Reports

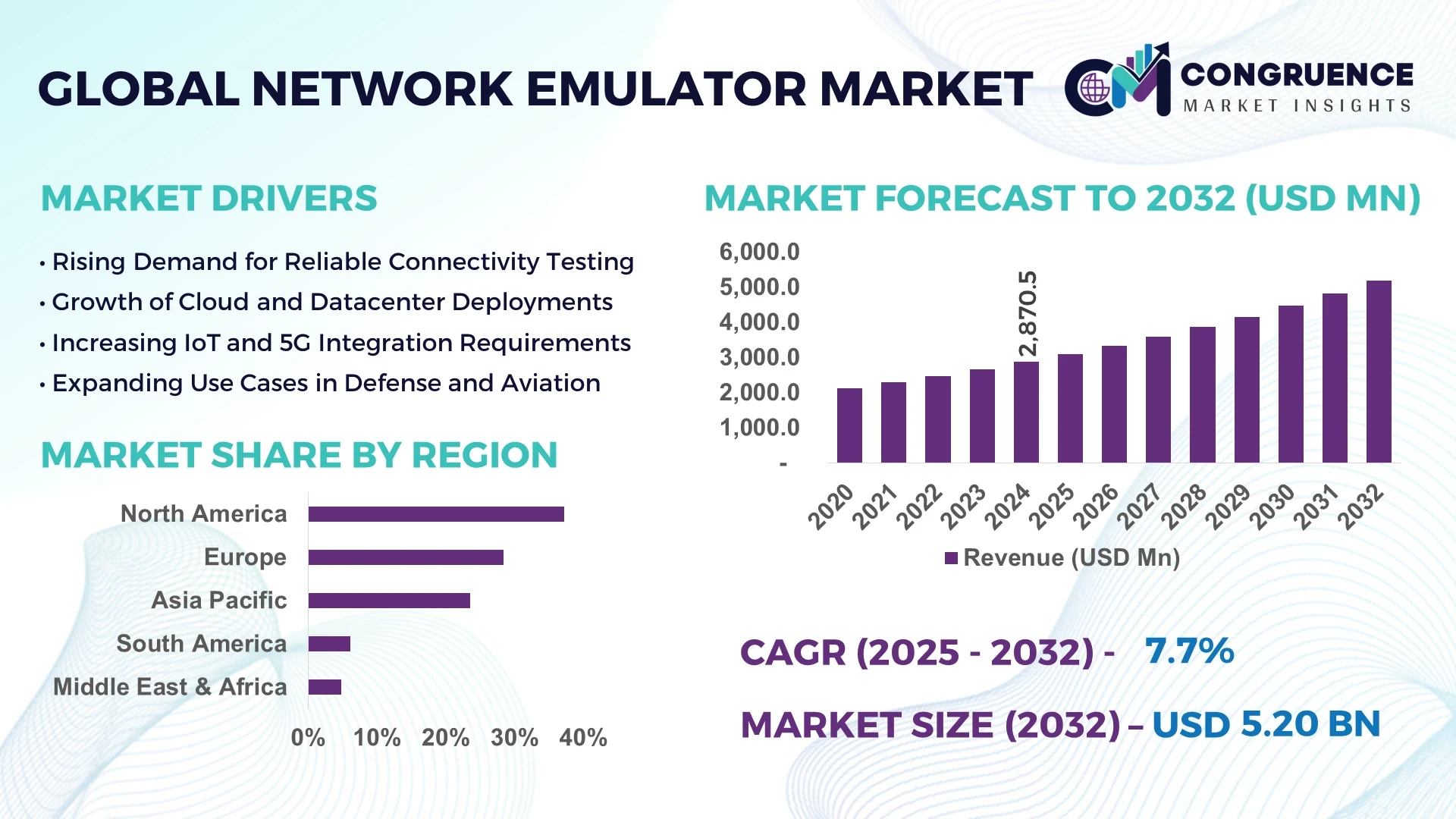

The Global Network Emulator Market was valued at USD 2,870.5 Million in 2024 and is anticipated to reach a value of USD 5,211.6 Million by 2032 expanding at a CAGR of 7.74% between 2025 and 2032.

In China, which leads the global marketplace, production capacity for network emulator equipment has reached over 15,000 units annually, supported by investments exceeding USD 200 million in next-generation development facilities. Key industry applications span telecommunications testing, cloud-native deployments, and autonomous vehicle connectivity trials. Significant technological advancements include integrated AI-enabled scenario simulation and multi-node latency tuning in real-time.

Across the Global Network Emulator Market, critical sectors such as telecom service providers, cloud and datacenter operators, and automotive and transportation enterprises contribute substantially to demand. Telecoms alone account for roughly one-third of all usage, while cloud infrastructure testing and connected-vehicle validations drive another quarter. Recent innovations center on virtualization of testing environments, high-fidelity multi-path network traffic reproduction, and low-latency hardware-in-the-loop systems. Regulatory and economic factors—including expanded 5G spectrum licensing, stricter network resilience mandates, and economic stimulus toward digital infrastructure—are accelerating adoption across regions. Consumption patterns show strong growth in Asia-Pacific for scalable lab-based testing, while Europe emphasizes compliance-ready, high-assurance emulation. Emerging trends point to increasing integration of emulation platforms with CI/CD pipelines for continuous testing, plus expansion into IoT device certification. The future outlook for the Network Emulator Market is one of deepening convergence between emulation, virtualization, and automation, offering decision-makers robust tools for network validation across digital transformation efforts.

AI is increasingly reshaping the Network Emulator Market by automating complex network scenario generation and enabling predictive adaptation of emulated networks. Decision-makers in telecom and cloud sectors now leverage AI-driven traffic pattern analysis to dynamically calibrate latency, jitter, and packet loss parameters, reducing manual scenario configuration time by over 50%. AI-enhanced emulation systems can detect anomalies in real time, triggering adaptive emulation adjustments that improve operational performance under volatile network loads. Furthermore, AI-powered clustering of test cases enables prioritization of high-risk scenarios, optimizing resource utilization within emulation labs and cutting test cycle durations by approximately 40%. In addition, machine learning models embedded in emulator platforms predict degraded network paths and pre-emptively adjust emulation parameters, yielding smoother handover testing for mobile networks. Enterprises deploying AI-integrated network emulators report measurable efficiency gains—in one case, scenario setup time dropped from hours to mere minutes, while validation accuracy improved by 20%. Such AI capabilities are especially valuable for continuous integration and deployment pipelines, where rapid, reliable network emulation drives faster rollout of network-dependent applications. Across sectors—from telecom operators verifying 5G-to-6G transitions to cloud providers validating service resilience—AI is enhancing agility, accuracy, and throughput in the Network Emulator Market.

“In mid-2024, a major emulator vendor introduced an AI-based scenario optimizer that reduced end-to-end latency variation by 15% during automated 5G network emulation runs.”

The Network Emulator Market dynamics are shaped by evolving infrastructure testing demands, growing adoption of virtualization, and shifting enterprise validation requirements. As networks become more complex, with layered virtualization, multi-access edge computing, and hybrid cloud interconnectivity, the need for accurate, scalable emulation environments intensifies. Decision-makers face pressure to validate performance, reliability, and security before deployment, driving investments in modular emulator systems that can simulate varied network topologies. Moreover, industry emphasis on rapid provisioning and environment reproducibility is pushing suppliers toward offering pre-configured emulator suites and containerized testing nodes. Regulatory mandates around network resilience and service-level testing in both developed and emerging markets are further influencing purchasing behavior. Overall, demand for flexible, cloud-integrated emulation platforms is rising, as enterprises seek to adapt to real-world network conditions under evolving operational constraints.

The proliferation of virtualized network functions (VNFs) and software-defined networking (SDN) is driving up demand for network emulators capable of replicating complex, multi-domain topologies. Enterprises deploying SD-WAN, NFV stacks, and cloud-native microservices require precise validation of network behavior under variable conditions. In response, emulator providers have delivered modular systems that handle up to 128 concurrently emulated nodes, enabling comprehensive testing of virtual overlays and dynamic routing changes. These platforms support programmatic control and API-based configuration, aligning closely with DevOps and NetOps workflows. In verticals such as finance and healthcare, where segmented networks must maintain strict performance, the ability to model virtualized architectures has become indispensable—fueling uptake of advanced emulator solutions.

The Network Emulator Market is challenged by limitations in hardware availability—particularly specialized network interface cards (NICs), FPGA modules, and high-performance packet processors needed for low-latency, high-throughput emulation. Some high-fidelity platforms require PCIe-based accelerators that have seen intermittent production bottlenecks, resulting in delivery lead times of 12 to 16 weeks. These hardware supply issues constrain the scalability of emulation labs and can delay deployment timelines for enterprises seeking to replicate real-world network loads. Organizations operating under tight validation schedules may need to limit concurrent test environments or defer upgrades, impacting overall productivity in network performance benchmarking and validation workflows.

An emerging opportunity lies in embedding network emulators directly into cloud-native CI/CD pipelines. Emulator platforms are increasingly offered as containerized microservices that can spin up within Kubernetes-based environments, enabling on-demand, ephemeral network scenario testing. This integration allows development teams to validate network behavior in automated build and deployment workflows, reducing time-to-market for network-reliant applications. Furthermore, emulator-as-a-service models are gaining traction; organizations that lack on-premises hardware can access scalable emulation environments via pay-as-you-go cloud platforms. Such trends enable broader adoption across SMEs and development teams, expanding the market beyond traditional telecom and enterprise labs.

Despite advances, configuring emulators for multi-domain scenarios—including cross-border latency, heterogeneous access technologies, and complex routing policies—remains costly and technically demanding. Setting up such testbeds often involves manual scripting and detailed orchestration of multiple emulation nodes or cloud instances, requiring specialized expertise. This complexity increases integration time, error risk, and labor costs. Moreover, multi-domain validation often demands external connectivity, compliance with data privacy regulations, and coordination with multiple providers—adding layers of procurement and management overhead. Thus, high complexity and associated expenditures create entry barriers for organizations seeking advanced, cross-domain network testing.

Surge in Virtual Emulator-as-a-Service Offerings: Enterprises are increasingly adopting cloud-hosted network emulation platforms offered on a subscription basis. These services allow teams to instantiate complex test environments—including mixed 4G/5G, WAN, and IoT segments—within minutes, supporting hundreds of concurrent sessions. The trend has enabled smaller organizations to access high-fidelity emulation previously confined to specialized labs, accelerating development cycles and democratizing advanced network validation.

Growth of Edge-Focused Emulator Deployments: There is a notable shift toward deploying emulator instances at edge locations to simulate real-world conditions like last-mile variability and mobile handoffs. Providers now ship miniature emulator appliances with sub-5 ms latency capabilities, usable in field labs or near-site testbeds. These compact systems help telecom operators and IoT integrators validate localized services more effectively.

Enhanced Real-Time Traffic Synthesis and Monitoring: Advanced emulator platforms now embed live traffic synthesis modules that recreate dynamic network flows based on captured production traces. These modules support granular adjustments—such as per-flow jitter or burst packet loss—and provide real-time performance dashboards. As a result, testing fidelity has improved; teams can now emulate diurnal and event-driven traffic spikes with sub-millisecond accuracy.

Emergence of AI-Driven Automated Scenario Generation Tools: Following development of AI optimizers, several emulator vendors now offer modules that analyze usage patterns and auto-generate emulation scenarios covering peak loads, failover events, and network degradation cases. Users report that scenario creation time has dropped sharply, while the breadth of coverage has expanded to include previously overlooked edge-case conditions—transforming network validation practices across industries.

The Network Emulator Market is segmented into types, applications, and end-user categories, each reflecting distinct technological capabilities and operational demands. Product types range from traditional hardware-based systems to increasingly sophisticated software-defined and hybrid solutions, each addressing specific testing environments and scalability needs. Applications span telecommunications, cloud and datacenter validation, IoT device certification, and automotive connectivity testing, with varying adoption rates based on sectoral priorities and infrastructure maturity. End-users include telecom operators, enterprises, research institutions, and defense organizations, each driving unique functional requirements in terms of latency control, throughput emulation, and topology flexibility. The segmentation highlights a shift toward software-centric, virtualized, and cloud-integrated solutions, aligning with the global movement toward agile, automated, and cost-efficient testing frameworks. Emerging adoption in edge computing and 6G research further broadens the scope for specialized emulator configurations across diverse industry verticals.

Hardware-based network emulators currently lead the market due to their unmatched precision in reproducing complex, high-throughput network conditions with minimal latency deviation. These systems are critical in sectors where deterministic performance is essential, such as defense communications and mission-critical industrial automation. However, software-based network emulators represent the fastest-growing type, driven by demand for scalable, flexible solutions that can be rapidly deployed within virtualized environments. Their compatibility with CI/CD pipelines and cost advantages over physical systems make them especially appealing to cloud-native development teams. Hybrid emulators, combining both hardware precision and software agility, are gaining traction for multi-environment testing needs, particularly in large enterprises managing both legacy and next-generation networks. Other niche types, such as portable and edge-focused emulators, contribute by supporting on-site and mobile validation scenarios, meeting the needs of industries like autonomous vehicle testing and disaster response communications.

Telecommunications network testing remains the dominant application segment, owing to the complexity of validating next-generation mobile infrastructure, from 5G rollouts to early-stage 6G trials. Operators rely on emulators to assess network resilience, handover stability, and service quality under varied conditions. The fastest-growing application is in IoT and connected device validation, fueled by rapid growth in smart city deployments, industrial IoT adoption, and consumer device interconnectivity. These scenarios demand highly adaptable emulation environments capable of handling diverse protocols and massive device densities. Cloud and datacenter validation also play a significant role, particularly as hyperscale operators integrate emulators into automated infrastructure testing to ensure uptime and service consistency. Additional applications, such as in automotive connectivity, aviation communication systems, and research-focused testbeds, contribute to the market’s breadth by addressing specialized performance and compliance requirements.

Telecom operators stand as the leading end-user group, leveraging network emulators extensively to optimize rollout strategies, ensure compliance with regulatory performance benchmarks, and conduct large-scale interoperability testing. The fastest-growing end-user category is cloud service providers, driven by the need to ensure seamless service delivery, rapid scaling capabilities, and fault-tolerant infrastructure across distributed environments. Enterprises in sectors such as finance, healthcare, and manufacturing also form a critical share of the market, particularly as they adopt SD-WAN and hybrid networking solutions requiring rigorous pre-deployment testing. Research and academic institutions contribute by utilizing emulators in advanced networking studies, including 6G research and edge computing scenarios. Defense and security organizations, while smaller in number, maintain high-value usage due to stringent performance and security validation needs for mission-critical communication systems. Together, these diverse end-users underscore the adaptability and growing strategic relevance of network emulators across multiple industries.

North America accounted for the largest market share at 37.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

The regional landscape reflects varying levels of technological maturity, infrastructure investment, and industry-specific adoption patterns. While developed markets focus on enhancing testing efficiency for advanced 5G, SDN, and IoT deployments, emerging economies are rapidly scaling emulator usage to accelerate digital transformation and network readiness. Strong demand drivers include the rollout of next-generation networks, cloud computing growth, and the adoption of automated testing in diverse verticals such as telecommunications, automotive, and aerospace. Government-led infrastructure initiatives and regional innovation hubs continue to shape competitive positioning across the global Network Emulator Market.

North America held a 37.2% share of the global Network Emulator Market in 2024, driven primarily by high adoption rates among telecom operators, hyperscale cloud providers, and defense contractors. Key industries such as telecommunications, aerospace, and autonomous vehicle development fuel consistent demand for high-fidelity network emulation systems. Regulatory changes, including updated network resilience and cybersecurity testing mandates, have further reinforced market uptake. Technological advancements—particularly AI-enabled automation in network scenario generation—are enabling enterprises to reduce setup times and improve simulation accuracy. The U.S. remains the dominant contributor within the region, while Canada is gaining momentum in software-defined and cloud-based emulator deployments for its expanding tech sector.

Europe accounted for 28.4% of the global Network Emulator Market in 2024, with Germany, the UK, and France leading adoption. Key demand comes from telecom operators, industrial IoT integrators, and automotive manufacturers seeking precise validation of connected systems. Regulatory bodies such as the European Telecommunications Standards Institute (ETSI) and the European Commission’s Digital Europe program are influencing testing protocols and driving compliance requirements. Sustainability initiatives are encouraging energy-efficient emulation solutions, reducing operational footprints without compromising performance. Emerging adoption of technologies such as network slicing, virtualized RAN testing, and 6G readiness is accelerating deployment in both enterprise and research environments across the region.

Asia-Pacific ranked second in overall market volume in 2024 and is positioned as the fastest-growing region. China, India, and Japan dominate consumption, supported by robust telecom infrastructure expansion, rapid 5G deployments, and large-scale IoT rollouts. Regional manufacturing hubs are producing both hardware and software-based emulators to meet rising domestic and export demand. China leads in AI-integrated emulator production, while Japan’s innovation hubs specialize in ultra-low-latency and automotive-focused solutions. India is emerging as a major software development center for cloud-native emulation platforms. The combination of infrastructure investments, innovation-led clusters, and government-backed digitalization programs is propelling the region’s strong growth trajectory.

South America represented 6.1% of the global Network Emulator Market in 2024, with Brazil and Argentina as the primary contributors. Regional demand is driven by ongoing upgrades to telecom infrastructure, expansion of energy sector networks, and modernization of public safety communications. Brazil’s government-backed broadband initiatives and Argentina’s smart city projects are generating new opportunities for emulator adoption. Technology providers in the region are also partnering with global firms to bring advanced emulation capabilities to local markets, particularly for WAN optimization and satellite communication testing. These developments are enhancing the region’s ability to validate network performance in diverse and challenging environments.

Middle East & Africa accounted for 4.8% of the global Network Emulator Market in 2024, with UAE, Saudi Arabia, and South Africa leading adoption. The oil & gas sector, large-scale construction projects, and expanding telecom infrastructure are key demand drivers. Technological modernization trends—such as the adoption of 5G private networks and integration of IoT into industrial operations—are fueling the need for advanced emulation systems. Local regulations supporting telecom quality assurance and cross-border trade partnerships are facilitating market expansion. UAE’s investment in smart city projects and South Africa’s focus on broadband access are also boosting the uptake of emulators for complex scenario testing.

United States – 28.5% Market Share

Dominance is driven by advanced telecom infrastructure, extensive R&D in network technologies, and high adoption of AI-enabled emulator platforms.

China – 21.7% Market Share

Leadership is fueled by large-scale production capacity, government-backed digitalization programs, and rapid adoption in telecom, automotive, and IoT sectors.

The global network emulator market features around 35 active competitors, ranging from multinational corporations to niche technology providers. Market leaders are focusing on partnerships with telecom operators, product innovation, and AI-driven solutions to strengthen positioning. Strategic alliances between software and hardware providers are enhancing product integration and scalability. Competitive differentiation is increasingly based on low-latency simulation, real-time analytics, and cloud-based deployment capabilities. Mergers and acquisitions have been notable, with companies targeting startups specializing in virtualized and software-defined networking tools. The market also reflects growing investment in open-source platforms to expand compatibility and reduce operational costs.

Keysight Technologies

Spirent Communications

VIAVI Solutions Inc.

Polaris Networks

iTrinegy

Apposite Technologies

Calnex Solutions

SolarWinds

PacketStorm Communications Inc.

The network emulator market is being reshaped by rapid advancements in virtualization, AI integration, and cloud-based testing. Modern network emulators are now capable of simulating complex hybrid environments, including 5G, IoT, and edge computing ecosystems. Virtualized network functions (VNFs) and software-defined networking (SDN) are enabling scalable, cost-effective testing without heavy reliance on physical infrastructure. AI algorithms enhance traffic prediction, anomaly detection, and automated testing workflows, reducing time-to-market for new network deployments. In telecom, emulators are supporting multi-vendor interoperability testing for 5G core and radio access networks. The rise of low-latency applications like autonomous vehicles, telemedicine, and immersive gaming is pushing demand for ultra-precise emulation. Furthermore, the transition toward cloud-native network architecture is prompting the adoption of subscription-based and on-demand emulator solutions. Hardware acceleration through FPGA-based designs is improving test performance, while integration with cybersecurity tools is strengthening resilience against cyber threats. These technological developments are setting the foundation for next-generation network validation.

In March 2024, Keysight Technologies launched its Cloud Peak emulator, designed to accelerate 5G network function validation in hybrid cloud environments, improving scalability for telecom operators.

In November 2024, Spirent Communications expanded its 5G network test portfolio with new AI-powered automation features, reducing testing time for mobile service providers by up to 40%.

In July 2023, VIAVI Solutions introduced an enhanced network emulator with integrated cybersecurity assessment tools, enabling real-time vulnerability detection.

In September 2023, Apposite Technologies unveiled a portable network emulator for field engineers, offering high-precision simulation in compact form factors for rapid deployment.

The Network Emulator Market Report offers an in-depth examination of the industry’s structure, trends, and competitive landscape, covering a broad range of market segments by application, technology, and region. It evaluates enterprise, telecom, government, and industrial uses of network emulation tools, highlighting differences in adoption patterns across geographic regions. The scope includes hardware-based, software-based, and hybrid emulator systems, with detailed segmentation by deployment models such as on-premises and cloud-based solutions. Geographically, the report encompasses North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with analysis of both mature and emerging markets. It also investigates technology trends including SDN, NFV, AI integration, and 5G testing, as well as their influence on market growth. Specialized applications such as IoT, autonomous systems, and mission-critical communications are reviewed, along with emerging niches like portable and edge-optimized emulators. This comprehensive coverage provides decision-makers with actionable insights into competitive positioning, innovation opportunities, and strategic investment areas within the network emulator sector.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 2,870.5 Million |

| Market Revenue (2032) | USD 5,211.6 Million |

| CAGR (2025–2032) | 7.74% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Keysight Technologies, Spirent Communications, VIAVI Solutions Inc., Polaris Networks, iTrinegy, Apposite Technologies, Calnex Solutions, SolarWinds, PacketStorm Communications Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |