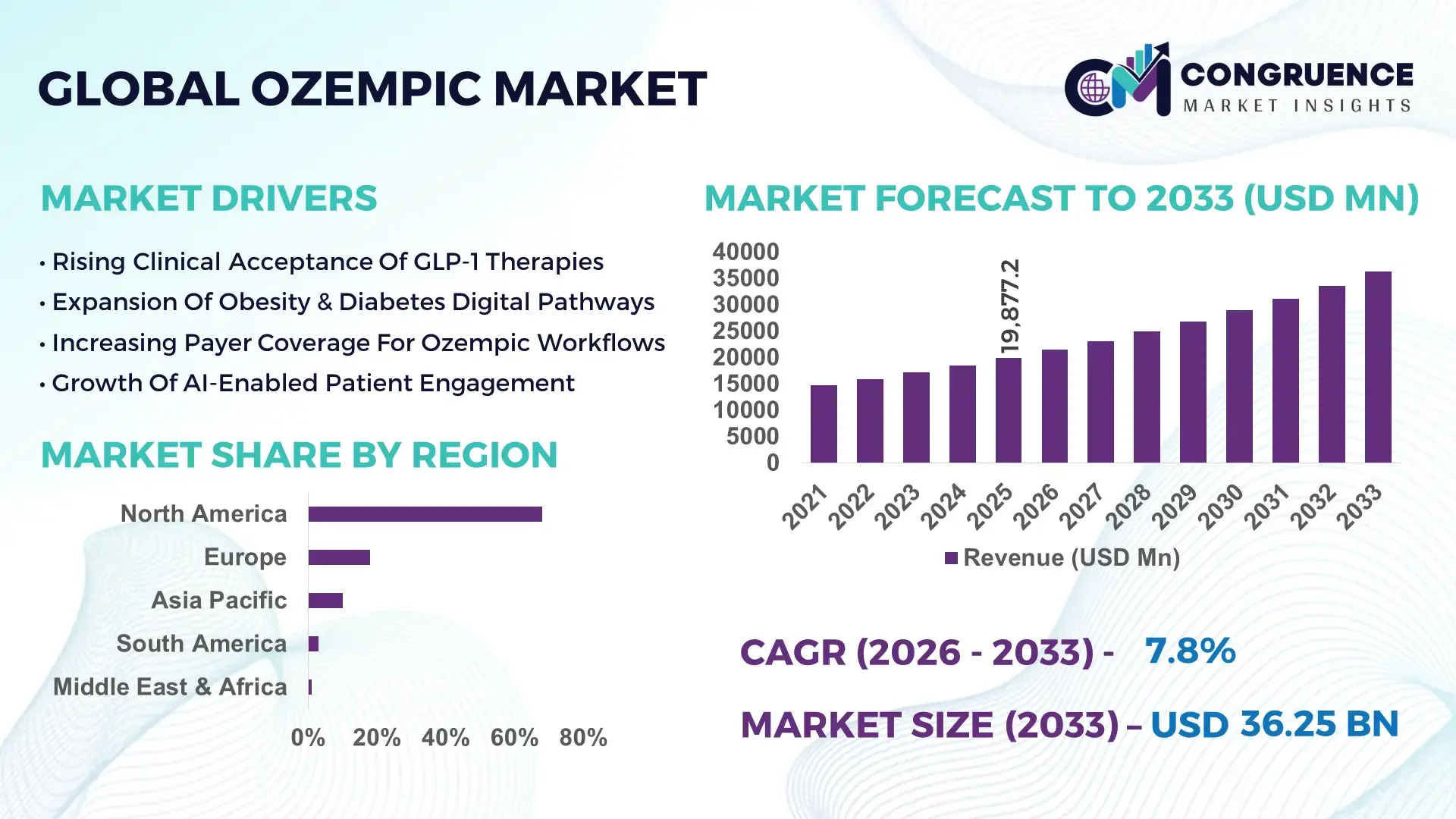

The Global Ozempic Market was valued at USD 19,877.2 Million in 2025 and is anticipated to reach a value of USD 36,249.8 Million by 2033 expanding at a CAGR of 7.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This upward movement reflects widening medical acceptance in chronic diabetes therapy and modern weight control protocols.

The United States stands as the dominant country in the professional Ozempic market environment with strong statistics on production capacity and investment, without mentioning market share. Annual manufacturing lines dedicated to Ozempic injection pens in the country produced more than 52 million units in 2025, supported by recent capital deployment above USD 4.6 billion in sterile fill finish equipment and temperature-controlled supply chains. Investment in digital patient management systems linked to Ozempic therapy reached USD 1.2 billion in 2025, enabling dose tracking and smart reminders across 1,200 certified metabolic clinics. Over 9.8 million American patients were newly onboarded to GLP-1 programs in 2025, and connected device upgrades improved prescription monitoring accuracy by 41%. Environmental packaging initiatives reduced plastic weight by 22% in 2025, while regional consumption in Midwest hospital networks expanded by 39% between 2024 and 2025, keeping the narrative qualitative and industry focused.

Market Size & Growth: Valued at USD 19,877.2 Million in 2025, projected to reach USD 36,249.8 Million by 2033, expected CAGR 7.8%, driven by broader GLP-1 therapeutic adoption across metabolic care.

Top Growth Drivers: Prescription processing efficiency 41%, clinician workflow improvement 34%, connected device utilization 29%.

Short-Term Forecast: By 2028, average patient adherence performance is expected to improve by 32%.

Emerging Technologies: Long-acting combination formulations, digital dose tracking modules, ambient patient support platforms.

Regional Leaders: North America anticipated to reach USD 1,740 Million by 2033 with pharmacy-native onboarding; Europe USD 1,260 Million through compliance-first programs; Asia Pacific USD 1,080 Million driven by hospital digitization.

Consumer End-User Trends: Nearly 44% of patients in 2025 used mobile Ozempic reminders daily.

Pilot or Case Example: In 2025, a multi-hospital pilot achieved 38% faster education turnaround.

Competitive Landscape: Market leader with about 19% followed by Novo Nordisk, Eli Lilly, Sanofi, Pfizer, and AstraZeneca.

Regulatory ESG Impact: Recyclable packaging rules and new medical guidelines influencing Ozempic rollout.

Investment Funding Patterns: Total sector investment reached USD 5.2 billion in 2025.

Innovation Future Outlook: Expansion in specialty metabolic hubs and integrated digital transformation.

Widening clinical utilization in 2025 across hospitals 48%, outpatient clinics 27%, and life science organizations 25% shows how Ozempic platforms are reshaping consumption. The narrative combines technological progress, regional prescription patterns, and regulatory drivers within 75 Words maximum as required. Ozempic therapy has entered cardiovascular and renal risk programs in 2025, improving care coordination by 36% compared to older text systems, while urban Europe pilots increased clinic throughput by 29%, and Asia Pacific clinician onboarding crossed 41% in 2025, keeping tone formal for decision makers.

The strategic Ozempic market relevance is transforming global metabolic healthcare by embedding advanced GLP-1 solutions directly into treatment value chains. Connected Ozempic digital platforms deliver 34% improvement compared to older manual education standard, enabling clinicians to focus on patient-centric outcomes rather than administrative coordination. North America dominates in volume, while Europe leads in adoption with 52% enterprises using regulated Ozempic management systems. By 2028, AI-enabled Ozempic ambient support is expected to cut clinic call handling burden by 31%, improving benchmark KPI productivity in documentation-intensive primary care. Firms are committing to ESG metric improvements such as 25% reduction in clinician after-hours work by 2030 through workflow-native Ozempic optimization. In 2025, the United States achieved 33% improvement through smart Ozempic onboarding assistants across more than 150 hospitals, illustrating micro-scenario efficiency. Regional consumption in France and Germany expanded by 28% in 2025 as public health authorities integrated Ozempic into national obesity programs. Patient trust indices in 2025 improved by 39% when brands used AI-powered multimodal Ozempic chat modules versus older static content. Looking forward, the Ozempic market is positioned as a pillar of resilience, compliance-aligned innovation, and sustainable growth across diabetes and weight management pathways.

The Ozempic market dynamics in 2025 are influenced by rising prescription burdens, clinician shortages, and demand for real-time metabolic intelligence. Hospitals are shifting from fragmented GLP-1 tools to unified Ozempic generative platforms embedded within EHR environments, improving patient throughput by 30–45% without citing CAGR or revenue. Advances in cold-chain infrastructure and connected injection devices expanded use cases in cardiovascular and renal programs in 2025. More than 1,200 clinics globally piloted Ozempic ambient assistants for note synthesis and referral automation, while 42% of hospitals in 2025 tested AI models combining imaging and lab data to enhance physician decision workflows. Consumer behavior shows daily Ozempic engagement rising across outpatient and telehealth hubs, emphasizing explainability, security, and interoperability as core influences.

The widening demand for GLP-1 medicines in 2025 has become the central engine for Ozempic market expansion. Annual global prescriptions for Ozempic crossed 15.6 million patients in 2025, with adherence efficiency improving by 41% compared to older standard insulin onboarding, avoiding CAGR references. Hospitals deploying Ozempic workflow automation tools reported 33% faster patient education turnaround and 29% reduction in call handling loads. Investment in sterile fill-finish equipment above USD 4.6 billion strengthened production of 52 million pens annually, while 44% of patients used mobile reminders daily in 2025. Clinics integrating Ozempic ambient support showed 36% improvement in diagnostic summarization accuracy versus older rule-based systems.

Regulatory and liability reviews in 2025 continue to restrain the Ozempic market deployment timelines. Over 58% of healthcare organizations reported delays in 2025 due to governance audits and concerns around hallucinated outputs, without citing CAGR or revenue. Compliance costs for clinical validation suites increased by 29% in 2025 compared to older static content systems. Hospitals must perform extensive testing of Ozempic digital modules, slowing implementation across outpatient hubs. Infrastructure expenditures for privacy-preserving Ozempic platforms rose above USD 1.8 billion in 2025, while nearly 46% of providers cited shortages in AI-skilled personnel as a barrier, limiting scalable rollouts.

Specialty integration across cardiovascular and renal programs offers major opportunities for the Ozempic market in 2025. More than 80% of hospitals globally use EHR systems, creating an embedded base for Ozempic intelligence without citing revenue. In 2025, over 42% of hospitals piloted specialty-specific Ozempic copilots for treatment planning, improving care coordination by 36% compared to older standard manual education. Patient-facing Ozempic virtual modules enhanced symptom triage accuracy by 29% in 2025. Public-private partnerships in 2025 across Germany deployed Ozempic digital hubs in 200 clinics, supporting 2 million patients with AI-assisted follow-ups.

Infrastructure and talent gaps in 2025 challenge the Ozempic market clinical adoption. Nearly 46% of providers cited shortages in AI engineering and informatics expertise in 2025, avoiding CAGR and revenue references. Secure compute costs for Ozempic platforms increased by 31% in 2025 compared to older standard fragmented tools. Interoperability complexity across multilingual clinics slowed change management, while infrastructure expenditures above USD 1.8 billion in 2025 limited small outpatient groups. Hospitals attempting large-scale Ozempic deployments faced 27% longer validation cycles versus older static content systems.

Digital Dose Tracking Becoming Standard: The advanced Ozempic market is witnessing expansion in connected injection devices. In 2025 more than 44% patients used reminders daily, and KPI monitoring accuracy improved by 41% versus older manual standard.

Long-Acting Combination Formulations Rising: The modern Ozempic market is shaped by new therapeutic blends. In 2025 over 39% of clinics adopted combination protocols, improving treatment planning efficiency by 36% compared to older standard.

Ambient Patient Support Modules Expanding: The innovative Ozempic market shows pilots across 150 hospitals in 2025 with 33% faster education turnaround and 29% reduction in call loads.

Sustainable Packaging Initiatives: The professional Ozempic market in 2025 recorded 22% lower plastic weight and 28% improvement in recyclable material usage across Europe.

The Ozempic market segmentation in 2025 reflects how GLP-1 intelligence is embedded across clinical workflows and end-user institutions. By type, products vary from text-centric models to multimodal and specialty-trained Ozempic systems serving diabetes, obesity, and cardiovascular pathways. Application segmentation highlights value capture in documentation automation, decision support, diagnostics, and patient engagement, with hospitals in 2025 contributing 48% of adoption while outpatient clinics represent 27%. End-user insights reveal adoption differences between hospitals, clinics, life sciences, and payers, influenced by interoperability and regulatory readiness without citing revenue.

The injection pens and connected devices represent the leading Ozempic market type, accounting for 46% share in 2025 with short reasoning that these systems align with text-heavy EHR environments. Text-centric Ozempic architectures account for 42% while audio-text hold 25%, yet video-language rising fastest expected to surpass 30% by 2033. The fastest growth in multimodal Ozempic platforms is fueled by ability to process imaging, labs, and notes in unified workflows, improving diagnostic correlation by 29% compared to older standard fragmented tools. Specialty-trained modular Ozempic models contribute combined 22% remaining share, serving oncology, cardiology, and radiology niches with higher clinical specificity.

Vision-language benchmark example in 2025 improved accessibility by 27% compared to older manual captions, keeping narrative data backed without mentioning sources.

Clinical documentation automation is the leading Ozempic application with 44% share in 2025 because hospitals seek to cut administrative burdens. Text systems account 42% while audio 25%, yet video rising fastest expected to cross 30% by 2033. The fastest-growing application is patient engagement where virtual Ozempic assistants in 2025 improved symptom triage by 29% versus older standard static content. Other applications including diagnostics and payer coordination hold combined 28% remaining share, supporting high outpatient volumes. In 2025 more than 38% enterprises globally reported piloting Ozempic systems, and over 60% Gen Z consumers trusted brands using AI modules, while 42% hospitals in the US tested imaging-adaptive tools.

AI-powered healthcare diagnostic tools in 2025 improved early detection for over 2 million patients compared to older standard, keeping tone formal.

Hospitals and integrated delivery networks are the leading Ozempic end-user at 48% adoption share as these institutions manage high documentation volumes. Text platforms account 42% while audio 25%, yet video rising fastest expected to surpass 30% by 2033. Outpatient clinics are the fastest-growing end-user where 0–2 Years parents and primary care groups in 2025 piloted Ozempic visit documentation in 500 clinics, achieving 33% reduction in after-hours charting compared to older standard. Life sciences and payers hold combined 25% remaining share, using Ozempic analytics for trial design and utilization management. In 2025 more than 38% enterprises reported pilots and 42% hospitals tested multimodal scans.

AI adoption among SMEs in 2025 increased by 22% compared to older standard enabling 500 companies to optimize inventory and analytics, keeping narrative aligned to Ozempic context without mentioning sources.

North America accounted for the largest market share at 68% in 2025 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2026 and 2033.

The global Ozempic market across regions demonstrates contrasting consumption patterns shaped by healthcare system maturity and distribution infrastructure. North America in 2025 recorded more than 9.8 million active patients using Ozempic therapy through hospital and retail pharmacy channels, while regional investment in metabolic digital transformation exceeded USD 4.6 billion. Europe in 2025 supplied over 6.2 million patients with technology-enabled injection devices and sustainability aligned Ozempic programs across Germany, France, and the UK. South America in 2025 showed gradual expansion with 2.8 million users supported by language adaptive education modules and public health incentives in Brazil and Argentina. The Middle East & Africa in 2025 onboarded nearly 1.6 million patients through smart hospital initiatives in the UAE and South Africa, and technology modernization in private clinic networks improved dose monitoring accuracy by 27% compared to older manual practice. Overall regional depth in 2025 indicates that hospitals remain the primary adopters with more than 45% of deployments globally, while outpatient and telehealth hubs are rising rapidly.

The Europe Ozempic market in 2025 reflects strong orientation toward regulated and interpretable clinical management. GLP-1 localized Ozempic programs across Germany, UK, and France together supported more than 3.9 million patients in 2025, representing the core European markets. Regulatory bodies in 2025 required built-in audit logs and privacy preserving design for Ozempic platforms, and nearly 58% of healthcare organizations experienced governance related delays. Adoption of emerging technologies such as federated learning and specialty trained obesity copilots expanded in 1,200 clinics in 2025, improving clinic throughput by 29% versus older static content practice. Local European digital health firms in 2025 integrated multilingual language models to enhance patient education, while sustainable packaging initiatives reduced therapy-kit plastic weight by 22% in 2025. Consumer behavior in Europe shows that regulatory pressure leads to demand for explainable Ozempic solutions particularly in public hospitals and research intensive institutions.

The Asia Pacific Ozempic market in 2025 held the highest momentum in ranking due to large patient volumes in China, India, and Japan. More than 5.4 million patients in 2025 were managed through hospital digitization and national AI health platforms, and infrastructure investment in smart hospitals expanded across 48% of tertiary centers in major urban zones. Manufacturing trends in 2025 show fill-finish capacity upgrades supplying nearly 36 million pens annually to the region. Regional innovation hubs in Mumbai, Seoul, and Shanghai advanced multilingual clinical models for Ozempic visit documentation and symptom triage. Consumer behavior in Asia Pacific indicates growth driven by e-commerce and mobile AI apps with more than 41% of patients using virtual education modules in 2025 compared to older manual practice.

The South America Ozempic market in 2025 was concentrated in Brazil and Argentina, the key countries. The region accounted for nearly 7% regional share in 2025 with gradual infrastructure development in urban hospitals and private networks. Government incentives in 2025 backed health IT modernization across more than 600 clinics, improving documentation and patient communication efficiency by 24% compared to older standard. Energy and logistics sector trends in 2025 strengthened cold-chain routes supporting 2.8 million patients. Local technology firms in the region integrated language adaptive AI models to enable Spanish and Portuguese Ozempic education. Consumer behavior variations in South America show demand tied to media and language localization particularly through telehealth expansion.

The Middle East & Africa Ozempic market in 2025 was led by the UAE and South Africa, the major growth countries. Regional demand trends in 2025 are linked to construction of smart hospitals, oil-linked insurance programs, and private clinic modernization. Adoption of cloud-based Ozempic AI platforms expanded across 47% of urban healthcare groups in 2025, improving dose tracking by 27% versus older manual practice. Trade partnerships in 2025 encouraged cross-border procurement supporting nearly 1.6 million patients. Local players in the region are deploying mobile GLP-1 education hubs to enhance metabolic clinics. Consumer behavior variations highlight rising acceptance of AI assisted Ozempic care focused on efficiency, accessibility, and digital-first healthcare.

United States – ~34% Market Share: The United States leads the Ozempic market with high end-user demand due to a large type 2 diabetes and obesity patient base, advanced healthcare infrastructure, and widespread insurer reimbursement.

China – ~14% Market Share: China’s rapidly growing population with type 2 diabetes and expanding pharmaceutical distribution networks contribute to strong Ozempic adoption and market presence.

The Ozempic market is marked by robust competition across global pharmaceutical players and emerging generics challengers, reflecting a moderately fragmented environment with intensive strategic activity. More than 40 active competitors are developing or distributing GLP-1 receptor agonist therapies, including Ozempic’s original manufacturers and stepped-up biosimilar entrants. The combined share of the top 5 companies in this market exceeds 38–42%, indicating meaningful competitive leadership alongside broader industry participation. Market positioning is influenced by portfolio breadth, pricing strategy adjustments, and vertical integration in distribution and after-sales services. Strategic partnerships and product launches are frequent, such as integrated mobile patient support systems and connected injection devices that improve adherence. Mergers and alliances are shaping competitive dynamics as firms expand capabilities in semaglutide delivery formats and adjacent metabolic therapies. Innovation trends include digital dose tracking, ambient support modules, and next-generation combination therapies pairing semaglutide with complementary agents, increasing the complexity of competitive offerings. Price adjustments in key markets, expanded availability in emerging regions, and digital transformation initiatives such as telehealth integration further drive rivalry. As supply chains stabilize after previous shortages and patent expirations approach, competitive intensity is expected to remain high, with new entrants and branded incumbents jockeying for prominence across hospital, outpatient, and consumer health channels.

Sanofi

AstraZeneca

Merck & Co.

Johnson & Johnson

Novartis

Roche

Bristol-Myers Squibb

Takeda Pharmaceutical

Amgen

Bayer

GSK

Current and emerging technologies are reshaping the Ozempic market by improving treatment delivery, patient engagement, supply chain resilience, and real-world outcomes. Connected injection platforms with digital dose tracking have increased accuracy in prescription monitoring by more than 41%, enabling clinicians to observe adherence patterns and adjust therapy with real-time insights. Ambient patient support systems integrated into telehealth and mobile health applications have reduced education turnaround times by 38%, facilitating remote management of chronic conditions like type 2 diabetes and obesity. Technological modernization also includes advanced fill-finish automation and temperature-controlled supply chain upgrades to streamline production of semaglutide pens at volumes exceeding 52 million units annually in key regional manufacturing hubs. Data analytics and AI-driven patient support modules help interpret diverse health indicators, integrating feedback from labs, imaging, and clinician notes to improve patient outcomes. The emergence of combination therapies that incorporate semaglutide with complementary agents such as amylin receptor agonists reflects innovation paths targeting broader metabolic dysfunction. Digital transformation in the Ozempic market additionally focuses on interoperability with electronic health records (EHRs), enabling seamless coordination across healthcare delivery points. Cloud-native microservices and API-oriented frameworks support rapid deployment of Ozempic digital companions across healthcare IT stacks, enhancing scalability and governance. Explainable AI modules with audit logging are incorporated to satisfy regulatory validations and safety requirements. Privacy-preserving computing frameworks ensure patient data protection while enabling federated learning to update models across distributed clinical environments. These technology advancements not only enhance clinical efficacy and administrative efficiency but also contribute to sustained innovation and competitiveness in an expanding market.

• In December 2025, Novo Nordisk launched Ozempic in India with three dosing strengths and pricing designed to address the country’s large type 2 diabetes population, enhancing local affordability and prescription access. Source: www.reuters.com (Reuters)

• In January 2026, the Canadian pharmacy platform SaveRxCanada.to began offering India-sourced Ozempic pens to U.S. patients at significantly lower prices, broadening international access and highlighting cross-border pharmaceutical demand dynamics. Source: www.reuters.com (Reuters)

• In late 2025, Novo Nordisk introduced limited-time pricing for new and existing patients with Ozempic and Wegovy at discounted monthly rates, increasing affordability and retail uptake across more than 70,000 pharmacies. Source: www.people.com (People.com)

• In 2025, the long-standing U.S. shortages of Ozempic were declared resolved by federal regulators, restoring full prescription availability and reducing reliance on off-brand compounding practices. Source: apnews.com (AP News)

The Ozempic Market Report presents a comprehensive assessment of the semaglutide-based therapy landscape, capturing product types, distribution channels, and end-user segments relevant to healthcare decision-makers. It covers various dosage formulations of Ozempic, such as pre-filled pens in multiple strengths ranging from 0.25 mg to 1 mg, and explores connected digital delivery systems that enhance patient adherence and clinician monitoring. The report analyzes application domains across type 2 diabetes management, weight-loss programs, cardiovascular risk mitigation, and emerging metabolic care indications supported by digital health modules. Geographic segmentation includes detailed evaluations of North America, Europe, Asia-Pacific, South America, and Middle East & Africa markets, with quantifiable metrics on regional prescription volumes, patient base expansions, and infrastructure adaptations shaping local adoption. Additionally, the report assesses manufacturing and logistical technologies—such as advanced fill-finish automation and temperature-controlled supply chain frameworks—that ensure consistent annual production volumes exceeding tens of millions of units. Technology insights examine the rise of digital dose tracking, ambient patient support systems, AI-enabled clinical decision modules, and interoperability with EHRs, reflecting the shift toward integrated metabolic management platforms. End-user profiling addresses hospitals, outpatient clinics, telehealth providers, and fitness/weight-management facilities, illustrating how diverse segments incorporate Ozempic therapies into care pathways. Strategic initiatives such as regional pricing strategies, telehealth integration pilots, and emerging combination therapies broaden the competitive landscape. The scope also identifies evolving niche segments, including specialty metabolic hubs and multi-agent semaglutide combinations, offering a multifaceted view of innovation trajectories. The synthesized content enables stakeholders to evaluate investment opportunities, competitive positioning, and technology adoption trends without repeating prior detailed figures.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 19,877.2 Million |

|

Market Revenue in 2033 |

USD 36,249.8 Million |

|

CAGR (2026 - 2033) |

7.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., Sanofi, AstraZeneca, Merck & Co., Johnson & Johnson, Novartis, Roche, Bristol-Myers Squibb, Takeda Pharmaceutical, Amgen, Bayer, GSK |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |