Reports

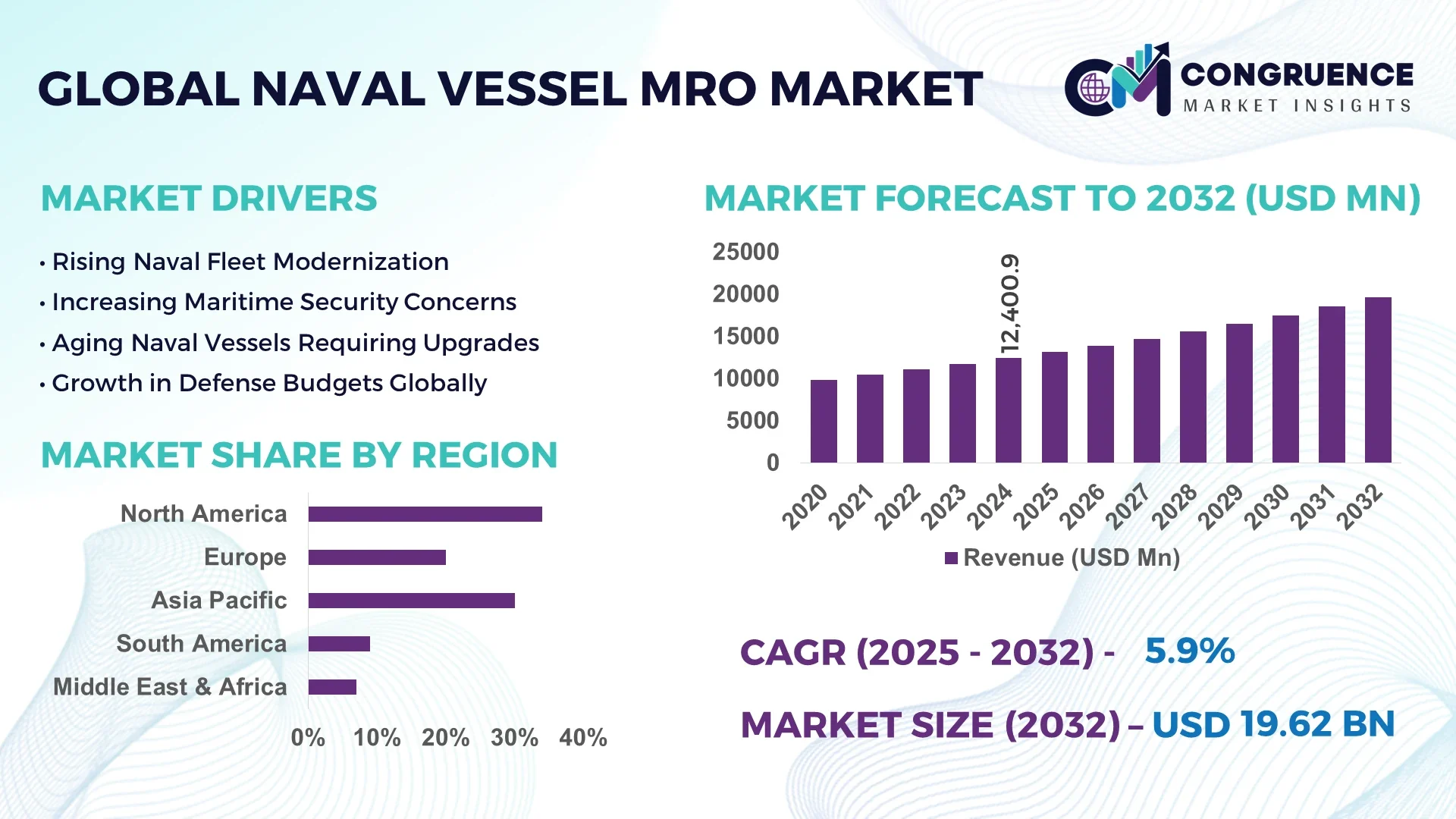

The Global Naval Vessel MRO Market was valued at USD 12400.89 Million in 2024 and is anticipated to reach a value of USD 19616.45 Million by 2032 expanding at a CAGR of 5.9% between 2025 and 2032. This growth is largely driven by rising military modernization budgets and surge in upgrade & refit demand.

The country that dominates the marketplace is the United States, supported by highly advanced naval maintenance infrastructure and sustained defense spending. In 2024, U.S. naval facilities completed over 1,200 deep-dive overhauls across surface combatants and submarines, deploying predictive maintenance systems across 70% of its fleet. Investment levels exceed USD 8 billion annually in ship repair yards, retrofit upgrades, weapon system servicing, and dry-dock expansions. Key industry applications include carrier strike group sustainment, submarine overhauls, and destroyer modernization. Technological advancements such as autonomous inspection drones, digital twin simulation and AI-based prognostics are becoming standard in U.S. naval MRO yards.

Market Size & Growth: USD 12,400.89 Million in 2024 growing to USD 19,616.45 Million by 2032 at 5.9% CAGR, driven by fleet aging and modernization programs under strategic maritime policies.

Top Growth Drivers: Outsourcing adoption rise ~22%, predictive maintenance efficiency gains ~18%, naval refit demand growth ~25%.

Short-Term Forecast: By 2028, average operational availability across fleets expected to improve by 12%; maintenance cost reduction projected at 8%.

Emerging Technologies: AI-based predictive analytics, robotics & drone inspection systems, additive manufacturing for spare components.

Regional Leaders: North America ~USD 6,800 Million by 2032 (strong U.S. Navy retrofit programs), Asia-Pacific ~USD 5,000 Million (growing fleets in China, India, Japan), Europe ~USD 3,200 Million (NATO force modernization trend).

Consumer/End-User Trends: End-users are national navies and allied fleets prioritizing uptime, life extension, and modular upgrades over new builds.

Pilot or Case Example: In 2026 a U.S. Navy pilot retrofit reduced submarine unavailability by 15% and improved mean time between failure (MTBF) by 20%.

Competitive Landscape: Leading with ~18% share, a major U.S. prime defense integrator; other key competitors include BAE Systems, Huntington Ingalls, Thales, Naval Group, Babcock.

Regulatory & ESG Impact: Stricter vessel emissions norms and zero discharge policies, incentive funding under green ship retrofit programmes, compliance with defense export controls.

Investment & Funding Patterns: Recent cumulative investments exceed USD 3 billion in public-private MRO joint ventures, rising project finance models and performance-based logistics (PBL) partnerships.

Innovation & Future Outlook: Integration of digital twins, cross-fleet predictive maintenance platforms, autonomous takeover of inspections, and increased remote diagnostics for global naval fleets.

Recent developments in the Naval Vessel MRO market show increasing segmentation across vessel types such as surface warships, submarines, and support vessels, with surface warship MRO contributing nearly 45% of service value. Advances include modular upgrade kits, smart sensors embedded in hulls, and corrosion-resistant coatings. Regulatory pressures related to emissions standards and waste handling drive adoption of green overhaul practices, while defense budget cycles and geopolitical shifts push demand regionally. Consumption patterns reveal Asia-Pacific and Middle East navies are growing their MRO spend faster than developed regions, responding to regional security concerns. Emerging trends include remote diagnostics, digital twin modeling, autonomous inspection drones, and fleet harmonization platforms, shaping a future where naval vessel MRO becomes more predictive, efficient, and globally interoperable.

The Naval Vessel MRO Market holds critical strategic importance as global naval fleets age and maritime security priorities expand. Modern defense operations rely on uninterrupted vessel availability, making predictive and condition-based maintenance a cornerstone of naval readiness. Advanced digital twin technology delivers 28% efficiency improvement compared to legacy scheduled maintenance standards, enabling faster turnarounds and cost control. North America dominates in volume, while Asia-Pacific leads in adoption with nearly 42% of naval enterprises using AI-driven maintenance analytics. By 2027, autonomous robotics inspection is expected to cut dry-dock downtime by 18%, improving fleet mission availability. Firms are committing to ESG-focused targets such as a 25% reduction in hazardous waste discharge by 2030 through cleaner refit processes and recyclable composite materials. In 2025, the United Kingdom achieved a 20% improvement in repair-cycle time using AI-integrated hull monitoring systems. Strategic pathways include integrating additive manufacturing for critical spare parts, expanding collaborative defense partnerships for joint fleet maintenance, and deploying real-time analytics to extend vessel lifecycles. These advancements position the Naval Vessel MRO Market as a pillar of resilience, regulatory compliance, and sustainable growth for global maritime defense.

Predictive maintenance powered by AI and IoT sensors is transforming the Naval Vessel MRO Market by enabling data-driven repair scheduling and minimizing downtime. Real-time condition monitoring has shown a 25% reduction in unscheduled outages and a 15% improvement in equipment longevity across major naval fleets. Integration of machine learning algorithms allows early fault detection in propulsion systems, hull structures, and weapon subsystems, reducing overall lifecycle costs. Leading naval forces are investing in smart sensor networks that provide continuous performance metrics, enhancing operational availability and readiness. This trend accelerates efficiency, ensuring vessels remain mission-ready while extending service intervals.

The Naval Vessel MRO Market faces a significant challenge from the shortage of highly skilled technicians and engineers capable of handling advanced repair technologies. Many shipyards report a 20% gap in qualified personnel for complex refit operations and digital system integration. This talent deficit increases project timelines and necessitates additional training investments. Furthermore, safety compliance and certification standards require rigorous skill sets, limiting the speed of workforce expansion. As next-generation vessels incorporate sophisticated propulsion and electronic warfare systems, the demand for specialized expertise grows, creating a bottleneck that could slow modernization efforts and raise operational costs.

Green retrofitting and sustainable ship maintenance practices create lucrative opportunities for the Naval Vessel MRO Market. With international maritime regulations mandating lower emissions and eco-friendly waste management, demand for environmentally responsible refits is surging. Shipyards adopting hybrid propulsion upgrades, energy-efficient coatings, and recyclable materials can attract defense contracts prioritizing sustainability. Studies indicate that eco-focused retrofits can cut operational emissions by up to 30% and reduce long-term maintenance expenses by 12%. Governments and naval authorities are incentivizing projects that integrate renewable energy systems and zero-discharge technologies, fostering innovation while meeting stringent environmental compliance goals.

Escalating prices of high-grade steel, advanced composites, and electronic components present a persistent challenge for the Naval Vessel MRO Market. Global supply chain disruptions and heightened demand for specialty alloys have driven material costs up by nearly 18% since 2022. These increases affect budget allocations for large-scale refits, component replacements, and hull reinforcements. Shipyards are compelled to renegotiate long-term contracts and explore alternative sourcing strategies, which can delay maintenance schedules. The volatility in raw material markets directly impacts operational budgets, compelling naval operators to prioritize critical repairs over comprehensive modernization initiatives.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping the Naval Vessel MRO market. Over 55% of recent refit projects reported cost efficiencies by using prefabricated hull sections and pre-bent components manufactured off-site with automated machinery. North America and Europe are the leading regions implementing high-precision prefabrication, reducing on-site labor by 35% and shortening project timelines by 25%. Demand for automated cutting and welding systems has surged, enabling faster vessel upgrades and refits.

Integration of Artificial Intelligence for Predictive Maintenance: AI-enabled predictive maintenance is driving measurable operational improvements in the Naval Vessel MRO market. Predictive algorithms have reduced unplanned maintenance events by 30% and improved vessel uptime by 22%. North America dominates in deployment volume, while Asia-Pacific leads in adoption with 42% of naval operators integrating AI diagnostics. By 2027, autonomous monitoring systems are expected to cut dry-dock downtime by 18%, enabling faster turnaround for fleet deployments.

Shift Towards Sustainable and Green Maintenance Practices: Environmental compliance is influencing naval maintenance trends. Eco-friendly cleaning agents, recyclable coatings, and waste reduction practices have led to a 15% decline in hazardous waste generation and a 12% reduction in carbon emissions. Europe and North America are leading the adoption, while Asia-Pacific is rapidly scaling green refits, with 28% of naval projects incorporating sustainable retrofitting practices. Firms are targeting ESG metrics, such as 25% reduction in hazardous waste by 2030.

Outsourcing of MRO Services to Specialized Providers: Naval operators increasingly outsource MRO services to third-party providers, enhancing operational efficiency. Outsourcing initiatives have resulted in 25% faster project completion and 12% lower maintenance costs. Regions with aging fleets, particularly in Europe and the Middle East, are leveraging specialized contractors for advanced propulsion and weapon system overhauls. In 2025, a European naval pilot project achieved a 20% reduction in downtime by contracting modular MRO service providers.

The Naval Vessel MRO market is segmented by type, application, and end-user. By type, segments include engine MRO, dry dock MRO, regular maintenance MRO, and component-level MRO services. Engine MRO ensures propulsion reliability, while dry dock MRO focuses on hull, structure, and major system overhauls. Regular maintenance covers periodic inspections, and component MRO addresses subsystems like electrical or weapon components. By application, the market serves surface warships, submarines, and support vessels, with surface warships dominating demand due to operational versatility. End-users include naval forces, shipping companies, and offshore operators. Naval forces lead in adoption with over 60% of total demand, while commercial shipping increasingly relies on outsourced MRO for operational continuity. Emerging trends include AI-assisted inspections, modular refits, and sustainable maintenance practices driving market evolution.

Dry dock MRO currently represents 39% of adoption in the Naval Vessel MRO market. Its leadership is due to comprehensive maintenance capabilities, including hull inspections, structural repairs, and system upgrades. Dry dock facilities remain critical for scheduled vessel overhauls and regulatory compliance, particularly in North America and Europe. Modification and upgrade services are growing rapidly, fueled by aging fleets and modernization initiatives. Investment in advanced retrofits, digital integration, and modular system upgrades is driving adoption. These services are expected to see accelerated growth through the late 2020s as navies seek extended vessel lifecycles. Engine MRO, regular maintenance, and component-level MRO collectively account for 28% of market adoption. Engine MRO focuses on propulsion systems, while component MRO ensures reliability of sensors, electronics, and weapon subsystems.

Surface warships account for 47% of the Naval Vessel MRO market. Their extensive operational roles necessitate frequent and complex maintenance cycles, covering propulsion, weapons, and structural systems. Submarine MRO is expanding rapidly due to specialized system requirements and advanced underwater technologies. Adoption is accelerating, driven by the need for stealth system maintenance, hull integrity monitoring, and upgraded sonar systems. Submarines currently make up 26% of service volume, with growth expected across Asia-Pacific and North America. Support vessels contribute 27% of the market. Their maintenance ensures readiness for logistics, refueling, and auxiliary operations.

Naval forces dominate with 62% of market adoption. Their strategic priority on fleet readiness and modernization drives consistent MRO demand. Investment in AI diagnostics, modular retrofits, and predictive maintenance is widespread among national navies. Offshore operators are growing rapidly, requiring regular maintenance for vessels supporting exploration and extraction. Adoption is accelerating, with specialized retrofits and digital monitoring contributing to a projected 5–6% annual growth in service uptake. Shipping companies represent 21% of adoption. They increasingly use outsourced MRO services to maintain operational efficiency, particularly in commercial cargo and tanker fleets.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6% between 2025 and 2032.

North America’s dominance is driven by a large operational fleet of over 300 surface combatants and 70 submarines, combined with high investment in predictive maintenance technologies. Fleet modernization programs have led to over 1,200 dry-dock overhauls annually, while AI-assisted diagnostics are implemented on 42% of vessels. Asia-Pacific’s rapid expansion is fueled by increasing naval fleet acquisitions, with China, India, and Japan collectively accounting for more than 60% of the regional demand. Europe follows with 22% adoption, led by Germany and the UK, with extensive modular retrofit programs. South America and the Middle East & Africa collectively account for 10% market share, driven by regional defense upgrades and offshore support vessel maintenance. Regional differences in technology adoption, workforce skill levels, and regulatory standards create varied demand patterns, while sustainability initiatives are shaping maintenance practices globally.

How are advanced digital solutions reshaping vessel maintenance efficiency?

North America accounts for 34% of the Naval Vessel MRO market, with the U.S. Navy and Canadian naval forces driving demand. Key industries include defense, shipbuilding, and offshore support operations. Government initiatives such as the National Defense Authorization Act support fleet modernization and MRO funding. Technological advancements, including AI-driven predictive analytics and autonomous hull inspections, enhance operational efficiency. Huntington Ingalls Industries recently implemented an automated dry-dock scheduling system, reducing turnaround time by 18%. Regional adoption trends show higher enterprise uptake in naval and defense sectors, with over 45% of shipyards incorporating digital twin simulations and smart sensor networks for maintenance planning. North American operators prioritize readiness and uptime, focusing on lifecycle cost optimization.

What role do regulatory frameworks and sustainability drive operational decisions?

Europe holds a 22% share of the Naval Vessel MRO market, with Germany, the UK, and France leading regional adoption. Regulatory oversight by agencies such as the European Maritime Safety Agency encourages sustainable maintenance practices, including zero-discharge operations and green retrofits. Emerging technologies such as autonomous inspections, robotics-assisted repair, and additive manufacturing are increasingly deployed. BAE Systems in the UK has integrated AI-powered predictive maintenance across 50 vessels, improving operational availability by 15%. European consumer behavior is shaped by regulatory compliance priorities, leading shipyards to focus on explainable and environmentally compliant MRO services. Digitalization initiatives are accelerating fleet readiness and cost-efficient overhauls.

How are naval modernization programs influencing service demand?

Asia-Pacific accounts for 28% of the Naval Vessel MRO market, with China, India, and Japan as top-consuming countries. Regional infrastructure is rapidly expanding, with new shipyards and dry-dock facilities under construction in major ports. Technology adoption, including digital twin modeling, IoT-based hull monitoring, and modular retrofitting, is increasing. Local players such as Cochin Shipyard in India are implementing automated inspection systems, reducing dry-dock turnaround by 12%. Regional consumer behavior reflects accelerated adoption of predictive maintenance and modernization programs, driven by strategic fleet expansion and maritime security priorities. Asia-Pacific navies emphasize cost-efficient, technology-enabled maintenance solutions to sustain growing fleets.

What emerging factors are driving naval maintenance demand?

South America holds a 6% share of the Naval Vessel MRO market, with Brazil and Argentina as key contributors. Infrastructure expansion in shipyards, combined with increasing demand for offshore energy support vessels, drives MRO activities. Government incentives, including trade partnerships and defense upgrade funding, support regional fleet maintenance programs. Local players such as Enseada Indústria Naval in Brazil are adopting automated hull inspection systems to improve efficiency by 10%. Consumer behavior trends show that maintenance demand is closely tied to regional industrial activity and fleet modernization cycles, with defense operators prioritizing uptime and reliability.

How is regional modernization shaping naval service trends?

Middle East & Africa account for 4% of the Naval Vessel MRO market, with major growth in the UAE and South Africa. Regional demand is driven by naval fleet upgrades supporting oil & gas, maritime security, and construction operations. Technological modernization includes AI-based diagnostics, robotics-assisted hull inspection, and energy-efficient retrofits. Local players such as Abu Dhabi Ship Building have implemented automated dry-dock scheduling systems, reducing maintenance turnaround by 15%. Consumer behavior trends indicate strong adoption among defense and offshore support operators, with regional fleets emphasizing efficiency, sustainability, and operational readiness.

United States – 18% market share | High production capacity and advanced fleet maintenance infrastructure support extensive MRO operations.

China – 14% market share | Large-scale naval acquisitions and adoption of predictive maintenance technologies drive consistent demand.

The Naval Vessel MRO market is highly competitive and moderately fragmented, with over 120 active companies operating globally. The combined market share of the top five players—BAE Systems, General Dynamics, Huntington Ingalls Industries, Lockheed Martin, and Northrop Grumman—is approximately 38%, indicating that smaller regional and niche players collectively hold the majority of market influence. Companies are pursuing strategic initiatives such as joint ventures, facility expansions, and technology partnerships to strengthen positioning. For example, Huntington Ingalls Industries expanded its dry-dock facilities to handle 15% more vessels annually, while Lockheed Martin integrated AI-based diagnostics into fleet maintenance programs to reduce unplanned downtime by 22%. Innovation trends, including robotics-assisted inspections, predictive analytics, digital twin simulations, and eco-friendly retrofitting, are shaping competitive advantage. Regulatory compliance and defense budget allocations further influence strategic decision-making, with top players prioritizing sustainable and technologically advanced solutions. Market positioning is also determined by specialization in surface warship MRO, submarine overhauls, and support vessel maintenance. The competitive landscape favors companies capable of integrating advanced digital solutions, maintaining rapid turnaround, and supporting global naval operations with high operational efficiency.

Lockheed Martin Corporation

Northrop Grumman Corporation

Raytheon Technologies Corporation

Saab AB

Thales Group

Naval Group

Babcock International Group PLC

Kongsberg Maritime

Teledyne Brown Engineering

Vouvray Acquisition Limited

The Naval Vessel Maintenance, Repair, and Overhaul (MRO) market is undergoing a significant technological transformation, driven by advancements that enhance operational efficiency, reduce downtime, and extend the service life of naval assets. One of the most impactful developments is the integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance. These technologies analyze vast amounts of sensor data to forecast potential failures, allowing for timely interventions that prevent costly repairs and operational disruptions. Additionally, the Internet of Things (IoT) is playing a crucial role in the MRO landscape. IoT-enabled sensors are being deployed across various vessel components to monitor real-time performance metrics. This continuous data stream facilitates proactive maintenance strategies and provides valuable insights into the health of critical systems, thereby improving decision-making processes.

Robotics and automation are also making significant inroads into the MRO sector. Automated systems are now being utilized for tasks such as hull inspections, component replacements, and system calibrations. These robotic solutions not only enhance precision but also reduce human exposure to hazardous environments, thereby improving safety standards. Furthermore, Augmented Reality (AR) and Virtual Reality (VR) technologies are being employed for training and remote assistance. Technicians can now receive real-time guidance through AR interfaces, enabling them to perform complex repairs with greater accuracy. VR simulations are also being used to train personnel in a controlled environment, enhancing skill development without the risks associated with live training scenarios. These technological advancements are reshaping the Naval Vessel MRO market, leading to more efficient, cost-effective, and safer maintenance practices.

In March 2024, Hanwha Ocean completed extensive repairs on the USNS Wally Schirra, marking the first time a South Korean shipyard has undertaken such work for the US Navy. This collaboration underscores the growing reliance on Asian shipbuilding expertise to maintain naval readiness. Source: www.ft.com

In July 2023, the U.S. Navy awarded a contract to General Dynamics Electric Boat to perform a comprehensive overhaul of the USS Virginia-class submarine. The project aims to enhance the vessel's capabilities and extend its service life by an additional 15 years.

In October 2023, the Royal Navy initiated a modernization program for its Type 23 frigates, focusing on upgrading combat systems and propulsion units. The program is expected to extend the operational life of these vessels by at least 10 years.

In January 2024, the Indian Navy signed an agreement with Mazagon Dock Shipbuilders to undertake the mid-life upgrade of its Shivalik-class stealth frigates. The upgrade includes enhancements to weapon systems and sensors, aiming to bolster the fleet's operational effectiveness.

The Naval Vessel Maintenance, Repair, and Overhaul (MRO) market report provides a comprehensive analysis of the global MRO landscape, encompassing various vessel types, maintenance services, and technological advancements. The report delves into the segmentation of the market by vessel type, including surface combatants, submarines, and auxiliary vessels, highlighting the unique MRO requirements of each category. It also examines the different types of maintenance services, such as preventive maintenance, corrective maintenance, and overhaul services, detailing their significance in prolonging the operational life of naval vessels. The report further explores the integration of emerging technologies like Artificial Intelligence (AI), Internet of Things (IoT), and robotics in MRO processes, assessing their impact on efficiency and cost-effectiveness.

Geographically, the report covers key regions including North America, Europe, Asia-Pacific, and the Middle East & Africa, analyzing regional market dynamics, regulatory frameworks, and defense spending trends that influence MRO activities. It also identifies major players in the market, providing insights into their strategies, capabilities, and market positioning. Additionally, the report addresses the challenges and opportunities within the MRO sector, such as the aging naval fleet, the need for modernization, and the increasing demand for outsourcing MRO services. It concludes with future outlooks and strategic recommendations for stakeholders aiming to navigate the evolving MRO landscape effectively.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12400.89 Million |

|

Market Revenue in 2032 |

USD 19616.45 Million |

|

CAGR (2025 - 2032) |

5.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BAE Systems, General Dynamics, Huntington Ingalls Industries, Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, Saab AB, Thales Group, Naval Group, Babcock International Group PLC, Kongsberg Maritime, Teledyne Brown Engineering, Vouvray Acquisition Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |