Reports

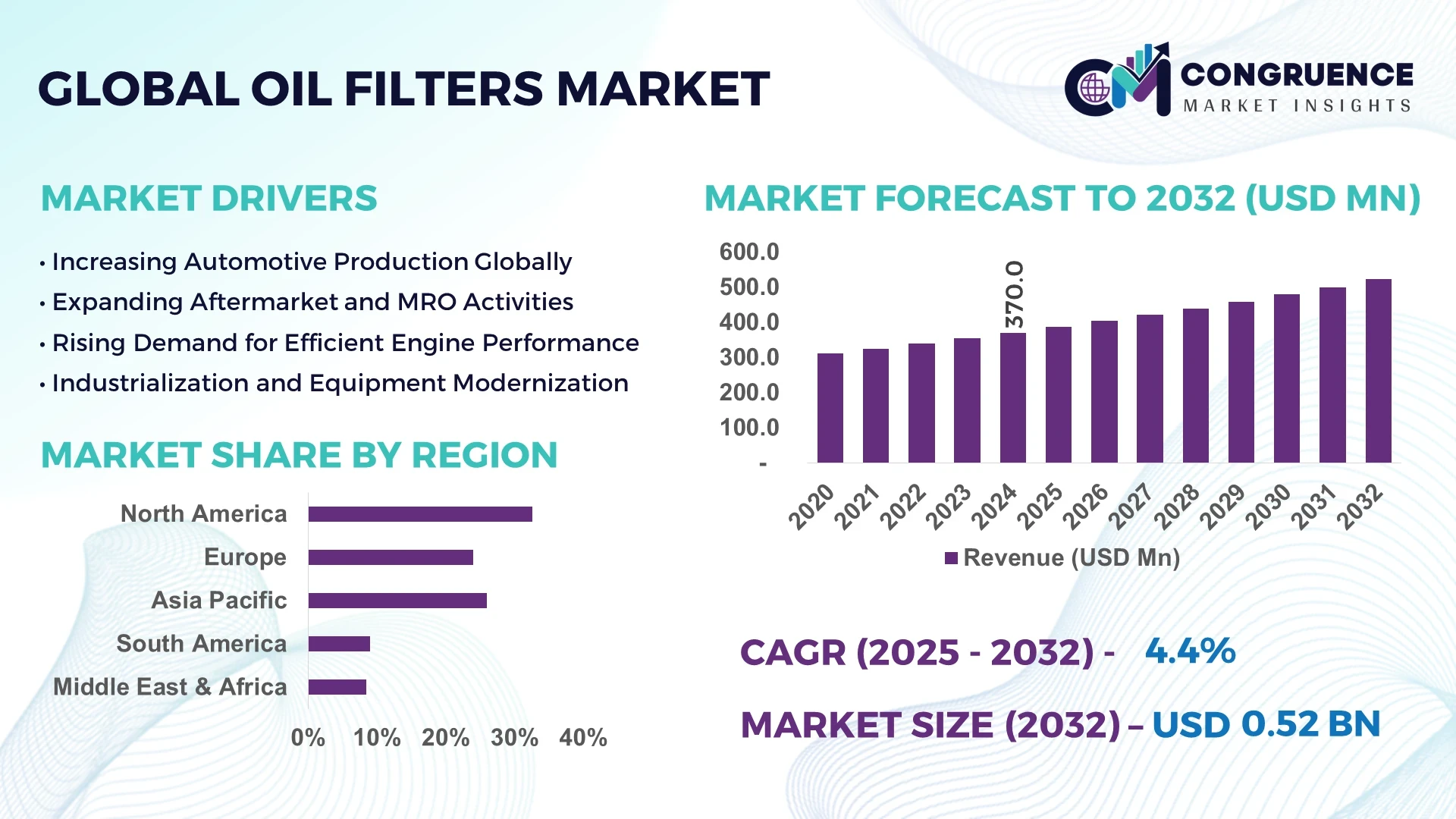

The Global Oil Filters Market was valued at USD 370 Million in 2024 and is anticipated to reach a value of USD 522.2 Million by 2032 expanding at a CAGR of 4.4% between 2025 and 2032.

The United States leads the global Oil Filters Market due to its robust production infrastructure, with over 200 million units produced annually. The country has seen significant investment in automotive and industrial filtration technologies, particularly in synthetic media filters and multi-layer filtration systems. It also boasts advanced R&D capabilities and integration of automation technologies within manufacturing facilities, enhancing filter efficiency and durability for diverse applications in automotive, aerospace, and heavy machinery sectors.

The Oil Filters Market is integral to several high-performance sectors including automotive, aerospace, marine, and industrial machinery, with the automotive segment accounting for a major portion of global demand. Recent innovations include synthetic and cellulose-blend media filters, self-cleaning systems, and smart filters embedded with sensors for real-time monitoring of oil quality and filter condition. Regulatory measures such as Euro 6 and Tier 4 engine emission standards have pushed OEMs to adopt more efficient filtration solutions. Environmentally, there is rising pressure to extend service intervals and reduce oil waste, which is influencing demand for long-life and eco-friendly filters. Regionally, Asia-Pacific is witnessing heightened consumption driven by vehicle ownership growth, while North America and Europe remain key hubs of technological advancement. Looking ahead, integration with predictive maintenance systems, especially in fleet management and industrial machinery, will shape future growth.

Artificial Intelligence (AI) is significantly transforming the Oil Filters Market by introducing intelligent automation, enhancing design precision, and optimizing lifecycle management. AI-powered systems now streamline the design and simulation of filtration components, reducing prototyping costs and improving efficiency. Manufacturers are deploying AI algorithms to predict filter performance under various conditions, enabling data-driven improvements in both structure and material composition. In industrial settings, AI-enabled condition monitoring systems are revolutionizing maintenance cycles by detecting contaminants and pressure drops in real-time, thereby extending filter life and reducing downtime.

In the automotive industry, AI-based predictive maintenance tools are helping fleet operators and OEMs anticipate oil filter degradation and schedule timely replacements. This minimizes operational disruptions and extends engine performance. Machine learning models trained on historical data also support the creation of adaptive filters suited to engine type, oil viscosity, and load cycles. In production, AI-driven visual inspection systems enhance quality control, detecting micro-defects invisible to the human eye. These advancements not only improve efficiency but also reduce material waste and ensure regulatory compliance in safety-critical applications such as aerospace and heavy-duty engines.

“In 2025, a leading automotive parts manufacturer introduced an AI-integrated oil filtration system that uses real-time data from onboard sensors to dynamically adjust flow rates, resulting in a 21% increase in filtration efficiency and reducing unscheduled maintenance by 17% in logistics fleets.”

The Oil Filters Market is undergoing dynamic transformation influenced by innovation, environmental pressures, and shifting consumption trends. Technological advancements in filtration media, especially the use of nanofiber and synthetic blends, are significantly improving filter efficiency and longevity. Additionally, the integration of digital solutions and smart sensors for real-time filter condition monitoring is shaping market expectations. Industrial expansion, especially in transportation, energy, and construction sectors, continues to fuel demand, while tightening global emission standards are prompting the adoption of higher-grade filtration systems. Regional dynamics also play a role, with Asia-Pacific driving volume growth and North America and Europe steering innovation.

Increasing vehicle production globally, especially in emerging markets, is boosting the need for oil filters that can withstand extended operating cycles. With industrial automation expanding, the use of hydraulic systems and heavy-duty equipment that require regular oil filtration is also on the rise. For instance, in 2024 alone, global passenger vehicle output increased by over 5 million units, directly increasing OEM demand for advanced engine oil filters. Additionally, industries now rely on automated equipment where oil filtration is critical for maintaining system integrity and minimizing machine downtime, further stimulating filter demand across industrial applications.

Disposal of used oil filters remains a significant challenge in the Oil Filters Market. Filters often contain residual oil and non-biodegradable components, making them subject to stringent environmental regulations. Countries in Europe and North America have enacted laws that require special treatment or recycling of used filters, increasing operational burdens for manufacturers and service providers. Moreover, managing hazardous waste compliance increases the cost structure of disposal logistics. Inadequate recycling infrastructure in some regions further compounds the issue, limiting scalability and slowing market penetration in otherwise high-potential zones.

The rising trend of smart filtration technologies presents a notable opportunity for market players. Filters embedded with IoT sensors can monitor pressure differentials, detect contamination levels, and communicate data to centralized systems. This is especially useful in fleet management and industrial machinery, enabling predictive maintenance and reducing downtime. For instance, the adoption of connected filtration units in industrial engines is expected to rise significantly, with early adopters reporting operational efficiency gains of up to 18%. This shift aligns with broader digitalization efforts across sectors and creates scope for recurring service models through aftermarket sales.

Advanced oil filters, particularly those incorporating multi-layer media or smart sensors, require precise manufacturing conditions and specialized raw materials. These components often carry higher production costs, limiting adoption in cost-sensitive markets. Furthermore, sourcing high-performance materials like nanofibers or synthetic blends is subject to supply volatility. Small-scale manufacturers face additional hurdles in scaling production due to capital-intensive machinery and quality assurance standards. As global competition intensifies, maintaining profitability while adhering to performance and regulatory standards becomes increasingly difficult, posing a considerable challenge to newer entrants and low-margin players.

Expansion of Electric and Hybrid Vehicle Applications: Although EVs require fewer oil-based components, hybrid vehicles still use internal combustion engines, necessitating advanced filtration systems. Manufacturers are developing compact, high-efficiency filters tailored for hybrid powertrains, including integrated thermal and pressure management systems. In 2024, over 1.3 million hybrid vehicles equipped with specialized oil filters were sold across Asia-Pacific, highlighting this evolving niche.

Surge in Demand for Long-Life and Eco-Friendly Filters: Environmental concerns are accelerating the development of long-life oil filters using sustainable materials. Filters that can last up to 25,000 miles are being adopted in commercial fleets to minimize oil change frequency and reduce waste. Additionally, bio-based polymers are being used in housings and components, promoting recyclability and reducing landfill pressure.

Increasing Use of Synthetic Media Filters in Heavy-Duty Machinery: Synthetic filter media, with its higher contaminant holding capacity and temperature resistance, is becoming a standard in sectors such as mining and construction. In North America, nearly 70% of new heavy-duty off-road machinery in 2024 featured synthetic oil filters, boosting operational uptime and reducing total cost of ownership.

Digital Supply Chain Integration and Customization: OEMs and distributors are increasingly utilizing AI-powered supply chain tools to forecast demand for oil filters based on regional vehicle population and seasonal maintenance cycles. These systems enable just-in-time inventory and facilitate custom filter configurations, improving service delivery and reducing warehouse overhead.

The Oil Filters Market is segmented comprehensively by type, application, and end-user verticals, each exhibiting distinct demand patterns and growth dynamics. Product differentiation is primarily based on the filtration media, structure, and operational capacity suited to specific engine types and environmental conditions. In terms of application, sectors such as automotive, industrial machinery, and power generation dominate due to their continuous operational requirements and maintenance standards. End-user segmentation reveals that OEMs, fleet operators, and maintenance service providers are pivotal to consumption trends. Technological upgrades, compliance mandates, and rising industrial automation are reshaping demand across all segments, with several niche categories showing accelerated growth due to evolving performance expectations and environmental regulations.

Full-flow oil filters currently lead the market due to their widespread adoption in passenger and commercial vehicles. These filters ensure uninterrupted oil supply and effectively remove larger contaminants, making them ideal for standard engine protection. Their ease of integration and compatibility with a wide range of engines have cemented their dominance across both OEM and aftermarket channels.

Meanwhile, bypass oil filters are emerging as the fastest-growing segment. Their ability to filter smaller particles and extend oil change intervals is increasingly valued in heavy-duty and high-load industrial engines. Fleet operators are particularly adopting bypass systems to enhance engine lifespan and reduce maintenance downtime. This is especially relevant in logistics and mining applications where equipment longevity is mission-critical.

Other types such as cartridge and spin-on filters hold important niche roles. Cartridge filters are gaining attention for their eco-friendly, non-metallic designs suitable for sustainable vehicle platforms. Spin-on filters remain popular due to their ease of replacement and cost-effectiveness, especially in the aftermarket servicing of older vehicles and light trucks.

Among all application areas, the automotive sector dominates the Oil Filters Market due to the sheer volume of vehicles on the road and the mandatory requirement for engine protection and emissions compliance. Internal combustion engine vehicles, both personal and commercial, account for a significant share of oil filter consumption globally.

The industrial machinery segment is witnessing the fastest growth, driven by increasing mechanization across construction, agriculture, and manufacturing sectors. With prolonged operating cycles and stringent reliability requirements, these machines rely heavily on high-performance oil filters. Investments in heavy-duty equipment and infrastructure projects across Asia-Pacific and Latin America are amplifying this demand.

Other applications such as power generation, marine engines, and aerospace systems also contribute notably. The power generation sector, particularly backup diesel generator units, relies on efficient oil filtration to ensure continuous operation and prevent mechanical failure. Marine and aerospace applications, though smaller in volume, demand high-specification filters that can withstand extreme conditions, making them premium niches in the overall market.

OEMs represent the largest end-user group in the Oil Filters Market, driven by high production volumes and tight integration of filtration systems into new vehicle platforms. Engine manufacturers prioritize compatibility and performance, often working with filter suppliers to co-develop systems that meet strict emissions and durability standards. OEM demand remains stable due to consistent vehicle production and regulatory compliance pressures.

Fleet operators and commercial vehicle service providers are currently the fastest-growing end-user group. Their shift toward predictive maintenance and cost optimization has accelerated the adoption of advanced and long-life filters. Large logistics companies, for example, are investing in premium oil filters to reduce vehicle downtime and extend maintenance intervals across geographically dispersed fleets.

Other significant end-users include maintenance, repair, and overhaul (MRO) companies and aftermarket retailers. These stakeholders serve a critical role in the replacement cycle, especially in aging vehicle populations and industrial setups. The aftermarket segment is also witnessing growing customization demands based on engine type, usage intensity, and environmental factors.

North America accounted for the largest market share at 32.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2025 and 2032.

The dominance of North America in the Oil Filters Market is driven by high automotive density, advanced filtration technologies, and stringent emission norms. However, rapid industrialization, rising vehicle production, and expanding infrastructure projects are accelerating demand in Asia-Pacific. Countries like China and India are heavily investing in automotive and heavy machinery sectors, boosting filter adoption. Moreover, favorable government initiatives to reduce vehicle emissions and the rise of smart filtration technologies are further intensifying growth across this region. Each region shows unique demand dynamics based on industrial maturity, regulatory frameworks, and technological penetration, shaping a complex but promising global landscape for oil filter manufacturers.

North America held approximately 32.6% of the global Oil Filters Market in 2024, with the U.S. and Canada being the primary contributors. The market is bolstered by strong demand from the automotive, aerospace, and heavy machinery sectors. Large-scale logistics operations and commercial fleets increasingly rely on premium oil filters for engine efficiency and longer service intervals. Notable regulatory standards such as the EPA’s vehicle emission policies continue to drive innovation in filtration systems. Additionally, digital transformation across manufacturing lines—especially the adoption of AI-driven quality control and predictive maintenance systems—is improving operational efficiencies. Government grants supporting clean technologies further enhance adoption of long-life and recyclable filter types across industries.

Europe captured around 27.4% of the global Oil Filters Market in 2024, led by industrialized nations such as Germany, France, and the United Kingdom. These countries emphasize sustainability and stringent emissions regulations set by bodies such as the European Environment Agency (EEA). The automotive sector—especially electric and hybrid manufacturing in Germany and the UK—continues to drive filter innovation. Lightweight, eco-friendly filters designed to meet Euro 6/7 standards are gaining traction. Simultaneously, increased investments in Industry 4.0 practices and AI-based diagnostics are reshaping OEM expectations. Environmental sustainability initiatives across the EU are also prompting shifts toward recyclable and biodegradable filter materials, aligning with broader circular economy goals.

Asia-Pacific ranks as the fastest-growing region in the Oil Filters Market and is projected to surpass 30% of total global volume by 2032. China, India, and Japan are the primary consumers, driven by expansive automotive production, rapid industrialization, and large-scale infrastructure development. China alone manufactures over 25 million vehicles annually, creating a sustained demand for OEM oil filtration systems. India is witnessing a rise in commercial vehicle sales and off-road machinery use, further intensifying aftermarket demand. Additionally, innovation hubs in South Korea and Japan are developing smart filter technologies and integrating sensor-based diagnostics into filtration systems. The region is also benefitting from government support for clean transportation and industrial modernization programs.

South America’s Oil Filters Market is largely concentrated in Brazil and Argentina, which together account for over 65% of regional demand. The regional market benefits from growing activity in logistics, construction, and mining sectors, all of which depend heavily on high-efficiency oil filtration systems. Brazil’s well-established automotive manufacturing base fuels consistent OEM demand, while Argentina is expanding its heavy machinery and agricultural equipment segments. Additionally, infrastructure development projects and transcontinental trade agreements are supporting market expansion. Governments are also incentivizing cleaner vehicle technologies, gradually encouraging the shift to advanced filtration systems. Though smaller in size, the region’s steady industrialization offers long-term growth potential.

The Middle East & Africa Oil Filters Market is witnessing steady growth, especially in countries like the UAE, Saudi Arabia, and South Africa. Regional demand is predominantly driven by oil & gas exploration, power generation, and heavy-duty construction. The UAE and Saudi Arabia are investing heavily in refining capacity and infrastructure projects that require sophisticated filtration systems. South Africa’s mining sector and industrial expansion further add to the demand. Governments in the GCC are encouraging adoption of eco-friendly technologies and machinery upgrades, while trade partnerships with Asian OEMs are improving access to next-gen filtration products. Digitization and automation trends are also starting to influence filtration maintenance and lifecycle management in this region.

United States – 25.2% Market Share

High production capacity, extensive automotive and heavy machinery usage, and strong integration of smart filter technologies.

China – 21.8% Market Share

Dominance in global vehicle manufacturing and rapid industrial expansion fueling high oil filter consumption across sectors.

The Oil Filters Market is characterized by a moderately fragmented competitive landscape, with over 40 active global and regional players competing across OEM and aftermarket segments. Competition is driven by factors such as filtration efficiency, lifecycle cost, eco-friendliness, and compatibility with modern engine technologies. Leading companies maintain a strong presence through diversified product portfolios and established distribution networks.

Strategic initiatives such as joint ventures with OEMs, global supply chain expansions, and product line enhancements are prominent among top competitors. In 2023 and 2024, several companies focused on upgrading their filter offerings with synthetic media, biodegradable materials, and smart diagnostic sensors. Mergers and acquisitions have also been used to access emerging markets and strengthen R&D capabilities.

Innovation remains a core differentiator, with players investing in AI-based monitoring systems and nanofiber materials to meet tightening emission standards and user demand for extended filter performance. The competition is especially intense in the aftermarket, where pricing, availability, and customization significantly impact brand preference. As environmental regulations tighten and vehicle platforms evolve, market players are under continuous pressure to innovate and optimize.

Mann+Hummel GmbH

Donaldson Company, Inc.

MAHLE GmbH

Parker Hannifin Corporation

Sogefi S.p.A.

Robert Bosch GmbH

Denso Corporation

Cummins Filtration

Hengst SE

FRAM Group Operations LLC

Technological advancement is a defining element in the current Oil Filters Market landscape. Manufacturers are integrating multi-layered synthetic media, nanofiber coatings, and microglass fiber composites to enhance filtration precision, durability, and flow consistency. These materials offer higher contaminant holding capacities and are especially valuable in heavy-duty and extended-drain interval applications.

Smart oil filters are gaining traction, with embedded sensors that monitor oil quality, temperature, pressure differential, and overall filter health in real-time. These intelligent filters communicate data to on-board diagnostics or cloud-based maintenance platforms, supporting predictive maintenance practices in both fleet and industrial settings.

Thermally adaptive filters have also emerged, capable of adjusting performance based on operating conditions. This is especially useful in hybrid and performance vehicles that experience varied load cycles. Eco-friendly advancements include biodegradable filter housings and reusable filter cores that help reduce landfill waste and align with sustainability goals.

Manufacturing processes are increasingly digitized, with AI-driven inspection systems ensuring high-quality output and reducing production errors. Customizable filter designs are being made possible through 3D prototyping and digital twins, enhancing the speed of innovation cycles. As electric and hybrid vehicles gain market share, new filtration demands—such as thermal oil cooling filters for battery systems—are also being explored.

• In February 2024, MAHLE launched a new series of smart oil filters with integrated pressure and temperature sensors for commercial vehicles, reducing maintenance costs and extending engine life by up to 18%.

• In November 2023, Mann+Hummel opened a new R&D facility in Shanghai focusing on advanced synthetic media development and next-gen filter designs tailored for Asian markets.

• In March 2024, Cummins Filtration introduced an eco-efficient spin-on oil filter line featuring 30% recycled components and a 20% longer service life, targeting commercial fleet operators.

• In May 2023, Donaldson Company unveiled an industrial oil filter with nanofiber media for power generation turbines, increasing particle retention efficiency by 25% compared to traditional glass fiber filters.

The Global Oil Filters Market Report provides a comprehensive analysis of the industry’s structure, segmentation, regional landscape, and technology trends. It covers detailed market segmentation by product type—including full-flow filters, bypass filters, cartridge filters, and spin-on filters—analyzing their adoption across diverse applications such as automotive engines, industrial machinery, marine systems, and power generation equipment.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering region-wise insights into demand drivers, innovation hubs, and regulatory environments. Each region’s market landscape is explored in terms of volume, demand dynamics, and industrial activities influencing oil filter consumption.

Key end-user sectors include OEMs, fleet operators, aftermarket distributors, and maintenance providers, each presenting unique demand patterns and challenges. The report also highlights technological transformations, such as the integration of AI in predictive diagnostics, sustainable filter materials, and advancements in synthetic filtration media.

The study pays particular attention to emerging and niche segments, including hybrid vehicle filters and smart filtration systems with IoT capabilities. This broad scope enables decision-makers to identify strategic opportunities, manage risks, and align business objectives with future trends shaping the Oil Filters Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 370.0 Million |

| Market Revenue (2032) | USD 522.2 Million |

| CAGR (2025–2032) | 4.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Mann+Hummel GmbH, Donaldson Company, Inc., MAHLE GmbH, Parker Hannifin Corporation, Sogefi S.p.A., Robert Bosch GmbH, Denso Corporation, Cummins Filtration, Hengst SE, FRAM Group Operations LLC |

| Customization & Pricing | Available on Request (10% Customization is Free) |