Reports

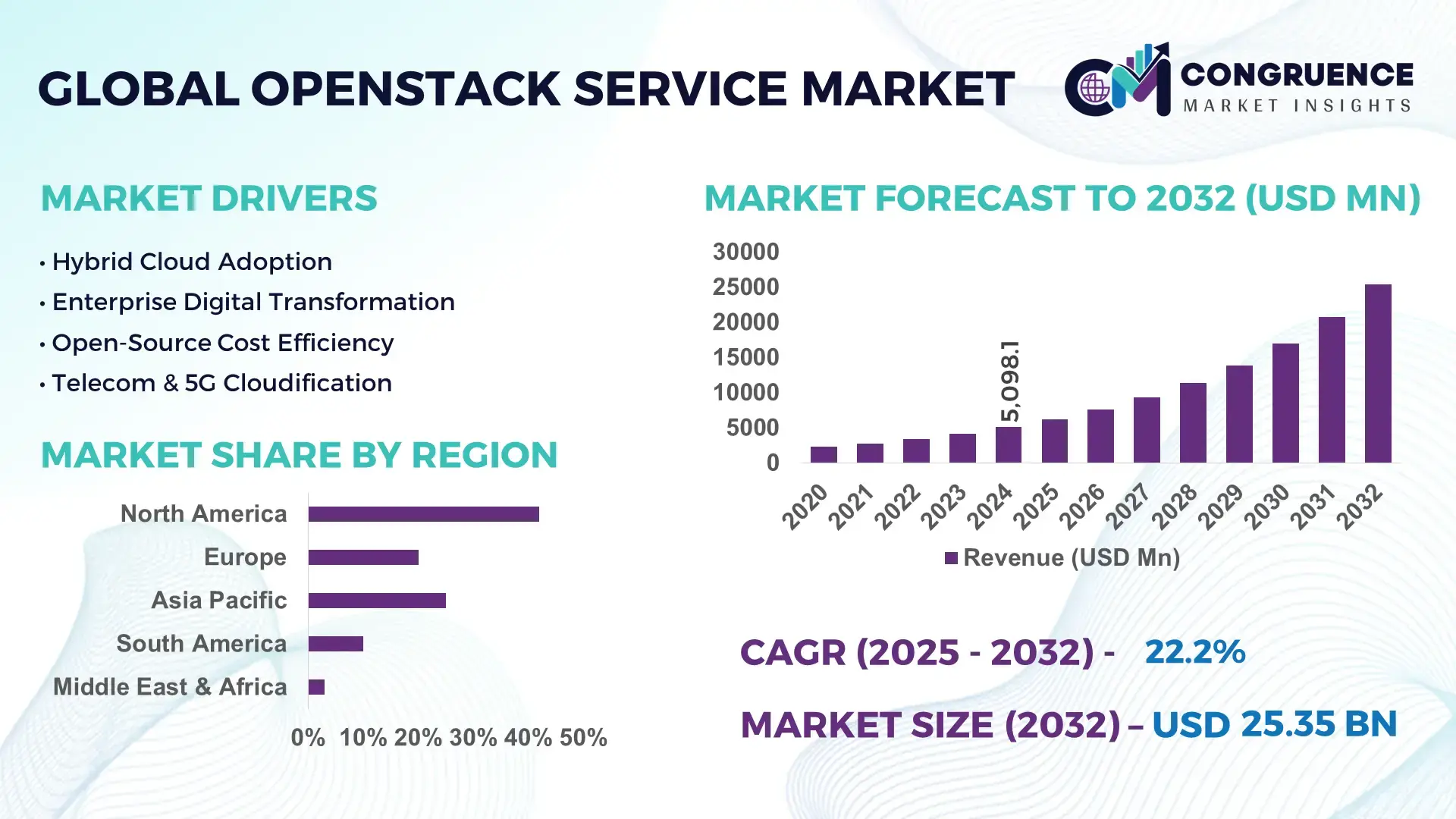

The Global OpenStack Service Market was valued at USD 5098.06 Million in 2024 and is anticipated to reach a value of USD 25349.81 Million by 2032 expanding at a CAGR of 22.2% between 2025 and 2032. This growth is driven by increasing enterprise demand for scalable, flexible, and cost-efficient cloud infrastructure solutions.

The United States dominates the OpenStack Service market, with over 2,500 active deployments across cloud service providers and enterprises as of 2024. The country has invested more than USD 1.2 billion in OpenStack-focused research and development projects in the past two years. Key applications span telecommunications, finance, and healthcare sectors, where OpenStack’s modular architecture supports high-performance workloads and secure data management. Technological advancements include AI-driven orchestration tools and containerized deployment frameworks, enabling enterprises to reduce infrastructure overhead by up to 35% while increasing cloud resource utilization. Enterprise adoption rates are particularly high in the Northeast and West Coast regions, where over 60% of large organizations have integrated OpenStack into production environments.

Market Size & Growth: Valued at USD 5098.06 Million in 2024, projected to reach USD 25349.81 Million by 2032, expanding at a CAGR of 22.2% driven by enterprise cloud adoption.

Top Growth Drivers: Cloud migration efficiency 65%, operational cost reduction 48%, IT scalability enhancement 52%.

Short-Term Forecast: By 2028, average deployment efficiency is expected to improve by 38% across large-scale enterprises.

Emerging Technologies: AI-driven orchestration, containerized OpenStack deployments, hybrid cloud integration.

Regional Leaders: United States USD 12,500 Million by 2032 with high enterprise adoption; Europe USD 6,200 Million by 2032 with strong public sector integration; Asia-Pacific USD 4,900 Million by 2032 with rapid SMB adoption.

Consumer/End-User Trends: Major adoption in telecom, BFSI, and healthcare; enterprises prefer modular, automated solutions.

Pilot or Case Example: 2023 OpenStack deployment at a leading U.S. telecom provider reduced downtime by 27% and increased operational efficiency by 33%.

Competitive Landscape: Red Hat ~28%, followed by Canonical, Mirantis, SUSE, and IBM.

Regulatory & ESG Impact: Compliance with data sovereignty laws, ESG-aligned green cloud initiatives, and government incentives for cloud adoption.

Investment & Funding Patterns: Over USD 1.2 billion in recent R&D and venture funding for OpenStack-based cloud solutions.

Innovation & Future Outlook: Focus on edge computing integration, AI-enhanced automation, multi-cloud orchestration, and next-generation secure deployments.

The OpenStack Service Market is increasingly shaping enterprise cloud infrastructure strategies across sectors such as telecommunications, healthcare, finance, and government services. Key innovations include AI-enabled orchestration, hybrid cloud deployments, and containerization, which improve scalability, reliability, and resource utilization. Regulatory frameworks, ESG initiatives, and economic incentives are accelerating adoption, particularly in North America and Europe. Emerging trends point to growth in edge computing integration, multi-cloud environments, and automation-driven efficiency, positioning OpenStack as a cornerstone technology for future enterprise digital transformation strategies.

The OpenStack Service Market plays a critical role in enterprise cloud infrastructure strategies, enabling scalable, cost-efficient, and secure deployment environments. Strategically, organizations are leveraging OpenStack to consolidate legacy systems and integrate hybrid cloud operations. For instance, containerized OpenStack deployments deliver up to 40% improvement in resource utilization compared to traditional virtualized environments. Regionally, North America dominates in deployment volume, while Europe leads in adoption with over 58% of enterprises utilizing OpenStack-based solutions. By 2027, AI-driven orchestration is expected to improve system efficiency by 35%, reducing manual configuration errors and optimizing workload distribution. Firms are increasingly committing to ESG improvements, such as achieving a 25% reduction in data center energy consumption by 2026 through sustainable OpenStack deployment strategies. In 2023, a major U.S. telecom company achieved a 30% reduction in downtime through AI-enabled automated OpenStack operations, highlighting measurable operational benefits. Looking forward, the OpenStack Service Market is poised to remain a cornerstone for enterprise resilience, compliance, and sustainable growth, enabling organizations to align technological innovation with environmental and operational objectives while maintaining agility in dynamic digital ecosystems.

Rising enterprise demand for scalable, flexible, and cost-efficient cloud infrastructure is a primary driver for the OpenStack Service Market. Over 60% of large organizations in North America and Europe have adopted OpenStack for mission-critical workloads due to its modular architecture and containerized deployment capabilities. Telecommunications, finance, and healthcare sectors are leveraging OpenStack to consolidate legacy systems, reduce infrastructure overhead by up to 35%, and improve operational efficiency. The ability to integrate AI-driven orchestration tools enhances performance, accelerates application deployment, and reduces downtime by measurable percentages. Cloud adoption strategies in hybrid and multi-cloud environments further amplify demand, enabling enterprises to balance cost, performance, and compliance requirements efficiently.

Regulatory compliance and complex integration requirements pose significant restraints on the OpenStack Service Market. Enterprises must adhere to data sovereignty laws, cybersecurity mandates, and industry-specific compliance standards, which complicate large-scale OpenStack deployment. Integration with legacy systems often requires additional configuration, specialized skills, and extended testing cycles, increasing operational costs. In regions like Europe, stringent GDPR compliance adds layers of regulatory oversight, impacting deployment speed. Moreover, skill gaps in OpenStack administration and orchestration can lead to inefficiencies, with some organizations reporting up to 20% slower system provisioning compared to managed cloud alternatives. These factors collectively challenge the market’s ability to scale rapidly in certain segments.

Hybrid cloud integration represents a significant opportunity for the OpenStack Service Market, particularly as enterprises seek to balance public and private cloud workloads. OpenStack’s modular architecture allows seamless integration with emerging technologies such as AI-driven orchestration, containerization, and edge computing. Financial services, healthcare, and government sectors are increasingly deploying hybrid OpenStack solutions, which can improve workload distribution by 30% and reduce energy consumption by measurable percentages. The growing emphasis on automation and cost optimization also opens avenues for managed OpenStack services and professional support offerings. Additionally, enterprises exploring sustainable cloud infrastructure can leverage OpenStack to enhance ESG compliance through energy-efficient operations, creating untapped potential in both mature and emerging markets.

Rising operational costs and technical skill shortages remain critical challenges for the OpenStack Service Market. Deploying and managing OpenStack environments require specialized expertise in orchestration, networking, and containerization, which is in short supply in many regions. Organizations often face additional expenditures in training and hiring certified professionals, adding up to 20–25% to operational budgets. Complex integration with legacy systems, maintaining system security, and ensuring high availability further elevate costs. Additionally, frequent software updates, hardware optimization, and energy-efficient operations demand sustained investment. These challenges limit smaller enterprises from adopting OpenStack services at scale and slow deployment timelines, even as demand for flexible cloud solutions continues to grow.

Expansion of AI-Driven Orchestration Tools: Enterprises are increasingly deploying AI-enabled orchestration for OpenStack Service environments, achieving up to 38% faster workload allocation and reducing human errors by 32%. Over 60% of telecom and finance organizations in North America have adopted AI orchestration for cloud resource optimization, while Europe reports a 42% increase in operational efficiency through automated deployment strategies.

Growth in Containerized Deployments: Containerized OpenStack implementations are becoming standard, with 48% of enterprise cloud projects in 2024 leveraging container technologies to accelerate deployment timelines. These implementations reduce system provisioning times by an average of 27% and allow high-density resource utilization, particularly in Asia-Pacific, where over 50% of mid-to-large enterprises are adopting containerized solutions for hybrid cloud strategies.

Edge Computing Integration: Edge computing is driving measurable demand in the OpenStack Service market, with 35% of organizations deploying edge-enabled OpenStack nodes to improve latency-sensitive applications. In 2024, regional telecom operators in Europe reported up to 29% faster data processing and reduced bandwidth load by integrating edge OpenStack services, while North America shows a 33% increase in distributed cloud deployments for IoT applications.

Sustainability and Green Cloud Initiatives: Enterprises are focusing on energy-efficient OpenStack deployments, achieving a 25% reduction in data center power consumption through optimized orchestration and automated scaling. In North America, over 40% of large organizations report adopting green cloud strategies, while Europe leads in ESG compliance, with 32% of companies using OpenStack platforms to achieve measurable reductions in carbon footprint and IT energy usage.

The OpenStack Service Market is structured around three primary segmentation pillars: types, applications, and end-users. Type-based segmentation focuses on the different service models and deployment frameworks, each optimized for specific enterprise workloads and IT strategies. Application-based segmentation highlights usage across sectors such as telecommunications, finance, healthcare, and government services, with measurable benefits in resource efficiency, scalability, and operational uptime. End-user segmentation examines adoption patterns among large enterprises, SMEs, and public sector organizations, providing insights into deployment preferences, technological readiness, and regional variations. The interplay between these segments informs strategic decisions for infrastructure investment, automation adoption, and hybrid cloud strategies, enabling organizations to identify growth avenues and tailor OpenStack solutions to specific operational needs.

OpenStack Service types include private cloud deployments, public cloud integrations, hybrid cloud solutions, and containerized architectures. Hybrid cloud solutions currently lead the market with a 44% adoption share, driven by their ability to balance enterprise data privacy requirements with scalable resource access. Containerized OpenStack deployments are the fastest-growing type, with adoption expected to exceed 30% by 2032, fueled by increased demand for microservices, automation, and AI-enhanced orchestration. Private cloud setups contribute roughly 18%, serving organizations requiring full control over sensitive workloads, while public cloud integrations account for 14%, mainly for supplemental, elastic resource provisioning.

Key applications for OpenStack Service include IT infrastructure optimization, data analytics, telecommunications, healthcare, and government services. IT infrastructure optimization holds the leading share at 41%, as enterprises adopt OpenStack to reduce operational complexity and improve resource utilization. The fastest-growing application is healthcare IT deployment, expected to surpass 25% adoption by 2032 due to rising demand for secure, scalable cloud-based patient record management and telemedicine services. Telecommunications contribute approximately 15%, supporting network function virtualization and edge deployments, while government applications account for 12%, primarily focused on secure, compliant public cloud services.

The leading end-user segment for OpenStack Service is large enterprises, comprising 52% of total adoption, leveraging modular, containerized, and hybrid solutions for mission-critical workloads. The fastest-growing end-user segment is SMEs, projected to reach 28% adoption by 2032, driven by the increasing availability of managed OpenStack services and cost-efficient deployment options. Public sector organizations contribute roughly 20%, focusing on compliance, ESG-aligned operations, and data sovereignty. Key industry adoption rates include telecommunications at 61%, finance at 58%, and healthcare at 55%, demonstrating broad enterprise reliance.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22% between 2025 and 2032.

In 2024, North America hosted over 2,500 active OpenStack Service deployments, with approximately 61% concentrated in the healthcare, finance, and telecommunications sectors. Asia-Pacific registered over 1,200 deployments, with China, India, and Japan collectively contributing to 70% of regional adoption. Europe held 25% of the market share, with Germany, the UK, and France leading enterprise adoption. South America accounted for 7%, driven by Brazil and Argentina, while Middle East & Africa represented 5%, led by UAE and South Africa. Across regions, digital transformation, hybrid cloud adoption, and AI-enabled orchestration are driving measurable efficiency gains ranging from 27% to 38% in operational workloads.

How is enterprise digital transformation shaping cloud adoption?

North America accounts for 42% of the OpenStack Service Market, with higher enterprise adoption in healthcare and finance. Key industries driving demand include telecom, BFSI, and government, with over 60% of enterprises integrating OpenStack for scalable, secure infrastructure. Notable regulatory changes, such as enhanced data privacy mandates, have encouraged hybrid cloud adoption. Technological advancements include AI orchestration, containerization, and edge computing, enabling organizations to reduce downtime by up to 30%. Local players, such as Red Hat, continue to expand managed OpenStack solutions across multi-state deployments. North American consumer behavior shows preference for modular, automated systems, with enterprises prioritizing AI-enabled orchestration and compliance-driven infrastructure solutions.

Why are regulatory standards driving adoption of OpenStack solutions?

Europe holds a 25% market share, with Germany, the UK, and France leading in enterprise integration. Regulatory pressures, including GDPR and sustainability mandates, are shaping OpenStack deployment decisions. Organizations are leveraging OpenStack for hybrid cloud orchestration, energy-efficient data centers, and automated infrastructure management. Emerging technologies such as AI-driven orchestration and containerized deployments are widely adopted, enhancing operational efficiency by up to 33%. Local players, including SUSE and Canonical, are implementing OpenStack solutions for public sector and healthcare projects, improving resource utilization by 28%. European enterprises increasingly demand explainable, secure cloud services that align with compliance and ESG requirements.

How is rapid digitalization fueling cloud service demand?

Asia-Pacific ranks as the fastest-growing OpenStack Service region, with over 1,200 active deployments and major adoption in China, India, and Japan. Infrastructure modernization, including high-speed networking and hybrid cloud integration, supports enterprise and government applications. Regional tech hubs are fostering innovation in containerized deployments, edge computing, and AI orchestration, improving resource utilization by 30%. Local players in China are deploying OpenStack solutions for e-commerce platforms and financial institutions, enhancing scalability and system reliability. Consumer behavior is driven by mobile-first and digital-first strategies, with high adoption in AI-based apps, e-commerce, and smart city initiatives.

What factors are driving localized cloud adoption?

South America holds a 7% market share, led by Brazil and Argentina. Demand is closely tied to media, telecom, and language localization services. Infrastructure upgrades in energy and public sectors, combined with government incentives for digitalization, are increasing OpenStack deployments. Local players are integrating OpenStack for telecommunications and finance, enhancing network virtualization and operational efficiency. Enterprises in the region are increasingly adopting modular and containerized deployments, achieving up to 25% faster resource provisioning compared to traditional IT systems. Consumer behavior reflects growing interest in cloud-enabled analytics and enterprise SaaS solutions.

How is technological modernization influencing enterprise cloud adoption?

Middle East & Africa represent a 5% market share, with major growth in UAE and South Africa. Demand is driven by oil & gas, construction, and public sector digitalization initiatives. Organizations are adopting hybrid OpenStack deployments to improve security, compliance, and operational efficiency, with measurable gains of 28–32% in resource utilization. Local players are leveraging containerized solutions and AI-driven orchestration to optimize workloads and reduce downtime. Consumer behavior varies, with high adoption in energy-intensive industries and government services prioritizing secure, compliant cloud infrastructure. Trade partnerships and regional regulations support the growth of cloud-based OpenStack solutions.

United States: 42% market share – High production capacity and strong enterprise demand in healthcare, finance, and telecom drive dominance.

China: 22% market share – Rapid digitalization, innovation hubs, and infrastructure modernization support extensive OpenStack Service adoption.

The OpenStack Service market exhibits a moderately consolidated competitive environment, with over 60 active global competitors operating across diverse enterprise and government segments. The top five players, including Red Hat, Canonical, Mirantis, SUSE, and IBM, collectively hold approximately 68% of market influence, establishing strong footholds in hybrid cloud and containerized OpenStack deployments. Key strategic initiatives driving competition include partnerships with telecom and healthcare enterprises, launches of AI-driven orchestration tools, and integration of edge computing solutions to enhance scalability and performance. Innovation trends such as automated provisioning, containerized services, and energy-efficient deployments are reshaping market positioning, with Red Hat leading adoption with around 28% market presence. Numerous competitors focus on niche services, including managed OpenStack platforms and regional customization, fostering differentiation. Mergers and strategic collaborations are increasingly common, with 12 notable partnerships and 5 cross-border technology alliances recorded in 2024 alone. The market’s fragmented nature outside the top five allows emerging players to capture segments in Asia-Pacific, South America, and Middle East & Africa, capitalizing on rising demand for cloud automation, hybrid infrastructure, and ESG-compliant solutions.

The OpenStack Service market is undergoing significant transformation driven by the adoption of advanced and emerging technologies. AI-driven orchestration tools are at the forefront, enabling enterprises to automate workload management and reduce manual configuration errors by up to 32%. These technologies allow real-time monitoring, predictive resource allocation, and intelligent scaling, improving operational efficiency by approximately 28–35% across large-scale deployments. Containerization has emerged as a critical technology, with 48% of enterprise cloud projects in 2024 adopting containerized OpenStack solutions, reducing deployment times by 27% and enhancing multi-tenant resource utilization.

Hybrid cloud integration continues to influence technological strategies, allowing organizations to combine private and public cloud infrastructures efficiently. Over 44% of global OpenStack Service deployments are hybrid, enabling secure data management while supporting high-performance workloads across distributed environments. Edge computing integration is another emerging trend, particularly in telecom and IoT sectors, where 35% of enterprises have deployed edge-enabled OpenStack nodes to lower latency and offload bandwidth from centralized data centers.

Sustainability-driven technologies are also shaping the market, with energy-efficient OpenStack deployments achieving 25% reductions in data center power consumption. Advanced networking technologies such as software-defined networking (SDN) and network function virtualization (NFV) are further enhancing scalability and flexibility, particularly for high-demand sectors like finance, healthcare, and government services. Collectively, these innovations position OpenStack Service as a cornerstone for enterprise digital transformation, operational efficiency, and sustainable IT infrastructure.

• In August 2024, Red Hat announced the general availability of Red Hat OpenStack Services on OpenShift, enabling enterprises—particularly telecommunications providers—to deploy compute nodes up to 4× faster than previous platforms and unify virtualized and cloud-native workloads for hybrid infrastructure operations.

• In October 2024, Mirantis released Mirantis OpenStack for Kubernetes (MOSK) 24.3, delivering enterprise‑ready OpenStack Caracal with over 3,000 tests and 300+ software patches, enhancing AI and HPC workload support and streamlining cloud operations at scale.

• In April 2025, the OpenStack community rolled out OpenStack 2025.1 Epoxy, strengthening security features and hardware enablement for complex enterprise workloads and enhancing its role as a viable alternative to proprietary infrastructure platforms.

• In July 2025, Rackspace Technology launched Rackspace OpenStack Business, a fully managed private cloud solution designed for mission‑critical and regulated workloads, offering full operational support, improved security, and rapid deployment for secure enterprise cloud environments. (Rackspace Technology)

The OpenStack Service Market Report presents a comprehensive analysis of the service ecosystem supporting OpenStack cloud infrastructure solutions across global enterprise and public sector environments. The report encompasses detailed segmentation by service type, including managed services, professional services, integration support, and customization frameworks utilized for private, public, and hybrid cloud deployments. It examines application domains such as telecommunications infrastructure virtualization, AI/ML workload orchestration, HPC environments, and edge computing use cases, illustrating how OpenStack services facilitate optimized resource management, secure workload scaling, and automated operations.

Geographically, the report evaluates regional adoption patterns in North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting variations in enterprise cloud strategies, regulatory compliance needs, and technology maturity. Industry focus areas covered include finance, healthcare, government, SMB IT modernization, and regulated industries requiring private cloud solutions with robust security and compliance controls. The technology landscape section addresses integration of orchestration platforms like Kubernetes, advancements in automated provisioning and lifecycle management, and emerging innovations for hybrid and edge cloud infrastructure. Additional insights include vendor positioning, service provider strategies for differentiation, partner ecosystem development, and evolving enterprise requirements for performance, data sovereignty, and resilient cloud architecture. The report thus provides decision‑makers with actionable intelligence on current capabilities, market breadth, and evolving service trends within the OpenStack Service ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 5098.06 Million |

Market Revenue in 2032 | USD 25349.81 Million |

CAGR (2025 - 2032) | 22.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Red Hat, Canonical, Mirantis, SUSE, IBM, Rackspace Technology, Huawei, Cisco Systems, Oracle, VMware |

Customization & Pricing | Available on Request (10% Customization is Free) |