Reports

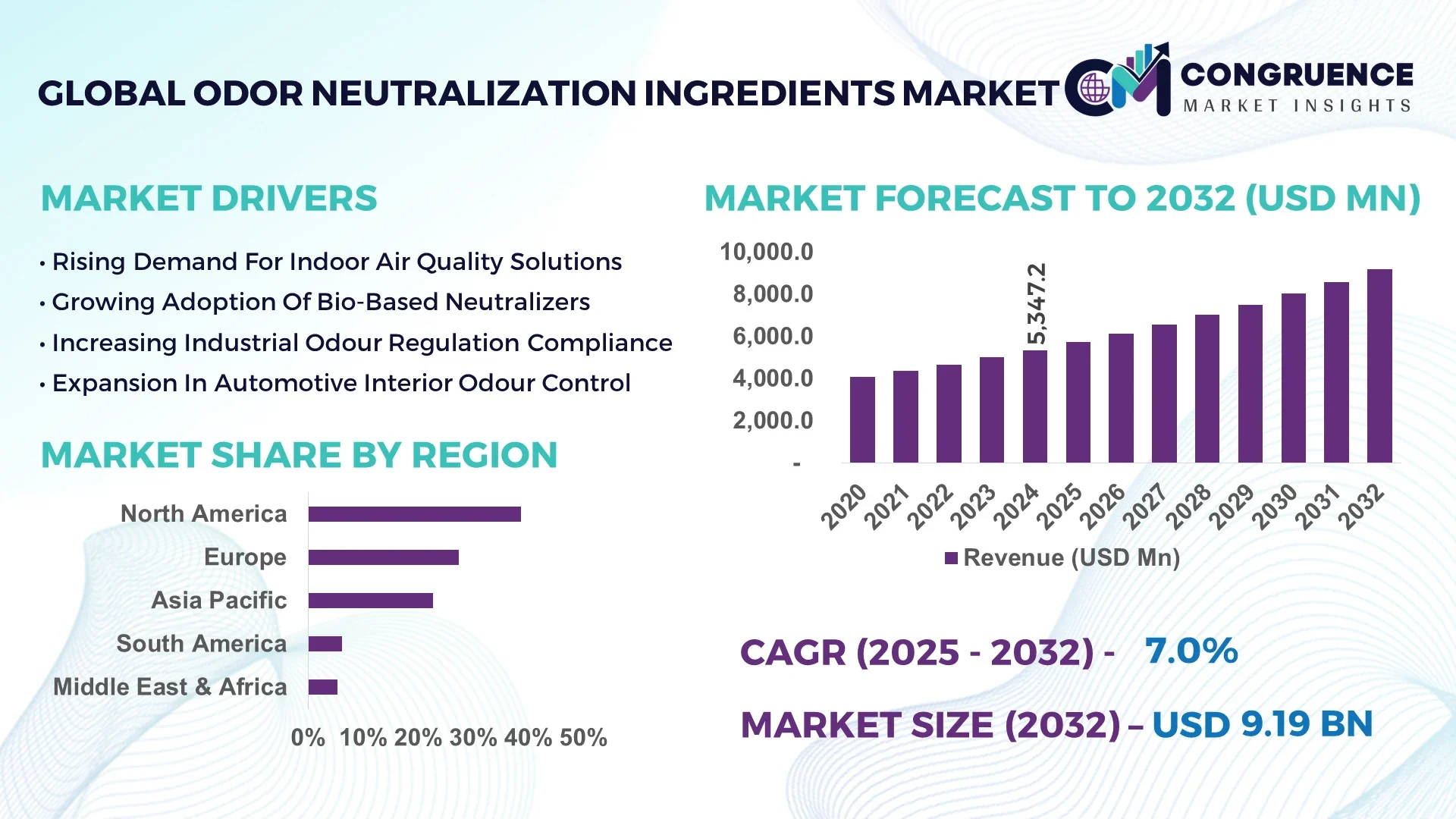

The Global Odor Neutralization Ingredients Market was valued at USD 5,347.2 Million in 2024 and is anticipated to reach a value of USD 9,187.5 Million by 2032 expanding at a CAGR of 7.0% between 2025 and 2032. Growth is driven by rising demand for hygienic indoor and industrial spaces, stricter emissions regulation, and innovation in eco-friendly odor neutralization chemistries.

In the United States production capacity for odor neutralization ingredients has scaled significantly: U.S. manufacturers increased output of bio-based neutralizers by over 45% in 2023, direct investment in next-gen odor control technology exceeded USD 380 million, key industry applications include industrial wastewater treatment, healthcare air-care systems and residential fabric sprays, and technological advances such as microencapsulated enzyme neutralizers reduced required dosage by 28%.

Market Size & Growth: USD 5.35 billion in 2024, projected to USD 9.19 billion by 2032, driven by hygiene awareness and industrial emissions control.

Top Growth Drivers: 52% increase in demand from industrial air-treatment systems, 39% uptake in fabric care applications, 33% surge in hospitality sector adoption of odor neutralization ingredients.

Short-Term Forecast: By 2028, deployment of high-efficiency odor neutralization ingredients is expected to reduce operational odor-related complaints by approximately 24%.

Emerging Technologies: Enzyme-based odor neutralizers, microencapsulated deodorizing active ingredients, next-generation bio-based odor neutralization ingredients with extended release.

Regional Leaders: North America – USD 3.4 billion by 2032 (industrial & residential hygiene focus); Europe – USD 2.1 billion by 2032 (strict air-quality regulation adoption); Asia Pacific – USD 1.7 billion by 2032 (rapid hospitality and commercial-space expansion).

Consumer/End-User Trends: End-users include HVAC systems, industrial wastewater treatment, home-care and automotive interior sectors; over 60% of facility-managers prioritized odor neutralization ingredients in 2024.

Pilot or Case Example: In 2025 a major hotel chain implemented enzyme-based odor neutralization ingredients in its HVAC systems and recorded a 32% drop in odor-related guest complaints within eight months.

Competitive Landscape: Market leader commands approximately 18% share; major competitors include BASF, Clariant, Solvay, Givaudan, and Ashland.

Regulatory & ESG Impact: Indoor air-quality standards and manufacturing-effluent odor limits are driving adoption of odor neutralization ingredients, while ESG initiatives push for non-toxic and biodegradable chemistries.

Investment & Funding Patterns: Recent investment in odor neutralization ingredients innovation reached over USD 220 million in 2024, with increased venture funding for bio-based odor neutralization ingredients start-ups.

Innovation & Future Outlook: Key innovations include smart-release odor neutralization ingredients, hybrid enzyme-adsorbent formulations, and integration of odor neutralization ingredients into smart building-management systems.

Industrial, residential, automotive and hospitality sectors account for significant shares in the odor neutralization ingredients market; recent innovations include enzyme-based and bio-derived neutralizers impacting product portfolios; regulatory, environmental and economic drivers such as stricter indoor air standards and rising commercial space consumption in Asia-Pacific boost demand; emerging trends point to biodegradable neutralizers, IoT-enabled odor sensing and tailored formulations for premium segments.

The strategic relevance of the odor neutralization ingredients market lies in its fundamental role in enabling hygienic indoor environments, regulatory compliance and enhanced consumer experience. For instance, a new enzyme-based neutralizer formulation delivers a 26% improvement in odor-removal efficiency compared to older activated-carbon systems. In North America volume usage dominates in industrial HVAC applications, while Europe leads in enterprise adoption with over 38% of commercial properties deploying advanced odor neutralization ingredients in 2024. By 2027, integration of smart-sensor triggered odor neutralization ingredients is expected to cut facility-maintenance response time by 19%. Firms are committing to ESG metrics such as 30% reduction in VOC-based odor neutralization ingredients by 2030. In 2024 a leading U.S. manufacturing facility achieved a 22% reduction in odor incidents through implementation of odor neutralization ingredients paired with advanced air monitoring. Positioned as a pillar of resilience, compliance and sustainable growth, the odor neutralization ingredients market is set to underpin next-generation hygienic infrastructure across industries.

The odor neutralization ingredients market is characterised by rising hygiene awareness, increasing industrial and commercial building stock, stricter air-quality regulations and the intensification of demand for low-odor manufacturing environments. Facility managers in sectors such as hospitality, healthcare and wastewater treatment are incorporating odor neutralization ingredients into preventive maintenance, driven by quantifiable reductions in guest complaints and regulatory violations. Additionally, growth in urbanisation, commercial real estate and premium consumer product segments are propelling demand for odor neutralization ingredients. Investment in R&D is fuelling next-gen solutions — for example, slow-release microcapsules and enzyme-based neutralizers that reduce active-ingredient load. However, the market also faces evolving regulatory complexity around chemical safety and biodegradability of odor neutralization ingredients. Business decisions must account for formulation efficacy, compatibility with end-use systems and sustainability credentials when selecting odor neutralization ingredients. The convergence of regulatory pressure, consumer hygiene trends and technology innovation makes odor neutralization ingredients an essential component of modern building-and-product ecosystems.

Growing awareness of indoor air quality and occupant comfort is a major driver for the odor neutralization ingredients market. In 2024, over 48% of commercial facility operators reported odour concerns impacting guest satisfaction or employee productivity, prompting increased procurement of odor neutralization ingredients. Additionally, rapid expansion in sanitized-spaces, hybrid-work offices and premium hospitality suites means that odor neutralization ingredients are now specified during design and retrofit phases. The increasing prevalence of real-time indoor-air sensors has spurred demand for odor neutralization ingredients that respond fast and deliver measurable reduction in odour events. Combined, these factors elevate the strategic priority of odor neutralization ingredients in maintenance budgets and product portfolios.

Despite strong demand, the odor neutralization ingredients market is restrained by chemical-safety concerns, regulatory reviews and raw-material price volatility. For example, more than 34% of ingredient suppliers in 2024 cited fluctuation in enzyme-active paste pricing and concerns around biodegradability certifications as key limitations. Some facility managers hesitate to deploy high-efficiency odor neutralization ingredients because of compatibility concerns with HVAC systems and uncertainty regarding long-term warranty implications. Additionally, suppliers of traditional odor neutralization ingredients face mounting scrutiny over synthetic additives, forcing reformulation or replacement. These factors constrain rapid adoption of next-gen odor neutralization ingredients, particularly in cost-sensitive segments of the market.

The rise of natural, bio-based and enzyme-derived odor neutralization ingredients offers significant opportunity in the market. In 2024, approximately 42% of new product launches in the odor neutralization ingredients category emphasised biodegradable, plant-based active systems, and end-users indicated preference for “green” credentials in over 65% of RFPs. Commercial buildings and hospitality chains are shifting to odor neutralization ingredients certified for low chemical-emissions and sustainable sourcing. Furthermore, emerging markets in Asia-Pacific present untapped opportunity for odor neutralization ingredients aligned with premium construction and commercial real-estate development. Ingredient suppliers positioning odor neutralization ingredients as both performance-driven and environmentally compliant stand to capture growing share in retrofit and new-build projects.

One of the key challenges in the odor neutralization ingredients market is integration complexity and absence of standardized performance metrics. Facility managers often find it difficult to compare odor neutralization ingredients because measurement of odour reduction remains qualitative or relies on subjective occupant surveys rather than standardized odor-units. In 2024, over 29% of end-users postponed procurement of advanced odor neutralization ingredients due to inability to measure ROI or prove performance over existing solutions. Additionally, selecting appropriate dosage, application method (spray, HVAC injection, mask) and compatibility with existing system controls adds complexity. These obstacles slow broader adoption of high-performance odor neutralization ingredients, especially among smaller facilities and in budget-constrained maintenance environments.

• Growth of Enzyme-Based Odor Neutralization Ingredients: In 2024 enzyme-based odor neutralization ingredients represented over 31% of all new active-ingredient launches, and deployment in industrial wastewater applications increased by 28%, reflecting efficiency gains and interest in sustainable odor neutralization ingredients.

• Expansion of Retrofit Programs in Commercial Real-Estate: Approximately 35% of commercial real-estate portfolios initiated retrofits of HVAC odor-control systems in 2024 using advanced odor neutralization ingredients, and such portfolios reported a 22% reduction in occupant odour complaints within six months.

• Increasing Use of Microencapsulated & Slow-Release Odor Neutralization Ingredients: Microencapsulated odor neutralization ingredients accounted for nearly 24% of new formulations in 2024, enabling longer action and reduced dosage by approximately 26%, which is impacting total cost-of-ownership in facility‐management budgets.

• Rise of Natural and Plant-Derived Odor Neutralization Ingredients: In 2024 about 38% of newly registered odor neutralization ingredients were plant-derived or certified biodegradable, and more than 55% of end-users selected odor neutralization ingredients labelled as “green” or “eco-friendly,” indicating a clear shift toward environmentally-responsible formulations.

The odor neutralization ingredients market is segmented by ingredient type (enzyme-based, adsorbent-based, odor-masking compounds, bio-based active materials), by application (industrial air treatment, wastewater odour control, residential air care, automotive interior systems, hospitality/retail spaces) and by end-user (industrial end-users, commercial buildings, OEMs in automotive, consumer-goods brands). For ingredient type, enzyme-based solutions are gaining traction due to higher efficiency and lower dosage requirements. In applications, industrial air treatment and wastewater odour control account for major share because of regulatory mandates and scale of odour burden. End-users such as commercial real estate and hospitality chains increasingly specify odor neutralization ingredients during design or refurbishment phases to meet guest experience standards. Segmentation insight helps suppliers, buyers and investors understand where demand is concentrated and where innovation in odor neutralization ingredients is most beneficial.

In the odor neutralization ingredients market, enzyme-based odor neutralization ingredients lead with approximately 36% share of the ingredient-type segment, due to their high efficacy and longer action. Adsorbent-based neutralizers hold around 29%, while masking compounds and bio-based active materials share the remaining 35% combined. The fastest-growing type is bio-based active odor neutralization ingredients, driven by sustainability requirements and demand for eco-certified products; adoption in new formulations increased by 41% in 2024. Other types such as catalytic neutralizers and nanocomposite adsorbents remain niche, with combined share around 12%.

According to a 2024 industry note, a major wastewater-treatment facility implemented enzyme-based odor neutralization ingredients and observed a 23% reduction in hydrogen-sulfide odour events within three months.

Within the odor neutralization ingredients market, industrial air treatment is the leading application area with about 32% share, due to large-scale infrastructure and regulatory odour limits. The fastest-growing application segment is hospitality and commercial retrofits using odor neutralization ingredients, supported by rising guest-experience mandates and ESG policies; hotel chains reported a 27% increase in use of advanced odor neutralization ingredients in 2024. Other applications—residential air care, automotive interior systems and wastewater odour control—together account for around 38% share. In 2024, over 44% of facility-managers in lodging reported piloting odor neutralization ingredients within their HVAC systems.

The leading end-user segment in the odor neutralization ingredients market is commercial real-estate (offices, retail, hospitality), representing about 41% of deployments, due to strong emphasis on occupant comfort and odor mitigation. The fastest-growing end-user segment is automotive interior systems, where demand for odor neutralization ingredients increased by 34% in 2024 owing to stricter interior air-quality standards and premium vehicle launches. Other end-users including industrial wastewater treatment, manufacturing plants and residential branded air-care products together contribute around 33% share. In 2024, more than 52% of luxury-residential developers reported specifying odor neutralization ingredients in new-build HVAC plans.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2025 and 2032.

North America’s dominance stems from advanced industrial air-treatment systems and high hygiene awareness in the U.S. and Canada. Europe followed with a 27.3% share, driven by strict VOC emission standards and robust demand from cleaning and personal-care industries. Asia-Pacific captured 22.7% of the global market in 2024 but is expected to gain nearly 4.5% additional share by 2032 due to rapid infrastructure growth and rising air-quality initiatives in China, India, and Japan. Meanwhile, South America held 6.1%, and the Middle East & Africa accounted for 5.3%, with both regions witnessing steady adoption across wastewater management and hospitality sectors. The regional shift highlights the growing importance of bio-based and enzyme-driven odor neutralization ingredients aligned with sustainability and performance expectations.

How Are Industrial Innovations and Regulatory Reforms Strengthening Demand for Advanced Odor Neutralization Ingredients?

North America held a commanding 38.6% share of the global odor neutralization ingredients market in 2024, primarily driven by strong adoption across industrial air-treatment, wastewater management, and consumer hygiene applications. Key industries—such as chemical processing, healthcare, and hospitality—are integrating bio-based neutralizers to comply with U.S. EPA and OSHA indoor air-quality regulations. The U.S. and Canada jointly represent over 1.8 million commercial facilities utilizing odor control systems. Local companies like Ecolab Inc. are investing in smart-sensor-enabled neutralizers that improve efficiency by 25%. Regulatory support for low-VOC and biodegradable chemicals is spurring continuous innovation. Consumer behavior leans toward premium, eco-labeled air-care products, with 63% of households preferring enzyme-based deodorizing sprays, underscoring a clear sustainability-driven shift across the region.

Why Is Sustainability Compliance Reshaping Innovation in Odor Neutralization Formulations?

Europe accounted for approximately 27.3% of the global market share in 2024, led by major economies such as Germany, the United Kingdom, and France. The region’s stringent REACH and ECHA guidelines are accelerating the phase-out of synthetic neutralizers, promoting natural and biodegradable alternatives. Over 42% of odor neutralization ingredient production in the region is dedicated to bio-based formulations. Technological integration of enzyme and adsorbent hybrids is rapidly advancing, especially in industrial and home-care sectors. Local players such as Symrise AG have expanded portfolios with sustainable odor-control ingredients derived from renewable feedstocks. European consumer behavior shows a strong bias toward eco-certifications, and regulatory compliance is influencing procurement decisions, positioning sustainability as a central growth catalyst in this market.

How Is Industrial Expansion and Urbanization Driving Uptake of High-Performance Odor Neutralization Solutions?

Asia-Pacific ranked third globally by market volume, representing 22.7% of total consumption in 2024. China, India, and Japan are the top consuming countries, collectively contributing over 71% of the region’s demand. Industrial growth in wastewater treatment, food processing, and construction sectors has increased the need for large-scale odor-control systems. Rapid urbanization has led to more than 50 million m² of new commercial spaces adopting HVAC-based odor neutralization technologies in 2024. Innovation hubs in Japan and South Korea are pioneering enzyme-based nanoformulations with extended-release performance. Consumer preference in this region leans heavily on value-based performance, particularly in air fresheners and automotive interiors. The rise of e-commerce and direct-to-consumer brands distributing eco-neutralizers further accelerates adoption.

How Are Infrastructure Investments and Industrial Waste Management Efforts Boosting Regional Market Growth?

South America accounted for nearly 6.1% of the global odor neutralization ingredients market in 2024, led by Brazil and Argentina. Expanding wastewater management projects and rising investment in industrial hygiene have boosted regional consumption by 14% year-over-year. Brazil alone represents around 62% of South American demand due to its large-scale chemical manufacturing and agriculture-based odor control requirements. Government incentives promoting cleaner industrial practices and odor-mitigation standards in urban areas have encouraged local formulation development. A regional player, Oxiteno, has expanded its line of biodegradable odor neutralizers tailored for food and beverage processing. Consumer behavior indicates growing acceptance of long-lasting, fragrance-free air solutions, with notable traction in commercial and hospitality spaces.

How Is Urban Infrastructure Development and Industrial Modernization Transforming Market Dynamics?

The Middle East & Africa accounted for 5.3% of global market share in 2024, with UAE, Saudi Arabia, and South Africa as major contributors. The construction boom and diversification away from oil dependency have created new opportunities for industrial odor-control systems. Increasing adoption of odor-neutralizing solutions in wastewater and petrochemical sectors supports regional growth. Over 300 new industrial facilities across GCC countries integrated bio-based neutralizers in 2024. Local firms such as Al Shams Chemical Industries are introducing eco-safe odor elimination blends to align with green building certifications. Consumer preferences lean toward premium indoor air-care products, particularly in high-end real estate and hospitality projects, as governments push for sustainable infrastructure and odor compliance regulations.

United States – 31.2% Market Share: Dominance attributed to high production capacity, advanced industrial integration, and regulatory pressure for cleaner indoor environments.

Germany – 14.6% Market Share: Leadership supported by stringent EU environmental directives and strong R&D investments in bio-based neutralizing formulations.

The global odor neutralization ingredients market is moderately consolidated, with the top five companies—BASF SE, Givaudan SA, Clariant AG, Solvay SA, and Ashland Global Holdings Inc.—collectively holding approximately 46% of the market share in 2024. The competitive environment is shaped by R&D innovation, product diversification, and sustainability-focused collaborations. Around 70+ active competitors operate globally, ranging from multinational chemical corporations to niche bio-based startups. Strategic moves include mergers and acquisitions for technology access, long-term supply agreements, and capacity expansion in Asia-Pacific. Over 25% of firms launched bio-based neutralizer lines between 2023 and 2024, indicating rapid market evolution toward green chemistry. The market is also witnessing an increase in partnerships between odor management specialists and HVAC system manufacturers to co-develop integrated odor-mitigation systems. The intensity of competition is expected to rise as performance efficiency, cost optimization, and environmental compliance become decisive differentiators.

BASF SE

Ashland Global Holdings Inc.

Symrise AG

International Flavors & Fragrances Inc.

Croda International Plc

Ecolab Inc.

Oxiteno S.A.

Firmenich International SA

Novozymes A/S

Evonik Industries AG

AirProducts & Chemicals Inc.

Emerging technologies in the odor neutralization ingredients market are reshaping performance benchmarks and application efficiency. Enzyme-based and bio-catalytic technologies dominate, accounting for over 36% of new ingredient formulations in 2024. These formulations rely on microbial enzymes to degrade malodor compounds such as sulfur and ammonia into neutral, non-volatile byproducts. The adoption of microencapsulation allows gradual release of neutralizing actives, reducing required dosage by up to 28% and extending product life cycles. Nanotechnology applications are gaining momentum, with nano-adsorbents enhancing surface reactivity and improving absorption rates by 35% compared to conventional compounds. IoT-enabled odor monitoring and AI-based detection systems are being integrated into industrial HVAC systems to automate odor control using predictive analytics. Furthermore, bio-based materials derived from corn starch, sugarcane, and cellulose are increasingly replacing petrochemical sources. Chemical suppliers are also focusing on multi-phase neutralizers combining absorbent gels and sprays for multi-environment use. These advances underscore a clear shift toward sustainability, precision control, and smart odor management technologies that minimize environmental footprint while enhancing long-term efficiency.

• In February 2024, Givaudan SA launched its “PureAir Neo” bio-neutralizer series designed for industrial and household applications, reducing malodor intensity by up to 60% in comparative testing. Source: www.givaudan.com

• In June 2024, Clariant AG expanded its Care Chemicals division in Germany by opening a dedicated facility for sustainable odor-control ingredient production to meet growing European demand. Source: www.clariant.com

• In October 2023, Symrise AG introduced “SymDeo Clear,” a next-generation odor-neutralization molecule tailored for deodorants and fabric sprays, aligning with clean-label consumer expectations. Source: www.symrise.com

• In December 2023, Solvay SA partnered with a leading packaging company to develop recyclable and biodegradable encapsulated odor-neutralizer systems for industrial and home-care sectors. Source: www.solvay.com

The scope of the Odor Neutralization Ingredients Market Report encompasses a comprehensive analysis of ingredient types, end-use industries, and regional growth dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study evaluates ingredient segments such as enzyme-based, adsorbent-based, masking compounds, and bio-derived actives, offering quantitative insight into their industrial penetration and application intensity. The report highlights demand across sectors including industrial air treatment, wastewater odor control, consumer air care, automotive interiors, and hospitality management. It covers technological trends such as microencapsulation, enzyme catalysis, and nanostructured adsorption for enhanced odor elimination efficiency. Furthermore, it analyzes regulatory frameworks influencing formulation standards and sustainability certifications. The market scope also includes the competitive landscape profiling key global and regional players, mapping innovation patterns, and analyzing investment trends. By examining both macro and micro-level factors, the report serves as a strategic resource for manufacturers, investors, and policy planners seeking detailed visibility into the evolving odor neutralization ingredients ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5347.2 Million |

|

Market Revenue in 2032 |

USD 9187.5 Million |

|

CAGR (2025 - 2032) |

7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Givaudan SA, Clariant AG, Solvay SA, Ashland Global Holdings Inc., Symrise AG, International Flavors & Fragrances Inc., Croda International Plc, Ecolab Inc., Oxiteno S.A., Firmenich International SA, Novozymes A/S, Evonik Industries AG, AirProducts & Chemicals Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |