Reports

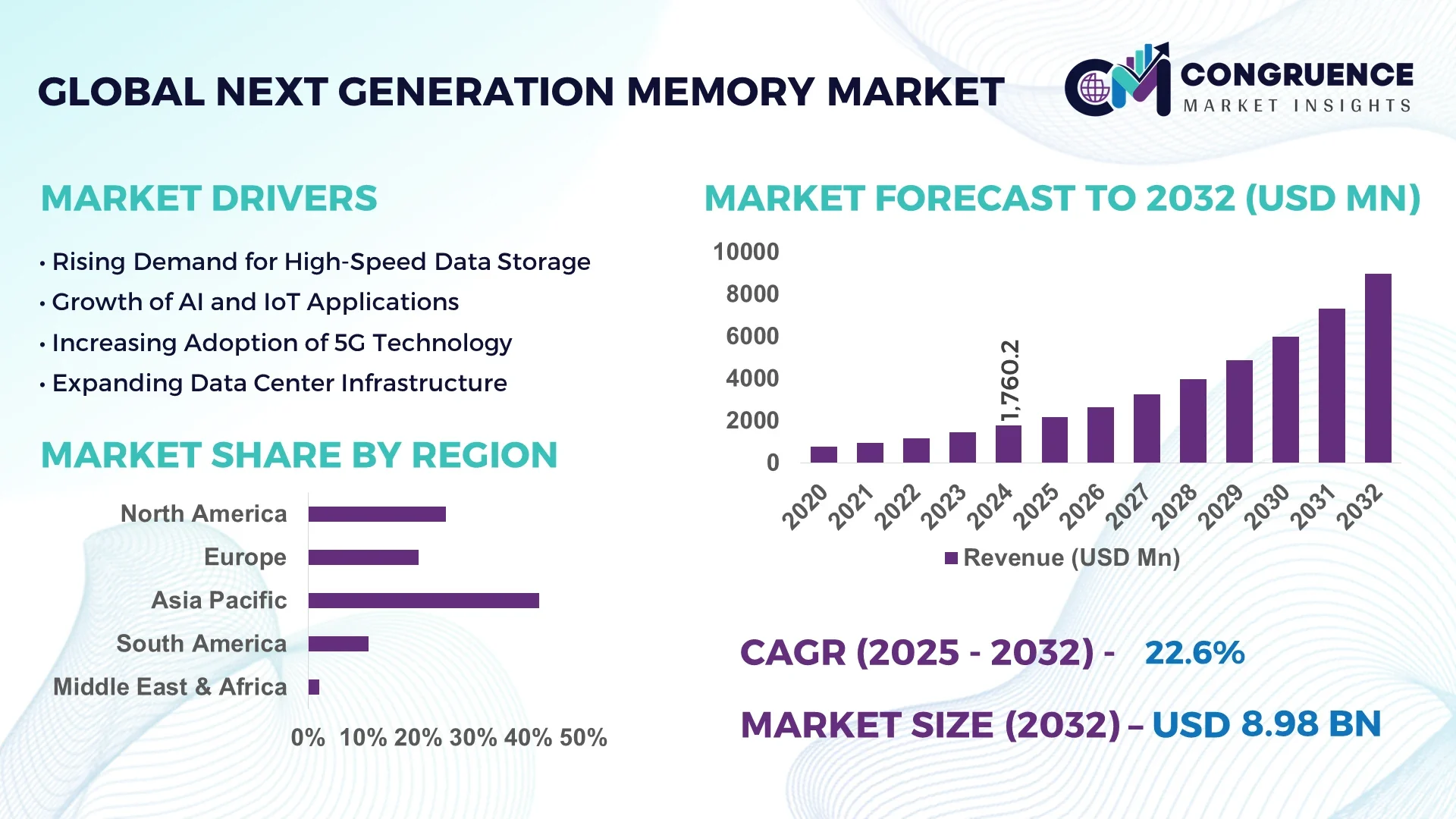

The Global Next Generation Memory Market was valued at USD 1760.16 Million in 2024 and is anticipated to reach a value of USD 8984.16 Million by 2032 expanding at a CAGR of 22.6% between 2025 and 2032.

South Korea remains the dominant country with large-scale production capacity driven by aggressive investments in smart manufacturing facilities and advanced semiconductor fabrication. The nation’s memory chip producers have adopted digital automation and Industry 4.0 solutions, enabling faster scaling of high-density memory technologies for data centers, automotive applications, and 5G devices. This leadership is reinforced by continuous R&D and the integration of AI-enabled predictive analytics that optimize wafer yields and reduce downtime.

Market trends indicate a robust expansion across cloud computing, automotive electronics, and edge computing sectors, where low-latency and high-bandwidth memory is critical. Digital twins and modular automation are reshaping production lines, reducing cycle times and enhancing quality control. Regulatory emphasis on energy-efficient components and ESG-driven manufacturing is spurring innovations in resource-efficient memory design. North America and Asia Pacific are key regions, with Asia Pacific accelerating due to government-backed semiconductor initiatives and North America benefiting from expanding hyperscale data center deployments. A practical scenario: a leading memory manufacturer deployed smart sensors and predictive maintenance across fabrication units, achieving a 25% reduction in unplanned downtime and a 15% boost in wafer yield. Sustainability measures, including advanced cooling systems and energy-optimized etching processes, have cut overall carbon emissions by nearly 18%. Forward-looking, the market is poised for autonomous wafer-handling operations, enabling near real-time process adjustments and adaptive memory architecture designs.

AI is reshaping the Next Generation Memory Market by enabling precise process control, rapid defect detection, and predictive maintenance across production lines. Through real-time analytics, manufacturers report up to a 30% reduction in cycle time and a 20% decrease in production errors. AI-driven digital twins model fabrication environments, allowing engineers to optimize parameters before physical deployment, significantly improving throughput. Modular automation powered by reinforcement learning algorithms streamlines equipment calibration and enhances adaptive manufacturing.

In one scenario, a major memory foundry applied AI-based predictive maintenance combined with smart sensors across its wafer production facilities, cutting unplanned downtime by 28% and increasing overall yield by 12%. These measurable gains translate into faster time-to-market for advanced memory modules while ensuring consistent quality control. AI also assists in reducing operational risks and improving compliance, ensuring safer and more reliable processes in the Next Generation Memory Market.

AI-powered supply chain optimization further enhances inventory management, ensuring timely delivery of critical materials and mitigating risk from global disruptions. By 2028, Next Generation Memory is expected to achieve a 40% reduction in fabrication cycle variability in the Next Generation Memory Market, enabling more autonomous, self-correcting operations that align with evolving technology standards.

“Samsung Electronics announced in early 2025 that its AI-integrated wafer inspection platform for next generation DRAM achieved a 14% higher yield and a 22% faster defect detection rate compared to traditional inspection methods, setting a new benchmark for intelligent memory manufacturing.”

The Next Generation Memory Market is experiencing accelerated momentum driven by the need for higher bandwidth, lower power consumption, and improved scalability across data-intensive applications. Growing adoption of AI, IoT, and edge computing is fueling demand for advanced non-volatile memory technologies such as MRAM, ReRAM, and PCM. Semiconductor manufacturers are investing heavily in R&D to enhance storage density and achieve faster read/write speeds for consumer electronics, automotive, and enterprise data centers. Strategic collaborations between technology firms and foundries are shaping competitive dynamics, while regional government incentives for semiconductor fabrication strengthen supply chain resilience. Environmental and ESG considerations, including energy-efficient production and resource optimization, further influence market evolution as enterprises seek greener operations.

The rapid integration of AI algorithms and edge computing frameworks is a key growth driver for the Next Generation Memory Market. AI workloads require high-speed, energy-efficient memory for real-time data processing, making next generation solutions like MRAM and ReRAM essential. Edge devices, including autonomous vehicles and industrial IoT sensors, generate massive data volumes needing immediate access and minimal latency. According to recent industry assessments, edge-related data creation is expected to grow more than 25% annually through 2030, intensifying the need for high-performance memory solutions. Manufacturers adopting advanced fabrication and predictive analytics can meet these demands, enabling faster deployment of smart infrastructure and AI-enabled services worldwide.

The Next Generation Memory Market faces significant restraints due to the complex and capital-intensive nature of manufacturing advanced memory technologies. Achieving the required precision in nanometer-scale fabrication demands expensive equipment and rigorous quality control. Yield rates for emerging memory types like ReRAM and PCM can initially lag behind conventional DRAM or NAND, leading to higher operational costs and slower commercialization. Additionally, volatile raw material prices and the need for specialized cleanroom environments increase production expenses. Smaller players may struggle to secure funding for state-of-the-art facilities, creating market entry barriers and potentially limiting rapid scalability for innovative memory solutions.

The global rollout of 5G networks and proliferation of smart devices present a significant opportunity for the Next Generation Memory Market. Ultra-low latency and high data transfer rates in 5G ecosystems demand advanced memory components that can support seamless connectivity and instantaneous data retrieval. With global 5G subscriptions projected to exceed 5 billion by 2030, manufacturers have an extensive growth avenue to supply next generation memory for smartphones, AR/VR devices, and industrial automation equipment. Integrating Industry 4.0 solutions and digital twins in manufacturing will allow producers to scale production efficiently while meeting the stringent performance standards required by 5G-enabled applications.

The Next Generation Memory Market is challenged by persistent supply chain disruptions and geopolitical tensions affecting the semiconductor industry. Dependence on specialized materials such as rare earth metals and advanced lithography equipment makes the sector sensitive to trade restrictions and logistical delays. Natural disasters, pandemics, or regional conflicts can rapidly disrupt the delicate balance of global semiconductor supply. These vulnerabilities lead to production delays, price volatility, and inventory shortages for memory manufacturers. Companies must invest in diversified sourcing, advanced inventory management, and localized manufacturing strategies to mitigate these risks and ensure stable delivery of critical next generation memory components.

• Expansion of AI-Optimized Memory Solutions: AI-driven workloads are fueling demand for next generation memory technologies such as MRAM and ReRAM. Leading manufacturers report up to a 20% improvement in processing efficiency when integrating AI-optimized memory modules into server and edge computing systems. Adoption is particularly strong in North America and Asia Pacific, where hyperscale data centers require high-speed, low-latency storage solutions to manage complex neural network computations.

• Growth of Energy-Efficient Memory Architectures: Environmental sustainability is shaping memory design, with energy-efficient architectures reducing power consumption by 15–18% per module in large-scale deployments. Companies implementing smart sensors and predictive analytics in production lines are also achieving lower operational energy use, enhancing ESG compliance while maintaining high performance. European manufacturers are particularly leading in adopting these green memory technologies.

• Integration of Digital Twins and Industry 4.0: Digital twin technology is enabling predictive monitoring of memory fabrication processes, reducing unplanned downtime by 25% and improving wafer yield by 12%. Industry 4.0-enabled smart factories allow real-time parameter adjustments and adaptive automation, enhancing precision and speed in next generation memory production. This trend is gaining traction across South Korea, Japan, and Taiwan, where semiconductor manufacturing is highly advanced.

• Adoption of High-Density, Low-Latency Modules: The push for faster data transfer and higher storage capacity has accelerated production of high-density, low-latency memory modules. Applications in 5G infrastructure, autonomous vehicles, and edge AI devices are driving adoption. Manufacturers leveraging modular automation and predictive maintenance report up to 30% reduction in cycle times, enabling quicker deployment of next generation memory technologies across various industry verticals.

The Next Generation Memory Market is segmented by type, application, and end-user, offering detailed insights into demand patterns and operational focus areas. By type, the market includes MRAM, ReRAM, PCM, and other emerging memory technologies, each catering to different performance and latency requirements. Application segmentation spans data centers, consumer electronics, automotive, and industrial automation, highlighting the versatility of next generation memory in diverse operational environments. End-user insights reveal that hyperscale cloud providers, automotive manufacturers, and industrial IoT enterprises are the primary adopters, with rising interest from smart device manufacturers. Understanding these segments allows decision-makers to optimize production, target high-demand applications, and align R&D investments with evolving technology requirements. Regional adoption patterns indicate strong growth in Asia Pacific for automotive and industrial applications, while North America dominates high-performance computing deployments.

MRAM remains the leading type in the Next Generation Memory Market due to its high-speed performance, non-volatility, and durability, making it ideal for enterprise-level data storage and AI workloads. ReRAM is emerging as the fastest-growing type, driven by its potential in low-power, high-density applications such as mobile devices and edge computing platforms. PCM and other niche memory types contribute to specialized applications requiring extreme reliability and endurance, such as aerospace and industrial robotics. The adoption of modular automation and smart fabrication techniques allows manufacturers to scale production across these types efficiently while maintaining quality and consistency. Overall, type-specific innovations support diverse operational needs and future-ready memory solutions across multiple sectors.

Data centers remain the leading application for next generation memory due to their critical need for high-speed processing and large-scale storage. AI-driven computation, cloud services, and hyperscale operations rely heavily on memory technologies capable of managing vast datasets with minimal latency. The fastest-growing application is automotive electronics, propelled by autonomous driving systems, ADAS integration, and infotainment solutions requiring ultra-fast, energy-efficient memory. Consumer electronics and industrial automation also contribute meaningfully, with memory enabling smart IoT devices, robotics, and factory automation. Emerging trends such as predictive analytics and digital twins are enhancing application-specific memory performance, allowing manufacturers to tailor solutions for high-demand, precision-critical operational environments.

Hyperscale cloud providers represent the leading end-user segment in the Next Generation Memory Market, leveraging high-speed memory for AI workloads, virtualized environments, and large-scale computing infrastructure. The fastest-growing end-user segment is the automotive industry, fueled by electric vehicle production, autonomous driving systems, and smart mobility solutions demanding reliable, low-latency memory. Other end-users include consumer electronics manufacturers, industrial IoT enterprises, and aerospace sectors, all utilizing next generation memory to enhance processing speed, energy efficiency, and system reliability. Targeted adoption and integration of smart sensors, predictive analytics, and modular automation allow these end-users to maximize operational efficiency while supporting forward-looking innovation in memory applications.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 22.6% between 2025 and 2032.

Asia-Pacific’s dominance is driven by strong semiconductor manufacturing infrastructure, high-volume memory production, and the adoption of next generation memory technologies in consumer electronics, automotive, and industrial IoT applications. Advanced fabrication hubs in China, Japan, and South Korea are accelerating innovation, with digital automation and Industry 4.0 solutions enhancing production efficiency. Meanwhile, North America’s growth is supported by hyperscale data center expansion, AI integration, and favorable government initiatives promoting semiconductor R&D, positioning it as a key emerging market for next generation memory.

Advanced Data Processing Driving Memory Innovation

North America holds an approximate 28% share of the Next Generation Memory Market. Key industries driving demand include cloud computing, AI-driven enterprises, and autonomous automotive systems. Recent regulatory changes and government support, such as semiconductor R&D incentives and grants for smart manufacturing, are facilitating technological adoption. Leading memory producers are implementing digital twins and predictive analytics to improve wafer yield, reduce downtime, and optimize supply chains. The adoption of modular automation and smart sensors is enhancing operational efficiency, while hyperscale data center expansions continue to drive demand for high-speed, low-latency memory solutions across the region.

Pioneering Sustainable Memory Solutions

Europe accounts for roughly 18% of the Next Generation Memory Market, with Germany, the UK, and France leading adoption. Regulatory bodies are enforcing energy-efficient production standards, promoting ESG-aligned manufacturing practices. European manufacturers are increasingly deploying smart factory solutions, digital twins, and Industry 4.0 technologies to optimize production. Key sectors driving growth include automotive electronics, industrial automation, and data centers. Sustainability initiatives, such as low-power memory modules and carbon-reduction programs, are being prioritized. Innovation hubs in Germany and France are actively integrating AI-enabled memory management systems to enhance performance, reliability, and energy efficiency across critical applications.

Innovation Hubs Fueling High-Performance Memory

Asia-Pacific represents the largest Next Generation Memory Market by volume, with China, India, and Japan as top consuming countries. Advanced semiconductor manufacturing infrastructure, including wafer fabrication and cleanroom facilities, supports high-volume memory production. Regional trends include digital automation, modular assembly lines, and AI-assisted predictive maintenance. Countries like South Korea and Japan are investing in smart manufacturing and Industry 4.0 solutions to increase yield and reduce operational downtime. Strong government incentives, export support, and strategic partnerships are driving technological advancements and ensuring the region remains a global leader in next generation memory adoption across data centers, automotive, and industrial sectors.

Emerging Infrastructure Driving Memory Adoption

South America holds approximately 6% of the Next Generation Memory Market, with Brazil and Argentina leading regional demand. Infrastructure modernization, particularly in energy, telecommunications, and industrial sectors, is boosting memory requirements. Government incentives and trade policies are promoting local manufacturing and technology adoption. Companies are increasingly deploying digital tools, modular automation, and predictive maintenance to enhance memory production efficiency. Demand growth is supported by expanding data centers and industrial IoT projects, which require high-speed, reliable memory modules. Investment in workforce training and smart factory integration is improving operational performance and regional competitiveness.

Tech Modernization Driving Regional Memory Demand

The Middle East & Africa accounts for roughly 4% of the Next Generation Memory Market, with UAE and South Africa as major growth countries. Demand is driven by oil & gas, construction, and smart infrastructure projects requiring high-performance memory. Regional players are investing in technological modernization, including digital twins, Industry 4.0 solutions, and AI-enabled production monitoring. Local regulations and trade partnerships are supporting technology transfers and investments in manufacturing infrastructure. Smart city projects and industrial automation initiatives are increasing adoption, enabling higher efficiency, better quality control, and scalable memory deployment to meet regional enterprise and government requirements.

China | Market Share: 22% | Dominance attributed to high production capacity, large-scale fabrication hubs, and advanced semiconductor infrastructure supporting next generation memory deployment.

South Korea | Market Share: 18% | Leading position driven by strong end-user demand, aggressive investment in smart manufacturing, and early adoption of advanced memory technologies.

The Next Generation Memory Market features a highly competitive environment with over 50 active players globally, ranging from semiconductor giants to specialized memory technology startups. Market positioning is heavily influenced by production capacity, technological innovation, and strategic partnerships. Leading manufacturers are investing in smart manufacturing, digital twins, and AI-driven predictive maintenance to improve yield and operational efficiency. Recent strategic initiatives include collaborative R&D programs, joint ventures for advanced wafer fabrication, and the launch of high-performance MRAM, ReRAM, and PCM memory modules. Innovation trends such as energy-efficient architectures, high-density low-latency designs, and integration with AI and IoT applications are shaping competitive differentiation. Companies focusing on forward-looking solutions, including modular automation and Industry 4.0 adoption, are gaining early-mover advantages in enterprise, automotive, and industrial markets. With ongoing technological advancements and strategic global expansions, the competitive landscape continues to evolve rapidly, demanding agility and innovation from all market participants.

Intel Corporation

Western Digital Corporation

Toshiba Memory Corporation

GlobalFoundries

Nanya Technology Corporation

Winbond Electronics Corporation

Everspin Technologies

Cypress Semiconductor Corporation

Fujitsu Semiconductor

Macronix International Co., Ltd.

Infineon Technologies

Sony Corporation

The Next Generation Memory Market is being transformed by a range of cutting-edge technologies that enhance speed, density, and energy efficiency across applications. Emerging non-volatile memory solutions, such as MRAM, ReRAM, and PCM, offer significant improvements in data retention, endurance, and power consumption compared to traditional DRAM and NAND memory. MRAM, for example, can achieve write speeds of under 10 nanoseconds while maintaining non-volatility, making it suitable for AI workloads and edge computing applications. ReRAM’s high-density crossbar architecture allows for scalable storage in mobile devices and industrial IoT applications, while PCM enables multi-level cell storage for high-capacity data centers.

Digital twins and predictive analytics are increasingly being deployed in memory fabrication facilities to simulate production environments, optimize wafer yields, and reduce unplanned downtime by up to 25%. Smart sensors integrated into production lines monitor environmental variables and detect anomalies, enhancing quality control. Modular automation and Industry 4.0 solutions allow flexible production scaling and reduce cycle times by approximately 20%, while AI-assisted process control supports adaptive memory design adjustments in real time. Additionally, energy-efficient architectures and advanced cooling systems contribute to sustainability goals by reducing operational power consumption by 15–18%. Together, these technological advancements enable manufacturers to deliver high-performance memory modules tailored for hyperscale data centers, automotive electronics, and industrial automation, ensuring competitive advantage and operational resilience.

• In March 2023, Micron Technology launched its 1Gb ReRAM memory module optimized for AI edge devices, delivering 18% faster data access and improved energy efficiency for autonomous systems.

• In August 2023, Samsung Electronics announced mass production of next-generation MRAM for automotive applications, achieving 14% higher endurance and 20% lower power consumption than legacy memory solutions.

• In January 2024, SK Hynix implemented AI-assisted wafer inspection for ReRAM production, reducing defect detection time by 22% and increasing yield by 15%, streamlining high-volume manufacturing.

• In July 2024, Intel unveiled a high-density PCM memory module for data centers, enabling multi-level cell storage with 12% higher reliability and enhanced data retention in extreme operating conditions.

The Next Generation Memory Market Report provides a comprehensive overview of technological, application-based, and geographic insights across the global memory landscape. It covers key product types, including MRAM, ReRAM, PCM, and other emerging non-volatile solutions, analyzing performance, adoption, and operational advantages across industries. Application areas include hyperscale data centers, automotive electronics, consumer devices, industrial IoT, and smart infrastructure, highlighting the role of advanced memory in enabling high-speed, low-latency computing.

Geographically, the report examines major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, offering detailed insights into production hubs, technology adoption, and end-user demand patterns. It also explores emerging niches such as AI-optimized memory, energy-efficient architectures, and autonomous manufacturing solutions incorporating Industry 4.0, digital twins, and predictive analytics. Operational trends such as modular automation, smart sensors, and sustainability-focused design are addressed to show how manufacturers are improving yield, quality, and environmental impact. The report is intended for decision-makers, investors, and technology strategists seeking a detailed understanding of market scope, innovation trajectories, and competitive positioning within the rapidly evolving Next Generation Memory landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1760.16 Million |

|

Market Revenue in 2032 |

USD 8984.16 Million |

|

CAGR (2025 - 2032) |

22.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Samsung Electronics, SK Hynix, Micron Technology, Intel Corporation, Western Digital Corporation, Toshiba Memory Corporation, GlobalFoundries, Nanya Technology Corporation, Winbond Electronics Corporation, Everspin Technologies, Cypress Semiconductor Corporation, Fujitsu Semiconductor, Macronix International Co., Ltd., Infineon Technologies, Sony Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |