Reports

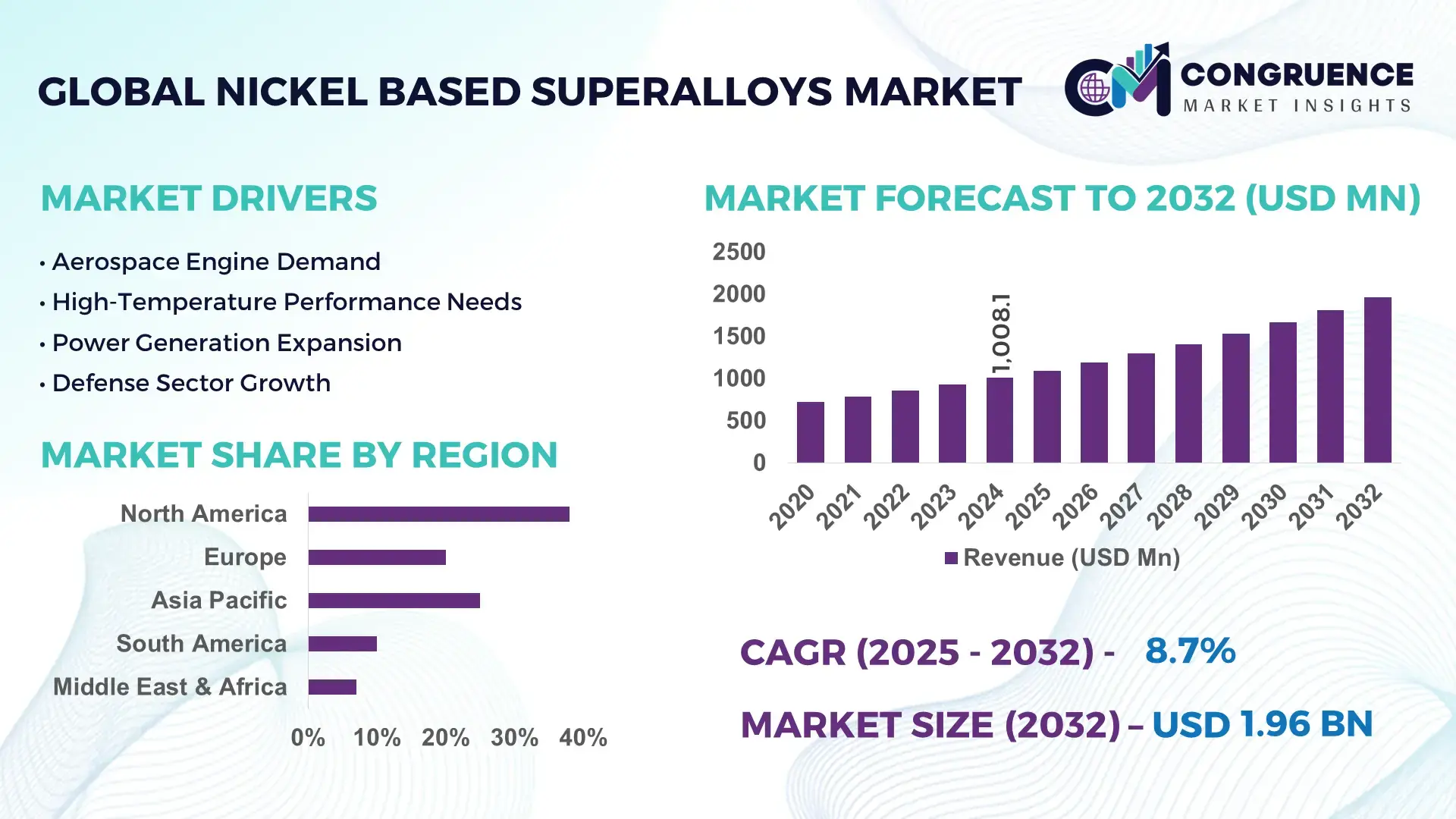

The Global Nickel Based Superalloys Market was valued at USD 1008.11 Million in 2024 and is anticipated to reach a value of USD 1964.92 Million by 2032 expanding at a CAGR of 8.7% between 2025 and 2032. This growth is driven by rising demand for high-temperature, corrosion-resistant materials across aerospace engines, power generation turbines, and advanced industrial manufacturing.

The United States represents the dominant country in the global nickel based superalloys market, supported by its advanced production infrastructure and sustained capital investment. The U.S. hosts more than 35% of the world’s aerospace engine manufacturing capacity, with nickel based superalloys accounting for nearly 55–60% of total material usage in commercial and military jet engines. Annual investment in high-performance alloy R&D exceeds USD 1.8 billion, led by aerospace, defense, and energy OEMs. The country also accounts for over 40% of global additive manufacturing deployments for superalloy components, accelerating innovation in turbine blades, combustion chambers, and space propulsion systems.

Market Size & Growth: Valued at USD 1008.11 Million in 2024, projected to reach USD 1964.92 Million by 2032 at a CAGR of 8.7%, supported by expanding aerospace engine production and next-generation power turbines.

Top Growth Drivers: Aircraft engine demand growth (~38%), efficiency improvement requirements in gas turbines (~27%), and adoption in space and defense propulsion systems (~21%).

Short-Term Forecast: By 2028, advanced alloy processing is expected to reduce component failure rates by approximately 18% while improving thermal efficiency by nearly 12%.

Emerging Technologies: Vacuum induction melting, additive manufacturing of superalloy components, and single-crystal alloy development for ultra-high-temperature applications.

Regional Leaders: North America projected to reach USD 720 Million by 2032 with aerospace-driven adoption; Europe to reach USD 510 Million with energy transition applications; Asia-Pacific to reach USD 480 Million driven by aircraft fleet expansion.

Consumer/End-User Trends: Aerospace OEMs and power utilities increasingly favor long-life alloys to minimize maintenance cycles and lifecycle costs.

Pilot or Case Example: A 2024 aerospace turbine upgrade program achieved a 14% thrust efficiency gain using next-generation nickel based superalloys.

Competitive Landscape: Leading player holds approximately 22% share, followed by four major global manufacturers with strong aerospace and energy portfolios.

Regulatory & ESG Impact: Emissions regulations and fuel efficiency mandates are accelerating adoption of lightweight, high-strength superalloys.

Investment & Funding Patterns: Over USD 4.6 Billion invested globally since 2022 in alloy capacity expansion, additive manufacturing, and recycling technologies.

Innovation & Future Outlook: Integration of AI-driven alloy design and increased recycling of nickel superalloys to enhance sustainability and supply security.

Nickel based superalloys are primarily consumed by the aerospace sector, contributing nearly 48% of total demand, followed by power generation at around 26%, oil and gas at 14%, and industrial manufacturing at 12%. Recent innovations include single-crystal turbine blade alloys, powder metallurgy advancements, and 3D-printed superalloy components that improve fatigue resistance and thermal stability. Regulatory pressure for fuel efficiency and lower emissions, combined with rising electricity demand and aircraft fleet modernization, continues to support market expansion. Asia-Pacific shows accelerating consumption due to new aircraft programs and power infrastructure investments, while North America and Europe focus on performance upgrades and lifecycle optimization. Emerging trends include recyclable superalloy systems, digital material modeling, and increased use in space launch vehicles, positioning the market for sustained long-term growth.

The Nickel Based Superalloys Market holds strategic relevance due to its critical role in enabling high-temperature, high-stress applications across aerospace, power generation, defense, and emerging space technologies. These materials support operating temperatures exceeding 1,000°C while maintaining mechanical strength and corrosion resistance, directly influencing fuel efficiency and asset longevity. From a strategic perspective, additive manufacturing of nickel based superalloys delivers approximately 20–25% material utilization improvement compared to conventional casting standards, while reducing lead times by nearly 30%. Regionally, Asia-Pacific dominates in production volume, supported by expanding turbine and aircraft assembly capacity, while North America leads in adoption with over 45% of aerospace and energy enterprises integrating advanced superalloy components into next-generation systems.

In the near term, digital alloy design and AI-driven process optimization are reshaping competitive pathways. By 2027, AI-enabled alloy modeling is expected to improve component fatigue life by nearly 15% and reduce prototyping cycles by around 25%. ESG considerations are also influencing strategic planning, with manufacturers committing to sustainability targets such as 20–30% recycled nickel content in superalloy feedstock by 2030 to reduce carbon intensity. A measurable micro-scenario highlights that in 2024, the United States achieved a 12% reduction in turbine maintenance downtime through the deployment of additively manufactured nickel based superalloy components in commercial aviation engines. Looking forward, the Nickel Based Superalloys Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable growth, underpinning long-term performance efficiency across mission-critical industries.

The expanding demand for fuel-efficient aircraft engines and high-output gas turbines is a key growth driver for the Nickel Based Superalloys Market. Modern jet engines now incorporate nickel based superalloys in more than 60% of their hot-section components, as these alloys enable higher combustion temperatures and improved thrust-to-weight ratios. In power generation, advanced gas turbines operating above 1,500°C rely heavily on nickel based superalloys to achieve thermal efficiency improvements of 10–15% over older designs. Global aircraft fleet modernization programs and investments in combined-cycle power plants are reinforcing long-term demand, as operators prioritize durability, reduced maintenance intervals, and higher operational reliability.

The Nickel Based Superalloys Market faces restraint from volatility in nickel, cobalt, and chromium prices, which directly impacts production planning and cost stability. Processing superalloys requires energy-intensive steps such as vacuum melting and precision heat treatment, increasing manufacturing complexity. Scrap recovery rates remain below 70% in conventional processes, limiting cost efficiency. Additionally, long qualification cycles in aerospace and defense applications, often exceeding five years, slow the adoption of new alloy compositions. These factors collectively constrain rapid capacity expansion and increase operational risk for manufacturers operating in price-sensitive environments.

Advanced manufacturing technologies present significant opportunities for the Nickel Based Superalloys Market by enabling design flexibility and performance optimization. Additive manufacturing allows internal cooling channels and lightweight geometries that can extend component life by up to 20%. Recycling innovations are improving nickel recovery rates beyond 85%, reducing dependence on primary raw materials. Growing investments in space launch vehicles, hydrogen-powered turbines, and small modular reactors are opening new application areas where superalloys are essential. These developments create opportunities for suppliers to diversify applications while aligning with sustainability and efficiency objectives.

Stringent certification and regulatory requirements pose ongoing challenges for the Nickel Based Superalloys Market, particularly in aerospace and defense sectors. Material qualification involves extensive mechanical testing, fatigue analysis, and long-duration performance validation, often spanning multiple years. Compliance with evolving environmental regulations also requires reformulation of alloys to reduce hazardous elements without compromising performance. Smaller manufacturers face barriers due to high testing costs and limited access to advanced R&D infrastructure. These challenges slow innovation cycles and increase time-to-market for next-generation superalloy solutions.

Rising Adoption of Modular and Prefabricated Industrial Systems: Modular and prefabricated engineering practices are reshaping demand patterns in the Nickel Based Superalloys market, particularly in aerospace engines, gas turbines, and industrial energy systems. Around 55% of newly commissioned turbine and propulsion projects report measurable cost and schedule benefits from modular construction approaches. Pre-cast and pre-machined superalloy components are increasingly fabricated off-site using automated CNC and additive manufacturing systems, reducing on-site assembly time by nearly 30% and lowering labor dependency by approximately 22%. Demand for precision-formed nickel based superalloy modules is notably higher in Europe and North America, where industrial productivity and downtime reduction remain strategic priorities.

Acceleration of Additive Manufacturing for Complex Superalloy Parts: Additive manufacturing continues to gain traction, with over 40% of advanced aerospace component programs now incorporating 3D-printed nickel based superalloy parts. This trend enables intricate cooling geometries and weight reductions of 15–20% compared to conventionally cast components. Scrap material usage has declined by nearly 25%, while design iteration cycles have shortened by approximately 35%. Industrial users increasingly adopt powder-bed fusion and directed energy deposition technologies to improve performance consistency and component customization.

Shift Toward High-Temperature, Long-Life Alloy Grades: End users are prioritizing next-generation nickel based superalloys capable of operating beyond 1,100°C, supporting higher thermal efficiency targets. More than 60% of newly developed turbine platforms now specify advanced single-crystal or directionally solidified alloys. These materials extend service intervals by 18–25% and reduce unplanned maintenance events by nearly 20%, directly improving asset utilization across aerospace and power generation sectors.

Growing Emphasis on Sustainability and Recyclability: Sustainability-driven procurement is influencing material selection, with manufacturers targeting recycled content levels of 20–30% in nickel based superalloy feedstocks. Improved recycling technologies have increased metal recovery rates to above 85%, while lifecycle emissions associated with alloy production have declined by roughly 12–15%. This trend aligns procurement strategies with ESG benchmarks while supporting long-term supply chain resilience and cost stability.

The Nickel Based Superalloys Market is segmented by type, application, and end-user, each reflecting distinct performance requirements and consumption patterns. Type-based segmentation highlights material engineering priorities such as temperature resistance, creep strength, and fatigue life. Application-based segmentation is shaped by operating environments, with aerospace and power generation demanding the highest alloy purity and precision. End-user segmentation reflects procurement behavior across OEMs, utilities, and industrial operators, where lifecycle cost, reliability, and compliance standards drive material selection. Together, these segments reveal how technological intensity, regulatory exposure, and operational criticality influence adoption levels across global industries.

Nickel-chromium-based superalloys represent the leading product type, accounting for approximately 38% of total adoption due to their balanced corrosion resistance and high-temperature strength, making them suitable for turbine blades and combustion components. Nickel-cobalt-based superalloys follow with around 26% adoption, offering superior creep resistance under extreme thermal stress. However, nickel-iron-based superalloys are the fastest-growing type, expanding at an estimated CAGR of 9.4%, driven by their cost-efficiency and rising use in industrial gas turbines and energy infrastructure. Single-crystal and powder metallurgy-based superalloys, while more specialized, collectively contribute nearly 36% of demand, supporting niche applications requiring ultra-high fatigue resistance.

Aerospace applications dominate the Nickel Based Superalloys Market, accounting for approximately 46% of total usage, as modern jet engines and space propulsion systems rely heavily on these alloys for hot-section components. Power generation follows with nearly 29% adoption, driven by gas turbines operating at higher firing temperatures to improve efficiency. Oil and gas, along with chemical processing, collectively represent about 15% of applications, while industrial manufacturing accounts for the remaining 10%. Among these, space and advanced propulsion systems are the fastest-growing application segment, expanding at a CAGR of approximately 10.1%, supported by increased launch activity and reusable engine platforms.

Aerospace OEMs are the leading end-users, contributing roughly 41% of total demand, as they prioritize high-performance materials to meet efficiency and safety benchmarks. Power utilities represent about 28% of end-user adoption, leveraging superalloys to extend turbine maintenance intervals and operational uptime. Defense organizations account for nearly 14%, while oil and gas operators and industrial manufacturers together contribute around 17%. Among these, space and defense contractors are the fastest-growing end-user group, expanding at an estimated CAGR of 9.8%, fueled by increased investment in advanced propulsion and hypersonic systems.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2025 and 2032.

North America’s leadership is supported by high aerospace engine production volumes exceeding 9,000 commercial and defense engines annually, while Europe holds approximately 27% share driven by energy transition and turbine modernization programs. Asia-Pacific represents nearly 24% of global consumption, supported by aircraft fleet expansion, power infrastructure projects exceeding 120 GW of new capacity, and growing space programs. The Middle East & Africa and South America together contribute around 11%, with demand concentrated in oil & gas turbines, industrial processing, and energy diversification projects. Regional differences in regulatory pressure, technology adoption, and industrial investment continue to shape demand intensity and alloy selection patterns across the Nickel Based Superalloys Market.

North America holds an estimated 38% share of the Nickel Based Superalloys Market, driven primarily by aerospace, defense, and power generation industries. The region operates over 45% of the world’s active commercial aircraft fleet, creating sustained demand for turbine blades, combustors, and exhaust components. Government-backed defense modernization programs and energy efficiency mandates support adoption of advanced alloy grades. Digital manufacturing, including additive production and AI-based process control, is used by more than 40% of large manufacturers in the region. A leading U.S.-based alloy producer expanded vacuum melting capacity in 2024 to support next-generation jet engines. Regional consumer behavior reflects higher enterprise adoption in aerospace, defense, and energy utilities, where reliability and lifecycle optimization are prioritized.

Europe accounts for approximately 27% of global demand, with Germany, the UK, and France representing over 65% of regional consumption. The region’s focus on emissions reduction and turbine efficiency has increased demand for high-temperature nickel based superalloys in power generation and aviation. Sustainability frameworks encourage recyclable alloy systems, with recycled content targets reaching 25% in new alloy production. Advanced casting and powder metallurgy techniques are increasingly adopted, particularly in Germany. A major European aerospace supplier reported a 15% improvement in turbine lifespan after transitioning to advanced single-crystal alloys. Consumer behavior reflects strong regulatory pressure, driving demand for compliant, traceable, and performance-certified superalloy materials.

Asia-Pacific ranks as the second-largest and fastest-expanding region, contributing nearly 24% of total volume. China, Japan, and India together account for more than 70% of regional demand, supported by aircraft manufacturing programs, thermal power capacity additions, and expanding space missions. The region hosts over 35% of global gas turbine installations under development. Manufacturing automation and domestic alloy production capacity are rising, with localized supply chains reducing import dependency. A major Japanese materials manufacturer introduced high-fatigue-resistant superalloys for industrial turbines in 2024. Regional consumer behavior reflects growth driven by manufacturing scale, infrastructure expansion, and increasing adoption of advanced industrial technologies.

South America contributes approximately 6% of global demand, led by Brazil and Argentina. Gas-fired power plants, oil refining upgrades, and industrial processing facilities drive regional consumption. Brazil alone accounts for nearly 55% of regional usage, supported by energy infrastructure investments and aerospace component manufacturing. Trade incentives and localized industrial policies encourage regional alloy sourcing. A Brazilian industrial supplier expanded high-temperature alloy machining capacity to serve power and petrochemical sectors. Consumer behavior in the region reflects demand linked to industrial localization, maintenance-intensive operations, and gradual adoption of advanced materials.

The Middle East & Africa region represents around 5% of the Nickel Based Superalloys Market, with demand centered on oil & gas turbines, petrochemical plants, and emerging power projects. The UAE and South Africa collectively contribute over 60% of regional demand. Modernization of gas processing facilities and investments in combined-cycle power plants are increasing alloy usage. Strategic trade partnerships and industrial diversification initiatives support material imports and localized finishing operations. A Middle Eastern energy operator reported a 20% extension in turbine service intervals after upgrading to advanced nickel based superalloys. Consumer behavior emphasizes durability and operational reliability in harsh environments.

United States Nickel Based Superalloys Market – 24% market share

Strong dominance due to high aerospace engine production capacity and sustained defense and energy sector demand.

China Nickel Based Superalloys Market – 18% market share

Leadership supported by large-scale industrial manufacturing, expanding aircraft programs, and power infrastructure investments.

The Nickel Based Superalloys market exhibits a moderately consolidated competitive structure, characterized by a limited group of large multinational producers alongside a wide base of regional and specialty alloy manufacturers. Globally, there are over 35–40 active commercial producers supplying nickel based superalloys for aerospace, power generation, defense, oil & gas, and industrial applications. The top five companies collectively account for approximately 55–60% of total market supply, reflecting strong concentration driven by capital-intensive production processes, long qualification cycles, and stringent performance standards.

Leading players maintain competitive advantage through vertical integration, proprietary alloy formulations, and long-term supply agreements with aerospace OEMs and turbine manufacturers. Strategic initiatives such as capacity expansions, powder metallurgy investments, and additive manufacturing integration are increasingly shaping competition. More than 45% of Tier-1 producers have invested in advanced melting technologies such as vacuum induction melting and electron beam melting to improve alloy purity and yield consistency. Product innovation remains central, with over 30 new high-temperature alloy grades introduced globally between 2022 and 2024, targeting operating temperatures above 1,100°C.

Partnerships between material suppliers and engine OEMs are rising, particularly for next-generation aviation and hydrogen-ready turbines. Mergers and acquisitions remain selective but strategic, focusing on securing raw material access and expanding regional footprints. Overall, competition in the Nickel Based Superalloys market is increasingly defined by technological depth, qualification credibility, and long-term reliability rather than price-based differentiation.

Allegheny Technologies Incorporated (ATI)

Haynes International

Carpenter Technology Corporation

VDM Metals

Precision Castparts Corp.

Special Metals Corporation

Aperam

Doncasters Group

AMG Advanced Metallurgical Group

Thyssenkrupp Materials

Technological advancement remains a critical differentiator in the Nickel Based Superalloys Market, directly influencing material performance, production efficiency, and lifecycle economics. One of the most impactful technologies is additive manufacturing, now adopted in over 40% of advanced aerospace and turbine development programs, enabling complex geometries such as internal cooling channels that improve thermal efficiency by 12–18% and reduce component weight by up to 20%. Powder-bed fusion and directed energy deposition processes are increasingly used for both prototyping and serial production, shortening development cycles by approximately 30–35%.

Advanced melting and refining technologies, including vacuum induction melting (VIM), vacuum arc remelting (VAR), and electron beam melting (EBM), are widely deployed to achieve ultra-low impurity levels below 10 ppm, improving creep resistance and fatigue life. More than 60% of large-scale producers now operate dual or triple-melt systems to ensure consistent alloy quality for safety-critical aerospace and defense applications. Additionally, single-crystal and directionally solidified casting technologies are gaining traction, accounting for nearly 45% of high-temperature turbine blade production, extending component service life by 18–25% under extreme thermal loads.

Digital transformation is also reshaping alloy development. AI-driven alloy design platforms can simulate thousands of compositional variations, reducing physical testing requirements by nearly 25% and accelerating qualification timelines. Process automation and in-line sensor integration are improving yield rates by 10–15%, while predictive maintenance systems reduce unplanned downtime in melting and casting operations by approximately 20%. Sustainability-oriented technologies, including closed-loop recycling systems, are enabling nickel recovery rates exceeding 85%, lowering energy intensity per ton of alloy produced. Collectively, these technologies are redefining competitiveness, scalability, and compliance across the Nickel Based Superalloys Market.

The scope of the Nickel Based Superalloys Market Report encompasses a comprehensive examination of material types, production technologies, application verticals, and geographic regions that define the competitive landscape and future growth vectors of this high-performance materials sector. Coverage by type includes nickel-chromium, nickel-cobalt, and nickel-iron alloys, as well as advanced categories such as single-crystal and powder metallurgy grades engineered for extreme temperature and stress environments. Segmentation incorporates analysis of production technologies — from vacuum induction and arc remelting to additive manufacturing and hybrid production techniques — illustrating how process innovations enhance mechanical properties, reduce defects, and shorten qualification cycles.

The report evaluates application sectors like aerospace engines, power generation turbines, oil & gas equipment, and industrial manufacturing, detailing how performance requirements and regulatory compliance influence material selection and engineering strategies. End-user insights highlight demand patterns among OEMs, defense contractors, and utilities, including enterprise adoption trends and operational priorities such as maintenance optimization and lifecycle extension. Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering regional volume and adoption insights, infrastructure trends, and technology hubs shaping local markets.

Technological focus areas include the integration of additive manufacturing, AI-driven alloy design, and sustainable production practices, while niche segments address recycling and secondary processing capacity. The breadth of analysis ensures a strategic view for decision-makers evaluating supply chain dynamics, competitive positioning, risk exposures, and innovation opportunities in the evolving global Nickel Based Superalloys Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1008.11 Million |

|

Market Revenue in 2032 |

USD 1964.92 Million |

|

CAGR (2025 - 2032) |

8.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Allegheny Technologies Incorporated (ATI), Haynes International, Carpenter Technology Corporation, VDM Metals, Precision Castparts Corp., Special Metals Corporation, Aperam, Doncasters Group, AMG Advanced Metallurgical Group, Thyssenkrupp Materials, Haynes International, Carpenter Technology Corporation, ATI – Allegheny Technologies Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |