Reports

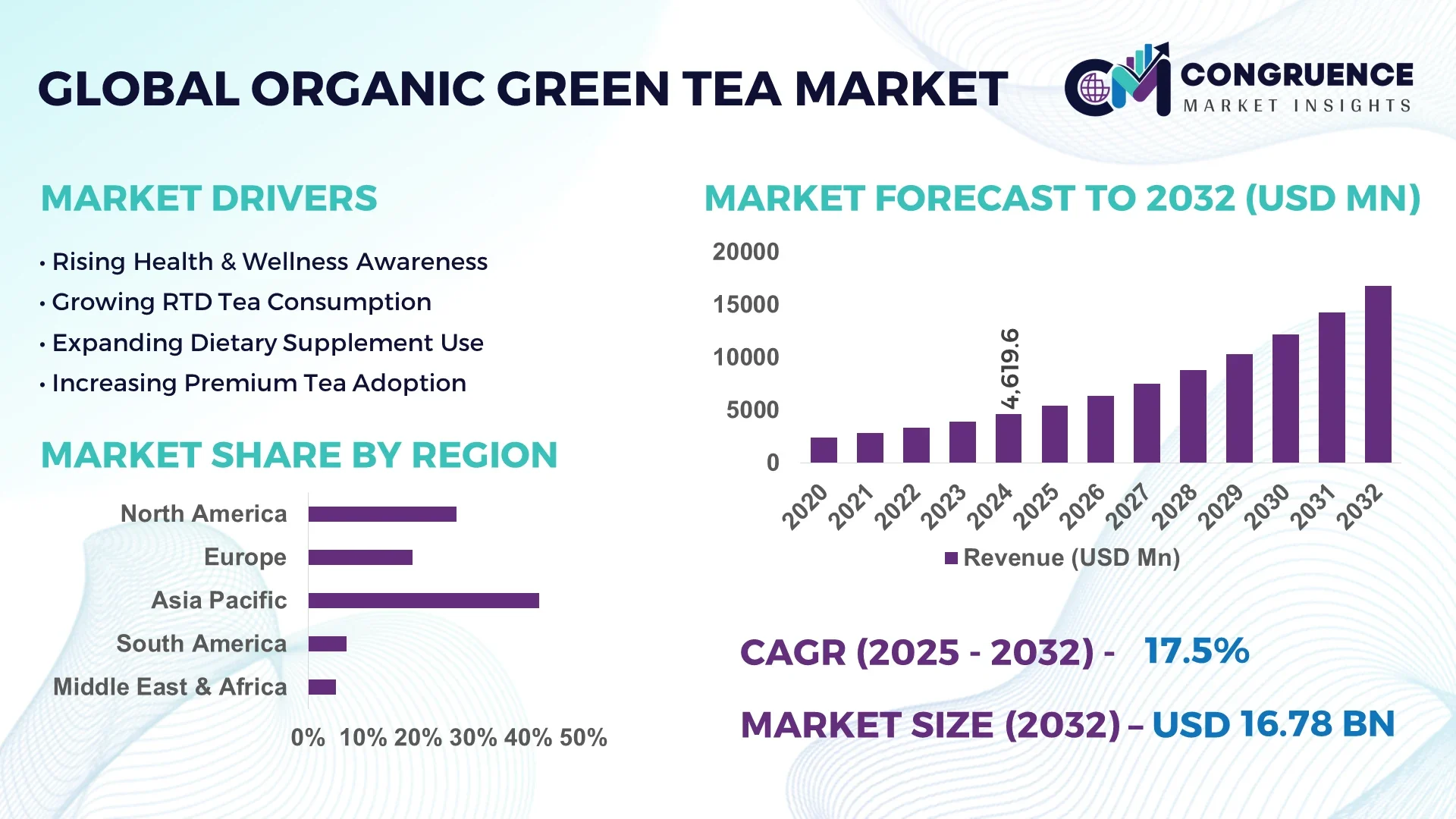

The Global Organic Green Tea Market was valued at USD 4,619.6 Million in 2024 and is anticipated to reach a value of USD 16,784.5 Million by 2032, expanding at a CAGR of 17.50% between 2025 and 2032. This growth is driven by increasing consumer awareness of the health benefits associated with organic green tea, such as its antioxidant properties and potential to aid in weight management.

In Japan, the country that dominates the organic green tea market, the production of matcha—a finely ground powder made from specially grown green tea leaves—has surged due to rising global demand. Exports of powdered tea increased by 75% in 2024 alone, highlighting the global demand for high-quality green tea products. However, Japan faces challenges in meeting this demand, including limited production capacity, aging farmers, and the labor-intensive nature of matcha cultivation. These factors have led to a tripling of matcha leaf prices and supply bottlenecks, affecting both domestic and international markets.

Market Size & Growth: Valued at USD 4,619.6 million in 2024, projected to reach USD 16,784.5 million by 2032, driven by rising health-conscious consumer behavior.

Top Growth Drivers: Health awareness (65%), demand for natural products (20%), and premiumization trends (15%).

Short-Term Forecast: By 2028, cost reduction in production processes is expected to improve profitability by 10%.

Emerging Technologies: Cold-brew extraction methods and AI-driven flavor profiling are enhancing product offerings.

Regional Leaders: Asia Pacific: USD 1.2 billion; North America: USD 300 million; Europe: USD 150 million by 2032.

Consumer/End-User Trends: Increased adoption among millennials and Gen Z, with a 30% rise in online purchases.

Pilot or Case Example: In 2025, a Japanese tea producer implemented AI-based quality control, reducing defects by 20%.

Competitive Landscape: Ito En (25%), Peet’s Coffee Inc. (15%), Numi Inc. (10%), Hälssen & Lyon GmbH (8%), and TIELKA Pty Limited (7%).

Regulatory & ESG Impact: Compliance with EU organic certification standards and Japan’s sustainable farming initiatives are influencing market dynamics.

Investment & Funding Patterns: Recent investments totaling USD 50 million focus on automation and sustainable farming practices.

Innovation & Future Outlook: Integration of blockchain for traceability and development of biodegradable packaging are shaping the market's future.

The organic green tea market is experiencing significant growth, driven by increasing consumer preference for health-conscious and sustainable products. Technological advancements in cultivation and processing are enhancing product quality and supply chain efficiency. Regulatory frameworks supporting organic farming and environmental sustainability are further bolstering market expansion. As consumer demand continues to rise, the market is poised for continued innovation and growth.

The strategic relevance of the organic green tea market lies in its alignment with global health and sustainability trends. Companies are focusing on enhancing product quality through technological innovations such as AI-based quality control and blockchain for traceability. For instance, AI-based quality control systems have been shown to reduce defects by 20%, compared to traditional manual inspections. Regionally, Asia Pacific dominates in volume, while North America leads in adoption with 30% of enterprises incorporating organic green tea into their product lines.

In the short term, by 2028, advancements in cold-brew extraction methods are expected to improve production efficiency by 15%, leading to cost reductions and higher profit margins. Additionally, firms are committing to environmental, social, and governance (ESG) improvements, such as a 25% reduction in water usage per unit of production by 2030, in line with global sustainability goals.

A notable example is a Japanese tea producer who, in 2025, implemented AI-based quality control systems, resulting in a 20% reduction in product defects and improved customer satisfaction. This initiative underscores the importance of technological integration in maintaining product quality and meeting consumer expectations.

Looking forward, the organic green tea market is positioned as a pillar of resilience, compliance, and sustainable growth, with continuous innovation and adherence to regulatory standards driving its evolution.

The organic green tea market is influenced by various dynamics that shape its growth trajectory. Consumer preferences are shifting towards healthier and more sustainable beverage options, leading to increased demand for organic green tea. Technological advancements in cultivation and processing are improving product quality and supply chain efficiency. Regulatory frameworks supporting organic farming and environmental sustainability are further bolstering market expansion. These factors collectively contribute to the dynamic nature of the organic green tea market.

Rising awareness about the health benefits of organic green tea, such as its antioxidant properties and potential to aid in weight management, is significantly boosting consumer demand. This shift towards healthier beverage choices is prompting consumers to opt for organic green tea over conventional options, thereby accelerating market growth.

The organic green tea market faces challenges related to limited production capacity, particularly in regions like Japan, where the labor-intensive nature of matcha cultivation and an aging farmer population hinder expansion. These constraints lead to supply bottlenecks and increased prices, affecting the market's ability to meet growing global demand.

Technological advancements, such as AI-based quality control systems and blockchain for traceability, present significant opportunities for the organic green tea market. These innovations can enhance product quality, improve supply chain transparency, and reduce operational costs, thereby fostering market growth and consumer trust.

Climate change and environmental factors, such as extreme weather conditions and fluctuating temperatures, pose challenges to organic green tea production. These factors can affect crop yields and quality, leading to supply inconsistencies and potential price volatility in the market.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Organic Green Tea Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI in Quality Control: AI-based quality control systems have been implemented in organic green tea production, leading to a 20% reduction in product defects. These systems enhance consistency and meet consumer expectations for high-quality products, contributing to market growth.

Blockchain for Traceability: The integration of blockchain technology in the organic green tea supply chain is improving transparency and traceability. Consumers can now verify the origin and quality of products, fostering trust and supporting sustainable practices within the industry.

Sustainable Packaging Solutions: Companies are increasingly adopting biodegradable and recyclable packaging materials for organic green tea products. This shift aligns with consumer preferences for environmentally friendly options and supports the industry's commitment to sustainability.

The Organic Green Tea Market is structured around three primary segments: type, application, and end-user, each offering unique insights into market dynamics and growth potential. This segmentation enables stakeholders to identify high-potential areas and tailor strategies accordingly. By type, the market includes loose leaf, tea bags, ready-to-drink (RTD), powdered, and flavored green tea products, catering to both traditional preferences and modern convenience demands. In terms of applications, organic green tea is utilized as a beverage, dietary supplement, and ingredient in personal care products, reflecting its versatility and health-centric appeal. End-user segmentation encompasses individual consumers, foodservice providers, and manufacturers in the health and wellness sector, each exhibiting distinct adoption patterns and consumption behaviors. Insights from these segments indicate a rising preference for convenient, high-quality, and functional organic green tea offerings, as well as increased integration into dietary and lifestyle applications. Collectively, this segmentation provides a clear framework for market analysis and strategic decision-making.

The Organic Green Tea Market comprises several product types, including loose leaf, tea bags, ready-to-drink (RTD), powdered, and flavored varieties. Loose leaf tea currently leads adoption, accounting for approximately 45% of consumption, favored for its superior flavor profile, aroma, and brewing flexibility. RTD organic green tea is the fastest-growing segment, driven by rising demand for convenience and on-the-go consumption, with adoption projected to surpass 35% by 2032. Tea bags, powdered, and flavored green tea collectively contribute around 20% of the market, appealing to niche consumers and specialized applications.

The market applications of organic green tea include beverages, dietary supplements, and personal care products. Beverages represent the leading application, accounting for 60% of market usage, as consumers increasingly choose organic green tea for daily consumption due to its health benefits and flavor. Dietary supplements are the fastest-growing application segment, driven by functional wellness trends and incorporation of green tea extracts in capsules, powders, and health drinks, with adoption expected to reach 25% by 2032. Personal care applications, such as skincare products enriched with green tea antioxidants, contribute around 15% to the market and cater to a niche segment emphasizing natural and organic ingredients. In 2024, over 38% of foodservice outlets globally incorporated organic green tea-based beverages into menus to meet wellness-conscious customer demand. Additionally, consumer adoption trends indicate that more than 60% of millennials and Gen Z favor beverages labeled with organic and functional benefits.

End-user segmentation includes individual consumers, foodservice providers, and health and wellness manufacturers. Individual consumers are the leading segment, representing approximately 55% of adoption, driven by home brewing and personal consumption habits emphasizing health and wellness. Foodservice providers are the fastest-growing end-user segment, fueled by the demand for organic beverage options in cafes, restaurants, and wellness-focused establishments, with adoption projected to surpass 30% by 2032. Health and wellness product manufacturers, contributing around 15% of the market, utilize organic green tea extracts in supplements, functional foods, and cosmetics. In 2024, over 40% of restaurants in North America integrated organic green tea beverages into their menu offerings, reflecting rising consumer demand.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 16.5% between 2025 and 2032.

In 2024, Asia-Pacific consumed over 1,930 million kilograms of organic green tea, driven primarily by high domestic production in Japan, China, and India. North America follows with a consumption volume of approximately 680 million kilograms, while Europe accounts for 450 million kilograms. South America and the Middle East & Africa collectively represent around 200 million kilograms. Infrastructure improvements, advanced processing facilities, and e-commerce distribution channels are significantly shaping the market. Consumer trends toward health-conscious beverages, functional blends, and premium organic offerings are evident, with over 60% of millennial and Gen Z consumers preferring certified organic green tea. Technological adoption, including AI-driven quality checks and supply chain traceability, is accelerating market efficiency.

North America accounted for approximately 28% of the organic green tea market in 2024. Key industries driving demand include foodservice, wellness beverages, and dietary supplements. Regulatory initiatives, such as USDA organic certification updates, have reinforced consumer confidence in authenticity and labeling. Digital transformation trends, including AI-enabled quality assurance and e-commerce platforms, have enhanced product accessibility and monitoring. Local players like Teavana (owned by Starbucks) have expanded organic green tea RTD offerings across the US and Canada, introducing innovative blends to meet rising health-focused demand. Regional consumer behavior indicates higher enterprise adoption in healthcare and fitness centers, with over 45% of wellness cafes offering organic green tea as a primary beverage option.

Europe held around 22% of the organic green tea market in 2024, with Germany, the UK, and France as the top-consuming countries. Regulatory pressure from the European Commission and sustainability initiatives has increased demand for traceable and certified organic products. Emerging technologies, including blockchain for supply chain transparency and AI-driven quality testing, are being implemented to meet regulatory requirements. Local players like Clipper Teas have launched new organic product lines with biodegradable packaging, catering to environmentally conscious consumers. European consumer behavior is influenced by strong regulatory expectations, with over 55% of households preferring certified organic beverages and functional green tea options.

Asia-Pacific dominates the market with 42% share in 2024. Leading consuming countries include Japan, China, and India. Infrastructure investments in modern processing facilities and tea plantations support high-volume production. Regional tech trends include AI-driven pest management and digital monitoring of plantations for quality assurance. Companies like Ito En in Japan have enhanced matcha production with automated leaf sorting and AI-based quality assessments. Consumer behavior in this region is increasingly influenced by e-commerce platforms and mobile applications, with over 60% of younger consumers purchasing organic green tea online and seeking functional or specialty blends.

South America accounted for approximately 8% of the market in 2024, with Brazil and Argentina as key contributors. Investments in energy-efficient processing and cold-chain logistics are supporting growth. Government incentives and trade policies, including tax benefits for organic farming and export facilitation, encourage local production. Players like Terra Verde have introduced certified organic tea lines to meet urban health-conscious consumer demand. Consumer behavior is influenced by media campaigns and regional language localization, with over 50% of urban populations seeking certified organic and functional beverages as part of lifestyle choices.

Middle East & Africa held around 5% of the market in 2024, with the UAE and South Africa as major contributors. Demand is increasing in sectors such as hospitality, luxury wellness, and corporate catering. Technological modernization trends include automated packing lines and digital quality control systems. Regulatory measures and international trade partnerships facilitate organic product imports and compliance. Local players like Alwazah Tea in the UAE have expanded retail and hotel distribution networks for organic green tea. Regional consumer behavior is characterized by a preference for premium and imported teas, with over 40% of luxury hotels offering certified organic green tea to guests.

Japan - 25% Market Share: Dominance driven by high production capacity and established export networks for premium matcha and green tea products.

China - 18% Market Share: Dominance due to strong end-user demand, large-scale plantations, and government support for organic tea cultivation.

The Organic Green Tea Market is characterized by a highly fragmented competitive landscape, with over 200 active global players ranging from large multinational corporations to niche artisanal producers. Collectively, the top five companies—Tata Consumer Products, Unilever, Associated British Foods, The Coca-Cola Company, and PepsiCo—command approximately 35% of the market share. These industry leaders are actively pursuing strategic initiatives such as mergers and acquisitions, partnerships, and product diversification to strengthen their market positions.

Innovation is a key driver of competition, with companies focusing on developing unique blends, functional beverages, and sustainable packaging solutions to meet evolving consumer preferences. For instance, the introduction of organic lemon ginger tea blends and the adoption of biodegradable packaging materials are gaining traction among health-conscious consumers. Additionally, advancements in digital transformation, including the implementation of AI-driven quality control systems and blockchain technology for supply chain transparency, are reshaping operational efficiencies and consumer trust.

The market's fragmented nature presents opportunities for both established and emerging players to capitalize on niche segments, such as premium organic blends and eco-friendly products. As consumer demand for clean-label and sustainably sourced products continues to rise, companies are increasingly aligning their strategies to emphasize authenticity, traceability, and environmental responsibility.

Associated British Foods Plc.

PepsiCo, Inc.

The Stash Tea Company

Harney & Sons Fine Teas

Halssen & Lyon GmbH

Ambassador Organics

Celestial Seasonings Inc.

Equal Exchange Co-op

Newman's Own Inc.

Numi Organic Tea

Arbor Teas

Art of Tea

Choice Organic Teas

Five Mountains

The Organic Green Tea Market is undergoing significant technological transformation to enhance product quality, operational efficiency, and consumer engagement. Artificial intelligence (AI) is being integrated into quality control processes, enabling real-time monitoring of tea leaves, detecting defects, and ensuring consistent product standards. Blockchain technology is increasingly utilized to trace the journey of tea leaves from farm to cup, providing consumers with verifiable information about product origins and authenticity. Internet of Things (IoT) sensors are being deployed in tea plantations to monitor environmental conditions, soil health, and crop growth, supporting data-driven and precision agricultural practices. Additionally, companies are investing in sustainable packaging innovations, adopting biodegradable and recyclable materials to meet growing consumer demand for eco-friendly products. The rise of e-commerce platforms and digital marketing strategies has further expanded the reach of organic green tea brands, facilitating direct-to-consumer sales and enhancing brand visibility. Collectively, these technological advancements are improving operational efficiency, fostering consumer trust, and driving innovation across the organic green tea industry.

In June 2024, Tata Consumer Products launched a new line of organic green tea blends infused with functional herbs, catering to the growing demand for health-oriented beverages. Source: www.tataconsumer.com

In August 2024, Unilever introduced biodegradable tea bag packaging across its organic green tea range, aligning with sustainability initiatives and consumer expectations for eco-friendly products. Source: www.unilever.com

In November 2024, Associated British Foods expanded its organic green tea offerings in European markets, leveraging its established distribution networks to reach a wider consumer base. Source: www.abf.co.uk

In January 2025, The Coca-Cola Company acquired a regional organic green tea brand to diversify its product portfolio and tap into the health-conscious beverage segment. Source: www.coca-colacompany.com

The Organic Green Tea Market Report provides a comprehensive analysis of the industry, encompassing various segments such as product types, applications, end-users, and regional markets. It offers insights into emerging trends, technological advancements, and consumer behaviors influencing market dynamics. The report also examines the competitive landscape, highlighting key players, strategic initiatives, and market share distributions.

Additionally, it explores regulatory frameworks, sustainability practices, and innovations shaping the future of the organic green tea industry. This detailed overview serves as a valuable resource for stakeholders seeking to understand market opportunities, challenges, and growth prospects within the organic green tea sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,619.6 Million |

| Market Revenue (2032) | USD 16,784.5 Million |

| CAGR (2025–2032) | 17.50% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Tata Consumer Products Limited, Unilever Group, The Coca-Cola Company, Associated British Foods Plc., PepsiCo, Inc., The Stash Tea Company, Harney & Sons Fine Teas, Halssen & Lyon GmbH, Ambassador Organics, Celestial Seasonings Inc., Equal Exchange Co-op, Newman's Own Inc., Numi Organic Tea, Arbor Teas, Art of Tea, Choice Organic Teas, Five Mountains |

| Customization & Pricing | Available on Request (10% Customization is Free) |