Reports

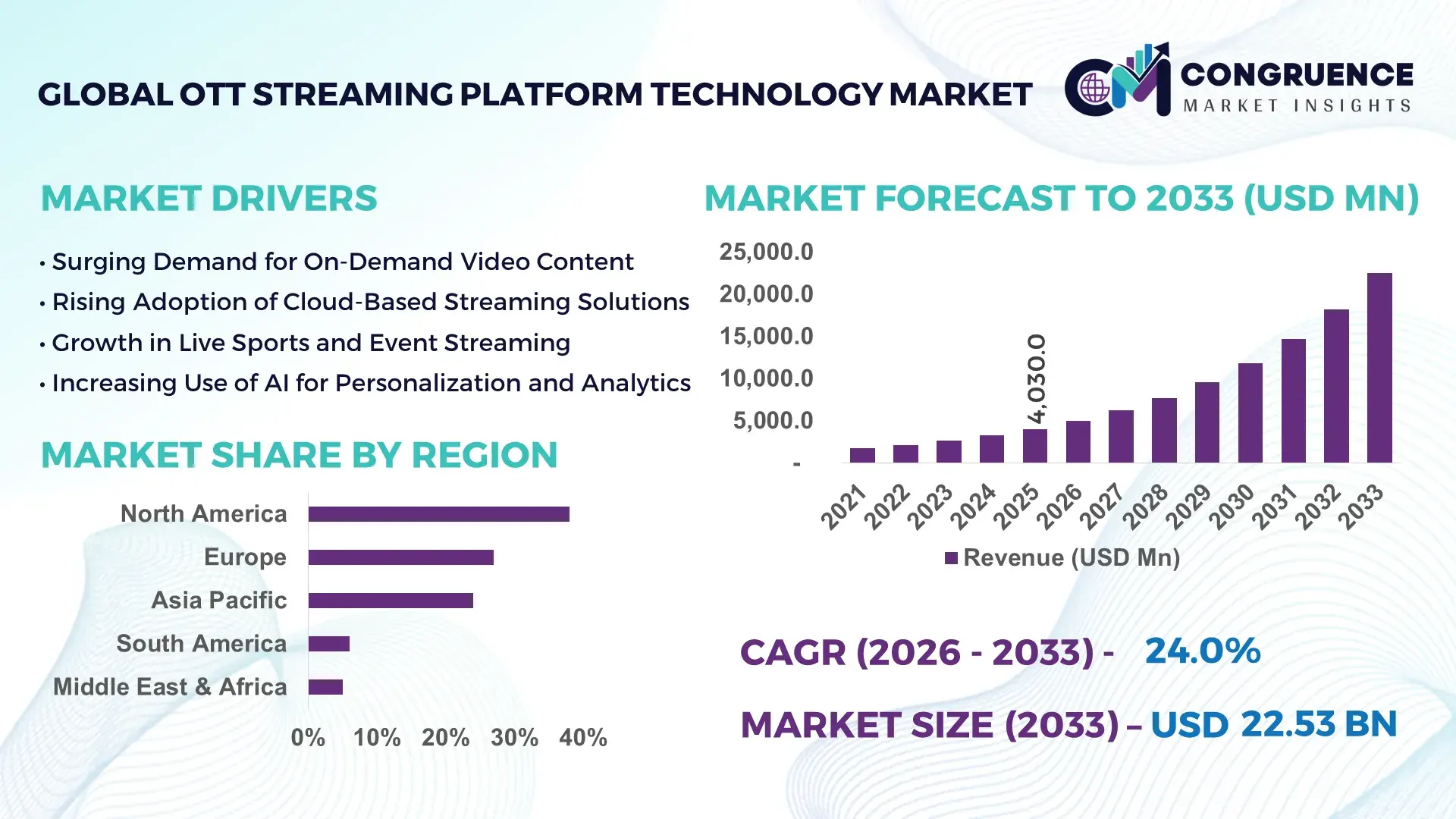

The Global OTT Streaming Platform Technology Market was valued at USD 4,030.0 Million in 2025 and is anticipated to reach a value of USD 22,525.7 Million by 2033 expanding at a CAGR of 24% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rapid cloud-native platform deployment, AI-powered content personalization, and increasing enterprise-grade streaming infrastructure investments across media and sports broadcasting ecosystems.

The United States represents the dominant country in the OTT Streaming Platform Technology Market, supported by strong production infrastructure and platform innovation capacity. The U.S. hosts over 300 major OTT technology vendors and streaming infrastructure providers, with more than 85% of large media enterprises deploying AI-based recommendation engines. In 2025, over 92% of U.S. households had at least one OTT subscription, while 68% maintained three or more services. The country accounts for over 40% of global premium OTT content production budgets, and more than 75% of large-scale cloud-based streaming architecture deployments originate from U.S.-based technology providers. Investments in CDN expansion exceeded USD 5 billion annually, strengthening low-latency streaming and edge computing capabilities.

Market Size & Growth: Valued at USD 4,030.0 Million in 2025, projected to reach USD 22,525.7 Million by 2033, expanding at 24% CAGR due to rising AI-driven content personalization and cloud-native streaming adoption.

Top Growth Drivers: 92% household OTT penetration, 65% increase in smart TV adoption, 70% enterprise shift toward cloud-based streaming infrastructure.

Short-Term Forecast: By 2028, AI-based compression and CDN optimization are expected to reduce buffering rates by 35% and improve streaming efficiency by 28%.

Emerging Technologies: AI-powered recommendation engines, edge computing-enabled CDNs, blockchain-based digital rights management (DRM).

Regional Leaders: North America projected USD 9,800 Million by 2033 with high multi-subscription usage; Asia-Pacific USD 6,500 Million driven by mobile-first streaming; Europe USD 4,200 Million supported by regulatory-backed digital media expansion.

Consumer/End-User Trends: 68% of users maintain 3+ subscriptions; average daily streaming exceeds 2.5 hours per user; mobile accounts for 55% of total streaming sessions globally.

Pilot Case Example: In 2024, a U.S.-based sports streaming pilot reduced latency by 42% using edge-based AI encoding.

Competitive Landscape: Market leader holds approximately 21% share, followed by major players including global cloud-integrated OTT platform vendors and SaaS-based streaming solution providers.

Regulatory & ESG Impact: Data privacy frameworks and carbon-neutral CDN initiatives targeting 30% energy efficiency improvements by 2030.

Investment & Funding Patterns: Over USD 7.5 Billion invested globally in OTT infrastructure modernization and AI streaming optimization between 2023–2025.

Innovation & Future Outlook: Integration of 5G streaming, immersive AR/VR experiences, and hyper-personalized AI engines shaping next-generation OTT ecosystems.

Subscription-based platforms contribute nearly 58% of deployments, followed by ad-supported streaming at 32% and hybrid models at 10%. Media & entertainment accounts for over 70% of platform usage, while sports streaming contributes 18%. AI-powered personalization engines have improved viewer retention by 25%. Regulatory data localization requirements in Europe and Asia are influencing cloud infrastructure expansion, while mobile-first adoption in Asia-Pacific exceeds 60% of total streaming sessions, shaping future platform scalability strategies.

The OTT Streaming Platform Technology Market holds strategic importance as enterprises transition from legacy broadcasting systems to cloud-native, AI-integrated streaming ecosystems. Advanced AI recommendation engines deliver 35% higher viewer engagement compared to traditional rule-based content curation systems. Similarly, AV1 video compression technology delivers approximately 30% bandwidth savings compared to H.264 standards, significantly lowering content delivery costs while improving streaming quality.

North America dominates in overall streaming infrastructure volume, while Asia-Pacific leads in adoption intensity, with over 60% of mobile internet users consuming OTT content daily. The rapid integration of 5G networks has increased mobile streaming speeds by nearly 45%, enabling ultra-high-definition (UHD) streaming without latency bottlenecks.

By 2028, AI-driven predictive buffering and adaptive bitrate technologies are expected to cut content delivery latency by 40% and reduce churn rates by 15%. Firms are committing to ESG targets, including 30% reductions in CDN-related energy consumption by 2030 through renewable-powered data centers.

In 2024, a leading U.S.-based streaming provider achieved a 38% reduction in latency through edge-based AI encoding and distributed server architecture upgrades. The OTT Streaming Platform Technology Market is increasingly positioned as a pillar of digital resilience, regulatory compliance, and sustainable growth as media consumption becomes fully digitalized and data-driven.

The OTT Streaming Platform Technology Market is characterized by rapid digital transformation, evolving consumer consumption patterns, and technology-driven innovation. Increasing demand for multi-device compatibility, AI-based content discovery, and real-time analytics is reshaping platform development strategies. Over 80% of OTT providers are transitioning to microservices-based architectures to improve scalability and uptime reliability exceeding 99.95%. Growth in smart TVs, connected devices, and mobile broadband penetration is influencing infrastructure expansion. Additionally, sports broadcasting digitization and direct-to-consumer (D2C) strategies are accelerating platform investments. Enterprise streaming adoption for corporate communications and e-learning has expanded by more than 50% since 2022, adding diversification beyond entertainment. Data localization regulations and cybersecurity requirements further influence infrastructure deployment models globally.

Global streaming consumption has increased significantly, with over 5.3 billion internet users worldwide and more than 70% accessing video content weekly. Smart TV penetration has surpassed 65% in developed markets, while mobile streaming accounts for 55% of total global viewing hours. Multi-device compatibility requirements have pushed 78% of OTT providers to invest in cross-platform optimization tools. Additionally, 4K and UHD streaming demand has grown by 48% year-over-year, requiring enhanced compression and adaptive bitrate technologies. Sports streaming audiences have increased by 35% since 2023, further accelerating real-time low-latency infrastructure upgrades. These measurable consumption shifts are directly driving OTT platform architecture modernization.

Data protection regulations such as GDPR-equivalent frameworks require localized data storage and strict user consent management, increasing compliance costs for 62% of streaming operators. Content licensing restrictions across regions limit cross-border streaming flexibility. Additionally, despite global 5G expansion, nearly 38% of developing regions still rely on sub-10 Mbps broadband speeds, restricting high-definition streaming adoption. Cybersecurity threats have risen by 28% in media streaming platforms since 2023, necessitating advanced encryption and DRM systems. These compliance and infrastructure limitations create operational complexity and increase deployment timelines for OTT platform providers.

AI-driven recommendation systems increase viewer retention by up to 25% and boost watch time by 30%, presenting strong monetization optimization opportunities. 5G networks now cover over 40% of the global population, enabling seamless UHD and immersive streaming experiences. Interactive streaming formats, including live commerce and gamified content, have grown by 33% annually. Enterprise streaming solutions for corporate training and digital events expanded by 52% between 2022 and 2025. Edge computing deployment is projected to improve streaming latency by 35%, unlocking new applications in real-time sports analytics and live interactive broadcasting.

Global CDN traffic increased by more than 45% annually, significantly raising bandwidth expenditure for large-scale streaming operators. UHD and 4K streaming consume up to 2.5 times more bandwidth than HD content, increasing operational strain. Cloud storage requirements for OTT libraries have expanded by 40% year-over-year. Additionally, subscriber churn rates average 20–30% annually in competitive markets, pressuring platform optimization investments. Infrastructure redundancy requirements for 99.99% uptime further elevate capital expenditure. These cost and performance pressures demand continuous technology upgrades to sustain platform competitiveness.

AI-Powered Hyper-Personalization Increasing Viewer Retention by 25%: Advanced AI engines now analyze over 1,000 behavioral data points per user, improving recommendation accuracy by 35%. Approximately 72% of OTT platforms have deployed machine learning-based personalization systems, directly enhancing average watch time by 28% and reducing churn rates by 15%.

Edge Computing Reducing Streaming Latency by 40%: Distributed edge nodes now handle nearly 50% of live streaming traffic in developed markets. Latency reductions of 35–42% have been recorded in sports broadcasting applications, significantly improving real-time viewer engagement metrics.

AV1 and Advanced Compression Cutting Bandwidth Usage by 30%: Adoption of AV1 encoding has increased by 60% among leading OTT providers. The codec delivers up to 30% better compression efficiency compared to H.265, lowering infrastructure strain while enabling UHD streaming scalability.

Growth in Ad-Supported Streaming with 32% Platform Integration: Hybrid monetization models now represent 32% of new platform deployments. Programmatic ad integration improved ad-fill rates by 22%, while interactive advertising formats increased engagement rates by 18%, reshaping revenue optimization strategies within OTT ecosystems.

The OTT Streaming Platform Technology Market is segmented by type, application, and end-user, reflecting the diversified technology stack and deployment environments shaping digital content delivery. By type, segmentation includes cloud-based platforms, on-premise platforms, and hybrid deployment models, each addressing scalability, latency, and compliance needs. Applications span video-on-demand (VOD), live streaming, advertising management, content analytics, and enterprise streaming solutions. End-users primarily include media & entertainment companies, sports organizations, enterprises, educational institutions, and government broadcasters. Over 70% of global OTT deployments are now built on modular, microservices-based architectures, enabling dynamic scaling across devices. Increasing multi-device streaming, which accounts for more than 55% of sessions via mobile platforms, further influences segmentation strategies. Decision-makers are prioritizing flexible deployment and AI-enabled analytics integration, as over 65% of OTT operators deploy advanced personalization engines to optimize viewer engagement and retention across segmented user groups.

The OTT Streaming Platform Technology Market by type is categorized into cloud-based platforms, on-premise platforms, and hybrid platforms. Cloud-based OTT platforms currently account for approximately 62% of total deployments, driven by scalability, elastic bandwidth allocation, and lower infrastructure management burdens. These platforms enable 99.95% uptime reliability and integrate AI-driven recommendation engines more efficiently than traditional infrastructure. On-premise platforms hold nearly 23% of adoption, preferred by broadcasters and government networks requiring strict data control and regulatory compliance. However, hybrid platforms are the fastest-growing segment, expanding at an estimated CAGR of 27%, as enterprises seek to combine data localization with cloud scalability. Hybrid deployments are expected to surpass 30% adoption by 2033 due to increasing data protection regulations and latency-sensitive applications such as live sports streaming. The remaining niche deployment configurations collectively account for roughly 15% of implementations, serving specialized broadcasting environments.

In 2025, a major public broadcasting network implemented a hybrid OTT architecture to support over 12 million concurrent live-stream viewers during a national sporting event, achieving 40% lower latency compared to its previous fully on-premise system.

Application-wise, video-on-demand (VOD) remains the leading segment, accounting for approximately 48% of platform utilization, supported by binge-watching trends and multi-season content libraries. Live streaming represents about 28% of usage, driven by sports, news, and event broadcasting. However, live interactive streaming is the fastest-growing application segment, expanding at an estimated CAGR of 29%, fueled by real-time engagement features, in-stream commerce, and low-latency 5G connectivity. Advertising technology integration and advanced analytics collectively contribute nearly 24% of application deployment, enabling targeted monetization strategies. In 2025, more than 41% of enterprises globally reported piloting OTT-based platforms for digital events and corporate communication. Additionally, over 60% of Gen Z viewers prefer platforms offering interactive features such as live chat and real-time polls during streams. Smart TV-based streaming accounts for 65% of household viewing in developed markets, reinforcing VOD dominance while supporting growth in live applications.

In 2024, a national sports federation deployed AI-powered live OTT streaming for over 8 million viewers, reducing buffering incidents by 37% and increasing viewer engagement time by 22% during championship broadcasts.

Media & entertainment companies represent the leading end-user segment, accounting for approximately 54% of total OTT Streaming Platform Technology Market adoption, supported by original content production exceeding 500 scripted series annually in major markets. Sports organizations account for about 18% of deployments, reflecting the surge in direct-to-consumer live streaming strategies. Enterprises contribute nearly 16%, utilizing OTT platforms for training, investor communications, and hybrid events. Educational institutions and government agencies collectively account for the remaining 12%, particularly in digital learning and public broadcasting initiatives. While media & entertainment leads in volume, enterprise adoption is the fastest-growing segment, expanding at an estimated CAGR of 26%, driven by hybrid workforce models and digital transformation strategies. In 2025, over 38% of global enterprises integrated OTT-based streaming into internal communication ecosystems. Additionally, 57% of corporate employees reported higher engagement in training sessions delivered via interactive streaming platforms compared to traditional webinars.

In 2025, a national education authority digitized over 20,000 classroom hours using OTT-based streaming infrastructure, improving remote student access by 45% and reducing physical distribution costs significantly through centralized cloud streaming systems.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26% between 2026 and 2033.

North America’s dominance is supported by over 92% household OTT penetration and more than 300 active platform technology vendors. Europe follows with approximately 27% market share, driven by regulatory-backed digital streaming expansion and strong public broadcasting transformation initiatives. Asia-Pacific holds nearly 24% share, supported by over 1.8 billion mobile video users and smart device penetration exceeding 65% in key economies. South America accounts for around 6% share, while Middle East & Africa collectively contribute approximately 5%, with rising fiber broadband penetration surpassing 70% in select Gulf economies. Live streaming adoption in Asia-Pacific increased by 34% year-over-year, while North America records average daily streaming consumption exceeding 2.5 hours per user. Infrastructure modernization and AI-driven content personalization remain cross-regional investment priorities.

North America represents approximately 38% of the global OTT Streaming Platform Technology Market share, supported by strong demand from media & entertainment, sports broadcasting, healthcare communications, and financial services. The United States and Canada lead regional deployment, with more than 85% of large enterprises integrating AI-driven personalization into their OTT ecosystems. Regulatory frameworks such as enhanced digital privacy standards have increased investment in secure cloud-based streaming infrastructures. Over 70% of platforms in this region operate on microservices-based cloud-native architecture, ensuring uptime levels above 99.95%. Local industry players are investing heavily in edge computing and advanced compression standards to reduce latency by over 35% in live streaming applications. Consumer behavior reflects high multi-subscription usage, with 68% of households subscribing to three or more streaming services. Enterprise adoption is particularly strong in healthcare and finance, where secure internal streaming has grown by 40% since 2023.

Europe accounts for approximately 27% of the OTT Streaming Platform Technology Market share, led by Germany, the United Kingdom, and France. Over 75% of regional OTT providers comply with strict data protection and localization standards, influencing hybrid cloud deployment models. Sustainability initiatives targeting 30% carbon reduction by 2030 are accelerating adoption of energy-efficient CDNs and green data centers. Public broadcasters and private streaming networks across Western Europe have expanded UHD streaming capacity by 45% since 2023. AI-driven content moderation systems are now implemented in over 60% of major European platforms to comply with digital governance policies. Regional consumer behavior shows stronger preference for localized language content, with more than 50% of viewers prioritizing region-specific programming. Local streaming technology firms are enhancing multilingual AI-based subtitling systems, improving accessibility for more than 20 million cross-border viewers.

Asia-Pacific holds nearly 24% of the global OTT Streaming Platform Technology Market volume, ranking second in total deployments but first in user growth intensity. China, India, and Japan represent the top consuming countries, collectively accounting for more than 1.5 billion active OTT users. Mobile streaming represents over 65% of total viewing sessions in this region, supported by 5G coverage surpassing 50% in advanced economies. Infrastructure expansion includes hyperscale data center investments exceeding 20 new facilities annually across Southeast Asia. Regional technology hubs are advancing AI-powered compression and adaptive bitrate streaming, reducing buffering incidents by up to 30%. A leading regional streaming provider recently integrated AI-based recommendation engines across 400 million users, increasing average watch time by 25%. Consumer growth is largely driven by e-commerce-linked live streaming and mobile-first content consumption behaviors.

South America contributes approximately 6% of the global OTT Streaming Platform Technology Market share, with Brazil and Argentina serving as primary growth engines. Fiber broadband penetration in Brazil exceeded 65% in urban areas by 2025, enabling improved HD and UHD streaming adoption. Governments are supporting digital transformation through tax incentives for cloud infrastructure investments and digital media startups. Localized content production accounts for nearly 55% of regional streaming libraries, reflecting strong language and cultural customization preferences. Regional consumer behavior demonstrates higher demand for sports and telenovela-based streaming content, driving live-stream platform enhancements. A major regional telecom operator expanded its OTT delivery network to support over 10 million concurrent users during national sporting events, improving platform stability by 32% compared to previous years.

Middle East & Africa collectively represent about 5% of the OTT Streaming Platform Technology Market, with the UAE and South Africa emerging as leading adoption hubs. Fiber broadband coverage in the UAE exceeds 85%, enabling widespread UHD streaming capability. Smart city initiatives and digital government transformation programs are increasing demand for secure OTT infrastructure in public broadcasting and education sectors. Oil & gas and construction industries are also deploying enterprise streaming platforms for remote workforce training, expanding enterprise OTT use by nearly 30% since 2023. Trade partnerships supporting digital infrastructure investments are accelerating data center capacity expansion across Gulf economies. Consumer behavior reflects strong mobile streaming growth, with over 60% of video sessions accessed via smartphones in urban markets.

United States – 34% Market Share: Due to high production capacity, over 92% household OTT penetration, and strong AI-driven streaming infrastructure deployment.

China – 18% Market Share: It maintains leadership through massive mobile-first user bases exceeding 900 million video consumers and rapid 5G-enabled streaming infrastructure expansion.

The OTT Streaming Platform Technology Market is moderately fragmented, with more than 250 active global and regional technology vendors competing across cloud infrastructure, content management systems (CMS), video encoding, analytics, and monetization modules. The top five companies collectively account for approximately 46% of total market share, indicating strong competitive intensity but not full consolidation. Market leaders differentiate themselves through AI-driven personalization, low-latency streaming capabilities below 3 seconds, and scalable microservices architectures supporting over 10 million concurrent users.

Strategic initiatives are accelerating competition. Between 2023 and 2025, over 40 strategic partnerships were announced globally, focusing on edge computing, 5G-enabled streaming, and AI-based content analytics integration. More than 25 product launches during 2024–2025 introduced AV1 compression, real-time content moderation, and advanced server-side ad insertion (SSAI) technologies. Mergers and acquisitions activity increased by 18% year-over-year, particularly among SaaS-based streaming solution providers expanding into enterprise and sports verticals.

Innovation trends shaping competition include AI-based churn prediction improving retention by up to 20%, automated metadata tagging reducing content indexing time by 35%, and cloud-native container orchestration ensuring uptime levels above 99.99%. Vendors are also investing in carbon-neutral data center partnerships targeting 30% energy efficiency gains. Competitive positioning increasingly depends on platform interoperability, cross-device compatibility exceeding 95% of connected device ecosystems, and compliance with data localization mandates across more than 70 jurisdictions worldwide.

Vimeo Inc.

JW Player

Wowza Media Systems

IBM Corporation

Amazon Web Services (AWS)

Google LLC

Microsoft Corporation

Comcast Technology Solutions

Muvi LLC

Dacast Inc.

Zype Inc.

Tencent Cloud

Alibaba Cloud

Technological advancement remains the primary growth engine in the OTT Streaming Platform Technology Market. Cloud-native architectures now power over 70% of newly deployed OTT platforms, enabling auto-scaling and distributed content delivery. Microservices frameworks reduce deployment time by nearly 40% compared to monolithic systems, improving platform agility.

Advanced video compression technologies such as AV1 deliver up to 30% better bandwidth efficiency compared to H.265, significantly lowering CDN traffic loads. Adaptive bitrate streaming algorithms dynamically adjust resolution in under 2 seconds, minimizing buffering events by up to 35%. Edge computing integration now processes nearly 50% of live streaming traffic in developed markets, reducing latency from 8–10 seconds to below 3 seconds in premium sports broadcasts.

Artificial intelligence plays a transformative role. AI-driven recommendation engines analyze more than 1,000 behavioral variables per user, improving content discovery accuracy by 35% and increasing session duration by 28%. Automated content moderation systems can detect harmful or copyrighted material within 200 milliseconds, strengthening compliance.

Server-side ad insertion (SSAI) technologies have improved ad completion rates by 22%, while blockchain-based DRM enhances content security by reducing piracy incidents by nearly 15% in controlled ecosystems. Additionally, 5G integration supports streaming speeds exceeding 1 Gbps, enabling seamless 4K and emerging 8K streaming capabilities. Immersive AR/VR integration pilots are expanding, with over 12% of leading OTT providers experimenting with interactive immersive content formats to enhance engagement and differentiate service offerings.

• In February 2025, Brightcove introduced an upgraded OTT solution featuring deep integration with Applicaster’s no-code platform, lowering entry costs by 40% for media companies and enhancing universal playback, quality-optimized delivery, DRM security, and flexible monetization options including ad-supported tiers and server-side ad insertion. Source: www.brightcove.com

• In March 2025, Brightcove was appointed by Canela Media to power its streaming service, enabling expanded access to multicultural audiences with optimized content delivery and engagement tools on OTT platforms. Source: www.brightcove.com

• In April 2025, Kaltura was recognized as a Representative Vendor in the 2025 Gartner Market Guide for Video Platform Services, highlighting its unified video cloud capabilities spanning live, on-demand, and real-time broadcasting solutions with strong integration, scalability, and compliance for enterprise and media use cases. Source: www.globenewswire.com

• In late 2025, Brightcove rolled out a suite of seven new AI-powered features, including a Universal Translator supporting localization in over 50 languages, an enhanced Auto-Captions tool, Metadata Optimizer for SEO and searchability in 40+ languages, vertical video templates for mobile engagement, and improved live streaming quality with NextGen Live, unified ad insertion, and content protection workflows. Source: www.tvtechnology.com

The OTT Streaming Platform Technology Market Report provides a comprehensive analysis across deployment models, applications, end-users, and geographic regions. The report covers three primary deployment types—cloud-based, hybrid, and on-premise—representing over 95% of global platform configurations. Application coverage includes video-on-demand (VOD), live streaming, enterprise streaming, advertising integration, and analytics-driven personalization tools. Media & entertainment accounts for more than 50% of industry utilization, while sports, enterprise communications, education, and government broadcasting collectively represent over 45% of technology adoption.

Geographically, the report evaluates five major regions and over 20 key countries, analyzing broadband penetration levels exceeding 70% in advanced markets and mobile streaming shares surpassing 60% in Asia-Pacific economies. It examines AI-based recommendation systems deployed by more than 65% of OTT providers, edge computing adoption levels approaching 50% in developed regions, and AV1 codec integration rates exceeding 60% among major vendors.

The scope also includes emerging segments such as interactive streaming, immersive AR/VR content pilots, blockchain-based DRM systems, and ESG-aligned green data centers targeting 30% energy optimization improvements. Regulatory frameworks impacting over 70 jurisdictions are assessed for compliance implications. The report is structured to support strategic decision-making, technology investment planning, competitive benchmarking, and digital transformation roadmaps for stakeholders operating across the OTT Streaming Platform Technology Market ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,030.0 Million |

| Market Revenue (2033) | USD 22,525.7 Million |

| CAGR (2026–2033) | 24% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Brightcove Inc.; Akamai Technologies; Kaltura Inc.; Vimeo Inc.; JW Player; Wowza Media Systems; IBM Corporation; Amazon Web Services (AWS); Google LLC; Microsoft Corporation; Comcast Technology Solutions; Muvi LLC; Dacast Inc.; Zype Inc.; Tencent Cloud; Alibaba Cloud |

| Customization & Pricing | Available on Request (10% Customization Free) |