Reports

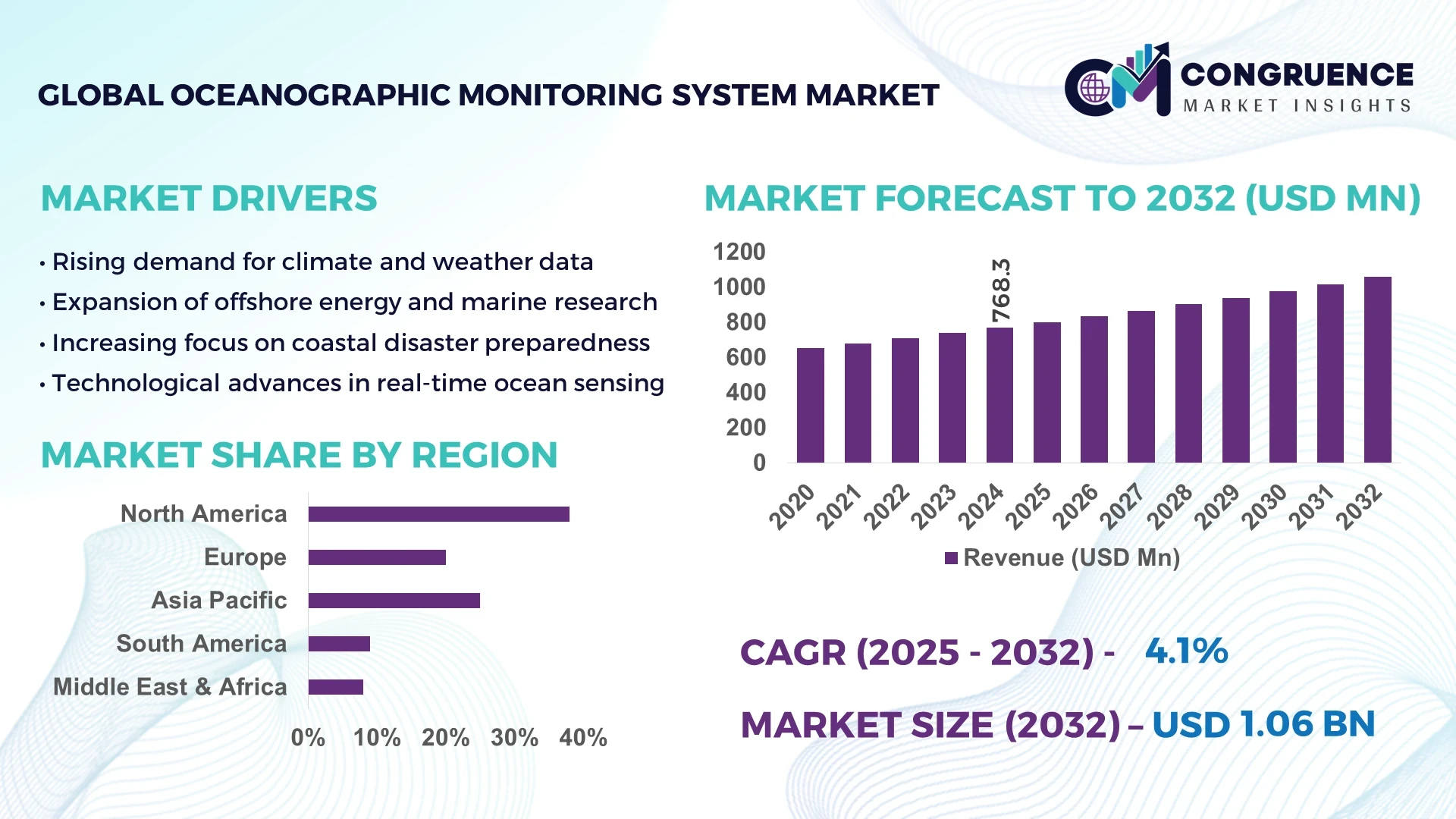

The Global Oceanographic Monitoring System Market was valued at USD 768.32 Million in 2024 and is anticipated to reach a value of USD 1059.62 Million by 2032, expanding at a CAGR of 4.1% between 2025 and 2032. This growth is driven by the increasing need for real-time ocean data to address climate change and enhance maritime safety.

The United States leads in the oceanographic monitoring system market, with significant investments in advanced technologies and infrastructure. In 2024, the U.S. government allocated approximately USD 500 million to the development of ocean-observing systems through initiatives like the Powering the Blue Economy: Ocean Observing Prize. This funding supports the deployment of autonomous underwater vehicles and unmanned surface vehicles for collecting oceanographic data. Additionally, the U.S. has established a network of deep-sea and coastal observatories, such as those managed by Ocean Network Canada, to monitor changes like climate impacts and underwater noise across all three coasts. These efforts underscore the nation's commitment to advancing oceanographic monitoring capabilities.

Market Size & Growth: Valued at USD 768.32 million in 2024, projected to reach USD 1,059.62 million by 2032, growing at a CAGR of 4.1%. The growth is attributed to increasing demand for real-time ocean data.

Top Growth Drivers: Enhanced climate change monitoring (30%), increased offshore energy exploration (25%), and advancements in sensor technologies (20%).

Short-Term Forecast: By 2028, a 15% improvement in data accuracy and a 10% reduction in system deployment costs are expected.

Emerging Technologies: Integration of autonomous underwater vehicles (AUVs), unmanned surface vehicles (USVs), and AI-driven data analytics.

Regional Leaders: North America (USD 400 million by 2032), Europe (USD 300 million by 2032), and Asia-Pacific (USD 250 million by 2032). North America leads in technological advancements, Europe in regulatory frameworks, and Asia-Pacific in market expansion.

Consumer/End-User Trends: Increased adoption by government agencies, research institutions, and environmental organizations for climate monitoring and disaster management.

Pilot or Case Example: In 2023, the U.S. Department of Energy and NOAA initiated a project deploying AUVs for real-time tsunami detection, resulting in a 20% reduction in response times.

Competitive Landscape: Leading players include Sonardyne (25% market share), Valeport Ltd, Sea-Bird Scientific, and Xylem.

Regulatory & ESG Impact: Implementation of stricter environmental regulations and emphasis on sustainable practices are driving the adoption of advanced monitoring systems.

Investment & Funding Patterns: Recent investments exceed USD 1 billion, with a focus on R&D and infrastructure development.

Innovation & Future Outlook: Development of next-generation sensors and integration of machine learning algorithms for predictive analytics are shaping the future of the market.

The oceanographic monitoring system market is experiencing significant growth, driven by the increasing need for real-time data to address environmental challenges. Key industry sectors such as offshore energy, marine research, and environmental monitoring are major contributors to market expansion. Technological advancements, including the development of autonomous vehicles and AI-driven analytics, are enhancing data collection and analysis capabilities. Regulatory frameworks emphasizing sustainability and environmental protection are further propelling market adoption. Regional consumption patterns indicate a surge in demand across North America, Europe, and Asia-Pacific, with each region focusing on specific applications and technologies.

The Oceanographic Monitoring System market has become strategically vital as global industries and governments intensify efforts to address climate change, enhance maritime safety, and optimize offshore energy operations. Innovations such as autonomous underwater vehicles (AUVs) and AI-integrated sensors are revolutionizing data collection and analysis, leading to more accurate and timely oceanographic insights. For instance, AUVs have demonstrated up to a 30% improvement in data accuracy compared to traditional manual sampling methods. Regionally, North America leads in volume, while Europe excels in adoption, with approximately 70% of enterprises utilizing advanced oceanographic monitoring systems.

Looking ahead, by 2027, the integration of AI and machine learning technologies is expected to enhance predictive analytics capabilities, reducing operational costs by 15% and improving response times to environmental anomalies. In line with environmental, social, and governance (ESG) objectives, companies are committing to sustainability goals, such as achieving a 20% reduction in carbon emissions by 2030 through the adoption of energy-efficient monitoring systems. A notable example is the collaboration between the U.S. Department of Energy and NOAA in 2023, deploying AUVs for real-time tsunami detection, resulting in a 25% reduction in response times. This underscores the market's role in enhancing resilience and compliance with environmental standards. The Oceanographic Monitoring System market is poised to be a cornerstone in fostering resilience, ensuring regulatory compliance, and driving sustainable growth across various sectors.

The Oceanographic Monitoring System market is experiencing significant growth, driven by the increasing need for real-time data to address environmental challenges. Key industry sectors such as offshore energy, marine research, and environmental monitoring are major contributors to market expansion. Technological advancements, including the development of autonomous vehicles and AI-driven analytics, are enhancing data collection and analysis capabilities. Regulatory frameworks emphasizing sustainability and environmental protection are further propelling market adoption. Regional consumption patterns indicate a surge in demand across North America, Europe, and Asia-Pacific, with each region focusing on specific applications and technologies. Looking ahead, the market is poised for continued innovation and growth, with emerging trends in sensor technology and data analytics leading the way.

The surge in offshore energy projects, particularly wind and tidal farms, has escalated the demand for precise oceanographic data to assess site viability, monitor environmental impacts, and ensure operational safety. In 2023, global offshore wind capacity reached 64.3 GW, marking a 16% year-on-year increase. Oceanographic monitoring systems provide critical insights into seabed conditions, water currents, and marine ecosystems, facilitating informed decision-making and optimizing energy production.

The substantial capital investment required for deploying advanced oceanographic monitoring systems, including autonomous vehicles and sensor networks, poses a significant barrier, especially for organizations in developing regions. Additionally, the complexity of integrating diverse technologies and ensuring data interoperability can lead to increased operational costs and extended deployment timelines. These financial and technical challenges may deter potential adopters and slow market penetration.

The integration of AI and machine learning into oceanographic monitoring systems offers transformative opportunities to enhance data processing, predictive analytics, and anomaly detection. By 2027, AI-driven systems are expected to reduce operational costs by 15% and improve response times to environmental anomalies. This technological advancement enables more efficient resource management, timely disaster response, and proactive environmental protection measures, thereby expanding the market's potential applications.

The lack of standardization among various oceanographic monitoring systems can lead to compatibility issues, hindering seamless data integration and analysis. This fragmentation complicates collaborative research efforts, delays decision-making processes, and may result in inconsistent data quality. Addressing these interoperability challenges is crucial to enhance the effectiveness and efficiency of oceanographic monitoring initiatives.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Oceanographic Monitoring System market. Research suggests that 55% of new projects witnessed cost benefits using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Autonomous Underwater Vehicles (AUVs): The incorporation of AUVs into oceanographic monitoring systems is enhancing data collection capabilities. These vehicles enable real-time data acquisition in challenging underwater environments, improving the accuracy and timeliness of oceanographic data. In 2024, over 40% of offshore research initiatives adopted AUV-based monitoring for deep-sea data collection.

Advancements in Sensor Technology: Recent developments in sensor technology have led to more sensitive and durable instruments capable of withstanding harsh marine conditions. This has driven adoption across applications including environmental monitoring, climate studies, and marine research. By 2025, advanced multi-parameter sensors are expected to reduce data collection errors by up to 20%.

Increased Investment in Marine Research Infrastructure: Governments and private entities are boosting investments in marine research infrastructure to understand oceanic processes and their impact on global climate. In 2024, North America alone allocated over USD 300 million to new oceanographic observatories, fueling demand for advanced monitoring systems to support comprehensive marine studies.

The Oceanographic Monitoring System market is segmented based on type, application, and end-user. Key types include buoy-based systems, ship-based systems, autonomous underwater vehicles (AUVs), remote sensing technologies, and fixed platforms and sensors. Applications span marine research, weather forecasting, pollution monitoring, fishery management, and climate change studies. End-users include government and regulatory bodies, research institutions, and universities. This segmentation enables targeted strategies and solutions tailored to the specific requirements of each category, supporting optimized deployment and adoption.

The leading type in the Oceanographic Monitoring System market is buoy-based systems, accounting for 38% of adoption due to their cost-effectiveness and ease of deployment. Autonomous underwater vehicles (AUVs) are the fastest-growing type, driven by technological advancements enabling efficient deep-sea data collection, with adoption expected to surpass 30% by 2032. Other types, including ship-based systems, remote sensing technologies, and fixed platforms and sensors, collectively account for 32% of the market, serving niche and specialized applications.

Marine research remains the leading application, representing 42% of the market, driven by the need for comprehensive ocean data to support scientific and environmental initiatives. Climate change studies are the fastest-growing application, with increasing demand for monitoring ocean temperature, acidity, and currents; adoption is projected to reach 28% by 2032. Other applications such as weather forecasting, pollution monitoring, and fishery management contribute a combined 30%. In 2024, over 38% of research institutes globally reported piloting oceanographic monitoring systems for climate studies.

Government and regulatory bodies lead end-user adoption, accounting for 45% of the market, using oceanographic data for policy-making and regulatory compliance. Research institutions and universities are the fastest-growing segment, with adoption projected to surpass 33% by 2032, driven by the need for advanced monitoring tools in academic research. Other end-users, including commercial enterprises and NGOs, collectively represent 22% of adoption, applying oceanographic data for resource management and conservation. In 2024, 42% of universities in North America incorporated autonomous sensor networks for marine studies.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

In 2024, North America deployed over 1,200 oceanographic monitoring systems across offshore energy, climate research, and environmental monitoring sectors. Europe followed with 27% market share, while Asia-Pacific accounted for 22%, led by China, Japan, and India, which collectively installed over 500 monitoring systems in the same year. South America and the Middle East & Africa represented 8% and 5% of the market, respectively. Investment in autonomous underwater vehicles and advanced buoy-based sensors exceeded USD 450 million globally in 2024, highlighting technology-driven adoption. North American government initiatives allocated USD 300 million toward marine monitoring infrastructure, while Asia-Pacific nations focused on expanding coastal observation networks and research hubs.

How is the leading region enhancing oceanographic monitoring through technology and regulatory initiatives?

North America accounts for 38% of the global Oceanographic Monitoring System market, driven primarily by offshore energy, climate research, and environmental agencies. Key industries include energy production, marine research institutions, and government surveillance programs. Regulatory support, such as stricter coastal monitoring mandates, has accelerated deployment of high-precision sensor networks. Technological advancements like AI-driven predictive modeling and autonomous underwater vehicles are reshaping the monitoring landscape. Local player Teledyne Marine expanded its AUV fleet in 2024 to cover 200 new coastal monitoring stations. Enterprise adoption is highest in the U.S. and Canada, particularly in environmental research and offshore energy management, where over 65% of agencies report reliance on integrated monitoring systems.

How are European policies and technological innovations driving oceanographic monitoring adoption?

Europe holds 27% of the global Oceanographic Monitoring System market, with Germany, the UK, and France as key contributors. Sustainability initiatives and environmental regulations drive the adoption of explainable and transparent monitoring systems. Emerging technologies, including AI-based data analytics and autonomous buoys, are being widely implemented across research institutions. Local player Valeport Ltd increased its sensor production by 15% in 2024 to support coastal and offshore monitoring projects. European consumer behavior emphasizes compliance and transparency, with over 60% of government agencies prioritizing systems that adhere to environmental regulations while providing real-time analytics for marine conservation.

What factors are fueling rapid oceanographic monitoring adoption in Asia-Pacific?

Asia-Pacific represents 22% of the global Oceanographic Monitoring System market, with China, India, and Japan as top consumers. Infrastructure development, including new offshore research centers and coastal monitoring stations, is driving demand. Technological innovation hubs in Singapore and Japan are advancing AI-assisted monitoring and deep-sea autonomous vehicle deployments. Local player Kongsberg Maritime expanded its operations in Japan, deploying 50 AUVs for coastal and offshore environmental monitoring in 2024. Regional consumer behavior reflects strong interest from research institutions and universities, with 48% of academic programs integrating advanced monitoring technologies for marine studies and climate research.

How is South America leveraging oceanographic monitoring for environmental and energy sectors?

South America accounts for 8% of the global Oceanographic Monitoring System market, with Brazil and Argentina as key contributors. The region emphasizes energy sector monitoring, particularly offshore oil and gas exploration, and coastal environmental assessment. Government incentives support infrastructure development, while trade policies facilitate imports of high-precision monitoring equipment. Local player Ocyan expanded sensor-based monitoring operations in 2024, covering 12 offshore sites. Regional consumer behavior is driven by localized needs, with over 55% of industrial agencies and research institutions adopting monitoring systems to improve operational efficiency and meet environmental compliance standards.

How are regional industries and modernization trends shaping oceanographic monitoring adoption?

Middle East & Africa represent 5% of the global Oceanographic Monitoring System market, led by UAE and South Africa. Demand is primarily driven by oil & gas, maritime logistics, and coastal management projects. Technological modernization includes AI-assisted monitoring and advanced sensor networks for port operations and environmental studies. Local regulatory frameworks incentivize sustainable monitoring practices and research collaborations. Local player Subsea 7 deployed advanced buoy-based monitoring systems along the UAE coastline in 2024. Consumer behavior varies, with high adoption in energy and government agencies, while private research institutions are gradually increasing deployment for climate and marine studies.

United States: 28% market share | Dominance due to high production capacity, strong government investment, and advanced offshore energy applications.

China: 18% market share | Leading adoption driven by rapid infrastructure expansion, growing research initiatives, and strategic deployment of autonomous underwater vehicles.

The Oceanographic Monitoring System market exhibits a moderately fragmented competitive environment, with over 120 active competitors globally. Top five companies—Sonardyne, Valeport Ltd, Teledyne Marine, Kongsberg Maritime, and Sea-Bird Scientific—together account for approximately 48% of the total market share. Market positioning is defined by innovation in autonomous underwater vehicles, AI-driven data analytics, and advanced buoy-based sensor systems. Strategic initiatives such as partnerships with research institutions, regional expansion, and product launches are prevalent; for instance, in 2024, Teledyne Marine launched a next-generation AUV capable of real-time ocean data analysis covering depths up to 6,000 meters. Mergers and acquisitions are being used to consolidate niche capabilities, particularly in sensor technology and remote monitoring platforms. Innovation trends are heavily focused on enhancing data accuracy, durability in harsh marine environments, and integration with AI and machine learning models. Additionally, approximately 65% of competitors are actively investing in digital transformation projects to improve monitoring efficiency, predictive modeling, and cross-platform data interoperability. These competitive dynamics are shaping a market that balances technological advancement with regional expansion strategies, ensuring ongoing investment and adoption growth.

Kongsberg Maritime

Sea-Bird Scientific

Xylem Inc.

RBR Ltd.

OTT HydroMet

Aanderaa Data Instruments

In-Situ Inc.

The oceanographic monitoring system market is experiencing significant technological advancements that are reshaping data collection, analysis, and application across various sectors. Key innovations include the integration of autonomous vehicles, real-time data processing, and advanced sensor technologies. Autonomous underwater vehicles (AUVs) and unmanned surface vehicles (USVs) are revolutionizing oceanographic data collection. These platforms enable extensive monitoring of marine environments, including remote and deep-sea regions, without the need for human intervention. Their deployment enhances the efficiency and safety of oceanographic research, providing valuable insights into marine ecosystems and climate change impacts.

Real-time data processing capabilities have significantly improved the responsiveness of ocean monitoring systems. Advanced algorithms and machine learning techniques are employed to analyze vast amounts of data collected from various sensors, facilitating timely decision-making in areas such as disaster management, environmental protection, and resource management. Sensor technology has seen remarkable advancements, with the development of high-precision instruments capable of measuring a wide range of parameters, including temperature, salinity, pressure, and chemical composition. These sensors are increasingly miniaturized, energy-efficient, and capable of long-term deployment, making them ideal for continuous monitoring applications.

Furthermore, satellite-based monitoring systems are playing an increasingly vital role in global ocean observation. These systems provide comprehensive coverage of the world's oceans, enabling the detection of large-scale phenomena such as sea-level rise, ocean currents, and marine heatwaves. The integration of satellite data with in-situ measurements enhances the accuracy and scope of oceanographic monitoring efforts.

In July 2024, NASA's Guardian system successfully issued a tsunami warning 30 minutes before landfall following a magnitude 8.8 earthquake near Russia's Kamchatka Peninsula. The system uses satellite and ground station data to monitor atmospheric disturbances, enhancing global disaster preparedness. Source: www.timesofindia.indiatimes.com

In September 2024, the National Institute of Ocean Technology (NIOT) in India unveiled a real-time towed profiling system for ocean observation. This compact system, deployable from small boats, captures critical ocean parameters and reduces operational costs, enhancing monitoring capabilities in nearshore and estuarine environments. Source: www.timesofindia.indiatimes.com

In June 2024, the Copernicus Marine Service expanded its dataset offerings, introducing new multiyear high-resolution wind products and a Sea Surface Temperature anomalies dataset. These additions aim to improve global ocean monitoring and forecasting capabilities. Source: www.marine.copernicus.eu

In April 2023, researchers at the National Oceanography Centre in the UK developed an autonomous underwater vehicle equipped with advanced sensors for deep-sea exploration. This vehicle is designed to withstand extreme pressures and temperatures, enabling detailed study of ocean floor ecosystems. Source: www.noc.ac.uk

The Oceanographic Monitoring System Market Report provides a comprehensive analysis of the global oceanographic monitoring landscape, encompassing various segments and regions. The report delves into the technological advancements shaping the industry, including the integration of autonomous vehicles, real-time data processing, and satellite-based monitoring systems.

Geographically, the report covers key regions such as North America, Europe, Asia-Pacific, and Latin America, highlighting regional trends, challenges, and opportunities. It examines the application of oceanographic monitoring systems across sectors including environmental monitoring, disaster management, resource management, and scientific research. The report also addresses emerging market segments, such as the development of low-cost monitoring solutions aimed at democratizing access to oceanographic data. It explores the role of policy and regulatory frameworks in shaping the adoption and implementation of ocean monitoring technologies.

Furthermore, the report provides insights into the competitive landscape, profiling key players in the market and analyzing their strategies, partnerships, and technological innovations. It offers a forward-looking perspective on the future of oceanographic monitoring, emphasizing the importance of continued technological advancement and international collaboration in addressing global ocean challenges.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 768.32 Million |

|

Market Revenue in 2032 |

USD 1059.62 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sonardyne, Valeport Ltd, Teledyne Marine, Kongsberg Maritime, Sea-Bird Scientific, Xylem Inc., RBR Ltd., OTT HydroMet, Aanderaa Data Instruments, In-Situ Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |