Reports

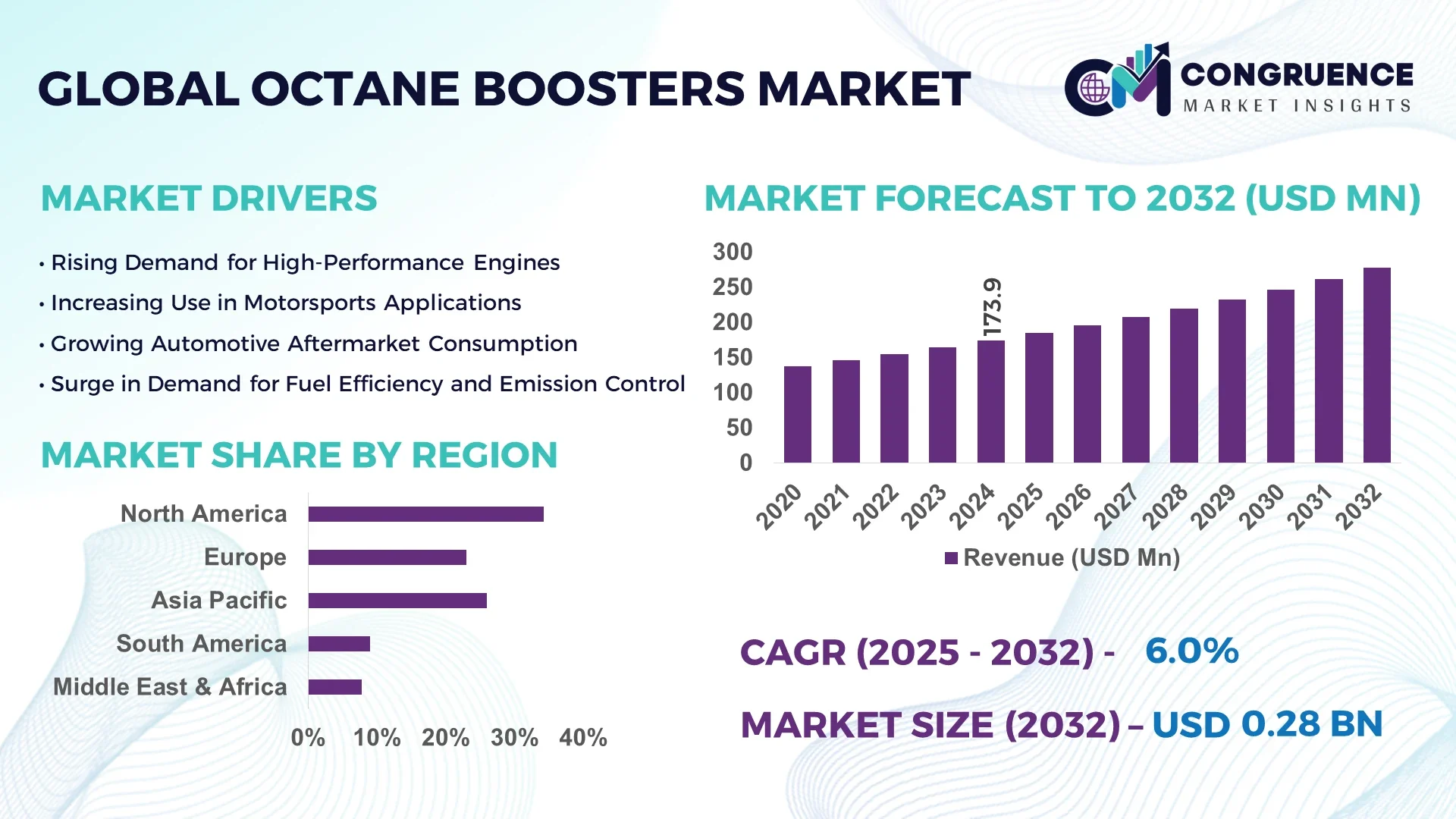

The Global Octane Boosters Market was valued at USD 173.94 Million in 2024 and is anticipated to reach a value of USD 277.24 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032.

The United States plays a key role in the octane boosters market, with robust production capacity supported by a dense network of petrochemical facilities, substantial investments in fuel additive technologies, and increasing demand from motorsports and premium automotive segments. Additionally, U.S.-based companies are integrating advanced automation in manufacturing for higher product consistency.

The Octane Boosters Market continues to evolve as industries focus on enhancing fuel performance and reducing engine knocking in combustion engines. Major end-use sectors include automotive, aviation, and marine, with the automotive sector driving the highest demand due to global efforts to meet stringent emission norms. Increasing production of high-performance vehicles and the growing aftermarket for automotive care products are also contributing to the market’s expansion. Recent innovations in eco-friendly and ethanol-compatible formulations have gained traction, aligning with tightening environmental regulations. Moreover, regional markets like Asia-Pacific are witnessing a surge in consumption driven by expanding vehicle ownership and infrastructural developments. Future trends indicate rising adoption of AI-driven quality control systems and growing interest in bio-based octane enhancers as sustainable alternatives.

Artificial Intelligence (AI) is reshaping the operational landscape of the Octane Boosters Market by introducing advanced analytics, real-time monitoring, and predictive modeling. AI-driven systems are enabling manufacturers to fine-tune chemical compositions of octane boosters with remarkable accuracy, ensuring consistent quality while reducing production costs. With AI integration, companies can simulate complex combustion scenarios to develop high-performance formulations suited for different engine types and fuel grades.

In the Octane Boosters Market, predictive maintenance powered by AI is minimizing unplanned downtimes in blending and packaging units, directly improving operational efficiency. Computer vision and machine learning algorithms are also being used for real-time inspection and defect detection, enhancing product integrity before distribution. AI is additionally helping firms to adapt to dynamic regulatory frameworks by automating compliance checks, reducing human errors, and improving turnaround times for product certifications.

On the supply chain side, AI is optimizing logistics by predicting demand fluctuations based on historical data, weather patterns, and regional fuel usage trends. This allows suppliers to manage inventory better, reduce storage costs, and enhance customer satisfaction. From a marketing perspective, AI tools are being employed to target niche customer segments with personalized campaigns based on vehicle types, fuel preferences, and regional demand. These developments are transforming how stakeholders in the Octane Boosters Market operate, innovate, and engage with customers in a competitive environment.

“In March 2024, a U.S.-based fuel additive manufacturer deployed an AI-powered combustion simulator that reduced R&D cycle times by 35% and enhanced the development of octane boosters tailored for ethanol-blended fuels, enabling faster regulatory approval and market readiness.”

The Octane Boosters Market is benefiting significantly from the rising popularity of vehicle tuning, customization, and performance optimization. Across the U.S., Europe, and Southeast Asia, the growing community of auto enthusiasts and racing professionals is propelling sales of premium-grade octane boosters. With more than 70% of enthusiasts opting for enhanced engine responsiveness, aftermarket demand for performance additives is accelerating. Additionally, car owners seeking better fuel economy and reduced engine knock are increasingly incorporating octane boosters in regular maintenance routines. Auto service centers and e-commerce platforms have also streamlined product accessibility, contributing to higher sales volumes. As performance upgrades become mainstream among younger demographics, the consumption of octane-enhancing fuel additives continues to rise globally.

One of the key restraints facing the Octane Boosters Market is the imposition of strict environmental regulations regarding fuel additives and chemical compositions. Governments across North America and Europe are phasing out certain metallic and aromatic compounds traditionally used in octane boosters due to their harmful emissions and non-biodegradable nature. This is particularly affecting formulations containing manganese or lead, which are being progressively banned or restricted. Compliance with REACH regulations in Europe and EPA standards in the U.S. requires manufacturers to invest heavily in R&D for eco-safe alternatives, thereby increasing operational costs. The regulatory landscape also delays product launches and limits market entry for smaller players, reducing innovation pace in some regions.

The increasing global focus on sustainable mobility is opening new opportunities within the Octane Boosters Market. Bio-based and ethanol-compatible octane boosters are gaining traction among fuel distributors and automakers aiming to reduce carbon footprints and meet emission reduction targets. In Brazil and the U.S., where ethanol-blended fuels are widely used, the demand for boosters compatible with E10 to E85 fuel blends is steadily growing. Innovations in plant-derived additives are creating viable alternatives to petroleum-based compounds, expanding product offerings in environmentally conscious markets. Additionally, government incentives supporting green chemistry and biofuel adoption are expected to further stimulate this emerging segment of the market.

A critical challenge in the Octane Boosters Market is ensuring consistent performance across a diverse range of engine types and fuel blends. Modern internal combustion engines vary widely in compression ratios, fuel injection technologies, and emission control systems. As a result, a one-size-fits-all octane booster formulation is rarely effective. Additives that perform optimally in high-octane race fuels may not yield the same results in ethanol-blended or low-octane fuels. Moreover, compatibility with oxygenated fuels like E85 presents formulation hurdles, requiring advanced chemical engineering. Manufacturers must invest in rigorous testing and customization to cater to these variables, adding to development time and costs, while also facing challenges in mass-market scalability.

Surging Demand for Lead-Free Formulations: Regulatory pressures and rising environmental concerns have accelerated the shift toward unleaded octane boosters. In 2024 alone, over 65% of newly launched products in the U.S. and EU markets were lead-free, with increasing uptake across South America and parts of Southeast Asia. These formulations are now being designed with advanced compounds like MMT (methylcyclopentadienyl manganese tricarbonyl) alternatives and oxygenates that enhance fuel performance without violating emission standards. This shift is encouraging long-term investments in clean fuel additive R&D.

Growth in High-Performance Racing Applications: The motorsports and racing sectors are seeing a spike in the use of specialized octane boosters engineered for high-compression engines. According to industry reports, sales of race-grade boosters rose by over 30% between 2022 and 2024 in markets such as Germany, the UK, Japan, and the U.S. Racing teams and vehicle modifiers prefer these boosters for their ability to prevent pre-ignition and enhance combustion stability under extreme conditions.

Expansion of E-Commerce Fuel Additive Sales: Online distribution channels are becoming a dominant force in the Octane Boosters Market. In 2024, e-commerce sales accounted for more than 40% of total global sales, especially for consumer-packaged boosters used by car owners. Platforms offering detailed usage tutorials, vehicle compatibility data, and subscription-based delivery models have significantly boosted product accessibility and brand loyalty.

Introduction of Smart Dispenser Technologies: Smart dispenser systems integrated into fueling stations and fleet depots are enabling real-time dosage management of octane boosters. These systems, which saw a 20% increase in installations across North America in 2024, allow fuel operators to mix boosters based on engine type, fuel grade, and environmental conditions. The technology also supports consumption analytics and regulatory compliance through digital logs, contributing to more precise additive usage and reduced wastage.

The Octane Boosters Market is segmented into distinct categories based on product types, application areas, and end-user sectors. Each segment demonstrates specific growth dynamics shaped by evolving fuel technologies, vehicle types, and environmental regulations. Product-wise, the market includes alcohol-based boosters, aromatic hydrocarbons, oxygenates, metallic additives, and others, each serving unique fuel optimization needs. Application areas range from private vehicle usage to aviation and motorsports, with varying performance criteria influencing booster preferences. End-user insights reveal a strong presence in automotive aftermarket services, fuel distributors, and industrial fleet operators. These segments are evolving as businesses seek performance efficiency, regulatory compliance, and compatibility with next-gen fuels. Understanding these subdivisions is essential for industry professionals aiming to align with market demands and expand their footprint.

Alcohol-based octane boosters represent the leading type in the market, widely adopted due to their compatibility with ethanol-blended fuels and eco-friendliness. These boosters, particularly those formulated with isopropyl or methanol bases, are favored in regions with high biofuel adoption, such as Brazil and the United States. They are easy to blend and reduce knocking in a variety of engines. The fastest-growing segment is oxygenate-based boosters. These compounds, including MTBE (methyl tert-butyl ether) and ETBE (ethyl tert-butyl ether), are gaining momentum due to their high oxygen content, enhancing combustion efficiency and lowering particulate emissions. Emerging markets in Asia-Pacific are seeing a rapid uptick in demand due to stricter emission norms and increasing vehicle density. Other types such as aromatic hydrocarbons and metallic additives hold niche roles. Aromatics are still utilized in performance tuning circles, while metallic additives like ferrocene serve legacy vehicles and specific industrial engines. However, regulatory limitations are narrowing their usage in mainstream applications.

Passenger vehicles remain the dominant application segment in the Octane Boosters Market. Car owners across North America and Europe, in particular, frequently use octane boosters to improve engine efficiency, extend fuel mileage, and minimize knocking. The increased availability of boosters through retail and online platforms further supports this trend. The motorsport and racing application is the fastest-growing segment. The demand for boosters that can support high compression ratios and deliver consistent power output has seen a significant rise in countries such as Germany, Japan, and the U.S. Innovation in combustion science and racing-grade fuel blends is fueling this growth. Other application areas include aviation and marine engines. Aviation-grade boosters are used in light aircraft to ensure smooth engine operation at variable altitudes, while the marine sector utilizes boosters in high-output diesel and gasoline engines. Though smaller in market size, these applications require high-reliability formulations, making them attractive for premium offerings.

The automotive aftermarket is the leading end-user segment in the Octane Boosters Market. Car service centers, tuning garages, and individual vehicle owners account for a substantial portion of the demand. With increasing awareness about fuel efficiency and emissions, consumers are incorporating boosters into regular engine care routines. The fastest-growing end-user segment is fleet operators and fuel distributors. Logistics firms and commercial vehicle operators are turning to octane boosters to improve fleet performance, reduce maintenance costs, and ensure compliance with local fuel quality standards. Fleet-scale adoption is also driven by the integration of AI systems that monitor fuel performance and recommend additive usage accordingly. Other contributors include performance enthusiasts and racing teams that require custom booster formulations, and industrial users operating high-performance machinery. These users demand consistency, reliability, and compatibility with specialized fuel systems, which is driving innovation in packaging, formulation, and distribution models.

North America accounted for the largest market share at 34.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

The high adoption of high-performance vehicles, strict emission regulations, and a well-developed automotive aftermarket have made North America the dominant region. Key manufacturing hubs in the U.S. are also pushing technological innovations in octane booster formulations. Meanwhile, Asia-Pacific is witnessing rapid expansion due to a surge in automobile sales, increasing fuel quality standards, and infrastructure development in nations such as China, India, and Indonesia. Growing fuel blending requirements and increasing motorsports activity in Asia are fueling regional demand for specialized octane boosters. These regional trends are reshaping the global Octane Boosters Market, creating a competitive but opportunity-rich environment across developing and developed economies.

Aftermarket Expansion Drives Additive Uptake in Performance-Focused Engines

North America held a market share of 34.2% in 2024 in the Octane Boosters Market, driven primarily by high penetration of premium and high-compression vehicles. The automotive aftermarket in the U.S. and Canada continues to dominate demand, particularly among performance enthusiasts and commercial fleet operators. Government initiatives promoting cleaner fuels have led to wider availability of ethanol-blended fuels, pushing the need for ethanol-compatible boosters. The Environmental Protection Agency (EPA) has also tightened standards around knock-reducing fuel additives, fostering a surge in eco-safe innovations. Technological advancements include AI-assisted dosing systems and cloud-integrated diagnostics in service stations, which are enhancing additive precision and vehicle compatibility across the region.

Innovation-Driven Growth Aligned with Sustainability Initiatives

Europe accounted for 27.8% of the Octane Boosters Market in 2024, with Germany, the UK, and France being the largest consumers. The shift toward carbon neutrality and cleaner fuels is reshaping booster demand across the continent. The European Chemicals Agency (ECHA) has enforced stricter norms around metallic additives, driving R&D into bio-derived alternatives. Germany, in particular, is investing heavily in e-fuel research, indirectly supporting octane booster development for synthetic blends. Emerging technologies like AI-powered fuel testing and smart dispensers are gaining traction in Scandinavian countries. Furthermore, the European Union’s Fit for 55 initiative is encouraging the use of additives that align with fuel economy and emission targets, leading to the development of cleaner, high-efficiency formulations.

Fuel Innovation and Infrastructure Growth Stimulate Consumption Surge

Asia-Pacific ranked as the fastest-growing region and recorded 22.5% of total global volume consumption in 2024 in the Octane Boosters Market. China, India, and Japan are leading demand due to their expanding vehicle fleets, rising disposable incomes, and government-backed fuel quality initiatives. The rapid modernization of fuel infrastructure—especially in India and Indonesia—is enabling wider distribution and use of advanced additives. Additionally, China’s leadership in electric and hybrid vehicles is prompting hybrid-specific fuel additive development, including AI-optimized booster compatibility testing. Innovation hubs in Japan and South Korea are pioneering compact, precision-based booster delivery systems for high-performance engines, pushing technological frontiers in fuel efficiency and customization.

Energy Reforms and Transport Expansion Drive New Market Entrants

In 2024, South America accounted for approximately 7.6% of the Octane Boosters Market, with Brazil and Argentina serving as the primary drivers. Brazil’s ethanol-rich fuel matrix has significantly boosted demand for ethanol-compatible octane boosters. Government incentives for renewable fuels and updated transport regulations are fostering the use of advanced additives across both passenger and freight vehicles. Argentina, too, has increased its focus on improving fuel quality standards, aligning with infrastructure upgrades. The region is witnessing the integration of smart fuel blending at refineries, while domestic and international players are investing in scalable production facilities to cater to emerging demand in the Southern Cone.

Technological Uptake in Fleet Services and Energy-Heavy Industries

The Middle East & Africa captured 8.0% of the Octane Boosters Market in 2024, driven by commercial demand across the oil & gas, logistics, and construction sectors. The UAE and South Africa stand out as key adopters of fuel additives due to their expanding urban transport networks and industrial machinery reliance. The increasing demand for cleaner fuels in GCC nations has triggered a transition to more advanced, environmentally compliant octane boosters. Smart fleet management systems in the UAE are incorporating automated booster injection technologies to enhance fuel efficiency and engine life. Meanwhile, regional trade alliances and regulatory harmonization with global standards are supporting cross-border octane booster trade and application.

United States – 31.7% market share

High vehicle ownership, advanced aftermarket services, and widespread use of high-compression engines sustain demand in the U.S. Octane Boosters Market.

China – 18.4% market share

Massive fuel consumption and expanding automotive infrastructure fuel China’s leadership in regional Octane Boosters Market adoption.

The Octane Boosters market features a moderately fragmented competitive environment with over 45 active manufacturers and suppliers operating globally. These players range from multinational fuel additive companies to regional performance chemical firms focusing on niche vehicle segments. Competitive intensity is rising due to product differentiation strategies, particularly in terms of formulation innovation and compatibility with ethanol-blended or synthetic fuels.

Several companies are investing in proprietary additive technologies that enhance fuel efficiency while meeting tightening environmental regulations. Strategic partnerships between additive developers and automotive OEMs are becoming more frequent, with collaborations focusing on engine-specific performance enhancers. Over the past two years, the market has witnessed a steady stream of new product launches, especially in North America and Europe, targeting high-octane premium vehicle segments. Additionally, mergers and acquisitions are playing a significant role in consolidating smaller players into larger, more diversified portfolios. Companies are also emphasizing eco-compliant and AI-integrated dosing systems, which not only add value but also provide a competitive edge through technological superiority. Digital transformation of distribution channels, including e-commerce-enabled B2B platforms, has further reshaped the competitive landscape by reducing entry barriers for emerging brands.

Lucas Oil Products, Inc.

Boostane LLC

Royal Purple Synthetic Oil (Calumet Specialty Products Partners)

Lennox Lubricants

Petrolift Octane Technologies

Klotz Synthetic Lubricants

VP Racing Fuels, Inc.

Gold Eagle Co.

Torco International Corporation

Würth Group

Technological advancements are playing a critical role in shaping the Octane Boosters market, with innovations spanning formulation chemistry, AI-enabled dosing, and smart integration into fuel systems. One of the key technological shifts is the development of metal-free octane booster compounds that are compatible with modern emission control systems. These newer formulations help reduce engine knocking without increasing harmful metal residue in exhaust gases, aligning with evolving global environmental standards. AI-integrated additive dispensers are gaining traction, especially at high-end service stations in North America and Europe. These systems automatically calibrate the amount of booster injected based on vehicle type, fuel type, and environmental conditions. This not only ensures optimal combustion performance but also improves engine longevity and reduces emissions.

Another prominent advancement is the use of nanotechnology in booster formulations. Nano-emulsified blends enhance solubility and deliver more efficient anti-knock performance, particularly in high-compression and turbocharged engines. Countries such as Japan and Germany are leading in testing nano-enhanced additives for high-octane applications. Digital traceability and blockchain-based inventory systems are being adopted by leading manufacturers to monitor distribution, reduce counterfeiting, and ensure regulatory compliance across international markets. These smart logistics solutions allow precise tracking of booster quality from production to end-use, offering operational transparency and minimizing safety risks.

• In March 2024, Lucas Oil launched a reformulated octane booster designed for turbocharged engines, featuring improved ethanol compatibility and metal-free anti-knock agents. Initial market tests showed a 14% improvement in engine efficiency when used with E10 and E15 fuel blends.

• In August 2024, VP Racing Fuels announced the expansion of its production facility in Texas to include a new R&D lab focused on AI-based fuel additive solutions. The facility aims to reduce development time for custom octane boosters by 40% using simulation models.

• In November 2023, Boostane LLC introduced its latest booster variant designed for high-performance marine engines. The product is engineered to prevent pre-ignition at high RPMs and supports a wider range of compression ratios than its predecessors.

• In May 2023, Royal Purple partnered with a European motorsport association to field-test their new racing-grade octane booster. The results demonstrated enhanced knock resistance and up to a 9% increase in fuel burn efficiency under extreme racing conditions.

The Octane Boosters Market Report offers an in-depth evaluation of the global landscape, examining a wide range of product types, end-user sectors, and application areas. It focuses on key industry domains including automotive, motorsports, marine, and off-road vehicles, each demonstrating unique performance requirements and additive demands. The report evaluates conventional metal-based and advanced metal-free formulations, along with bio-compatible and ethanol-blend-compatible boosters that meet modern engine specifications. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with individual insights into leading and fast-emerging countries such as the United States, Germany, China, India, Brazil, and the UAE. Each region is assessed based on its consumption patterns, regulatory environment, and industrial infrastructure that influence octane booster adoption.

The report further investigates technological developments including AI-powered additive calibration systems, nanotechnology-infused formulations, and blockchain-enabled traceability solutions. These innovations are analyzed in terms of their impact on product performance, environmental compliance, and manufacturing efficiency. In terms of segmentation, the study explores demand by product type (e.g., gasoline-based, alcohol-based, organometallic, nano-formulated), by application (e.g., passenger vehicles, performance vehicles, industrial engines), and by end-user (e.g., automotive consumers, fuel distributors, racing teams, fleet operators). The analysis also includes emerging niche applications such as UAVs and hybrid engines, offering a forward-looking perspective for investors and strategic planners.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 173.94 Million |

|

Market Revenue in 2032 |

USD 277.24 Million |

|

CAGR (2025 - 2032) |

6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Red Hat Inc., VMware Inc., Canonical Ltd., SUSE LLC, Rancher Labs, Mirantis Inc., Platform9 Systems, Weaveworks Inc., D2iQ (formerly Mesosphere), Docker Inc., Portworx by Pure Storage, Kubermatic GmbH, Kasten by Veeam, Sysdig Inc., Loft Labs Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |