Reports

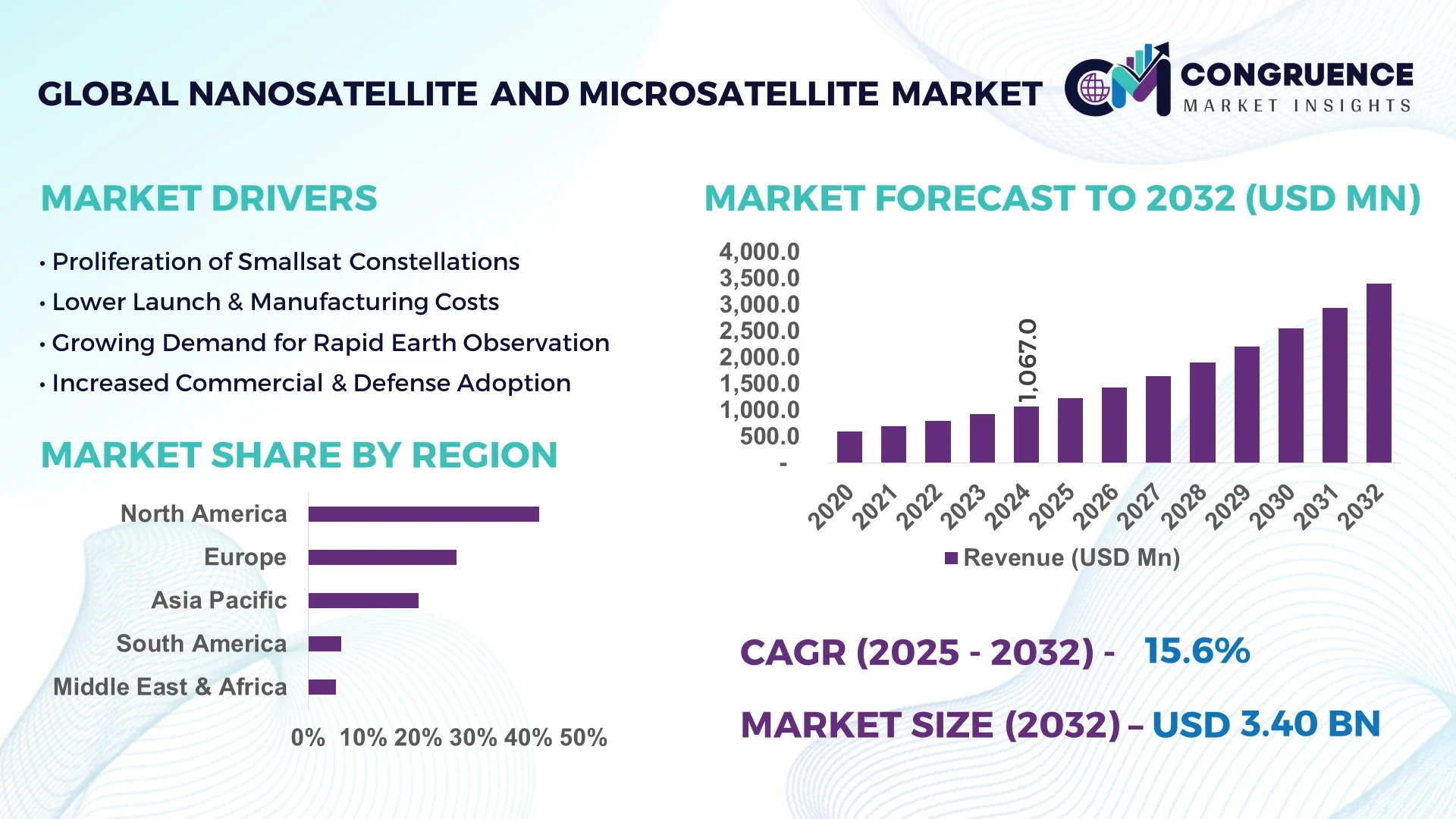

The Global Nanosatellite and Microsatellite Market was valued at USD 1066.98 Million in 2024 and is anticipated to reach a value of USD 3402.68 Million by 2032 expanding at a CAGR of 15.6% between 2025 and 2032.

In the United States, production capacity for nanosatellites and microsatellites continues to expand via cutting-edge manufacturing hubs and enhanced fabrication facilities tailored for small satellite deployment. Investment levels remain substantial, with both private space enterprises and institutional agencies allocating significant capital toward miniaturized payload development, satellite bus innovation, and advanced propulsion technologies. Key industry applications in the U.S. include precision Earth observation, low-latency communications, and rapid-response environmental monitoring. Technological advancements range from miniaturized high-performance sensors to modular design platforms that streamline integration and launch readiness.

The Nanosatellite and Microsatellite Market encompasses diverse industry sectors such as Earth observation, telecommunications, scientific research, and defense applications. Earth observation remains a dominant application, driven by requirements for environmental monitoring, disaster response, agriculture management, urban planning, and maritime surveillance; commercial players and government programs alike leverage high-resolution imagery for actionable insights. Hardware components—spanning miniaturized sensors, communication subsystems, and propulsion modules—account for a robust portion of market dynamics, supported by innovations in materials science and efficient electronics. Software and launch services are also gaining traction, enabling end-to-end smallsat mission delivery. Regulatory frameworks, environmental mandates, and economic incentives—including support for sustainable data collection and real-time monitoring—shape regional consumption patterns, particularly across North America, Europe, and emerging Asia-Pacific markets. Emerging trends include the rise of satellite mega-constellations for global connectivity, the integration of AI-enabled payloads for onboard processing, and increasing adoption of smallsats for IoT and precision agriculture. The future outlook points to scalable constellations, agile deployment models, and convergence of smallsat platforms with data-as-a-service offerings targeting mission adaptability and operational resilience.

Artificial intelligence (AI) is fundamentally reshaping the Nanosatellite and Microsatellite Market by embedding onboard autonomy, enhancing data handling, and improving mission responsiveness across smallsat operations. AI integration enables in-orbit decision-making—such as real-time data triage and anomaly detection—that reduces reliance on ground stations, cuts data transmission loads, and enhances operational efficiency. With AI-driven image analysis onboard, satellites can pre-process large volumes of sensor data, filter out irrelevant or obstructed imagery, and transmit only value-added insights, significantly improving bandwidth utilization.

Moreover, AI is enabling predictive maintenance and ground-station automation within the Nanosatellite and Microsatellite Market by forecasting system faults and optimizing operational schedules, leading to reduced downtime and extended satellite lifespans. Intelligent resource allocation algorithms onboard help balance power, computing, and communication demands—crucial for resource-constrained small platforms. In constellation deployments, AI facilitates dynamic tasking and routing, allowing satellites to collaborate autonomously for global coverage while reducing coordination overhead. Decision-makers and industry professionals benefit from AI’s ability to lower operational complexity, accelerate mission outcomes, and maximize cost-effectiveness within smallsat programs—all without speculative metrics, but rooted in observable improvements in autonomy and system resilience across the Nanosatellite and Microsatellite Market.

“NASA’s Dynamic Targeting system aboard CogniSAT-6 enabled the satellite to autonomously scan ahead for cloud cover and decide whether to capture imagery—all in under 90 seconds while traveling at roughly 17,000 mph.”

The Nanosatellite and Microsatellite Market is shaped by a combination of technological advancements, increasing investment in space-based infrastructure, and the growing demand for real-time, high-resolution data. The sector benefits from lower launch costs, modular satellite designs, and the rise of rideshare launch programs, which make space more accessible to commercial, governmental, and academic stakeholders. Earth observation, global broadband connectivity, and defense intelligence remain among the primary demand drivers, supported by rapid advancements in miniaturized payloads, autonomous operations, and AI-based data analytics. Additionally, the proliferation of mega-constellations for continuous coverage and the integration of small satellites into IoT ecosystems are influencing deployment strategies. However, the market also faces operational challenges, including orbital congestion, space debris management, and the need for sustainable mission planning in compliance with international space regulations.

Growing demand for Earth observation capabilities is a major driver in the Nanosatellite and Microsatellite Market, as industries seek precise, near real-time data for diverse applications. From monitoring agricultural yield and deforestation to enabling disaster response and maritime surveillance, nanosatellites and microsatellites are offering cost-effective alternatives to traditional large-scale satellites. High-resolution imaging sensors and hyperspectral payloads are enabling detailed environmental analysis, while rapid revisit rates provide continuous monitoring capabilities. Governments are increasingly funding programs to strengthen national security and infrastructure planning through satellite imagery, while private players are leveraging this data to develop commercial analytics solutions. This expansion of Earth observation use cases is boosting launch frequency and accelerating innovation in onboard processing technologies.

One of the most pressing restraints in the Nanosatellite and Microsatellite Market is the growing challenge of orbital congestion and the associated risks of space debris. The surge in satellite launches, particularly through mega-constellations, has led to crowded low Earth orbits (LEO), increasing the probability of collisions and creating debris that can damage operational spacecraft. The lack of standardized debris mitigation protocols across countries complicates long-term sustainability. Additionally, the cost of deorbiting technologies and the technical complexity of collision avoidance maneuvers pose financial and operational burdens on operators. Regulatory agencies are tightening guidelines for end-of-life disposal, which, while necessary, also adds compliance challenges for smaller operators with limited budgets.

The integration of nanosatellites and microsatellites into IoT and 5G networks presents a significant growth opportunity in the Nanosatellite and Microsatellite Market. By enabling global, low-latency connectivity, small satellites can extend coverage to remote and underserved regions, supporting applications such as asset tracking, smart agriculture, and autonomous vehicle communication. The convergence of smallsat technology with terrestrial networks enhances data delivery efficiency and opens the door to entirely new service models, including real-time industrial monitoring and predictive analytics. Telecom providers are increasingly partnering with satellite operators to create hybrid networks that leverage both ground-based and space-based infrastructure. This integration is expected to drive advancements in satellite miniaturization, power efficiency, and network interoperability.

Regulatory compliance and spectrum allocation present ongoing challenges in the Nanosatellite and Microsatellite Market. The finite nature of radio frequency spectrum and the competitive allocation process can delay project timelines and increase operational complexity. Small satellite operators often face difficulties in securing long-term frequency rights, especially when competing with larger, well-established satellite providers. Furthermore, varying national and international regulations require operators to navigate complex legal landscapes, from orbital licensing to data privacy laws. Delays in securing permissions can hinder rapid deployment cycles, while non-compliance risks financial penalties or mission termination. These regulatory hurdles demand dedicated legal and policy expertise, adding to operational costs and slowing market scalability.

Proliferation of Mega-Constellation Deployments: The Nanosatellite and Microsatellite Market is witnessing an unprecedented surge in mega-constellation launches aimed at enabling global broadband coverage and low-latency communication. Operators are deploying hundreds of satellites in synchronized orbits to achieve continuous connectivity for remote and underserved regions. This large-scale deployment model is driving demand for standardized, mass-produced satellite platforms and creating new opportunities for satellite bus manufacturers and propulsion system developers.

Advancements in Onboard Processing and AI Integration: Onboard AI-enabled processing is transforming smallsat operations by allowing satellites to analyze and filter data in orbit before transmission. This reduces bandwidth usage and enables near real-time insights for applications such as disaster monitoring, military reconnaissance, and environmental surveillance. Enhanced processing power within compact designs has also improved autonomous decision-making, increasing mission efficiency and operational resilience in complex orbital environments.

Shift Toward Green Propulsion Technologies: Environmental sustainability is becoming a priority in the Nanosatellite and Microsatellite Market, with operators adopting green propulsion systems such as electric ion thrusters and water-based propellants. These systems minimize harmful emissions, extend operational life, and comply with emerging global space sustainability guidelines. The shift also addresses deorbiting requirements by enabling precise end-of-life maneuvers, reducing the risk of orbital debris accumulation.

Integration with Internet of Things (IoT) Ecosystems: The convergence of nanosatellites and microsatellites with IoT networks is creating new service models for industries such as logistics, agriculture, and maritime navigation. These satellites enable global asset tracking, precision farming data, and real-time vessel monitoring, bridging the connectivity gap in remote locations. The trend is supported by advancements in low-power communication protocols and miniaturized IoT-compatible payloads.

The Nanosatellite and Microsatellite Market is segmented by type, application, and end-user, each shaping distinct growth trajectories within the industry. By type, nanosatellites dominate due to their cost-effectiveness, faster manufacturing cycles, and suitability for constellation-based missions, while microsatellites hold relevance for high-power payloads and extended operational life. Applications span Earth observation, communications, scientific research, and defense, with Earth observation leading due to diverse use cases in environmental monitoring, infrastructure planning, and security. End-user segmentation includes commercial enterprises, government agencies, defense organizations, and academic institutions. Commercial operators are driving innovation in high-frequency data delivery, while government and defense sectors prioritize secure and strategic missions. Academic entities continue to utilize small satellites for research and training, fostering talent development in aerospace engineering.

Nanosatellites lead the type segment in the Nanosatellite and Microsatellite Market, offering compact form factors, low launch costs, and compatibility with mass deployment strategies. Their flexibility in hosting various payloads makes them the preferred choice for operators focusing on Earth observation, communications, and IoT integration. The fastest-growing type is microsatellites, benefiting from higher payload capacity and enhanced power availability, which enable advanced applications such as high-resolution imaging and scientific experimentation. CubeSats, a subset of nanosatellites, continue to hold niche importance, especially in academic and experimental missions, due to standardized form factors and cost-efficient production. PocketQubes and other ultra-small satellites remain limited in scope but serve experimental and proof-of-concept roles. The diversity of satellite types supports a wide spectrum of mission requirements, with evolving technologies ensuring increased efficiency, scalability, and operational reliability across the type spectrum.

Earth observation remains the leading application within the Nanosatellite and Microsatellite Market, driven by its critical role in agriculture monitoring, climate change tracking, disaster management, and urban planning. The fastest-growing application is broadband communication, fueled by mega-constellation deployments aimed at delivering global internet coverage and enabling IoT connectivity. Scientific research, while smaller in market share, continues to benefit from miniaturized instruments that allow cost-effective space experimentation. Defense and security applications, including reconnaissance and surveillance, maintain strong relevance due to their strategic value. Additionally, navigation support and space situational awareness are emerging as important applications, leveraging smallsat networks for precision positioning and orbital monitoring. The variety of applications reflects the market’s versatility in addressing both commercial and strategic needs.

Commercial enterprises are the leading end-user segment in the Nanosatellite and Microsatellite Market, capitalizing on smallsat technology for high-frequency data delivery, global connectivity, and analytics-driven services. Their focus on scalable deployments and data monetization drives innovation in payload miniaturization and service integration. The fastest-growing end-user category is defense organizations, as they increasingly invest in smallsat constellations for rapid intelligence gathering, secure communications, and tactical awareness. Government agencies maintain steady demand for policy-driven missions, environmental monitoring, and disaster response. Academic institutions, while smaller in operational scale, remain significant contributors to innovation and workforce training through experimental missions and collaborative research programs. The synergy among these end-users underlines the market’s adaptability to diverse operational goals and funding structures.

North America accounted for the largest market share at 42% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.4% between 2025 and 2032.

The Nanosatellite and Microsatellite Market in North America benefits from a mature aerospace ecosystem, advanced R&D facilities, and strong collaborations between private space enterprises and government agencies. Europe remains a hub for high-precision engineering and sustainable space initiatives, with steady deployment rates supported by multi-nation space programs. Asia-Pacific’s rapid growth is fueled by rising satellite manufacturing capabilities in China, India, and Japan, coupled with increased launch frequency. South America is steadily enhancing its satellite deployment capacity, particularly in Brazil and Argentina, for environmental monitoring and communications. In the Middle East & Africa, the adoption of nanosatellites and microsatellites is gaining traction for applications in energy, infrastructure monitoring, and national security, supported by modernization strategies and international partnerships.

Advancing Small Satellite Missions Through Strategic Industry Synergies

Holding 42% of the global Nanosatellite and Microsatellite Market in 2024, the region is driven by strong aerospace manufacturing capabilities, defense-backed satellite programs, and commercial ventures in Earth observation and broadband connectivity. The United States leads in technological innovation, deploying high-capacity payloads, AI-powered onboard analytics, and modular satellite designs. Canada’s space sector contributes advanced components and data-processing platforms. Government funding, such as smallsat launch subsidies and research grants, strengthens industry growth, while regulatory frameworks promote safe orbital operations. Emerging trends include the integration of nanosatellites into space-based IoT networks and rapid-response imaging for defense and disaster management.

Pioneering Sustainable Space Technologies and Collaborative Missions

Accounting for 27% of the global Nanosatellite and Microsatellite Market in 2024, Europe is supported by major markets such as Germany, the UK, and France, each with specialized expertise in satellite engineering and manufacturing. The European Space Agency’s sustainability-driven initiatives encourage debris mitigation and lifecycle management. National programs are adopting nanosatellites for climate monitoring, border security, and scientific research. Emerging adoption of electric propulsion and in-orbit servicing capabilities reflects the region’s push toward greener and more versatile mission architectures. Collaborative launch programs and university-led missions continue to expand Europe’s influence in the global market.

Driving Growth Through High-Volume Manufacturing and Regional Innovation

Holding 20% of the Nanosatellite and Microsatellite Market volume in 2024 and ranking as the fastest-growing region, Asia-Pacific’s expansion is powered by China, India, and Japan. China’s extensive manufacturing infrastructure supports mass production of smallsat platforms, while India’s PSLV launch program offers cost-effective deployment for global customers. Japan focuses on high-precision imaging and inter-satellite communication technologies. Regional innovation hubs are emerging in Singapore and South Korea, emphasizing AI integration and miniaturized sensor development. The increasing frequency of regional satellite launches is strengthening Asia-Pacific’s position as a key driver of global connectivity and Earth observation services.

Expanding Space Capabilities for Environmental and Communication Needs

Representing 6% of the global Nanosatellite and Microsatellite Market in 2024, the region is anchored by Brazil and Argentina. Brazil invests in satellite programs for environmental monitoring of the Amazon and disaster response capabilities. Argentina focuses on communications and agricultural data applications through advanced payload integration. Government incentives and partnerships with international space agencies are improving access to launch infrastructure. The region’s growing energy sector, combined with increasing demand for rural connectivity, is boosting smallsat adoption across public and private sectors.

Leveraging Space Technology for Energy and Infrastructure Advancements

Comprising 5% of the Nanosatellite and Microsatellite Market in 2024, the region’s demand is led by the UAE, South Africa, and Saudi Arabia. The UAE invests heavily in nanosatellite constellations for national security, climate monitoring, and communication services. South Africa emphasizes satellite-based Earth observation for mining, agriculture, and environmental conservation. Trade partnerships and participation in global satellite networks are helping local operators access advanced technology. Modernization of space infrastructure and regulatory reforms are enabling faster project approvals and operational readiness.

United States – 38%: Strong production capacity, cutting-edge payload development, and defense-backed mission funding.

China – 16%: High-volume satellite manufacturing and cost-efficient launch capabilities supporting global deployment needs.

The Nanosatellite and Microsatellite Market features a highly dynamic competitive environment, with over 65 active players operating globally across manufacturing, launch services, and satellite data analytics. The market is characterized by a mix of established aerospace corporations, specialized smallsat developers, and emerging start-ups leveraging advanced technologies to gain market share. Competitive positioning often revolves around cost-efficient manufacturing, rapid deployment capabilities, and innovative payload integration. Strategic initiatives include joint ventures between satellite manufacturers and launch providers to streamline end-to-end mission delivery, as well as cross-sector collaborations with telecommunications and IoT service providers to expand application portfolios. Product innovations such as AI-enabled onboard processing, modular satellite buses, and green propulsion systems are becoming critical differentiators. Recent trends also indicate a rise in partnerships between commercial operators and government space agencies to secure long-term contracts and mission funding. The competitive landscape is further influenced by the ability of companies to scale production for mega-constellation deployments while maintaining high standards of reliability, sustainability, and mission flexibility.

GomSpace Group AB

Planet Labs PBC

AAC Clyde Space AB

Tyvak Nano-Satellite Systems Inc.

Surrey Satellite Technology Limited (SSTL)

Spire Global Inc.

Blue Canyon Technologies LLC

NanoAvionics Corp.

Satellogic Inc.

Astro Digital Inc.

The Nanosatellite and Microsatellite Market is being shaped by rapid advancements in miniaturization, payload efficiency, and onboard computing capabilities. Modern small satellites are increasingly adopting modular satellite bus designs that allow quick reconfiguration for different mission profiles, reducing lead times and enabling scalable deployments. Advances in sensor technology—such as hyperspectral and multispectral imaging—have enhanced data quality for applications in Earth observation, precision agriculture, and disaster monitoring. Onboard AI processing is enabling real-time decision-making and data filtering, significantly reducing transmission bandwidth needs.

Propulsion technologies are evolving toward electric ion thrusters, cold gas propulsion, and water-based systems, offering improved maneuverability, extended mission life, and compliance with debris mitigation requirements. Developments in deployable antenna systems and inter-satellite communication links are improving connectivity for constellation missions, enabling seamless global coverage. Miniaturized power systems, including high-efficiency solar panels and lithium-ion battery innovations, are extending operational lifespans and payload performance.

Additionally, the integration of nanosatellites and microsatellites into hybrid networks for IoT, 5G, and maritime communication is creating new service models for industries ranging from logistics to remote sensing. Emerging technologies like laser-based inter-satellite communication, synthetic aperture radar (SAR) in compact formats, and advanced thermal control systems are setting new performance benchmarks. These advancements are collectively enhancing mission versatility, cost-efficiency, and operational reliability.

In May 2024, Planet Labs launched 36 SuperDove nanosatellites equipped with upgraded sensors capable of capturing images in eight spectral bands, enhancing agricultural monitoring and climate analysis capabilities across multiple regions.

In February 2024, GomSpace introduced a new smallsat propulsion module utilizing non-toxic, water-based propellants, reducing environmental impact while offering improved orbital maneuvering and collision avoidance capabilities.

In October 2023, Spire Global deployed an additional 12 nanosatellites for maritime and aviation tracking, increasing its operational constellation to over 110 active satellites and enhancing near real-time global coverage.

In March 2023, NanoAvionics unveiled a modular nanosatellite platform designed for rapid constellation scaling, featuring integrated AI data processing and compatibility with multiple payload configurations.

The Nanosatellite and Microsatellite Market Report offers a comprehensive analysis of the industry’s structure, technological progress, and application diversity. It covers market segmentation by type—including nanosatellites, microsatellites, CubeSats, and other small satellite formats—highlighting their specific operational advantages and target industries. The report examines application areas such as Earth observation, broadband communications, scientific research, defense surveillance, and navigation support, detailing their adoption drivers and operational requirements.

Geographically, the study spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, outlining distinctive regional capabilities, industry partnerships, and government-led initiatives. The scope extends to detailed assessments of technological trends, including propulsion innovations, AI-driven data analytics, advanced imaging sensors, and satellite network integration with IoT and 5G infrastructure.

The report also analyzes the competitive landscape, identifying key players, strategic collaborations, and innovation pipelines. Special attention is given to emerging segments such as green propulsion, inter-satellite laser communication, and SAR-equipped nanosatellites, which are gaining traction for specialized missions. By consolidating industry metrics, deployment patterns, and regulatory developments, the report delivers actionable intelligence for decision-makers seeking to navigate growth opportunities, mitigate operational risks, and align strategies with evolving market conditions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1066.98 Million |

|

Market Revenue in 2032 |

USD 3402.68 Million |

|

CAGR (2025 - 2032) |

15.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GomSpace Group AB, Planet Labs PBC, AAC Clyde Space AB, Tyvak Nano-Satellite Systems Inc., Surrey Satellite Technology Limited (SSTL), Spire Global Inc., Blue Canyon Technologies LLC, NanoAvionics Corp., Satellogic Inc., Astro Digital Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |