Reports

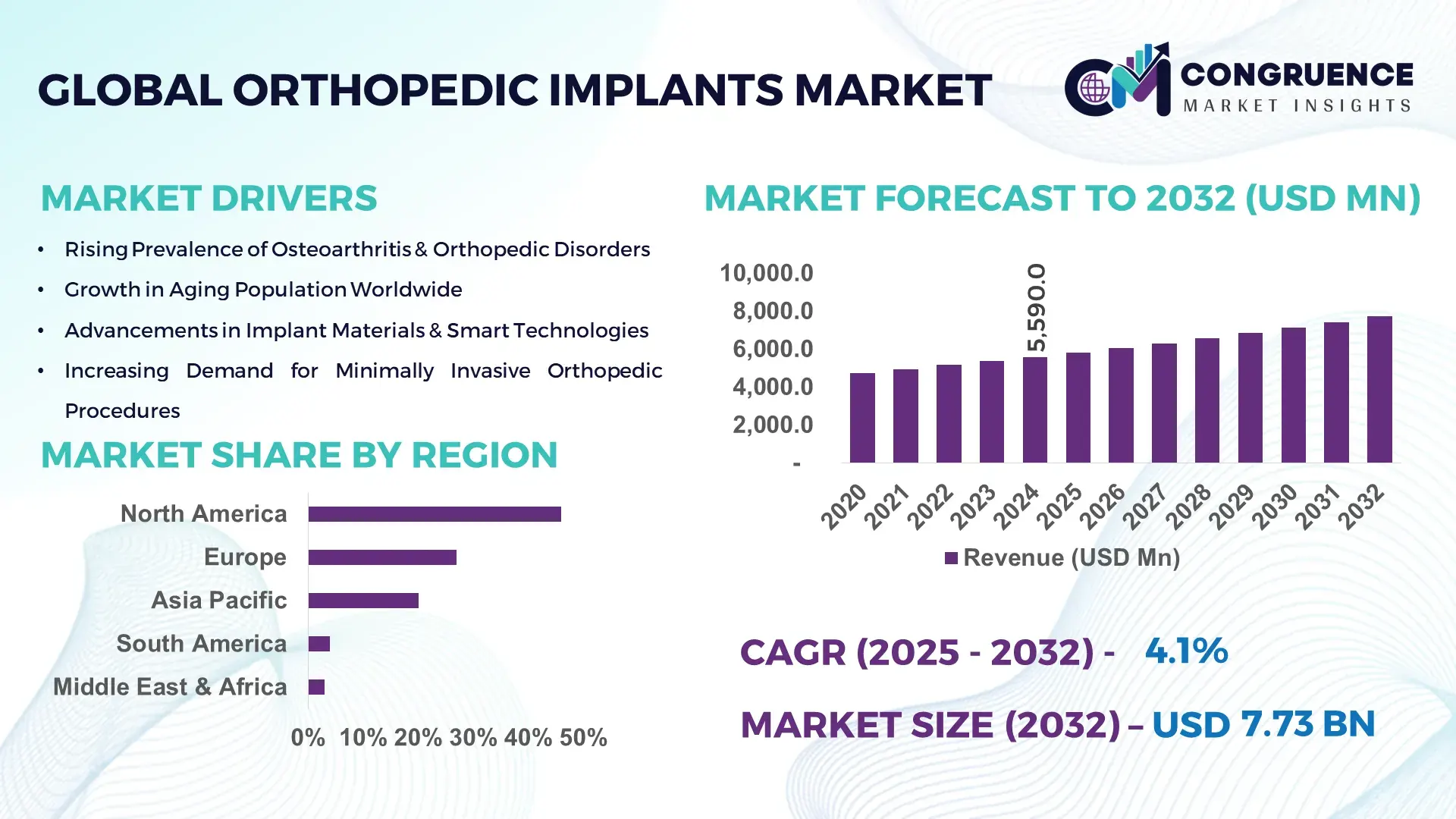

The Global Orthopedic Implants Market was valued at USD 5,590.0 Million in 2024 and is anticipated to reach USD 7,733.1 Million by 2032, expanding at a CAGR of 4.14% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by the increasing demand for advanced reconstructive solutions supported by continuous material and design innovations.

The United States remains the leading country in the orthopedic implants market, supported by high manufacturing capacity exceeding 65 million implant units annually, substantial R&D expenditure surpassing USD 2.4 billion per year, and strong adoption across trauma, joint reconstruction, and spine applications. Investments in robotic-assisted surgical platforms, additive manufacturing (with over 900 active medical 3D-printing facilities), and biocompatible alloys reinforce its technological advantage. The country also records advanced clinical utilization, with more than 1.3 million orthopedic surgeries performed annually, ensuring sustained demand for next-generation implants.

Market Size & Growth: The market stands at USD 5.59 billion in 2024 and is projected to reach USD 7.73 billion by 2032, driven by a 4.14% CAGR supported by increasing surgical volumes and material advancements.

Top Growth Drivers: Includes 38% adoption of minimally invasive orthopedic procedures, 42% efficiency improvement in implant designs through 3D printing, and 36% rise in AI-supported surgical planning.

Short-Term Forecast: By 2028, implant manufacturing efficiency is expected to improve by 28% through automated machining and precision additive workflows.

Emerging Technologies: Growth is propelled by biointegrative implants, smart sensor-embedded devices, and robotics-assisted joint replacement systems.

Regional Leaders: By 2032, North America is projected to reach USD 3.1 billion, Europe USD 2.4 billion, and Asia Pacific USD 1.9 billion, each showing distinct adoption trends including robotics use, fast regulatory clearance, and expanding hospital networks.

Consumer/End-User Trends: Hospitals and surgical centers show rising adoption of advanced implants, especially in spine and trauma segments, with a strong shift toward patient-specific designs.

Pilot or Case Example: In 2027, a U.S. orthopedic center achieved a 33% reduction in surgical time using AI-guided implant alignment systems.

Competitive Landscape: The market leader holds approximately 14% share, followed by major players including Zimmer Biomet, Johnson & Johnson (DePuy Synthes), Stryker, Smith & Nephew, and Medtronic.

Regulatory & ESG Impact: Sustainability guidelines and implant recall frameworks are increasing the adoption of compliant, traceable, and recyclable implant materials.

Investment & Funding Patterns: Over USD 1.6 billion in recent investments flowed into orthopedic robotics, digital surgery tools, and biomaterial innovation.

Innovation & Future Outlook: Advancements in bioceramics, composite polymers, and real-time intraoperative imaging are shaping future growth, supported by expanding personalized implant programs worldwide.

The orthopedic implants market continues advancing with innovative biomaterials, AI-enhanced surgical planning tools, supportive regulations targeting device safety, and increasing demand for joint and trauma procedures across emerging and mature economies, reinforcing strong long-term expansion potential.

The strategic relevance of the Orthopedic Implants Market lies in its foundational role in sustaining global healthcare outcomes, enabling surgical efficiency, and supporting long-term patient mobility across aging populations. With surgical volumes expected to rise steadily, the industry is prioritizing advanced materials, digital surgery platforms, and automation to improve clinical precision. For instance, smart sensor–enabled implant technologies deliver up to 27% improvement in post-operative alignment accuracy compared to conventional mechanical systems, providing measurable gains in rehabilitation and patient satisfaction.

Regional variations demonstrate distinct pathways for market development. North America dominates in volume, driven by high procedure rates and advanced hospital infrastructure, while Europe leads in adoption, with nearly 48% of orthopedic centers using robotic-assisted techniques. These comparative dynamics reveal how different regions progress through innovation cycles at varying speeds. In the short term, significant breakthroughs are anticipated: by 2027, AI-powered pre-surgical modeling is expected to reduce intraoperative errors by nearly 22%, improving surgical predictability and reducing revision risks.

Compliance pressures and sustainability expectations are also reshaping the sector. Firms are committing to 20–30% reductions in implant-related waste by 2030, integrating recyclable alloys and traceable supply-chain systems. A measurable micro-scenario emerged in 2026, when a leading Japanese manufacturer achieved 18% production efficiency improvement through a hybrid titanium-ceramic additive manufacturing process.

Together, these strategic factors position the Orthopedic Implants Market as a pillar of resilience, regulatory alignment, and long-term sustainable growth—deeply intertwined with healthcare modernization and next-generation medical engineering.

The Orthopedic Implants Market is shaped by rapid technological transformation, evolving demographic needs, and continuous clinical innovation. Advancements in 3D printing, surgical robotics, and bioactive materials are driving product development, enabling implants that improve osseointegration, reduce recovery times, and support precision-based surgery. Increasing incidence of musculoskeletal disorders, including arthritis and trauma-related injuries, contributes to steady surgical demand worldwide. Regulatory frameworks are strengthening device traceability and lifecycle management, reinforcing patient safety standards. Meanwhile, emerging economies are expanding orthopedic care infrastructure, fostering greater consumption of advanced implants. These collective dynamics establish a strong foundation for sustained industry evolution.

The growing global adoption of minimally invasive orthopedic procedures is significantly influencing the Orthopedic Implants Market. Minimally invasive techniques result in reduced hospital stays, lower complication rates, and faster recovery, leading to higher acceptance among patients and healthcare providers. Statistics indicate that more than 40% of joint replacement surgeries worldwide now utilize minimally invasive approaches, improving surgical precision and reducing post-operative pain. Additionally, the integration of robotics and navigation systems enhances implant placement accuracy by up to 25%, making these procedures highly preferred. This shift is also driving demand for specialized implant designs tailored for smaller incisions, further accelerating the use of advanced orthopedic devices across hospitals and surgical centers.

Regulatory complexities remain a substantial restraint for the Orthopedic Implants Market, as stringent approval pathways extend product development timelines and increase compliance costs. Medical device regulations require extensive clinical validation, multi-phase testing, and ongoing quality audits, making market entry challenging for manufacturers. For instance, device approval cycles in major regions can range from 18 to 36 months, significantly delaying commercialization. Enhanced post-market surveillance requirements demand continuous monitoring and reporting of device performance, adding operational pressures. Additionally, the need to meet biocompatibility standards, sterility benchmarks, and long-term safety criteria can lead to redesigns or extended testing periods. These factors collectively slow innovation speed and limit rapid introduction of next-generation implants.

Rapid advancements in biomaterials present substantial opportunities for the Orthopedic Implants Market, enabling the development of lighter, more durable, and biologically compatible implants. Innovations in porous titanium, bioresorbable polymers, and hybrid ceramic composites improve osseointegration and reduce revision surgery rates. Studies indicate that next-generation porous implants can enhance bone-implant adherence by up to 30%, improving long-term clinical outcomes. The growing interest in surface-engineered coatings, such as antimicrobial layers and bioactive films, is further expanding design possibilities. These materials also support the development of patient-specific implants created through advanced additive manufacturing. As hospitals increasingly adopt precision-based orthopedic solutions, biomaterial innovation will drive new growth segments across trauma, spine, and joint reconstruction categories.

Rising raw material and manufacturing costs pose a significant challenge to the Orthopedic Implants Market, particularly due to dependency on specialized alloys, ceramics, and composite materials. Prices for medical-grade titanium and cobalt-chromium alloys have increased by 12–18% in recent years, elevating production expenses. Complex machining requirements and precision finishing processes also add labor and equipment costs, especially for high-tolerance implants. Additionally, additive manufacturing systems and robotics-driven production tools require substantial capital investment and maintenance. Supply chain disruptions further affect consistency in material availability, causing delays and cost variations. These pressures reduce profit margins and hinder the affordability of advanced orthopedic devices in price-sensitive markets.

Rising Adoption of Next-Generation Biomaterials: Innovations in surface-engineered coatings, including antimicrobial and bioactive layers, are improving implant performance significantly. New-age porous titanium structures show up to 30% stronger bone integration, while hybrid ceramic composites reduce wear rates by nearly 22%, enhancing device longevity across joint and spine applications.

Expansion of Robotics-Assisted Orthopedic Surgery: Robotics-enabled procedures grew by over 40% in major surgical centers between 2020 and 2024, improving accuracy and reducing surgical variability. Robotic navigation systems have achieved up to 25% improvement in implant alignment and lowered intraoperative errors, accelerating global adoption in knee and hip reconstruction.

Growth in Patient-Specific and 3D-Printed Implants: The number of healthcare facilities using additive manufacturing for custom orthopedic devices increased by nearly 60%, enabling better anatomical fit and reduced revision risk. Patient-specific implants support surgical efficiency improvements of 15–20%, especially in complex joint and craniofacial reconstructions.

Integration of Smart Implant Technologies: Sensor-enabled implants capable of tracking load, movement, and healing rates are gaining traction, with adoption increasing by 35% over the past three years. These devices enhance post-operative monitoring and enable data-driven rehabilitation, reducing complications by up to 18% in early recovery phases.

The Orthopedic Implants Market is segmented across product types (joint reconstruction – hip, knee, shoulder; spinal implants and fixation systems; trauma fixation devices; sports medicine implants; and emerging smart/ sensor-enabled implants), applications (primary and revision joint arthroplasty, spinal fusion and stabilization, fracture fixation, arthroscopic/sports procedures, and others), and end users (hospitals, ambulatory surgical centers (ASCs), orthopedic & specialty clinics, and rehabilitation centers). Decision-makers should note that segmentation drives procurement strategies, reimbursement patterns, and clinical pathways: product-type mix determines inventory and manufacturing complexity, application mix governs surgical-scheduling and clinical-service needs, and end-user distribution influences channel strategy and pricing. Large hospitals remain the primary procurement channel for complex implants and spinal systems; ASCs are expanding for routine hip/knee and sports procedures; and specialty clinics are important for device follow-ups and outpatient orthobiologic services. These segmentation dynamics shape manufacturing scale, regulatory submissions, and commercialization roadmaps for new implant technologies.

Joint reconstruction implants (hip and knee systems) are the leading product type, accounting for approximately 38–39% of the market in recent industry analyses; this prominence is tied to high global volumes of hip and knee arthroplasty procedures, extensive product portfolios from OEMs, and continuous incremental innovation in bearing surfaces and instrumentation. Smart and sensor-enabled implants (often described as “smart orthopedic implants”) are the fastest-growing product type — reflecting sensor integration, telemetry, and remote monitoring — with specialized market reports placing smart-implant growth rates well above mainstream segments (market forecasts show smart implants expanding at double-digit CAGRs; one recent estimate places the smart-implant CAGR near 17.3% over the coming decade). Other types (spinal implants, trauma fixation devices, shoulder/ankle/foot implants, orthobiologics) together represent the remaining ~61% of the market and serve clear niche and large-volume clinical needs (spine for chronic degenerative disease and trauma for acute fracture care).

Joint replacement (hip and knee arthroplasty) is the leading application area, representing roughly 38–39% of application-related demand, driven by high procedure volumes, aging populations, and expanding indications (primary and revision procedures). The fastest-growing application trajectory is visible in spinal implants and devices, which have shown strong expansion due to increasing diagnosis and surgical correction of degenerative and deformity conditions; spinal market analyses indicate meaningful near-term growth (single-region and global reports project mid-single-digit to low-double-digit improvements in spinal device uptake and spending). Other applications — trauma fixation, sports medicine arthroscopy, and smaller joint reconstructions — together comprise the remaining ~60% of application demand and remain essential to comprehensive orthopedics strategies. Consumer and clinical adoption signals: registry and surgical-data sources document large and rising procedure counts (the American Joint Replacement Registry has now captured millions of hip and knee arthroplasties in recent reporting cycles), and hospital systems are increasing robotic and navigation adoption for joint and spine procedures.

Hospitals are the leading end-user segment, holding the largest share of implant procurement (hospital end-use shares are commonly reported in the low-to-mid 60% range — for instance ~63–64% in several market breakdowns), reflecting their role in complex, inpatient orthopedics, trauma care, and spinal surgery. ASCs (ambulatory surgical centers) are the fastest-growing end-user channel for orthopedic implants as more routine hip, knee, and sports procedures shift to outpatient settings; ASC market expansion and case-shift trends show consistent year-on-year increases (ASC market/usage data show notable growth rates and capacity expansion). Other end users — orthopedic specialty clinics, outpatient procedural centers, and rehabilitation providers — make up the remaining ~36–37% of end-user demand and are increasingly important for outpatient follow-up, orthobiologics delivery, and specialized low-complexity cases. Adoption statistics and trends: registry and market-intelligence reporting indicate rising outpatient procedure volumes and rapid expansion of robotic-assisted and navigation-enabled programs in leading hospital systems; major registries document millions of recorded joint procedures in recent cycles, while ASC networks expanded case volumes markedly year-over-year.

North America accounted for the largest market share at 46% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Regional dynamics in the orthopedic implants sector reflect differences in demographic structures, healthcare modernization, and surgical procedure volumes. Europe held the second-largest share at 27%, supported by strong clinical infrastructure and a high penetration rate of joint reconstruction procedures. Asia Pacific captured 21%, driven by a rapidly aging population exceeding 670 million individuals and expanding implant manufacturing hubs in China and India. South America represented approximately 4% of demand, while the Middle East & Africa accounted for 3%, supported by ongoing investments in specialty hospitals. The regional landscape is shaped by variations in technology adoption, regulatory pathways, and surgical training density, with procedure volumes increasing by up to 18% annually in emerging economies compared to mature markets that report 3–6% growth.

North America held a 46% share of the global orthopedic implants market in 2024, supported by the region’s high surgical rate—exceeding 1.4 million hip and knee replacements annually. The sector is driven by strong demand from healthcare, sports medicine, trauma care, and military rehabilitation programs. Regulatory frameworks, including updated device traceability requirements and stricter biocompatibility standards, have encouraged the adoption of next-generation orthopedic solutions. Technological advancements such as robotic-assisted surgery, patient-specific implants, and AI-guided preoperative planning continue to gain momentum, with over 60% of large hospitals integrating digital surgical workflows. Local players are actively contributing to growth; for example, a leading U.S. manufacturer recently expanded its 3D-printed titanium implant line to support rising procedure volumes. Consumer behavior in the region shows a preference for high-reliability medical technologies, with adoption rates in healthcare significantly higher than global averages.

Europe accounted for 27% of global orthopedic implant demand in 2024, led by strong markets such as Germany, the UK, France, Italy, and Spain. The region’s demand is influenced by a high concentration of specialized orthopedic centers and some of the world’s largest surgeon networks. Regulatory bodies enforcing stringent quality and post-market surveillance requirements have encouraged broader adoption of advanced and traceable implant technologies. Sustainability initiatives are reshaping design and manufacturing, prompting increased use of recyclable materials and low-waste production methods. Europe is also becoming an early adopter of sensor-embedded implants and AI-supported diagnostic imaging systems. A regional manufacturer recently launched a modular implant platform tailored to minimally invasive procedures, strengthening local innovation. Consumer behavior indicates that European healthcare buyers prioritize transparency, predictability, and clinical validation, resulting in heightened demand for explainable and well-documented orthopedic solutions.

Asia Pacific held 21% of the global orthopedic implants market in 2024 and ranked as the fastest-growing region due to increasing surgical capacity and expanding healthcare access. China, India, Japan, South Korea, and Australia collectively represent more than 70% of regional consumption. The region is experiencing rapid infrastructure modernization, including new orthopedic specialty centers and high-volume joint replacement programs. Strong manufacturing ecosystems in China and India are enabling large-scale production of titanium, cobalt-chromium, and polymer-based implants while bringing down treatment costs. Innovation hubs in Singapore, Tokyo, and Bengaluru are accelerating advancements in 3D printing, bioresorbable materials, and robotics. A key regional producer recently introduced cost-effective trauma fixation systems tailored for emerging markets. Consumer behavior trends show that mobile-first healthcare adoption is rising significantly, with growing preference for digital consultation and preoperative planning tools, positioning Asia Pacific as a transformative growth engine.

South America accounted for 4% of the global orthopedic implants market in 2024, with Brazil, Argentina, Chile, and Colombia serving as major contributors. The region’s demand is influenced by the rise of private healthcare facilities, orthopedic trauma cases, and expanding insurance coverage. Investments in medical infrastructure and the growth of specialized surgery centers are improving access to joint reconstruction and minimally invasive orthopedic procedures. Government incentives encouraging foreign medical device imports and localized assembly are also improving supply chain efficiency. A notable regional manufacturer recently scaled production of polymer-based implants to meet increasing demand for cost-sensitive orthopedic solutions. Consumer behavior trends indicate a strong preference for localized language support and tailored medical education, particularly in patient-facing digital platforms, reflecting the region’s diverse linguistic landscape.

The Middle East & Africa held 3% of the global orthopedic implants market in 2024, supported by strong healthcare investments in the UAE, Saudi Arabia, South Africa, and Egypt. Regional demand is shaped by growth in construction, sports, and industrial sectors, which contribute to high trauma-related procedure volumes. Countries in the Gulf Cooperation Council are expanding advanced medical cities and partnering with global device manufacturers to introduce cutting-edge orthopedic technologies. Digital modernization, including AI-driven diagnostics and robotics-assisted surgery, is increasingly being integrated into premium care settings. A regional orthopedic device firm recently launched a new line of joint reconstruction components designed for high-temperature environments and longer durability. Consumer behavior trends reveal growing expectations for premium healthcare services and technology-enhanced treatments, particularly among urban populations.

United States – 38% Market Share: The U.S. leads the orthopedic implants market due to high procedure volumes, well-established clinical infrastructure, and strong adoption of advanced surgical technologies.

Germany – 12% Market Share: Germany maintains a dominant position in the orthopedic implants market because of its high surgeon density, strong manufacturing capabilities, and wide availability of specialized orthopedic centers.

The global Orthopedic Implants Market is moderately consolidated but remains highly competitive, with 20–25 major global competitors and a broader long tail of specialized regional and niche firms. The top 5 companies — Zimmer Biomet, Stryker Corporation, DePuy Synthes (part of J&J), Smith & Nephew and Medtronic plc — collectively control over 55% of the total global implant market.

These leading players maintain strong market positioning through broad product portfolios (joint, spine, trauma, extremities), global distribution networks, and continuous innovation. Recent years have seen aggressive strategic initiatives: for example, several top firms expanded their product lines to include robotics-assisted systems, smart implants with embedded sensors, and 3D-printed custom implants to address demand for better patient outcomes and personalized care. A number of smaller and mid-size firms have also grown — “other” manufacturers accounted for roughly 27% of hip and knee implant market volume in 2023, indicating substantial competition beyond the big five.

Innovation trends contribute heavily to competitive dynamics: firms are investing in additive manufacturing, bioactive materials, and digital surgical systems to differentiate. At the same time, regulatory standards, quality and safety compliance, and global distribution capability limit the effective number of competitors capable of achieving scale. The result is an industry where large incumbents dominate volume and broad global reach, while specialized or regional firms carve niches — for trauma fixation, orthopedic biologics, or cost-sensitive markets — creating a layered competitive environment.

Smith & Nephew

Medtronic plc

Globus Medical

Exactech, Inc.

Conmed Corporation

The orthopedic implants market is being reshaped by rapid technological innovation that touches design, manufacturing, surgery, and post-operative care. Key current and emerging technologies include robotics-assisted joint replacement, 3D-printed custom implants, sensor-embedded smart implants, advanced biomaterials, and digital surgical planning platforms. Robotics-assisted systems — such as robotic-arm guided tools — are becoming standard in joint replacement surgeries, offering high precision and reducing soft tissue damage, reoperation rates, and improving alignment accuracy. Many of these systems now support over 1 million procedures globally, illustrating widespread adoption and surgical community trust. Additive manufacturing (3D printing) enables patient-specific implant geometries and rapid production cycles. This is particularly valuable for complex reconstructions, anatomically unique patients, or regions where supply-chain flexibility is needed. The availability of 3D-printed spinal and extremity implants is enabling hospitals to reduce time-to-surgery and lower inventory burden. Smart implants — embedded with sensors and telemetry — are gaining traction. These devices offer real-time monitoring of load, alignment, and recovery metrics, enabling postoperative monitoring and data-driven rehabilitation. The move toward smart implants satisfies growing demand for long-term patient outcome tracking and personalized care pathways. Market reports show the smart-implant segment growing briskly in 2023–2024. Material innovation remains central: newer biomaterials, such as porous titanium for improved bone ingrowth, ceramics or ceramic-metal hybrids for reduced wear, and bioresorbable polymers for fracture fixation, are being adopted. These materials improve implant longevity, biocompatibility, and adaptability across patient groups. Digital surgical planning tools — combining imaging, AI-based preoperative simulations, and patient-specific analytics — enhance surgical decision-making and implant selection. These tools improve fit, reduce intraoperative time, and support precision medicine approaches in orthopedic surgery.

Overall, the convergence of robotics, additive manufacturing, smart implants, and advanced biomaterials marks a significant shift: toward personalized, data-driven, and quality-optimized orthopedic care. Decision-makers investing in R&D or selecting technology partners should prioritize multi-modal platforms, integration flexibility (across implant types), and long-term data capabilities.

In October 2024, Smith & Nephew launched its LEGION™ Hinged Knee System with proprietary OXINIUM™ technology in the United States, offering improved wear resistance and corrosion protection for revision knee procedures. Source: www.smith-nephew.com

In February 2024, Stryker Corporation showcased the expansion of its MAKO SmartRobotics™ joint-replacement platform and introduced a new Triathlon® Hinge system aimed at improving outcomes in complex knee revision surgeries. Source: www.stryker.com

In 2024, Medtronic plc strengthened its spinal implant portfolio by advancing development of 3D-printed titanium interbody fusion devices and promoting minimally invasive spine surgery solutions globally.

In 2023–2024, Zimmer Biomet expanded its connected orthopedic ecosystem by integrating sensor-enabled implants (smart knee systems) along with digital surgical workflow tools, reflecting a shift toward data-driven postoperative monitoring and personalized patient care.

The Orthopedic Implants Market Report covers a broad and detailed analysis of the global market, encompassing multiple dimensions: product types (joint reconstruction — hip, knee, shoulder; spinal implants and fixation systems; trauma and fracture fixation devices; extremities implants; and emerging smart/sensor-enabled implants), applications (primary and revision arthroplasty, spinal fusion and stabilization, fracture repair, arthroscopic and sports-medicine procedures, reconstructive and extremities surgery), and end-users (hospitals, ambulatory surgical centers, orthopedic clinics, rehabilitation centers). It also segments the market geographically across major regions — North America, Europe, Asia-Pacific, South America, Middle East & Africa — providing share, volume, and growth dynamics for each region.

The report additionally focuses on technology trends: additive manufacturing (3D printing), robotics-assisted surgical systems, smart implants, advanced biomaterials, and digital surgical planning platforms. It evaluates regulatory and compliance frameworks, material and manufacturing innovations, and emerging sub-segments such as sensor-embedded implants, bioresorbable fixation systems, and personalized/customized implant solutions.

Furthermore, the report explores market dynamics and competitive environment, profiling leading global players, their strategic initiatives (product launches, acquisitions, R&D investments), and the broader competitive ecosystem including mid-size and niche regional manufacturers. For decision-makers and industry professionals, the report offers insights into adoption patterns, technology readiness, regional regulatory hurdles, manufacturing capacity, and future opportunity zones — including growth in emerging markets, demand for minimally invasive procedures, and adoption of smart and patient-specific implants. The scope thus ensures a holistic view of both current operations and future trajectories across regions, technologies, applications, and business models.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 5,590.0 Million |

| Market Revenue (2032) | USD 7,733.1 Million |

| CAGR (2025–2032) | 4.14% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Key Players Analyzed | Zimmer Biomet, Stryker, DePuy Synthes (J&J), Smith & Nephew, Medtronic, Globus Medical, Exactech, ConMed |

| Customization & Pricing | Available on Request (10% Customization Free) |