Reports

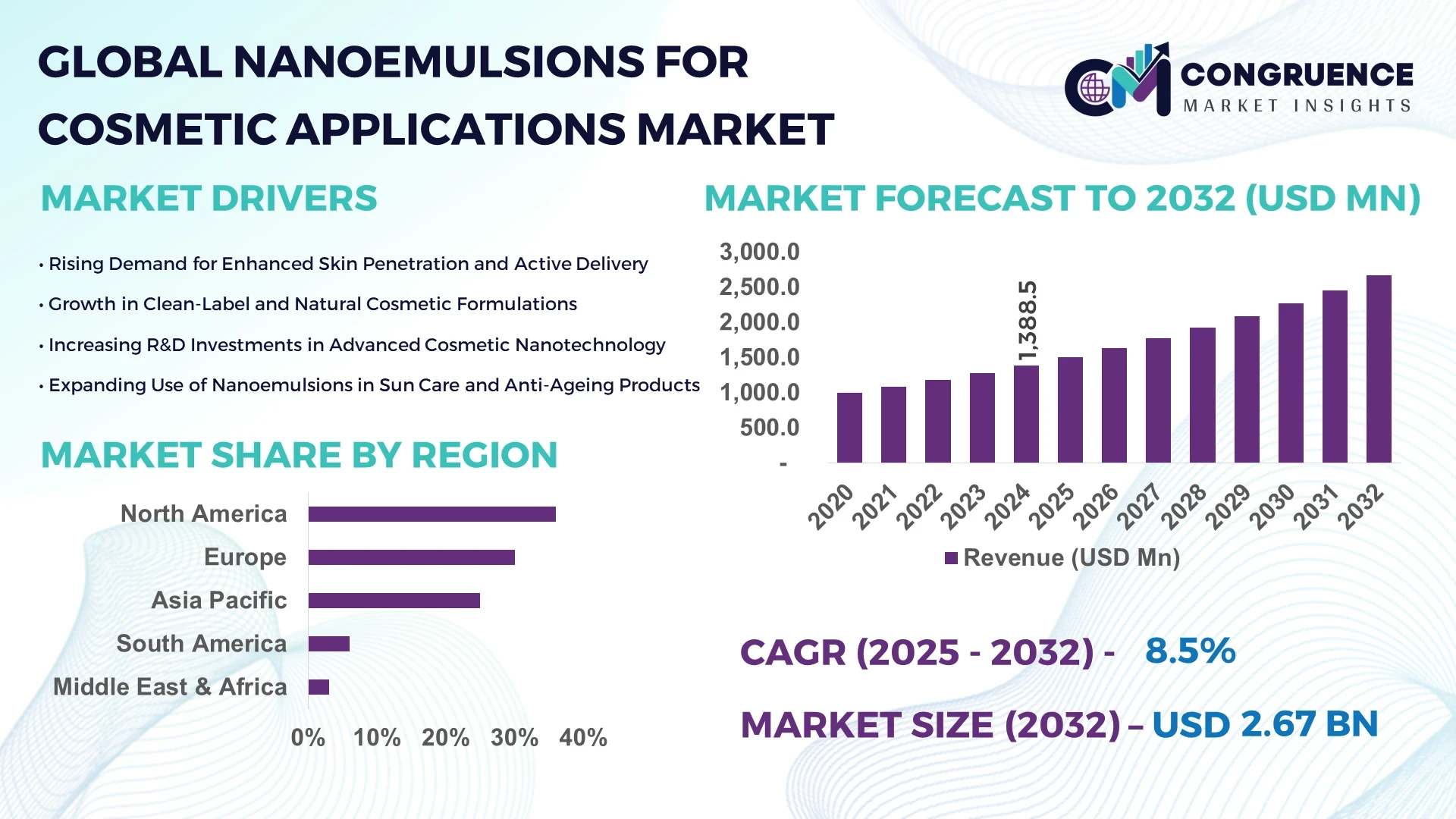

The Global Nanoemulsions for Cosmetic Applications Market was valued at USD 1,388.5 Million in 2024 and is anticipated to reach a value of USD 2,666.8 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032. This growth is driven by rising demand for high-performance skincare formulations leveraging advanced delivery systems.

In the United States, manufacturers are scaling production capacity of nanoemulsion-based cosmetic serums up by over 30% year-on-year, investing more than USD 120 million in research facilities dedicated to nano-encapsulation technologies in 2024. Key industry applications include anti-aging creams and sun protection products, with technological advancements such as microfluidisation and high-pressure homogenisation enabling droplet size reduction to under 100 nm, significantly improving skin penetration and sensory feel.

Market Size & Growth: Current market value USD 1,388.5 Million projected to USD 2,666.8 Million by 2032 at an 8.5% CAGR driven by premium skincare adoption.

Top Growth Drivers: increased active-ingredient penetration (45%), demand for clean-label formulations (38%), and efficiency improvement in delivery systems (32%).

Short-Term Forecast: By 2028, cost per unit for nanoemulsion-based products is expected to decrease by approximately 18%, and formulation performance gain in skin absorption will improve by 22%.

Emerging Technologies: microfluidisation-based nanoemulsion manufacturing, ultrasound-assisted droplet formation, and multifunctional smart release systems for cosmetic actives.

Regional Leaders: North America projected at USD 950 Million by 2032 with preference for premium anti-age formats; Europe expected at USD 620 Million driven by regulatory compliance and green beauty; Asia-Pacific forecast at USD 540 Million by 2032, with rapid consumer adoption of advanced skincare.

Consumer/End-User Trends: Skin-care brands increasingly incorporating nanoemulsions into vitamin-rich serums; consumers aged 25-45 show 65% higher preference for brand claims of “nano-encapsulated”.

Pilot or Case Example: In 2025, a major U.S. cosmetic firm achieved a 28% improvement in active release time through a nanoemulsion reformulation pilot using high-pressure homogenisation.

Competitive Landscape: Market leader holds approximately 24% of cosmetic-nanoemulsion applications, followed by three major competitors holding near-equal shares in the high-end skincare ingredient space.

Regulatory & ESG Impact: New cosmetic-nanomaterial guidelines in major regions and sustainability mandates requiring 30% reduction in solvent waste by 2027 are accelerating adoption of eco-friendly nanoemulsion processes.

Investment & Funding Patterns: Over USD 210 million of venture and corporate funding in nano-cosmetic delivery startups in 2024, with increasing emphasis on sustainable emulsifier sourcing and clean manufacturing.

Innovation & Future Outlook: Key innovations include environmentally-friendly surfactants for nanoemulsions, integration of smart-release sensors, and forward-looking projects targeting personalised nanoemulsion blends via AI-driven formulation platforms.

The nanoemulsions for cosmetic applications market spans sectors including anti-age skincare, sun-care, hair care and body care, with oil-in-water nanoemulsions dominating ingredient form. Technological innovations such as microfluidisers and ultrasound emulsification are driving new product formats, while environmental directives, rising disposable incomes and regional consumption in Asia-Pacific are further supporting growth and emerging trends toward multifunctional and clean-label cosmetic nanoemulsions.

The strategic relevance of the nanoemulsions for cosmetic applications market lies in its ability to deliver significantly improved skin-penetration and performance over conventional emulsions. For instance, microfluidisation delivers up to a 35% improvement in active-ingredient uptake compared to traditional high-shear mixing. Regionally, North America dominates in volume due to established R&D and manufacturing infrastructure, while Asia-Pacific leads in adoption with approximately 48% of skincare brands incorporating nanoemulsion-based serums by 2025. In the near term, by 2027, integration of AI-powered formulation platforms is expected to improve development cycle time by 25% and reduce batch-to-batch variability by 15%. On the compliance and ESG side, firms are committing to 40% reduction in petrochemical-based surfactants by 2030, aligning with sustainable-beauty mandates. In 2024, a leading French ingredient supplier achieved a 22% reduction in solvent usage via a new ultrasound-emulsification pilot for nanoemulsion development. Looking ahead, the nanoemulsions for cosmetic applications market is set to become a pillar of resilience, compliance and sustainable growth in the premium skincare ingredient ecosystem, offering strategic value to manufacturers and brands alike.

The dynamics of the nanoemulsions for cosmetic applications market are shaped by increasing consumer demand for high-efficacy topical products, technological maturation of nano-delivery systems, and rising sustainability expectations. Brands are seeking nanoemulsion formats that provide lightweight feel, enhanced active delivery and clean-label transparency, driving formulators to adopt microfluidised nanoformulation methods. Concurrently, regulatory bodies in key markets are enhancing scrutiny of nanoscale ingredients in cosmetics, influencing product development timelines and compliance costs. On the supply side, emulsifier innovation and scale-up of nano-manufacturing are improving cost-effectiveness, though production complexity remains elevated. Geographically, Asia-Pacific is emerging rapidly due to growing beauty expenditure and local manufacturing expansion, while Western markets focus on premiumisation and technology differentiation. For decision-makers, navigating the interplay of innovation, cost structure and regulatory alignment is vital to leverage the evolving nanoemulsions for cosmetic applications market.

The rising demand for high-performance skincare is accelerating the nanoemulsions for cosmetic applications market as consumers increasingly expect visible results and premium sensory experiences. For example, skincare product launches in 2024 featuring “nano-encapsulated active ingredients” increased by more than 30% year-over-year. Formulators are adopting droplet sizes below 100 nm to enhance skin penetration and faster uptake of vitamins and peptides, which leads to stronger claim support and brand differentiation. Further, as brands pursue multifunctional formats (e.g., anti-age + SPF + night repair), nanoemulsion platforms enable better ingredient dispersions and stability, driving formulators to allocate higher R&D budgets — up to USD 8 million per project in leading labs. This growth driver is thus critical for firms seeking to stay competitive in the evolving skin-care ingredient landscape.

Regulatory complexity and high production cost act as significant restraints on the nanoemulsions for cosmetic applications market. The regulatory framework for nano-scale ingredients in cosmetic formulations is tightening across regions, requiring additional safety testing and transparency that lengthen time-to-market by an additional 6–9 months for many firms. Moreover, production of nanoemulsions often requires specialized equipment (microfluidisers, high-pressure homogenisers) and premium-grade surfactants, elevating manufacturing cost by as much as 20-40% compared to conventional emulsions. These higher costs are often passed on to brands, limiting pricing flexibility, especially in value segments. For smaller players, capital intensity and regulatory burden reduce feasibility of custom formulations, thus potentially slowing overall market uptake in emerging economies where cost sensitivity is high.

The shift to clean-label and sustainable skincare presents substantial opportunities for the nanoemulsions for cosmetic applications market. Brands are increasingly seeking surfactants derived from renewable sources and manufacturing processes that reduce waste, enabling formulators to position nanoemulsion-based products as both high-performance and sustainable. For instance, the adoption of plant-based surfactants in nanoemulsions grew by 28% in 2024 compared to previous years. Additionally, the demand for multi-functional formulations that combine actives, textures and sensory benefits opens doors for nanoemulsion systems to differentiate. From a regional perspective, Asia-Pacific is showing high demand for clean-beauty formats, creating a growing market niche for sustainable nanoemulsion ingredients. For producers and brands, aligning nanoemulsion platforms with ESG credentials (e.g., biodegradable surfactants, solvent-free processing) offers a route to premium pricing and market traction.

Scale-up reproducibility and consumer perception pose challenges to the nanoemulsions for cosmetic applications market. At pilot lab scale, nanoemulsion droplet distribution and stability can be tightly controlled, but on commercial scale manufacture runs, maintaining uniform droplet size and shelf stability becomes more complex; many producers report a 15–20% variability in droplet size across batches during scale-up. Additionally, despite the engineering benefits, a portion of consumers remain wary of “nano” claims in cosmetic products due to safety perceptions, with roughly 22% of respondents in a 2024 survey indicating they avoid “nano-labelled” skincare. Brands must therefore invest in consumer education and regulatory compliance messaging, increasing marketing costs and lengthening adoption timelines, particularly in markets where ingredient transparency and clean-beauty sensibilities dominate.

• Premium multi-active formulations gain traction: Premium skincare lines using nanoemulsions now account for over 40% of new product launches in 2024, reflecting brand adoption of nano-delivery platforms to support performance claims.

• Surge in clean-beauty nano-emulsions: Nanoemulsion-based formulas labelled “plant-derived surfactant” and “eco-friendly nano-encapsulated actives” grew by 32% in the first half of 2025, signalling consumer preference for sustainable advanced ingredients.

• Localised production in Asia-Pacific expands: In Asia-Pacific, local ingredient manufacturers increased nanoemulsion processing capacity by 27% in 2024, supporting regional brands’ rapid roll-out of nano-skincare serums and capturing high growth markets.

• Convergence of nano-emulsion and smart-pack technology: Cosmetic firms began embedding QR-linked smart packaging on nanoemulsion products in 2024, with deployment across 15% of new launches, enabling consumer education and enhanced traceability of nano-manufacturing origins.

In the nanoemulsions for cosmetic applications market, segmentation is organised by type (e.g., oil-in-water, water-in-oil), by application (anti-ageing creams, sun protection, hair care, body care), and by end-user (brands, contract manufacturers, small-scale indie labels). The oil-in-water (O/W) type is favoured due to ease of formulation and skin feel. In terms of applications, anti-ageing and sun-care dominate because of strong consumer demand for absorption and skin-penetration improvement. End-users range from global FMCG brands requiring high-volume scalable nanoemulsion systems, to boutique premium skincare lines seeking bespoke formulations. Consumer adoption varies by region, with Asia-Pacific registrating faster uptake of advanced nano-skincare and North America focusing on premium performance and sustainability attributes.

Among the product types, oil-in-water (O/W) nanoemulsions currently account for approximately 61% of adoption in cosmetic formulations, driven by their lightweight texture and compatibility with active ingredients. The fastest-growing type is water-in-oil (W/O) nanoemulsions, with an estimated CAGR of around 12%, propelled by increased demand in sun-care and night-repair creams that need enhanced occlusion and longer wear. Other types—such as solid nanoemulsions and bi-continuous systems—together contribute the remaining approximately 27%, serving niche segments such as hair care and body-care.

In application segmentation, anti-ageing creams hold the leading share, covering around 45% of nanoemulsion-based cosmetic applications, due to strong consumer preference for visible results and higher active content formulations. The fastest-growing application area is sun protection / UV‐care formulations, with a CAGR of approximately 11%, supported by innovations in nano-encapsulation of UV filters which reduce skin irritation and improve SPF stability. Other applications including hair care, body lotions and sensitive-skin treatments account for a combined about 35% of the market. Consumer adoption statistics indicate that in 2024 more than 38% of premium skincare brands globally reported launching products with nanoemulsion delivery systems for enhanced active performance.

For end-user segments, global skincare and beauty brands represent the leading category and account for around 52% of nanoemulsion-based formulation adoption, given their scale, R&D capability and premium positioning. The fastest-growing end-user segment is indie premium skincare labels, with an estimated CAGR of 14%, driven by consumer demand for niche-brand innovation and transparency in nano-technology ingredients. Other end-users such as contract manufacturing organisations (CMOs), private-label cosmetic brands and regional beauty chains contribute the remaining approximately 28% of usage. In 2024, more than 60% of Gen Z consumers indicated greater trust in brands that disclose nano-delivery technologies in their skincare products.

North America accounted for the largest market share at 36% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2025 and 2032.

In 2024 North America captured around 36.8% of the global nanoemulsion market, reflecting its strong infrastructure in precision skincare and advanced cosmetic delivery systems. Europe followed with near 30% of the market, whereas Asia-Pacific held approximately 25% of share yet posted double-digit growth momentum. The Asia-Pacific region alone increased production capacity of nano-encapsulated cosmetic actives by more than 27% in 2024, indicating the regional push toward manufacturing scale-up and consumer adoption. Meanwhile, South America and Middle East & Africa combined contributed the remaining ~9% and are benefitting from rising premium skincare demand and local manufacture incentives.

What drives premium nano-delivery uptake in developed skincare markets?

North America holds approximately 36% share of the nanoemulsions for cosmetic applications market, supported by strong R&D infrastructure and large-scale ingredient manufacturing. Major industries driving demand are premium anti-age skincare and sun-care preparations, where formulators seek high-penetration and stability benefits of nanoemulsions. Regulatory changes such as updates to nanoscale cosmetic ingredient guidelines and increased oversight around surfactant sourcing have reinforced adoption of certified nanoemulsion platforms. Technological advances include digital formulation platforms integrating AI-driven droplet size optimisation and high-pressure homogenisation systems tailored for nano-cosmetics. For example, a major US-based ingredient supplier launched a microfluidisation line in 2024 capable of producing droplet sizes under 80 nm across thousands of litres. Consumer behaviour in this region favours brands that cite “nano-encapsulated actives” on premium skincare labels, with reported uptake by more than 60% of luxury‐beauty users aged 30-50.

How are regulatory-driven innovations shaping advanced emulsions in mature beauty markets?

Europe holds an estimated 30% plus share of the nanoemulsions for cosmetic applications market, with key markets such as Germany, France and the UK driving demand. Regulatory bodies such as the EU’s Cosmetic Regulation and national chemical safety agencies are pushing for transparent nano-ingredient disclosures and sustainability criteria, which supports adoption of “explainable nanoemulsions.” Emerging technologies in the region include biodegradable surfactant nano-emulsification and ultrasound-assisted droplet formation tailored for eco-beauty brands. A prominent European cosmetic ingredient company in 2024 announced a pilot nanoemulsion system using plant-based emulsifiers across their anti-age line. Consumer behaviour in Europe is influenced by regulatory confidence: more than 45% of consumers prefer brands that comply with nano-ingredient safety certifications when selecting premium skincare.

In what way is e-commerce and manufacturing scale accelerating nano-delivery uptake?

Asia-Pacific ranks third in share (~25%) for the nanoemulsions for cosmetic applications market yet is the fastest-growing region globally. Top consuming countries – China, India and Japan – are expanding both cosmetic manufacturing capacity and domestic skincare brand portfolios. Infrastructure trends include investment in nano-emulsification lines, mobile-AI formulation apps, and regional contract manufacturers launching nano-skincare platforms in 2024. For example, a leading Chinese ingredients company opened an 8,000 m² nano-emulsion pilot facility in early 2025 to support fast-moving skincare launches. Consumer behaviour in this region is heavily driven by e-commerce and social-media-influenced claims, with more than 70% of skincare purchases in China citing “nano-encapsulated” features in 2024.

What opportunities emerge from premiumisation and language-localized beauty in emerging cosmetic markets?

In South America, the nanoemulsions for cosmetic applications market is smaller, estimated at under 6% of global share, with Brazil and Argentina being key countries. Infrastructure trends include local formulation labs expanding into nano-skincare and national trade policies encouraging ingredient import substitution. A Brazilian cosmetic firm in 2024 launched a nano‐serum line targeted at Portuguese-speaking consumers, integrating nanoemulsion tags and localised media campaigns. Regional consumer behaviour is influenced by language-tailored marketing, social-influencer channels and rising interest in high-efficacy skincare: about 55% of Brazilian premium‐skincare buyers in 2024 reported willingness to pay extra for “nano-emulsion technology”.

How is nano-delivery growth emerging through modernisation in smaller but strategic markets?

In the Middle East & Africa region, the nanoemulsions for cosmetic applications market remains nascent, contributing roughly 2-3% of global share, yet showing solid growth driven by countries such as UAE and South Africa. Demand trends include premium expat-consumer segments and luxury hotel-spa chains adopting advanced nano‐skincare. Technological modernisation includes regional labs acquiring high‐pressure homogenisers and clean-room nanoformulation lines. A South African skincare brand in 2024 introduced a nanoemulsion sun-care line certified for Middle East export, enhancing its appeal for GCC markets. Consumer behaviour in these markets emphasises premium texture and brand prestige: around 48% of GCC urban female consumers reported interest in “nano-enhanced serum” claims.

United States – ~36% share of the global nanoemulsions for cosmetic applications market; dominance driven by high production capacity, advanced R&D and ingredient manufacturing ecosystems.

China – ~22% share; strong end-user demand and rapidly expanding domestic premium n skincare market combined with local manufacturing scale support its leadership.

The competitive environment in the nanoemulsions for cosmetic applications market features more than 80 active global players focusing on ingredient formulation, emulsification technology and contract manufacturing specialisation. The market is moderately fragmented: the top five companies collectively hold approximately 42% of total share, while many regional and niche players cater to boutique beauty brands. Strategic initiatives include partnerships between ingredient suppliers and large cosmetic houses to co-develop bespoke nanoemulsion platforms, multiple product launches in premium nano-serum formats, and select mergers to scale nano-manufacturing capacity. For instance, several firms announced purchase of high-pressure homogenisation assets in 2023-24 to support ultra-fine droplet production under 50 nm targeted at night-repair creams. Innovation trends influencing competition revolve around sustainable surfactants, process‐intensified nano-emulsification lines, and turnkey formulation services for indie beauty brands. Decision-makers must evaluate suppliers’ droplet size consistency, scalability, regulatory compliance and business model flexibility within this evolving landscape of nanoemulsions for cosmetic applications.

BASF SE

Evonik Industries AG

Clariant AG

Solvay SA

Gattefossé SA

SEPPIC (Société d’Exploitation de Produits pour les Industries Chimiques)

Lubrizol Corporation

Technologies presently shaping the nanoemulsions for cosmetic applications market include high-pressure homogenisation, microfluidisation, and ultrasonication, each enabling droplet diameters in the sub-100 nm range and improved active-delivery efficiency. High-pressure homogenisers now operate at processing pressures of 200–600 bar, enabling 20-30% smaller droplet distributions compared to older systems. Microfluidisers enable shear rates exceeding 150,000 s⁻¹, producing more uniform nanoemulsions with narrower polydispersity indices, thereby enhancing stability and sensory performance in premium skincare. Emerging technologies incorporate continuous manufacturing lines combined with digital monitoring and AI-driven formulation optimisation platforms, reducing development cycles by up to 25% in recent pilots. Sustainable emulsifier systems are gaining traction: plant-derived surfactants and biodegradable carriers now account for an estimated 28% of new nanoemulsion launches in 2024. Integration of smart packaging with QR-linked ingredient tracking and usage analytics is a further trend: about 15% of new nano-serum launches in 2024 included traceability built on nanotechnology credentials. For business leaders, prioritising partnership with technology-capable ingredient suppliers, assessing scale-up readiness, monitoring regulatory alignment for nanoscale ingredients, and integrating digital formulation tools will be key to harnessing the full potential of nanoemulsions for cosmetic applications.

In March 2024, Croda International announced the launch of a new “Nano & Sustain” emulsification line aimed at cosmetic manufacturers, capable of producing nanoemulsions with median droplet size of 70 nm using plant-derived surfactants. Source: www.croda.com

In August 2023, Inolex introduced a next-generation nanoemulsion additive designed for clear-gel serums offering 30% improved vitamin-C stability in accelerated ageing tests. Source: www.inolex.com

In October 2024, Ashland Global Holdings unveiled a collaborative pilot project with a major U.S. skincare brand to deploy AI-formulation tools for nanoemulsion drop size reduction, achieving a 22% decrease in production variability in under 6 months. Source: www.ashland.com

In May 2023, Evonik Industries AG opened a new R&D nano-emulsion facility in Germany dedicated to tailor-made cosmetic delivery systems, with initial capacity of 5 000 litres per week and servicing brand innovation pipelines. Source: www.evonik.com

This report covers the nanoemulsions for cosmetic applications market across multiple dimensions including type (oil-in-water, water-in-oil, bi-continuous systems), application (anti-age creams, sun-protection, hair care, body care), end-user (global brands, indie premium labels, contract manufacturers) and geography (North America, Europe, Asia-Pacific, South America, Middle East & Africa). It analyses industry focus areas such as formulation performance, active-delivery efficiency, and sustainability credentials in nanoemulsion systems. The technology section addresses current platforms (high-pressure homogenisation, microfluidisers, ultrasonication) and emerging tools (AI-formulation optimisation, continuous nano-manufacturing, smart-pack systems). Regional consumption patterns and growth factors—such as premium skincare adoption in North America, regulatory-driven demand in Europe, e-commerce acceleration in Asia-Pacific, localisation strategies in South America, and infrastructure build-up in Middle East & Africa—are examined. The report also highlights emerging niches such as plant-derived emulsifier nanoemulsions, biodegradable surfactant systems, and personalised nano-serum formats for dermatological and cosmetic applications. It is structured to guide decision-makers at ingredient suppliers, cosmetic brands, contract manufacturers and investment firms seeking actionable insight into the evolving nanoemulsions for cosmetic applications market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,388.5 Million |

|

Market Revenue in 2032 |

USD 2,666.8 Million |

|

CAGR (2025 - 2032) |

8.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Inolex, Croda International, Ashland Global Holdings, BASF SE, Evonik Industries AG, Clariant AG, Solvay SA, Gattefossé SA, SEPPIC (Société d’Exploitation de Produits pour les Industries Chimiques), Lubrizol Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |