Reports

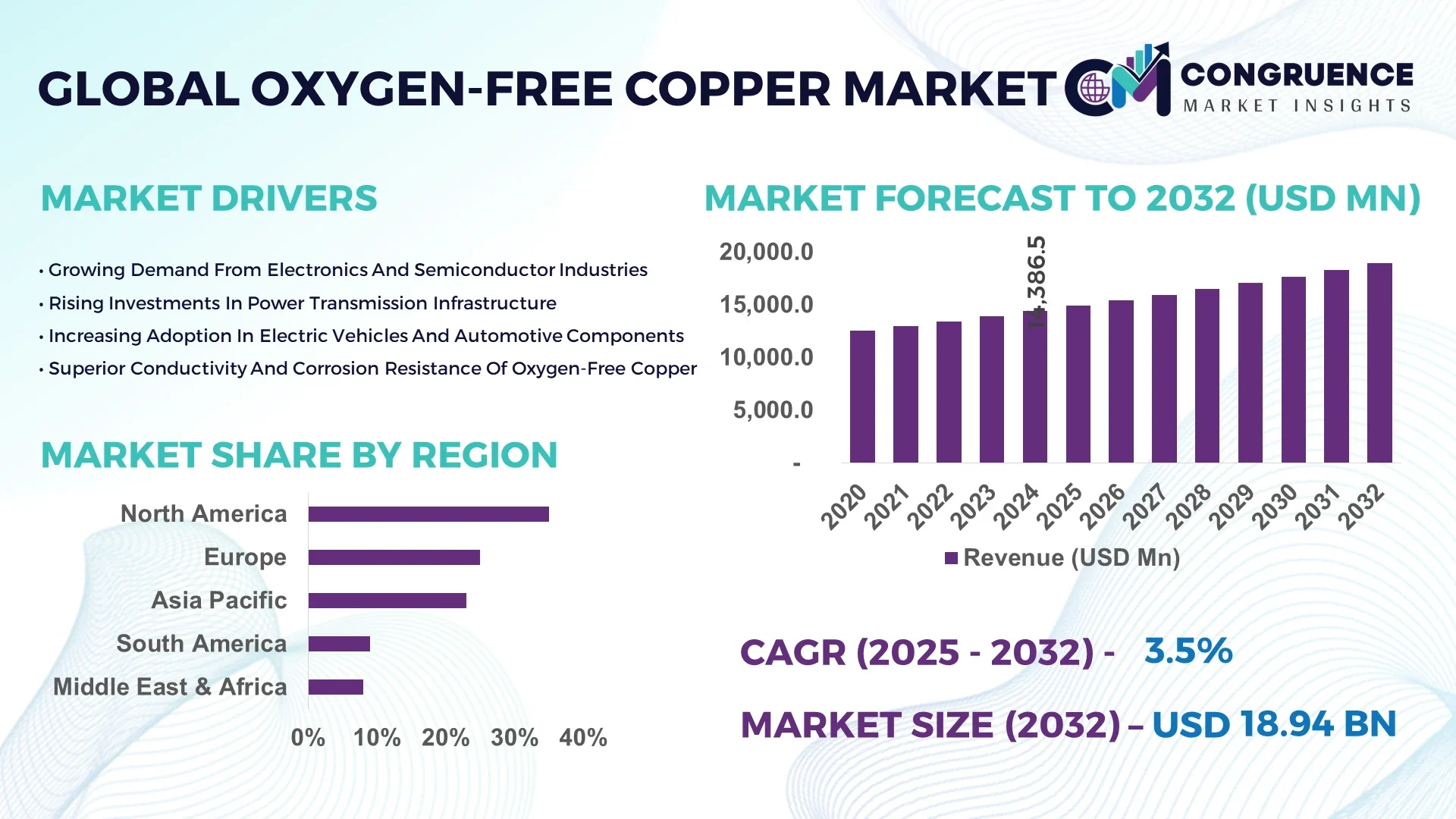

The Global Oxygen-Free Copper Market was valued at USD 14,386.5 Million in 2024 and is anticipated to reach a value of USD 18,944.27 Million by 2032, expanding at a CAGR of 3.5% between 2025 and 2032.

Oxygen-free copper (OFC) is a premium-grade copper material known for its excellent electrical conductivity and minimal impurities, particularly low oxygen content. This makes it ideal for high-performance applications, such as semiconductors, power cables, and electronic components, where superior conductivity is critical. The growing demand for high-quality copper in the automotive, electronics, and renewable energy industries is a major factor driving the market. The Asia-Pacific region, led by China, Japan, and South Korea, is the largest consumer of OFC, driven by rapid industrialization and technological advancements in these countries. Moreover, the shift towards electric vehicles and renewable energy sources is expected to boost the demand for OFC in the coming years, further propelling market growth.

Artificial Intelligence (AI) is making significant strides in various industries, including the oxygen-free copper market, by enabling manufacturers to optimize production processes, improve quality control, and enhance supply chain efficiency. AI technologies, such as machine learning algorithms, are being utilized to predict demand patterns, optimize raw material usage, and reduce wastage during copper production. This results in cost savings and increased profitability for manufacturers. Furthermore, AI-driven automation has improved the precision of copper alloy composition, ensuring consistent product quality and reducing the need for manual inspections. In terms of logistics, AI is helping in tracking shipments, predicting delivery times, and managing inventory more effectively. As manufacturers increasingly adopt these AI technologies, the oxygen-free copper market is set to benefit from enhanced production capabilities, reduced costs, and streamlined operations. The role of AI in developing more efficient copper production techniques and improving the overall supply chain will continue to drive the market’s growth in the coming years.

"In 2024, a leading copper manufacturer in South Korea implemented an AI-based quality control system that uses deep learning algorithms to detect defects in copper products during the manufacturing process. This technology significantly reduces production errors, enhances product quality, and decreases material waste."

The dynamics of the oxygen-free copper market are shaped by various factors, including demand for high-quality materials in electrical and electronic applications, advancements in AI and automation, and the growing emphasis on renewable energy sources. As industries continue to require more efficient and reliable materials, the demand for OFC is expected to rise. Additionally, advancements in manufacturing processes, such as the integration of AI and automation, are helping to reduce costs, improve product quality, and streamline production, thereby enhancing market dynamics. The increasing focus on sustainability and environmental concerns is also playing a crucial role in shaping market trends, as industries seek materials with minimal environmental impact.

Increasing demand for high-performance materials

The growing demand for high-performance materials in industries such as automotive, electronics, and renewable energy is driving the oxygen-free copper market. In particular, the rise of electric vehicles (EVs) has led to an increased need for OFC, as it offers superior electrical conductivity for EV batteries and charging stations. The electronics industry also relies on OFC for components such as connectors and semiconductor devices, further boosting market demand. As global industrialization continues and the demand for energy-efficient materials rises, oxygen-free copper remains a critical component in achieving higher performance in various sectors.

High production costs of oxygen-free copper

Despite its advantages, the high production costs of oxygen-free copper act as a restraint on its market growth. The production process for OFC involves high-quality raw materials and specialized manufacturing techniques that are energy-intensive, leading to increased production costs. Furthermore, fluctuations in the prices of raw copper, coupled with stringent regulations on environmental impact, can add to the overall cost of production. This price sensitivity often leads to competition from other alternatives, which may limit the widespread adoption of OFC in certain applications.

Growth in the renewable energy sector

The renewable energy sector presents significant opportunities for the oxygen-free copper market. As the world shifts toward more sustainable energy sources, OFC is increasingly being used in the construction of wind turbines, solar panels, and other green energy technologies due to its superior conductivity and resistance to corrosion. With the global push to reduce carbon emissions and promote clean energy solutions, the demand for OFC in renewable energy applications is expected to increase, creating new opportunities for market expansion.

Limited availability of high-quality raw materials

One of the key challenges facing the oxygen-free copper market is the limited availability of high-quality raw materials required for its production. The extraction of high-purity copper is a complex and resource-intensive process, and as demand increases, it becomes more challenging to source the necessary materials. Additionally, geopolitical factors and trade restrictions can further disrupt supply chains, leading to volatility in raw material availability and impacting production costs..

The oxygen-free copper market is experiencing several key trends that are shaping its future. First, there is a growing demand for OFC in the automotive and electronics industries, particularly with the rise of electric vehicles and the increasing need for high-performance components in electronic devices. As industries strive for higher energy efficiency and reduced environmental impact, OFC’s superior conductivity and corrosion resistance make it an attractive material. Additionally, advancements in production technologies, such as the integration of AI and automation, are enabling manufacturers to improve the efficiency of their operations, reduce costs, and enhance product quality. Furthermore, the shift towards renewable energy sources is driving the use of OFC in wind and solar power systems. These trends are expected to continue to propel the growth of the oxygen-free copper market, with new opportunities arising in sectors such as telecommunications, energy storage, and electric vehicle infrastructure.

The copper market can be segmented based on type, application, and end-user insights, offering a comprehensive overview of its diverse demand. By type, the market is driven by variations in copper's composition, such as Electrolytic Tough Pitch Copper (ETP), High Conductivity Copper (HCC), and Oxygen-Free High Conductivity Copper (OFHC), each offering different levels of conductivity and purity. Applications of copper range from electrical wiring to power transmission lines, with industries relying on copper for electronics, automotive, aerospace, and industrial machinery. End-user insights provide additional understanding of the demand within sectors like electrical and electronics, automotive, and telecommunications, highlighting copper’s critical role in these industries’ operations and innovation.

North America accounted for the largest market share at 35% in 2024, however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2025 and 2032.

North America followed closely behind, accounting for 30% of the market share in 2024, with steady growth anticipated in the coming years. Europe, contributing 25% to the market, will see moderate growth, driven by advancements in the electronics and automotive sectors. The Middle East and Africa hold a smaller share but are forecast to experience a surge in demand due to increasing industrialization. Each region’s growth trajectory reflects distinct drivers such as infrastructure development, technological advancements, and industrial needs, positioning them strategically within the global oxygen-free copper market.

Rising Demand from Electric Vehicles and Electronics Driving Market Growth

North America held a significant portion of the oxygen-free copper market in 2024, accounting for approximately 30% of the global share. The demand for high-conductivity copper is being driven by the region’s strong automotive and electronics industries, especially with the rising adoption of electric vehicles (EVs). Copper is a critical material in electric motors and batteries, and as more automakers shift towards EV production, the demand for high-quality copper materials, including oxygen-free copper, is expected to remain robust. In addition, advancements in telecommunications and the need for reliable and high-performance components in networking and semiconductor applications will continue to fuel demand in the region.

Sustainability and Electric Mobility Boost Oxygen-Free Copper Demand

In 2024, Europe accounted for about 25% of the global oxygen-free copper market share. The European market is primarily driven by the automotive and renewable energy sectors, with increasing demand for copper in electric vehicles, wind turbines, and solar energy systems. As the European Union continues to invest in sustainable energy and electric mobility, oxygen-free copper remains crucial for its high conductivity and efficiency in powering electronic systems and energy storage solutions. Additionally, the region's robust industrial manufacturing sector, including aerospace and machinery, contributes significantly to copper consumption, further supporting growth in the market.

Leads in Oxygen-Free Copper Consumption, Driven by Industrialization and EV Growth

Asia-Pacific is the largest and fastest-growing market for oxygen-free copper, accounting for approximately 40% of the global share in 2024. The region's rapid industrialization, particularly in China, India, and Southeast Asia, is driving significant demand for high-quality copper in various sectors, including electronics, telecommunications, and automotive. The booming electric vehicle market in China is particularly noteworthy, as it accounts for the largest share of global EV production, necessitating increased use of copper in batteries and electric motor systems. Additionally, Asia-Pacific is a major hub for manufacturing semiconductor components, where oxygen-free copper is indispensable for high-performance applications.

Infrastructure Expansion and Renewable Energy Adoption Fuel Market Potential

The Middle East and Africa (MEA) region holds a smaller share of the oxygen-free copper market, contributing about 5% in 2024. However, the market in this region is expected to grow as infrastructure development, particularly in oil and gas, construction, and telecommunications, accelerates. The demand for high-performance materials such as oxygen-free copper is rising due to the expansion of manufacturing sectors, where the material is used in electrical wiring, industrial machinery, and electronic components. Additionally, the push for more sustainable energy solutions and the adoption of renewable energy in the region will further support market growth, with copper playing a vital role in energy systems.

The oxygen-free copper market is highly competitive, with several global players actively driving innovation and meeting the growing demand across various industries. Major companies in the market focus on expanding their production capacities, developing new alloys, and establishing stronger distribution networks to cater to the demand in sectors such as electronics, automotive, and telecommunications. Key players compete based on product quality, cost-effectiveness, and technological advancements in copper refining and production techniques. The market also sees a growing emphasis on sustainability and energy-efficient solutions, particularly with the increasing focus on electric vehicles and renewable energy systems. As the global economy shifts towards greener technologies, companies in the oxygen-free copper market are expected to enhance their capabilities and remain at the forefront of meeting the future needs of their customers.

KME Germany GmbH & Co. KG

Furukawa Electric Co., Ltd.

Mitsubishi Materials Corporation

Hitachi Metals, Ltd.

Southwire Company, LLC

Aurubis AG

Wieland-Werke AG

Luvata Oy

Trefimetaux S.A.

Daewon Metal Co., Ltd.

The oxygen-free copper market has witnessed significant technological advancements in recent years, enhancing the material's performance and expanding its applications across various industries. In November 2023, SK Nexilis commenced the production of ultra-thin oxygen-free copper foils, measuring just 4 microns, at its new facility in Malaysia. This plant, with an annual capacity of 57,000 tons, represents an investment of nearly USD 690 million.

Advancements in manufacturing processes have led to the development of oxygen-free copper with improved electrical conductivity and reduced impurities. These enhancements make the material increasingly suitable for high-performance applications in electronics, automotive, and renewable energy sectors.

The integration of digital technologies and Industry 4.0 concepts in production has further optimized the manufacturing of oxygen-free copper. Smart manufacturing techniques have improved quality control, efficiency, and traceability, contributing to the material's growing demand.

Additionally, the focus on sustainability has prompted the adoption of environmentally friendly methods in copper production. Companies are exploring eco-friendly practices such as recycling and responsible sourcing to meet the rising demand for sustainable products.

These technological innovations not only enhance the properties of oxygen-free copper but also align with global trends towards sustainability and high-performance materials, positioning the market for continued growth and diversification.

November 2023: SK Nexilis initiated the production of ultra-thin oxygen-free copper foils at its new facility in Malaysia. The plant, with an annual capacity of 57,000 tons, represents an investment of nearly USD 690 million.

October 2023: Anglo-American signed a Memorandum of Understanding with Mitsubishi Materials to collaborate on producing copper products. This partnership aims to meet the rising demand for copper across various industries.

December 2024: Glencore entered into a multi-year agreement with Cyclic Materials Inc. to supply over 10,000 metric tons of recycled copper. The copper will be processed and refined at Glencore's Horne smelter in Quebec, North America's largest recycler of copper and precious metals.

December 2024: China's Jiangxi Copper and Chilean miner Antofagasta set the benchmark smelter treatment charges for the following year at $21.50 per metric ton, a significant decrease from the previous year's $80.00. This drop is attributed to rapid global smelter capacity expansion, especially in China.

October 2023: SK Nexilis commenced commercial production at its first overseas facility in Kota Kinabalu, Malaysia. This facility is part of the company's strategy to expand its global footprint and meet the increasing demand for high-quality copper products.

The Oxygen-Free Copper Market report provides a comprehensive analysis of the market's current state and future prospects. It examines the market dynamics, including drivers, restraints, opportunities, and challenges, to offer a clear understanding of the factors influencing market growth. The report delves into the segmentation of the market by grade, product type, application, and region, providing detailed insights into each segment's performance and potential.

It also highlights the technological advancements shaping the industry, such as innovations in manufacturing processes and the adoption of digital technologies, which enhance the quality and efficiency of oxygen-free copper production. The report further explores the impact of sustainability trends, noting the increasing emphasis on environmentally friendly practices and the growing demand for recycled copper.

Regional analyses are included to assess the market's performance across different geographies, identifying key growth areas and emerging markets. The report also profiles leading companies in the oxygen-free copper industry, offering insights into their strategies, product offerings, and market positions.

Overall, the report serves as a valuable resource for stakeholders seeking to understand the complexities of the oxygen-free copper market, providing data-driven insights to inform strategic decisions and investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 14,386.5 Million |

|

Market Revenue in 2032 |

USD 18,944.27 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types:

By Application:

By End-User:

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

KME Germany GmbH & Co. KG, Furukawa Electric Co., Ltd., Mitsubishi Materials Corporation, Hitachi Metals, Ltd., Southwire Company, LLC, Aurubis AG, Wieland-Werke AG, Luvata Oy, Trefimetaux S.A., Daewon Metal Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |