Reports

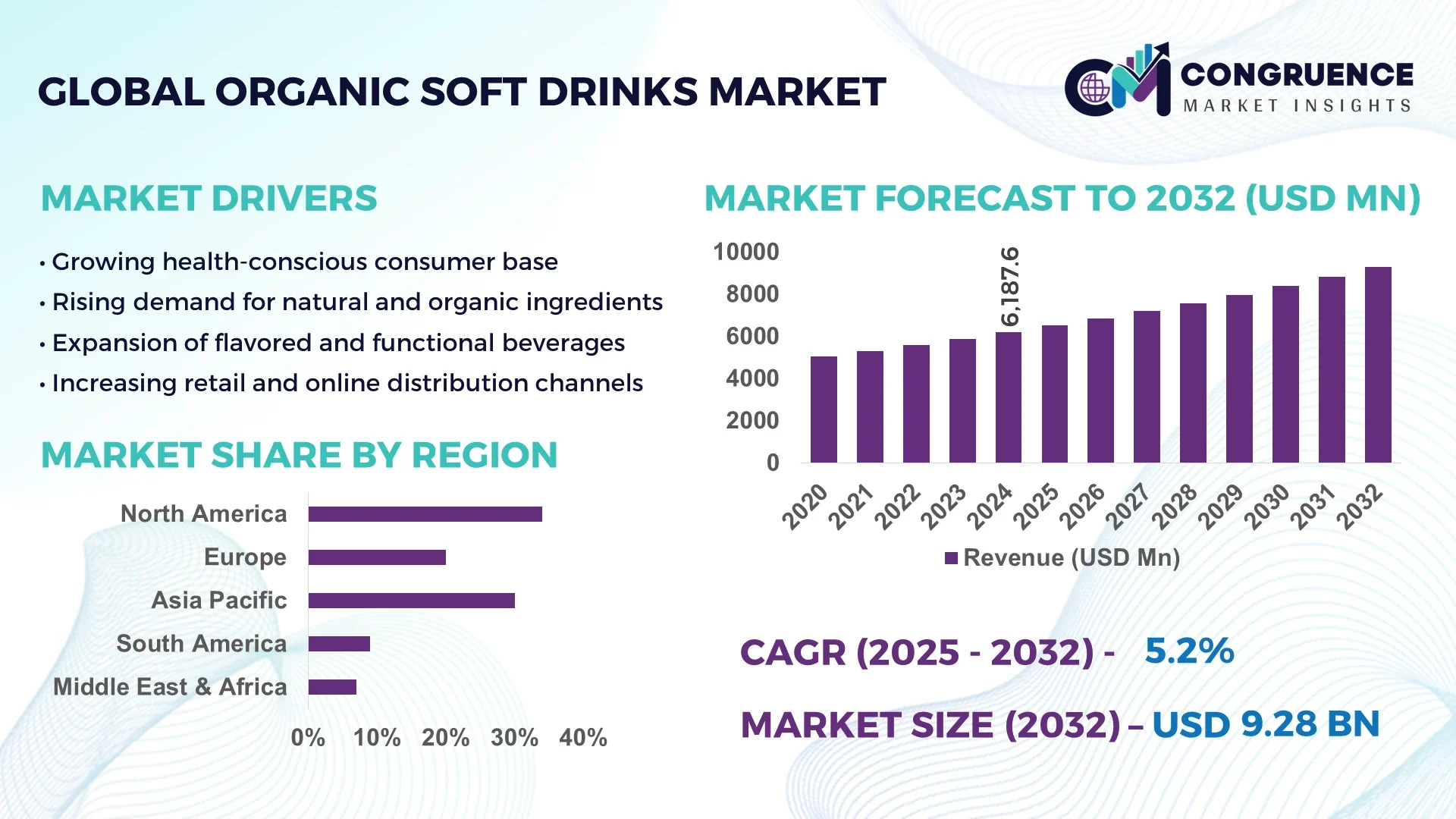

The Global Organic Soft Drinks Market was valued at USD 6187.58 Million in 2024 and is anticipated to reach a value of USD 9282.11 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032. Rising consumer focus on clean-label, chemical-free beverages is fueling steady growth across global markets.

The United States demonstrates significant production capacity for organic soft drinks with advanced automated bottling and cold-pasteurization systems. Investments in U.S. organic beverage manufacturing exceeded USD 200 million in 2023, enabling large-scale production of organic carbonated drinks, botanical infusions, and fruit-based blends. Technological advancements such as high-pressure processing (HPP), natural preservation methods, and zero-waste packaging support quality retention and sustainability. Consumer adoption is strong, with more than 70% of U.S. shoppers purchasing organic soft drinks within the last year and fruit-focused beverages representing over 40% of new product launches.

Market Size & Growth: USD 6.19 Billion in 2024 projected to reach USD 9.28 Billion by 2032 with a CAGR of 5.2%, supported by rising demand for healthier, clean-label drinks.

Top Growth Drivers: Health-conscious consumption 65%, preference for chemical-free ingredients 50%, sustainability adoption 45%.

Short-Term Forecast: By 2028, organic ingredient costs expected to decline by 8–10% with shelf-life performance gains of about 20% using HPP technology.

Emerging Technologies: High-pressure processing for natural preservation, plant-based sweeteners such as stevia and monk fruit, and biodegradable smart packaging.

Regional Leaders: North America projected at ~USD 3.5 Billion by 2032 with strong demand for organic sodas; Asia-Pacific at ~USD 2.8 Billion driven by urban middle-class consumers; Western Europe at ~USD 2.0 Billion supported by regulatory incentives and premium positioning.

Consumer/End-User Trends: Preference for zero-sugar, botanical-infused beverages and functional soft drinks enriched with vitamins and antioxidants.

Pilot or Case Example: In 2024, a U.S. beverage producer introduced HPP processing, reducing spoilage by 25% and extending shelf life by 15% for organic fruit drinks.

Competitive Landscape: Market leader holds about 20–25% share with notable competitors including Honest Tea, Suja Life, Galvanina, Evolution Fresh, and Hain Celestial Group.

Regulatory & ESG Impact: Stricter global organic certification standards, sugar-tax initiatives, and incentives for sustainable packaging and farming practices.

Investment & Funding Patterns: Approximately USD 150–200 Million invested recently in production facilities and ingredient supply chains, with venture funding increasing nearly 30% annually.

Innovation & Future Outlook: Growth in botanical infusions, adaptogen-enhanced soft drinks, digital traceability through blockchain, and zero-waste processing methods.

Key industry sectors encompass organic carbonated sodas, fruit-based soft drinks, and herbal or botanical beverages. Fruit-centric drinks hold the largest share of new product introductions, while carbonated organic blends are innovating with natural sweeteners and low-sugar formulas. Technological progress includes probiotics, adaptogens, and lightweight recyclable packaging. Regulatory drivers—such as stricter organic standards, sugar-content labeling, and eco-packaging incentives—shape industry dynamics. Environmental and economic factors, including rising disposable income and heightened pesticide concerns, encourage adoption across North America, Asia-Pacific, and Western Europe. Emerging trends highlight expanding e-commerce channels, premium wellness-oriented formulations, and strategic partnerships between beverage brands and certified organic farms to secure sustainable ingredient supply and maintain cost efficiency.

The strategic relevance of the Organic Soft Drinks Market lies in its ability to merge health-focused consumer preferences with sustainable production practices, positioning it as a key segment in the global beverage industry. Advanced manufacturing systems such as High-Pressure Processing (HPP) deliver a 25% improvement in nutrient retention compared to conventional thermal pasteurization, enabling producers to maintain natural flavors and extend shelf life without synthetic additives. North America dominates in production volume, while Europe leads in adoption with nearly 68% of beverage enterprises integrating certified organic soft drinks into their product lines.

By 2027, AI-driven supply chain optimization is expected to cut ingredient procurement costs by approximately 12%, improving operational efficiency and reducing time-to-market. Firms are committing to ESG metrics including a 40% packaging waste reduction by 2030, supported by recyclable and biodegradable packaging innovations. In 2024, a leading Japanese beverage company achieved a 30% water usage reduction through AI-enabled real-time monitoring and smart bottling systems, demonstrating measurable sustainability gains. Looking ahead, the Organic Soft Drinks Market is set to become a pillar of resilience, compliance, and sustainable growth, leveraging technology, regional strengths, and rigorous environmental standards to meet evolving global consumer demands.

The Organic Soft Drinks Market is driven by the rising demand for clean-label, chemical-free beverages and increasing consumer focus on wellness-oriented products. Expanding urban populations and higher disposable incomes foster demand for premium organic drinks, while global sustainability goals encourage producers to adopt eco-friendly packaging and responsible sourcing. Technological advancements such as AI-powered supply chain management and smart packaging enhance product traceability and shelf-life monitoring. Regulatory frameworks requiring stricter organic certification and accurate labeling reinforce product integrity and build consumer trust. This market demonstrates agility in adapting to regional preferences, from fruit-based drinks in North America to botanical-infused beverages in Europe and Asia-Pacific, creating a robust and diversified growth environment.

Increasing health consciousness among consumers has significantly boosted demand for organic beverages free from artificial additives and pesticides. Surveys indicate that over 70% of millennials and Gen Z buyers actively seek natural, low-sugar drinks, supporting a shift toward premium organic soft drinks. This heightened awareness stimulates innovation in functional ingredients such as probiotics, adaptogens, and vitamin-enriched formulations. Retail expansion through health-focused grocery chains and online channels accelerates availability, while supportive government programs promoting organic farming provide steady raw material supply. Together, these factors create strong momentum for sustained market expansion.

Organic soft drinks face elevated production costs due to stringent certification requirements, premium ingredient sourcing, and specialized processing technologies like HPP. Organic raw materials can cost 20–30% more than conventional inputs, challenging profit margins for manufacturers. Seasonal fluctuations in organic fruit supply also add to price volatility. Compliance with strict labeling and environmental regulations demands additional investment in quality assurance and traceability systems. These cost pressures can limit market entry for small producers and slow scaling efforts for established brands, potentially restraining the pace of growth despite strong consumer demand.

The push for eco-friendly packaging presents significant growth opportunities. Biodegradable bottles, plant-based plastics, and refillable container systems align with global sustainability goals and appeal to environmentally conscious consumers. Market studies show that products with certified sustainable packaging experience up to 35% higher consumer preference compared to conventional packaging. Governments are introducing incentives and tax benefits for companies adopting recyclable materials, further enhancing profitability. Brands leveraging innovative packaging not only reduce their environmental footprint but also strengthen brand equity and market competitiveness, creating a win-win scenario for manufacturers and consumers alike.

The Organic Soft Drinks Market relies on intricate international supply chains for organic ingredients such as specialty fruits, herbs, and natural sweeteners. Disruptions caused by climate variability, geopolitical tensions, and transportation delays can lead to shortages and inconsistent pricing. Maintaining strict organic certification across multiple sourcing regions adds complexity, requiring meticulous documentation and audits. Currency fluctuations further impact cost stability, making forecasting and inventory management difficult. These challenges necessitate advanced logistics planning and investment in diversified sourcing strategies to maintain consistent product availability and meet the growing global demand.

Premium Botanical Infusions Accelerating Demand: Premium botanical infusions are transforming consumer preferences, with sales of herbal-based organic soft drinks increasing by 34% in 2024 compared to 2022. Products infused with hibiscus, elderflower, and chamomile now represent 22% of new launches. Manufacturers report a 28% improvement in repeat purchases when botanical blends are paired with natural sweeteners, reflecting rising interest in functional wellness beverages.

Zero-Sugar and Low-Calorie Formulations Expanding Rapidly: Demand for zero-sugar and low-calorie organic soft drinks grew 31% year-over-year, supported by advanced natural sweeteners that deliver 15% better taste stability than earlier formulations. In North America, 47% of consumers under 35 actively seek beverages with less than 5 grams of sugar per serving, reinforcing strong momentum for naturally sweetened drinks without artificial additives.

Smart Packaging and Digital Traceability Adoption: Integration of QR-code enabled smart packaging rose 26% in 2024, allowing consumers to verify organic certifications and ingredient origins instantly. Brands using digital traceability report a 20% decrease in counterfeit product risks and a 12% rise in consumer trust scores, strengthening brand credibility and market differentiation.

Functional Nutrient Fortification Driving Innovation: Fortified organic soft drinks containing vitamins, probiotics, or adaptogens recorded a 29% jump in global launches over the past two years. Products with added vitamin C achieved 18% higher shelf velocity, while probiotic blends delivered a 25% improvement in digestive health claims acceptance, reflecting consumer focus on immune support and overall wellness.

The Organic Soft Drinks Market is segmented by type, application, and end-user profiles, each reflecting unique demand drivers and innovation trends. Product types include carbonated organic sodas, fruit-based blends, herbal or botanical infusions, and functional nutrient-enriched drinks. Applications span retail distribution, foodservice channels, and specialized wellness outlets, while end-users range from supermarkets and cafés to health-oriented specialty stores and online marketplaces. Fruit-based beverages maintain strong appeal among younger demographics, while functional drinks gain traction in wellness centers and fitness hubs. This diversified segmentation highlights the market’s adaptability to shifting consumer preferences and regional consumption patterns, creating robust opportunities for industry stakeholders.

Carbonated organic soft drinks lead the market with approximately 38% share, driven by consumer demand for refreshing beverages enhanced with natural sweeteners and clean-label ingredients. Fruit-based organic drinks follow closely at 30%, buoyed by innovation in exotic flavors such as mango-ginger and blueberry-lavender. Herbal and botanical infusions hold 20% share, appealing to consumers seeking functional benefits like relaxation and digestive health. Functional nutrient-enriched drinks, though currently at 12% share, are the fastest-growing segment with a projected double-digit annual growth rate of about 11% over the next few years, propelled by rising health-conscious lifestyles and interest in immunity support. Other niche types, including sparkling teas and kombucha-based sodas, collectively contribute around 10% of the market.

Retail distribution dominates with nearly 45% share, supported by extensive supermarket and hypermarket penetration that ensures broad consumer access to organic soft drinks. Foodservice, including cafés, restaurants, and quick-service chains, accounts for about 28%, benefiting from the rising trend of on-the-go consumption. E-commerce and online specialty health platforms represent 17% and are the fastest-growing application, with an estimated 12% annual increase fueled by subscription-based delivery models and digital marketing campaigns. Wellness-focused venues such as gyms and nutrition centers make up the remaining 10%, serving health-conscious buyers seeking functional beverages.

In 2024, over 42% of urban millennials globally reported purchasing organic soft drinks through mobile apps at least once a month, reflecting shifting buying behaviors.

Supermarkets and hypermarkets remain the leading end-user segment with about 40% market share, leveraging their wide distribution networks and ability to offer diverse product assortments. Cafés and specialty beverage shops hold roughly 25% share, catering to premium and artisanal drink seekers. The fastest-growing end-user segment is online and direct-to-consumer channels, expanding at an estimated 13% annual rate, supported by subscription boxes and influencer-driven marketing. Other contributors include fitness centers, spas, and hospitality chains, which collectively account for 15% and attract consumers interested in wellness-focused options.

Consumer adoption reflects strong digital engagement: in 2024, 39% of Gen Z consumers in the United States reported preferring home delivery for organic beverages, and 33% in Europe subscribed to monthly organic drink plans.

North America accounted for the largest market share at 34% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Europe followed closely with a 28% share, while Asia-Pacific captured 22% of the total market volume. South America represented 9% and the Middle East & Africa contributed around 7%. In North America, the United States alone represented 24% of global consumption, supported by more than 1,200 certified organic beverage plants. Europe’s key markets—Germany, the United Kingdom, and France—collectively accounted for over 18% of worldwide organic soft drink sales. Asia-Pacific recorded a surge in e-commerce transactions, with mobile-based purchases of organic beverages growing 32% year-over-year, highlighting the region’s digital transformation and expanding consumer base.

North America held about 34% of the global Organic Soft Drinks Market in 2024, driven by strong demand from the health and wellness sector and robust retail distribution networks. Key industries such as hospitality, quick-service restaurants, and premium grocery chains fuel consumption. Regulatory frameworks like the USDA Organic certification strengthen consumer confidence and ensure quality standards. Advanced manufacturing technologies including high-pressure processing and AI-enabled inventory management improve efficiency and reduce waste. A notable player, Honest Tea, continues to expand cold-brewed organic soft drink lines across U.S. supermarkets, aligning with consumer preferences for clean-label beverages. Regional buyers show high adoption of low-sugar and functional drinks, with 48% of millennials preferring beverages with added vitamins and adaptogens.

Europe captured about 28% market share in 2024, led by Germany, the United Kingdom, and France as primary consumers of organic beverages. The European Food Safety Authority enforces strict labeling standards, while the EU Green Deal encourages eco-friendly packaging and carbon-reduction initiatives. Technological adoption is strong, with digital traceability systems and biodegradable bottle manufacturing gaining traction. Italian brand Galvanina has introduced plant-based PET bottles, reducing plastic usage by 25%. Consumer behavior favors botanical-infused, low-calorie drinks, with 52% of European shoppers choosing beverages with natural sweeteners, reflecting a strong alignment with health and sustainability goals.

Asia-Pacific represented approximately 22% of the global market volume in 2024, with China, Japan, and India as top consuming nations. Expanding beverage manufacturing infrastructure in China and rising disposable incomes in India fuel rapid adoption. E-commerce plays a pivotal role, with mobile-based organic soft drink purchases increasing 32% year-over-year. Innovation hubs in Japan and South Korea lead the way in smart packaging technologies and AI-driven supply chain optimization. A key player in Japan introduced probiotic-infused organic sodas that improved shelf life by 15%. Regional consumers demonstrate a strong preference for fruit-based and functional drinks, particularly those supporting immunity and digestive health.

South America accounted for about 9% of the global market in 2024, with Brazil and Argentina as major contributors. Government incentives promoting organic agriculture and favorable trade agreements support local production and export activities. Regional beverage companies are investing in solar-powered bottling facilities to reduce energy costs by 18%. Brazilian consumers exhibit rising interest in herbal-infused drinks, and 41% of urban households report monthly purchases of organic soft drinks through supermarkets and online platforms. Local brands continue to diversify product offerings, with several introducing zero-sugar fruit sodas to meet the growing health-conscious population.

The Middle East & Africa region represented nearly 7% of global market share in 2024, with notable demand from the UAE, Saudi Arabia, and South Africa. Economic diversification and modernization initiatives drive investment in food and beverage manufacturing, while halal-certified organic drinks gain popularity. Governments are encouraging sustainable packaging and recycling targets, aiming for a 35% reduction in plastic waste by 2030. Local players in the UAE are adopting smart bottling systems to improve production efficiency by 20%. Consumers in this region increasingly favor premium organic soft drinks with natural flavors and functional benefits, reflecting a shift toward wellness-oriented lifestyles.

United States – 24% Market Share: Strong production capacity supported by advanced manufacturing infrastructure and high consumer demand for clean-label beverages.

Germany – 12% Market Share: Robust regulatory framework and widespread adoption of sustainable packaging solutions drive significant consumption of organic soft drinks.

The Organic Soft Drinks market in 2024 remained moderately fragmented, with over 220 active competitors operating across more than 40 countries. The top five companies collectively accounted for approximately 38% of the global market share, reflecting a dynamic competitive environment where regional players and global giants coexist. Strategic initiatives such as cross-border partnerships, product diversification, and eco-friendly packaging innovations have intensified competition. For example, more than 60 product launches featuring low-sugar and functional ingredients were recorded globally in 2024. Mergers and acquisitions also surged, with at least 12 notable deals aimed at expanding distribution networks and strengthening supply chains. Innovation trends focus on plant-based sweeteners, AI-driven supply chain optimization, and biodegradable packaging, which are reshaping consumer expectations and driving differentiation. Companies are increasingly investing in digital marketing and direct-to-consumer e-commerce strategies to capture niche health-conscious demographics, ensuring that market positioning hinges on sustainability credentials and continuous product innovation.

Danone S.A.

Keurig Dr Pepper Inc.

Hain Celestial Group

Honest Tea

Fentimans Ltd

Belvoir Farm

Purity Organic

Technological advancements are transforming the Organic Soft Drinks market by enhancing production efficiency, ingredient innovation, and sustainable packaging. Automated bottling systems now achieve production speeds exceeding 1,200 bottles per minute while reducing energy use by up to 18%, enabling large-scale output without compromising product integrity. High-pressure processing (HPP) technology is increasingly adopted to maintain natural flavors and nutrients while extending shelf life by 25–30% compared to conventional pasteurization.

Ingredient innovation plays a pivotal role, with precision fermentation allowing the creation of natural sweeteners and functional additives that reduce sugar content by up to 40% while maintaining taste. Digital flavor profiling systems powered by AI are used to analyze consumer preferences across more than 50 markets, enabling rapid development of region-specific formulations.

Sustainable packaging is another core focus. Plant-based PET bottles have achieved a 30% lower carbon footprint, while biodegradable caps and labels are gaining traction. Companies are also integrating smart packaging features, including QR codes that track supply chains and provide product transparency to millions of consumers. Blockchain-enabled traceability systems ensure authenticity of organic certifications, reducing fraudulent labeling cases by approximately 15% in 2024. These combined technologies create a competitive edge and meet the rising global demand for environmentally responsible, health-focused beverages.

• In February 2024, PepsiCo expanded its organic beverage line with a new low-sugar sparkling drink infused with botanical extracts, rolling out across 15 countries and targeting a 20% increase in health-conscious consumer reach. Source: www.pepsico.com

• In September 2024, Nestlé introduced a fully recyclable plant-based PET bottle for its organic iced tea brand, reducing packaging-related emissions by 28% and piloting the product in Germany and France. Source: www.nestle.com

• In June 2023, The Coca-Cola Company launched a blockchain-based traceability platform across North America to verify organic ingredient sourcing, improving supply chain transparency for over 500 million liters of beverages annually.

• In November 2023, Danone unveiled an AI-driven production system in its European facilities, cutting water usage by 22% and increasing production efficiency by 15% for its range of organic soft drinks. Source: www.danone.com

The Organic Soft Drinks Market Report provides a comprehensive analysis of market dynamics across product types, applications, and end-user categories, offering strategic insights for stakeholders and decision-makers. Covering all major geographies—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—the report details consumption trends, production capacities, and distribution networks influencing market growth across more than 40 countries. The report segments the market by product type, including sparkling beverages, juices, energy drinks, and specialty botanical blends, each assessed for technological adoption and consumer demand patterns. It further explores application areas such as retail, foodservice, and online channels, providing data-backed insights into regional adoption levels and evolving consumer behaviors.

Technological analysis highlights key innovations like AI-based flavor development, blockchain traceability, and biodegradable packaging, detailing their impact on operational efficiency and sustainability. End-user insights span from large beverage conglomerates to emerging artisanal brands, capturing niche trends such as functional wellness drinks and low-sugar formulations that are reshaping product portfolios. By combining detailed segmentation with forward-looking insights into supply chains, regulatory landscapes, and consumer trends, the report serves as an essential resource for businesses seeking to enter or expand in the global Organic Soft Drinks market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6187.58 Million |

|

Market Revenue in 2032 |

USD 9282.11 Million |

|

CAGR (2025 - 2032) |

5.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

The Coca-Cola Company, PepsiCo Inc., Nestlé S.A., Danone S.A., Keurig Dr Pepper Inc., Hain Celestial Group, Honest Tea, Fentimans Ltd, Belvoir Farm, Purity Organic |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |