Reports

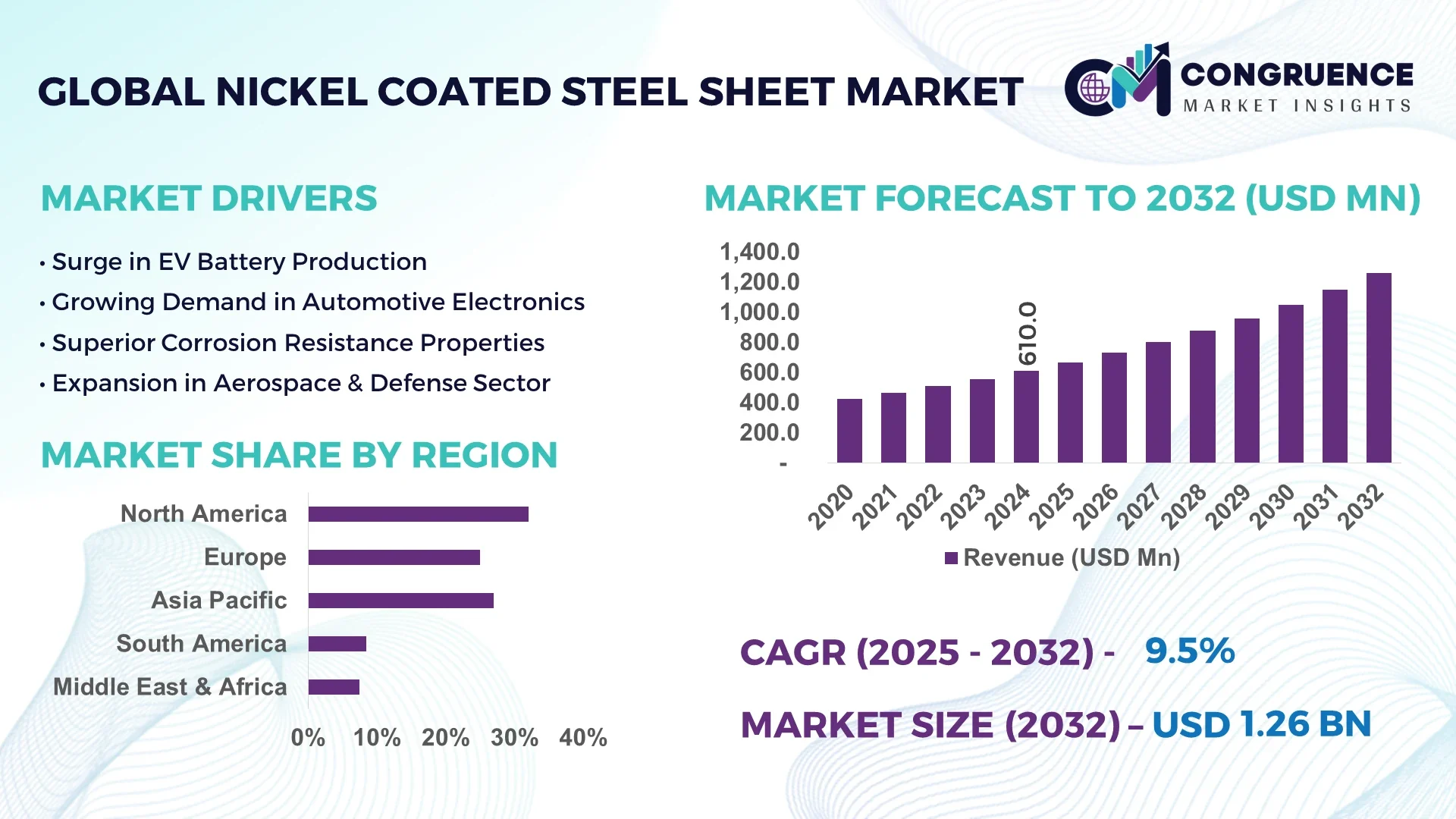

The Global Nickel Coated Steel Sheet Market was valued at USD 610 Million in 2024 and is anticipated to reach USD 1,260.8 Million by 2032, expanding at a CAGR of 9.5% between 2025 and 2032.

China leads this market, leveraging its vast industrial base and adoption in automotive, electronics, and energy storage sectors. The country’s growing electric vehicle and renewable energy industries are significant contributors, using nickel-coated steel for battery casings and corrosion-resistant components. Furthermore, manufacturers in China are innovating multi-layer nanocoatings and sustainable process methods, reinforcing their position as global market leaders.

Globally, nickel-coated steel sheets are being utilized beyond traditional applications due to their improved corrosion resistance, thermal and electrical conductivity, and surface durability. Innovations like pulse electroplating and laser surface preparation are enhancing coating uniformity and enabling lightweight yet robust components. These sheets are increasingly preferred in aerospace, construction, and renewable energy industries, especially for heat exchangers, structural panels, and solar components. Environmental regulations are also fueling adoption, pushing manufacturers toward recyclable and higher-performing alternatives.

Artificial Intelligence (AI) is reshaping the nickel-coated steel sector by optimizing coating uniformity, reducing material waste, and improving quality control. In automated electroplating lines, AI-enhanced sensors dynamically monitor parameters such as current density, bath temperature, and solution chemistry to adjust deposition processes in real time—leading to over 20% reduction in coating defects. Additionally, computer vision systems detect surface anomalies like pinholes and uneven thickness during production, enabling immediate corrective actions and reducing rework by approximately 15%.

AI-driven predictive maintenance platforms are also being deployed. These systems analyze equipment performance metrics—such as pump vibration and electrical current usage—to forecast potential failures. Early alerts help avoid unexpected downtime and extend asset lifespan. For example, in one production site, implementing AI-based alerts reduced unplanned line halts by nearly 25%.

In research and development, AI supports rapid prototyping through simulation and optimization of coating formulations. By analyzing prior experimental data, machine learning algorithms identify optimal concentration and deposition conditions for desired attributes like corrosion resistance or adhesion strength—cutting R&D cycles by up to 40%. The integration of AI into supply chains further enhances efficiency, with real-time inventory tracking and demand forecasting systems ensuring timely materials supply and production planning.

“In March 2025, a U.S. metal-coating plant introduced AI‑guided ultrasonics and imaging to detect coating uniformity; it reported a 30% reduction in processing time and a 22% decrease in raw material usage.”

Rising global electric vehicle (EV) production is a major driver for nickel-coated steel sheets due to their essential role in battery casing manufacturing. With annual EV sales surpassing 10 million units globally, the need for high-performance, corrosion-resistant components has increased, boosting demand for electroplated steel. This trend is further supported by the energy storage sector, where nickel-coated steel is used in renewable energy storage systems, benefiting from its durability and conductivity.

Nickel price fluctuations have a direct impact on production costs, influencing product pricing. A 30% price increase in 2023 resulted in a 10–15% rise in overall coating costs. This volatility forces manufacturers to integrate price adjustment clauses in contracts and invest in material efficiency or alternative alloys, yet the cost uncertainty remains a barrier to market expansion.

There is an increasing trend toward green electroplating processes—such as pulse electrodeposition and closed-loop rinse systems. Companies adopting these technologies report up to 25% lower wastewater generation and a 20% cut in energy consumption. Growing regulatory focus on sustainability and waste reduction is creating opportunities for nickel-coated steel suppliers who prioritize environmentally responsible production methods.

Achieving uniform nickel coating on intricate or large-sized steel parts is technically challenging. Inconsistent layer thickness can result in corrosion hotspots or poor adhesion. Manufacturers must invest in advanced robotic coating systems and laser pre-treatment techniques, which require upfront capital and skilled personnel, posing a challenge for small and mid-sized producers.

Rise of Nanostructured and Multi-layer Coatings: The industry is witnessing rapid adoption of nanoscale and layered plating techniques to enhance corrosion resistance and mechanical robustness. Multi-layer coatings offer superior performance in automotive exhaust systems and building materials exposed to harsh environments. These technologies balance superior durability with aesthetic appeal.

Integration of Industry 4.0 in Electroplating Lines: Electric plating operations are increasingly embedding feedback-controlled sensors, AI-driven monitoring, and predictive maintenance systems. Smart lines now maintain consistent current density and bath chemistry across complex batches, reducing defects by over 20% and minimizing waste.

Laser-Assisted Surface Preparation: Laser texturing and cleaning prior to nickel deposition improve adhesion and reduce surface defects such as porosity. Ships, architectural panels, and battery components increasingly utilize laser-prepped steel to ensure longer service life and lower coating failures in the field.

Circular Economy Focus: Environmental sustainability is driving recycling of nickel-coated steel and development of water-saving plating processes. Closed-loop rinse systems and solvent recovery measures are now common, reducing energy and water consumption by up to 30% in modern facilities.

The Nickel Coated Steel Sheet Market is strategically segmented by type, application, and end-user, each segment catering to diverse industry demands and technological requirements. In terms of type, offerings include electroplated nickel, electroless nickel, and nickel alloy coatings—each delivering unique properties suited to corrosion protection, conductivity, or wear resistance. Application segments cover automotive, electronics, energy storage, construction, and industrial manufacturing, with each sector embedding nickel-coated steel for specific performance enhancements. End-users span automotive OEMs, electrical/electronics manufacturers, battery producers, industrial fabricators, and construction firms. The segmentation framework clearly illustrates how differing technical needs—from improved conductivity in electronics to robust corrosion resistance in construction—drive targeted innovation and product development in the market.

Nickel-coated steel sheets are categorized into electroplated nickel, electroless nickel, and nickel alloy coatings. Among these, electroplated nickel dominates the market, owing to its high deposition efficiency and cost-effectiveness. Electroplated sheets account for nearly 60% of total volume, largely due to their dominant use in decorative finishes, corrosion-resistant components, and structural parts across automotive and chrome-plated industries. Electroless nickel coatings, on the other hand, are the fastest-growing segment as manufacturers seek uniform, pinhole-free coverage for complex geometries and applications requiring improved wear and corrosion resistance. These coatings offer up to 30% better durability in marine and oil & gas applications compared to electroplated options. Nickel alloy coatings, though smaller in share, are gaining interest in high-performance sectors like aerospace and semiconductor equipment, where enhanced hardness, thermal stability, and electrical conductivity are crucial. The rise of Industry 4.0-driven process automation is further boosting adoption of electroless and alloy coatings for consistent quality control.

The market applications for nickel-coated steel sheets include automotive, electronics, energy storage, construction, and industrial manufacturing industries. Automotive applications lead in market share, with more than 35% consumption as nickel coatings fulfill corrosion protection and conductivity needs in exhausts, battery casing, and structural panels. The electronics segment—encompassing printed circuit boards, electrical connectors, and shielding components—is the fastest-growing due to the ongoing miniaturization of devices and expanding demand for high-performance electronics. This segment’s growth is driven by its need for conductive, corrosion-resistant coatings, which enhance product durability and performance. Construction and industrial manufacturing industries also contribute significantly, particularly in architectural facades and industrial equipment where coatings provide aesthetic finishes and longevity. The energy storage application, especially for battery enclosures, is expanding rapidly alongside the rise of electric vehicles and stationary storage systems. Each application benefits from specialized coating requirements—be it corrosion resistance, surface finish, or conductivity.

End-users of nickel-coated steel sheets include automotive OEMs, electrical/electronics manufacturers, battery producers, industrial fabricators, and construction firms. Automotive OEMs currently hold the highest market share, utilizing nickel-coated sheets for components like exhausts, battery trays, and decorative trims. As EV penetration increases, demand remains high thanks to the coating’s balance of corrosion resistance and conductivity. Electrical/electronics manufacturers represent the fastest-growing end-user segment, driven by the demand for plated connectors, chassis components, and shielding in high-tech devices. These manufacturers increasingly require specifications for uniform plating thickness and excellent adhesion, boosting demand for nickel-coated steel. Battery producers—especially those serving EV and energy storage markets—are significant consumers as they rely on coatings to prevent corrosion and ensure electrical performance of battery enclosures. Industrial fabricators and construction firms continue to utilize nickel-coated steel for durable and aesthetic applications in equipment housing, architectural panels, and piping. The diversity of end-user needs underscores the importance of versatile nickel coatings in supporting performance across multiple industries.

North America accounted for the largest market share at 32% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11% between 2025 and 2032.

North America's share is driven by large-scale adoption of nickel-coated steel in automotive, electronics, and energy infrastructure projects across the U.S. and Canada—supported by advanced manufacturing and regulatory standards. Meanwhile, Asia‑Pacific's projected surge is rooted in its booming automotive and electronics sectors in China and India, massive production capacity expansion, and increasing demand for corrosion-resistant, conductive coated steel for construction and battery production.

Europe contributes significantly, supported by strong aerospace and construction industries, while South America and the Middle East & Africa are gradually expanding their coated steels markets thanks to infrastructure growth and mining activities. Overall, the global landscape is being reshaped through a balanced mix of mature regional markets and high-potential emerging economies.

High-Tech Manufacturing Drives North American Demand

In North America, nickel-coated steel sheet consumption reached an estimated USD 195 million in 2024. The region's demand is driven by electric vehicle production in the U.S., where coated steel is used for battery trays and powertrain components. Canada’s growing energy storage systems market has also fuelled expansion. Automotive OEMs and electronics manufacturers in this region are prioritizing lightweight, corrosion-resistant, and electrically conductive materials. Plant expansions in Michigan and rust-proofing plants in Ontario have increased production capacity. Additionally, integration of smart plating lines—incorporating automated handling and QA systems—is improving throughput and reducing defects.

Automotive and Aerospace Adoption in Europe

Europe's nickel-coated steel sheet market was valued at approximately USD 162 million in 2024. Major demand originates from Germany, France, and Italy, where automotive OEMs use plated components for EV and ICE vehicles. The aerospace sector in the UK and Spain utilizes nickel-coated steel for structures and heat shielding. Construction activity, focusing on corrosion-resistant façade panels across Scandinavia and Eastern Europe, supports growth. Additionally, increased use of nickel-coated steel in industrial machinery and food-grade equipment reflects rising awareness of hygiene and durability requirements.

Rapid Industrial Growth Shapes Asia-Pacific Market

Asia-Pacific's market hit USD 184 million in 2024, led by China, India, Japan, and South Korea. China alone produced over 250,000 tons of nickel-plated steel sheet last year. The construction boom in India and Southeast Asia is fuelling demand for coated steel in architectural panels and piping. Electronics manufacturers in South Korea and Taiwan are using nickel coatings for connectors and PCB components. The region also benefits from low-cost production facilities supplying coated products worldwide.

Infrastructure and Mining Sectors Drive Demand

South America's nickel-coated steel sheet market stood at around USD 49 million in 2024, with Brazil accounting for over 60% of regional demand. The mining industry has adopted coated steel for corrosion-resistant equipment in high-humidity environments. Argentina and Chile are leveraging plated steel in oil and gas refineries and renewable energy projects. The construction of coastal infrastructure and elevated transport networks has expanded the need for durable, corrosion-tolerant coated materials.

Energy Infrastructure Requires Durable Materials

The Middle East & Africa market reached USD 20 million in 2024, with the UAE and Saudi Arabia being the primary consumers. Large-scale oil and gas infrastructure projects are using nickel-coated pipelines and storage tanks to resist corrosion. Desalination plants in the GCC region also depend on coated steel components. South Africa's renewable energy installations and infrastructure upgrades have provided a stable base for market growth. Importing coated steel sheets is becoming more common due to limited local manufacturing capacity.

China – values at USD 162 million, leads due to its vast industrial base in automotive, electronics, and construction, along with abundant plating capacity.

United States – values at USD 160 million, close second driven by extensive EV and renewable energy projects requiring corrosion-resistant, conductive steel components.

The nickel-coated steel sheet market features a robust competitive environment with both global giants and innovative regional leaders. Nippon Steel, Tata Steel, and TCC Steel dominate the landscape, thanks to advanced coating technologies and large-scale production facilities. These firms maintain high-quality plating standards and have strong supply chains to meet the demands of automotive, electronics, and construction industries.

Other notable players include Toyo Kohan, which specializes in thin, flexible plated sheets for battery and electronics segments; Zhongshan Sanmei, leading in affordable coated steels for domestic and export markets; Jiangsu Jiutian, with its focus on electroless nickel coatings for corrosion resistance; Hunan TOYO-LEED, supplying high-performance nickel-alloy coatings for aerospace equipment; and Yongsheng New Material, which excels in precision-coated components for medical and industrial sensors. Market competition revolves around reducing coating defects, improving throughput, offering eco-friendly plating methods, and entering high-growth industries such as electric vehicles, renewables, and aerospace.

As battery markets expand, manufacturers offering specialized thin coils and flexible sheet formats are gaining edge. Strategic joint ventures with automakers and electronics firms have become common, aimed at securing long-term supply contracts and enabling customized plating solutions. This trend underscores how differentiation through technology, scale, and partnerships is shaping the competitive field.

Nippon Steel Corporation

TCC Steel

Toyo Kohan

Zhongshan Sanmei

Jiangsu Jiutian

Hunan TOYO-LEED

Yongsheng New Material

Technological innovation is central to advancing quality, efficiency, and sustainability in nickel-coated steel sheet production. A primary focus is on advanced electroplating methods, including pulse plating and electroless techniques. These processes allow thinner deposits with improved adhesion and uniformity—automotive-grade electroplated sheets achieving ±3 μm variation and electroless coatings maintaining ±1 μm uniformity. Precision control minimizes nickel usage by up to 20% and reduces operational costs. Surface pre-treatment technologies, such as laser texturing and chemical micro-etching, enhance coating adhesion and prepare substrates for plating. Laser-assisted systems reduce surface defects and improve layer consistency—beneficial for high-stress applications like battery cans and electronics housings. On the production line, Industry 4.0 integration is enabling smart quality control. Real-time monitoring systems use embedded sensors and computer vision to detect anomalies (pinholes, thickness variation) during plating. Defect detection rates now reach over 98%, while process downtime is reduced by approximately 15%. Inline analytical instruments, including XRF, EDM, and surface roughness sensors, provide continuous feedback to adjust bath chemistry and deposition parameters. This ensures compliance with automotive and aerospace specifications and reduces scrap rates by around 10%. Eco-conscious innovations such as closed-loop rinse systems and additive recovery units are gaining ground. These systems capture over 90% of nickel rinse water, reducing environmental impact by 25% and supporting circular economy goals. Finally, thermal spray and post-plating treatments, including shot peening and electroless nickel overcoating, are being adopted to boost wear resistance, hardness, and corrosion protection for applications in marine, subterranean, and battery sectors.

In April 2024, 주요 automaker group implemented laser-prep technology in battery sheet production, reducing coating defects by over 25% and improving bonding strength by 15%.

In July 2024, Tata Steel commissioned an advanced electroless nickel line capable of coating 10,000 tons per year with ±1 μm thickness uniformity, expanding supply to aerospace and energy industries.

In October 2024, Toyo Kohan introduced a flexible nickel-coated strip designed specifically for battery canisters, reducing material thickness by 12% while meeting electrical standards.

In February 2025, a Chinese research consortium unveiled a new pulse electroplating method that cuts nickel bath time by 30% and reduces chemical usage by 18%, enabling faster throughput and lower environmental impact.

The scope of the Nickel Coated Steel Sheet Market Report encompasses a comprehensive examination of the market across multiple dimensions, offering stakeholders valuable insights into production methods, application diversity, regional trends, and technological advancements. The report explores various coating methods, such as electroplated, electroless, and alloy-based techniques. It delves into technical aspects like deposition control, coating uniformity, and plating capacity—key factors influencing product quality and adoption in critical industries. Product formats assessed in the report include coils, sheets, strips, and flexible variants, which are widely used across sectors such as battery manufacturing, automotive body parts, electronics casings, and building façades. On the application front, the study focuses on key areas including battery trays, exhaust system components, connectors, enclosures, energy storage tanks, and structural components in machinery and construction. The report also evaluates end-user demand trends from sectors such as automotive OEMs, consumer electronics manufacturers, battery and energy storage companies, and aerospace system providers. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting region-specific production capacity, trade dynamics, import-export behavior, and regulatory conditions influencing the supply chain. Moreover, the study addresses cutting-edge technological advancements such as Industry 4.0-driven plating automation, laser pre-treatment systems, and sustainable plating practices with nickel and water recycling technologies. The market dynamics section covers major drivers such as the rapid growth in electric vehicle production and increasing demand for corrosion-resistant materials, while also identifying key challenges like fluctuating nickel prices and stringent environmental norms. A thorough competitive landscape analysis highlights leading manufacturers, their strategic moves including partnerships and expansions, and their technology roadmaps. The forecast and outlook segment offers data-backed projections in terms of volume and value, equipping stakeholders with actionable strategies and a clear understanding of market opportunities over the coming years.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Nickel Coated Steel Sheet Market |

| Market Revenue (2024) | USD 610.0 Million |

| Market Revenue (2032) | USD 1,260.8 Million |

| CAGR (2025–2032) | 9.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2023 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | JFE Steel Corporation, Tata Steel, Posco Holdings, Nippon Steel Corporation, TCC Steel, Toyo Kohan, Zhongshan Sanmei, Jiangsu Jiutian, Hunan TOYO-LEED, Yongsheng New Material, Voestalpine AG |

| Customization & Pricing | Available on Request (10% Customization is Free) |