Reports

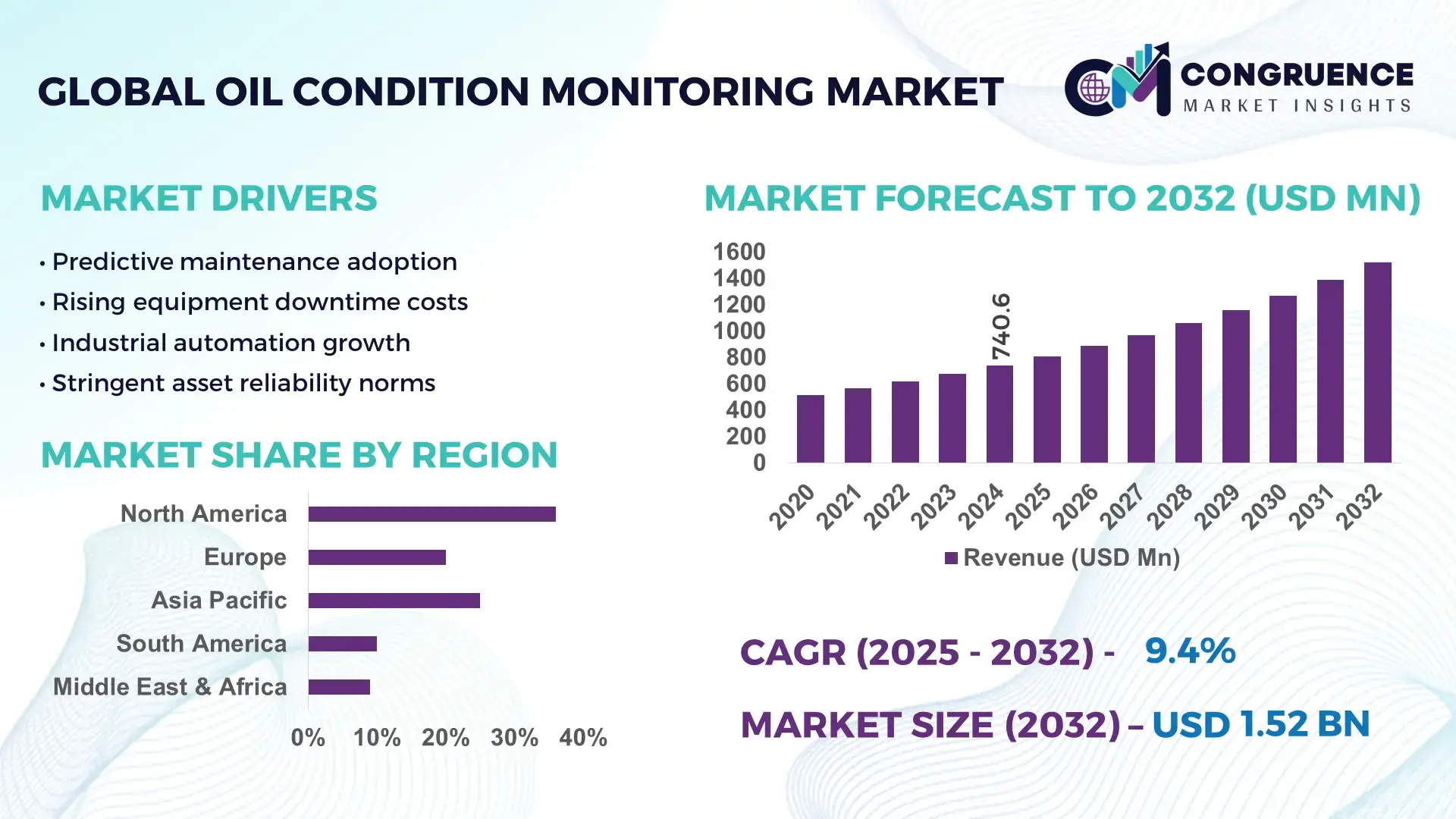

The Global Oil Condition Monitoring Market was valued at USD 740.63 Million in 2024 and is anticipated to reach a value of USD 1519.65 Million by 2032 expanding at a CAGR of 9.4% between 2025 and 2032. This expansion is driven by the accelerating shift toward predictive and condition-based maintenance across asset-intensive industries to minimize equipment failures and optimize operational efficiency.

The United States holds a commanding position in the Oil Condition Monitoring Market, supported by large-scale industrial production capacity and sustained investment in reliability-centered maintenance. The country hosts more than 900,000 manufacturing and industrial facilities, with oil analysis widely deployed in power generation, aerospace, mining, railways, and commercial fleets. Industrial maintenance expenditure in the U.S. exceeds USD 300 billion annually, with condition monitoring solutions accounting for a growing proportion. Advanced oil analysis laboratories process millions of samples per year, while widespread adoption of Industry 4.0 has enabled deployment of AI-driven oil sensors, online analyzers, and cloud-based diagnostics across utilities, manufacturing plants, and transportation networks.

Market Size & Growth: USD 740.63 Million in 2024, projected to reach USD 1519.65 Million by 2032, registering a CAGR of 9.4% due to rising predictive maintenance integration.

Top Growth Drivers: Predictive maintenance adoption ~62%, asset downtime reduction ~35%, maintenance cost efficiency improvement ~28%.

Short-Term Forecast: By 2028, industrial operators are expected to realize up to 22% reduction in unplanned maintenance expenses through continuous oil condition monitoring.

Emerging Technologies: AI-powered oil diagnostics, real-time online oil sensors, cloud-connected condition monitoring platforms.

Regional Leaders: North America projected at ~USD 520 Million by 2032 with strong automation uptake, Europe ~USD 410 Million driven by regulatory compliance, Asia Pacific ~USD 460 Million supported by rapid industrial expansion.

Consumer/End-User Trends: Increasing usage among power utilities, mining operations, manufacturing plants, and large commercial vehicle fleets.

Pilot or Case Example: A 2023 power generation pilot recorded a 30% reduction in unplanned downtime using real-time oil monitoring systems.

Competitive Landscape: Leading company holding approximately 18% share, followed by SGS, Bureau Veritas, Intertek, Parker Hannifin, and ALS Limited.

Regulatory & ESG Impact: Stricter emissions norms and sustainability mandates accelerating adoption of oil condition monitoring practices.

Investment & Funding Patterns: Over USD 1.2 Billion invested recently in sensor innovation, digital oil analytics, and condition monitoring platforms.

Innovation & Future Outlook: Growing convergence with digital twins, IoT ecosystems, and enterprise asset management software.

The Oil Condition Monitoring Market supports key sectors such as power generation, oil & gas, mining, automotive and transportation, and heavy manufacturing, with power and industrial machinery contributing the highest demand. Technological advancements including inline oil sensors, automated sampling, and machine-learning-based diagnostics are improving fault detection accuracy and maintenance response times. Regulatory focus on emissions control, waste oil reduction, and energy efficiency continues to influence adoption, particularly in North America and Europe, while Asia Pacific demand is fueled by industrial growth and infrastructure investment. Future market development is expected to center on real-time analytics, remote monitoring, and sustainability-driven maintenance optimization.

The Oil Condition Monitoring Market has become strategically relevant as industries transition from reactive and preventive maintenance toward data-driven asset reliability models. Oil condition monitoring supports early fault detection in gearboxes, turbines, compressors, engines, and hydraulic systems, enabling operators to reduce catastrophic failures and extend equipment life. AI-enabled online oil sensors deliver approximately 40% improvement in fault detection accuracy compared to traditional periodic laboratory oil analysis, allowing real-time intervention rather than delayed corrective action. Asia Pacific dominates in volume due to its extensive manufacturing base and heavy equipment deployment, while Europe leads in adoption with nearly 58% of large industrial enterprises integrating oil condition monitoring into predictive maintenance programs. By 2028, AI-based anomaly detection and cloud analytics are expected to reduce unplanned equipment downtime by nearly 25% across asset-intensive industries. From an ESG and compliance perspective, firms are committing to lubricant lifecycle optimization and waste reduction targets, including up to 30% reduction in waste oil disposal by 2030 through extended oil drain intervals and contamination control. In 2023, Germany’s power generation sector achieved a 28% reduction in bearing-related failures by deploying continuous oil condition monitoring integrated with digital twin platforms. Looking ahead, the Oil Condition Monitoring Market is positioned as a foundational pillar for operational resilience, regulatory compliance, and sustainable industrial growth, supporting smarter maintenance decisions, lower environmental impact, and long-term asset performance optimization.

Predictive maintenance adoption is a primary driver accelerating demand for oil condition monitoring solutions. Industrial operators increasingly recognize that lubricant condition is a leading indicator of machine health, enabling early detection of wear, contamination, and degradation. Studies across heavy industries show that predictive maintenance programs incorporating oil analysis can reduce maintenance-related equipment failures by up to 45% and extend asset service life by 20–30%. Power utilities, mining operators, and commercial fleet owners are integrating oil condition data into centralized monitoring platforms to optimize maintenance intervals and reduce spare parts inventory. As machinery becomes more automated and capital-intensive, reliance on oil condition monitoring continues to expand as a critical enabler of operational continuity and cost control.

Despite its benefits, adoption of oil condition monitoring faces restraints related to upfront costs and system complexity. Online oil sensors, automated sampling systems, and advanced analytics platforms require significant capital investment, particularly for small and mid-sized industrial operators. Integration with existing maintenance software, SCADA systems, and enterprise asset management platforms can add technical and training challenges. In traditional facilities, retrofitting legacy equipment for continuous oil monitoring may require production downtime and additional infrastructure. These factors can slow adoption, especially in price-sensitive markets where manual oil sampling and basic preventive maintenance practices remain prevalent.

Digital transformation presents substantial opportunities for the Oil Condition Monitoring Market through integration with Industry 4.0 ecosystems. Cloud connectivity, machine learning, and advanced data visualization enable centralized monitoring of geographically dispersed assets. Industrial firms adopting smart factories increasingly seek real-time lubricant health data to complement vibration and thermal monitoring. Fleet operators and renewable energy providers are deploying oil condition monitoring to support remote asset management and reduce service visits. Additionally, growing emphasis on sustainability creates opportunities for solutions that optimize lubricant usage, extend oil life, and support circular economy initiatives by reducing waste oil generation.

A key challenge facing the Oil Condition Monitoring Market is the shortage of skilled professionals capable of interpreting oil analysis data and translating insights into actionable maintenance decisions. Advanced diagnostics involving particle analysis, spectroscopy, and AI-driven alerts require specialized expertise. Inconsistent data quality, varying sampling practices, and lack of standardized thresholds across industries can lead to misinterpretation or underutilization of insights. Organizations without trained reliability engineers may struggle to realize full value from oil condition monitoring investments, limiting performance improvements despite technology deployment.

Expansion of Real-Time Online Oil Sensors Across Industrial Assets: Industrial operators are rapidly shifting from periodic laboratory oil analysis to continuous online oil monitoring systems. Over 48% of large manufacturing plants have installed inline oil sensors on critical assets such as turbines, compressors, and gearboxes to enable real-time contamination and wear detection. These systems have demonstrated up to 32% faster fault identification and nearly 27% reduction in unexpected equipment stoppages, supporting uninterrupted production and higher asset utilization rates.

Integration of AI and Advanced Analytics in Oil Diagnostics: Artificial intelligence is increasingly embedded in oil condition monitoring platforms to enhance predictive accuracy. AI-driven oil analysis solutions now process more than 10 million data points per asset annually, enabling pattern recognition beyond manual interpretation. Enterprises deploying machine-learning-based diagnostics have reported up to 41% improvement in maintenance decision accuracy and nearly 35% reduction in false alarms compared to rule-based oil analysis systems, driving confidence in automated maintenance workflows.

Growing Adoption in Renewable Energy and Power Infrastructure: Oil condition monitoring is gaining traction in wind turbines, hydroelectric generators, and thermal power plants to protect high-value rotating equipment. Nearly 44% of newly commissioned wind turbines are now equipped with oil condition monitoring for gearboxes and hydraulic systems, contributing to a 29% reduction in gearbox-related failures. Power utilities using continuous oil monitoring have also extended oil drain intervals by up to 25%, lowering lubricant consumption and maintenance interventions.

Rising Focus on Sustainability and Lubricant Lifecycle Optimization: Sustainability-driven maintenance strategies are reshaping oil condition monitoring adoption across industries. Around 52% of industrial firms now use oil condition data to support lubricant reuse, filtration, or extended service intervals. These practices have resulted in approximately 30% reduction in waste oil disposal volumes and up to 18% lower lubricant procurement requirements, aligning maintenance operations with environmental compliance targets and long-term cost optimization goals.

The Oil Condition Monitoring Market is segmented based on type, application, and end-user, reflecting the diverse ways oil analysis technologies are deployed across asset-intensive industries. By type, the market spans laboratory-based oil analysis, portable onsite testing solutions, and online continuous oil monitoring systems, each serving distinct maintenance strategies and asset criticality levels. Application-wise, oil condition monitoring is used extensively in engines, turbines, gearboxes, compressors, and hydraulic systems, where lubricant health directly impacts operational reliability. End-user segmentation highlights strong adoption across power generation, oil and gas, manufacturing, mining, transportation, and marine sectors. Segmentation trends indicate a clear shift toward continuous monitoring and real-time diagnostics in high-risk and high-value equipment, while traditional laboratory analysis remains relevant for compliance, periodic health checks, and secondary assets. Decision-makers increasingly align segmentation choices with asset criticality, downtime cost exposure, regulatory requirements, and digital maintenance maturity.

Laboratory oil analysis currently represents the leading product type, accounting for approximately 46% of overall adoption, driven by its standardized testing methods, broad contaminant detection capability, and strong acceptance across regulated industries. Portable onsite oil analysis systems account for around 28% of adoption, offering faster diagnostics and reduced sample turnaround times for field operations. However, online continuous oil condition monitoring is the fastest-growing type, expanding at an estimated CAGR of 12.8%, supported by rising demand for real-time data and automated alerts. Online systems currently represent about 18% of adoption but are gaining traction rapidly in power plants, wind turbines, and heavy manufacturing assets where unplanned downtime costs are highest. The remaining niche and hybrid solutions, including semi-online and integrated sensor-lab models, together contribute nearly 8% of adoption, mainly in specialized industrial environments.

Engines remain the leading application segment, representing nearly 38% of oil condition monitoring usage, due to widespread deployment across transportation fleets, power generation units, and industrial machinery. Gearboxes and turbines together account for approximately 34% of applications, reflecting their sensitivity to lubricant degradation and wear debris. Hydraulic systems and compressors form a combined 20% share, primarily in manufacturing, construction, and process industries. Among these, wind turbine gearboxes and industrial turbines represent the fastest-growing application area, expanding at an estimated CAGR of 11.6%, supported by renewable energy capacity expansion and reliability mandates. Adoption in auxiliary and specialty equipment makes up the remaining 8%, serving niche industrial processes.

Power generation is the leading end-user segment, accounting for approximately 34% of total adoption, driven by the need to protect high-value turbines, generators, and auxiliary systems operating under continuous load. Manufacturing follows closely with about 27% adoption, particularly in automotive, metals, and process industries where equipment uptime directly impacts output. Oil and gas, mining, transportation, and marine sectors together contribute nearly 31% of usage, reflecting widespread reliance on heavy rotating and hydraulic equipment. Renewable energy operators represent the fastest-growing end-user group, expanding at an estimated CAGR of 13.2%, fueled by large-scale wind and hydro installations and remote asset management needs. Other end-users, including railways and construction fleets, account for the remaining 8%, with adoption rates exceeding 45% in large fleet operators.

North America accounted for the largest market share at 36.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

Regional performance of the Oil Condition Monitoring Market reflects industrial maturity, asset density, and digital maintenance readiness. North America leads due to high penetration of predictive maintenance across power generation, aerospace, and manufacturing, supported by over 70% adoption of condition-based maintenance among large enterprises. Europe follows with approximately 28.4% share, driven by regulatory compliance, sustainability mandates, and advanced industrial automation. Asia-Pacific holds nearly 24.6% share, supported by rapid expansion of manufacturing capacity, energy infrastructure, and heavy equipment deployment across China, India, and Southeast Asia. South America and the Middle East & Africa together contribute around 10.2%, where adoption is closely tied to oil & gas, mining, and infrastructure investments. Regional demand patterns highlight increasing deployment of online oil monitoring systems, rising integration with digital asset management platforms, and growing focus on lubricant lifecycle optimization across all geographies.

How is advanced industrial digitization shaping maintenance intelligence adoption?

North America represents approximately 36.8% of the Oil Condition Monitoring Market, supported by extensive deployment across power generation, aerospace, automotive manufacturing, and large commercial fleets. Regulatory emphasis on operational safety and equipment reliability has accelerated adoption of condition-based maintenance practices across utilities and industrial operators. Digital transformation initiatives have resulted in over 65% of large enterprises integrating oil condition data with enterprise asset management systems. Technological advancements include AI-enabled diagnostics, cloud-based oil analysis dashboards, and real-time sensor deployment in turbines and compressors. Local players are expanding automated oil laboratories and inline sensor portfolios to support predictive maintenance contracts. Consumer behavior in this region shows higher enterprise adoption in capital-intensive industries, with over 60% of operators prioritizing real-time monitoring over periodic oil sampling to minimize downtime and maintenance risk.

Why is compliance-driven maintenance intelligence accelerating adoption?

Europe accounts for nearly 28.4% of the Oil Condition Monitoring Market, with strong demand from Germany, the United Kingdom, France, and the Nordic countries. Regulatory bodies and sustainability frameworks have driven adoption of oil analysis to support energy efficiency and waste reduction targets. Over 55% of industrial firms in Western Europe use oil condition monitoring as part of certified maintenance and compliance programs. Emerging technologies such as explainable AI diagnostics and digital twins are increasingly deployed to meet transparency requirements. Local solution providers focus on integrated oil monitoring platforms aligned with ISO and environmental standards. Consumer behavior reflects a strong preference for traceable, auditable Oil Condition Monitoring solutions, particularly in energy, rail, and heavy manufacturing sectors.

What factors are accelerating large-scale industrial monitoring deployment?

Asia-Pacific holds around 24.6% of the Oil Condition Monitoring Market and ranks as the fastest-growing region by volume. China, India, and Japan represent the largest consuming countries, driven by expanding manufacturing output, power capacity additions, and infrastructure development. The region operates over 40% of the world’s industrial machinery installations, increasing demand for equipment reliability solutions. Regional technology trends include cost-efficient online oil sensors, mobile-based diagnostics, and centralized monitoring hubs supporting multi-site operations. Local players are scaling oil analysis laboratories and digital platforms to serve industrial clusters. Consumer behavior varies widely, with adoption driven by large manufacturing groups and state-owned utilities seeking to reduce maintenance costs and extend asset life.

How are energy and mining investments influencing monitoring demand?

South America contributes approximately 6.1% to the Oil Condition Monitoring Market, with Brazil and Argentina leading regional adoption. Demand is closely linked to oil & gas operations, mining activities, and power generation infrastructure. National energy modernization programs have increased deployment of oil analysis for turbines, compressors, and heavy mining equipment. Government incentives for operational efficiency and reduced downtime have supported gradual adoption of predictive maintenance tools. Local service providers focus on portable oil analysis and outsourced laboratory testing to address budget constraints. Consumer behavior indicates selective adoption, with monitoring prioritized for critical assets rather than full-fleet coverage.

Why is asset reliability becoming central to industrial modernization?

The Middle East & Africa region accounts for roughly 4.1% of the Oil Condition Monitoring Market, driven primarily by oil & gas, petrochemicals, power generation, and large-scale construction. The UAE, Saudi Arabia, and South Africa represent key growth countries, supported by industrial diversification and infrastructure investment programs. Technological modernization initiatives emphasize online oil monitoring for rotating equipment operating under extreme conditions. Regional regulations and trade partnerships encourage adoption of reliability-centered maintenance practices. Consumer behavior reflects a focus on high-value asset protection, with oil condition monitoring deployed mainly on mission-critical equipment rather than across entire asset portfolios.

United States – 29.4% market share – Strong industrial base, high predictive maintenance adoption, and extensive deployment across power generation and manufacturing assets.

Germany – 11.6% market share – Advanced industrial automation, regulatory-driven maintenance compliance, and widespread use of Oil Condition Monitoring in heavy machinery and energy systems.

The Oil Condition Monitoring Market is moderately fragmented, with over 85 active global competitors operating across laboratory-based, portable, and online monitoring segments. The top five companies—SGS, Bureau Veritas, Intertek, Parker Hannifin, and ALS Limited—collectively hold approximately 42% of the market, reflecting both strong market positioning and a competitive mix of established and emerging players. Key strategic initiatives shaping competition include partnerships with industrial OEMs, launch of AI-enabled real-time oil analysis platforms, acquisitions of specialized laboratories, and expansion into renewable energy and remote monitoring applications. Product innovation is a central differentiator, with over 35% of firms investing in digital dashboards, cloud-connected sensors, and predictive analytics solutions to enhance diagnostic accuracy. Regional expansion is also prominent, particularly in Asia-Pacific and South America, where industrial growth and infrastructure development are creating new opportunities. Competitors increasingly leverage strategic collaborations with engineering service providers and technology vendors to integrate oil monitoring into enterprise asset management systems, supporting operational efficiency, compliance, and sustainability goals. Overall, market dynamics indicate high innovation intensity, with continuous technology upgrades and strategic alliances defining leadership positions.

Parker Hannifin

ALS Limited

Emerson Electric

Shell Global Solutions

Lubrication Engineers

Fluitec International

Royal Dutch Shell Oil Analytical Services

The Oil Condition Monitoring Market is increasingly shaped by advanced technologies that enhance predictive maintenance, operational efficiency, and equipment reliability. Online and real-time oil sensors now cover over 45% of high-value rotating machinery in industrial facilities, offering continuous monitoring of viscosity, acidity, water content, and particulate contamination. These sensors provide actionable alerts within minutes, reducing unplanned downtime by up to 28% compared to traditional lab-based oil analysis. Portable oil analyzers have gained adoption in field operations, enabling on-site testing for more than 60% of maintenance crews in mining, construction, and energy sectors, reducing sample turnaround from days to hours.

Emerging AI and machine learning platforms are transforming data interpretation and predictive analytics. These systems process millions of data points per asset annually to detect anomalies, predict component failures, and recommend maintenance interventions. In 2024, AI-enabled diagnostics improved early fault detection accuracy by approximately 38% across utility and manufacturing plants. Cloud-based oil monitoring platforms now allow centralized monitoring for multi-site operations, supporting over 1,200 industrial facilities globally with remote asset management.

Digital twin technology is being integrated with oil condition monitoring to simulate equipment behavior and lubrication performance under various operating conditions. Over 55% of large industrial enterprises have piloted digital twin-based monitoring, observing up to 25% improvement in maintenance planning accuracy. Furthermore, predictive maintenance ecosystems increasingly leverage IoT connectivity, automated sampling, and mobile-access dashboards to enhance real-time decision-making and extend lubricant service life, reinforcing operational reliability and cost efficiency across sectors.

The Oil Condition Monitoring Market Report provides a comprehensive examination of the technologies, segments, regional landscapes, and industry applications shaping this critical maintenance domain. The report covers product types including laboratory‑based oil analysis, portable on‑site testing solutions, and online continuous monitoring systems, detailing sensor technologies, analytical techniques, and integration models with enterprise maintenance platforms. It examines application categories such as engines, turbines, compressors, gearboxes, and hydraulic systems, outlining usage patterns, diagnostic needs, and operational priorities across sectors.

Geographic scope includes major regions—North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—highlighting regional adoption trends, infrastructure drivers, regulatory influences, and technology penetration rates. The report also segments end users, revealing deployment dynamics across power generation, oil & gas, manufacturing, transportation, marine, and heavy industries, while identifying variations in consumer priorities and maintenance practices. Additionally, it assesses emerging niches such as IoT‑enabled sensor networks, AI‑driven analytics, digital twin integration, and subscription‑based monitoring services, illustrating how these innovations expand coverage and diagnostic depth.

Attention to technical methodologies—spectroscopy, particle counting, fluid viscosity measurement, and chemical property analysis—provides detailed insight into the tools and metrics underpinning oil condition assessment. The report further addresses operational integration with enterprise asset management and condition‑based maintenance frameworks, offering decision‑makers a structured view of capabilities, implementation practices, and strategic technology investments across global industrial environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 740.63 Million |

|

Market Revenue in 2032 |

USD 1519.65 Million |

|

CAGR (2025 - 2032) |

9.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

SGS, Bureau Veritas, Intertek, Parker Hannifin, ALS Limited, Emerson Electric, Shell Global Solutions, Lubrication Engineers, Fluitec International, Royal Dutch Shell Oil Analytical Services |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |