Reports

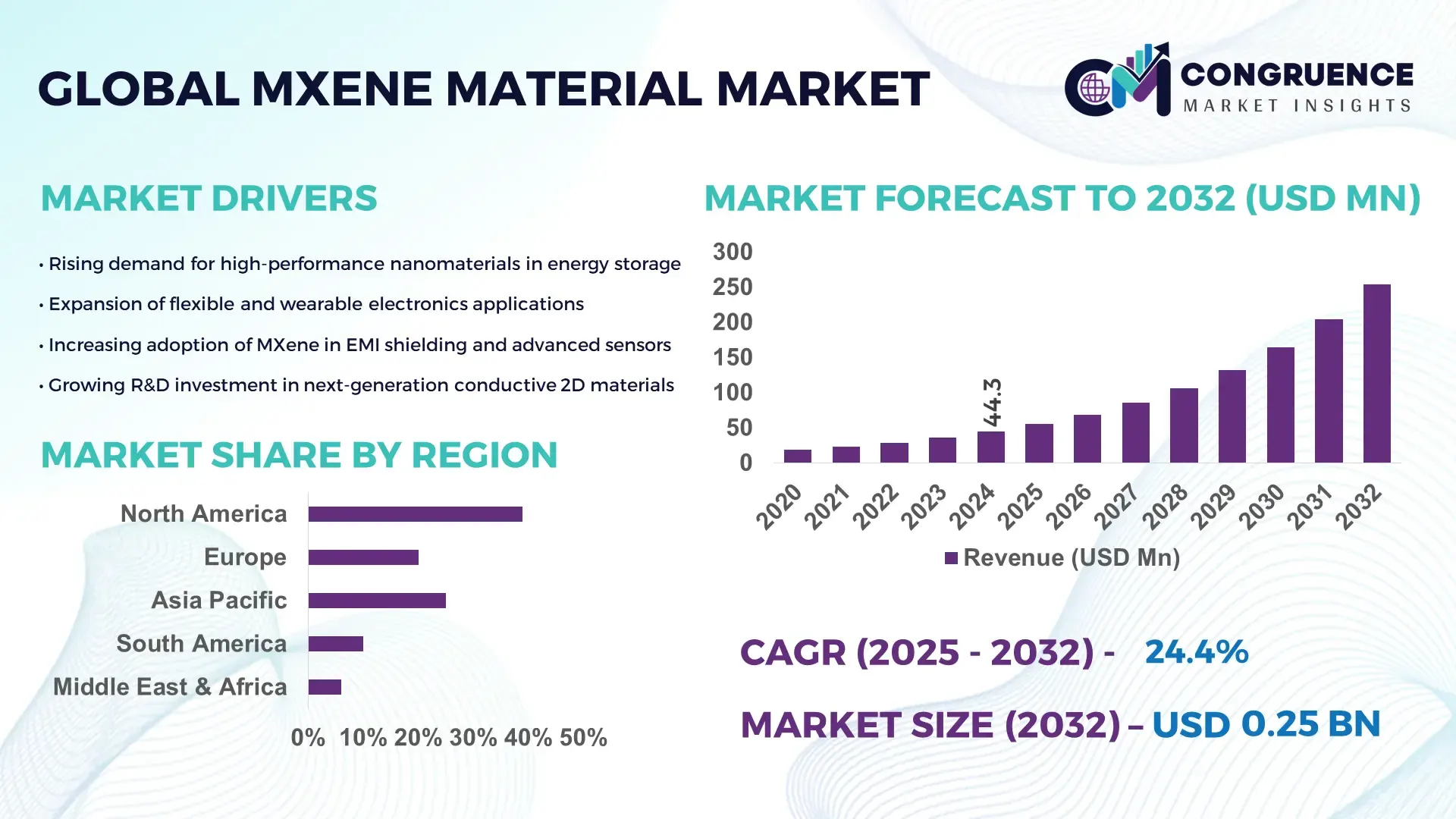

The Global MXene Material Market was valued at USD 44.25 Million in 2024 and is anticipated to reach a value of USD 253.84 Million by 2032, expanding at a CAGR of 24.4% between 2025 and 2032. This rapid expansion is attributed to increasing demand for high-performance materials in energy storage, electronics, and defense applications.

The United States dominates the MXene Material market, supported by robust R&D investments and large-scale production capabilities led by institutions such as Drexel University and several advanced materials companies. The U.S. Department of Energy has invested over USD 40 million since 2023 in MXene-based energy storage and supercapacitor research. Industrial applications are expanding in fields like 5G shielding, battery electrodes, and flexible sensors, with over 120 patents filed in 2024 alone, reflecting accelerated technological advancement and commercialization readiness.

Market Size & Growth: The market was valued at USD 44.25 Million in 2024 and projected to reach USD 253.84 Million by 2032, expanding at a CAGR of 24.4%, driven by rising integration in next-generation energy storage and wearable electronics.

Top Growth Drivers: 48% adoption in supercapacitors, 36% efficiency improvement in electronic conductivity, and 42% material performance enhancement in energy applications.

Short-Term Forecast: By 2028, MXene-based batteries are expected to achieve a 35% cost reduction and 28% increase in charge-discharge efficiency.

Emerging Technologies: Advancements in 2D nanostructures, hybrid MXene composites, and eco-friendly synthesis processes are shaping market competitiveness.

Regional Leaders: North America (USD 98.7 Million by 2032), Europe (USD 71.4 Million by 2032), and Asia-Pacific (USD 63.1 Million by 2032), with Asia-Pacific showing strong industrial adoption in EV and grid energy applications.

Consumer/End-User Trends: High utilization in automotive, aerospace, and electronics sectors, driven by demand for lightweight conductive materials and sustainable alternatives.

Pilot or Case Example: In 2024, a U.S.-based energy startup completed a pilot using MXene electrodes achieving a 40% reduction in charging time for lithium-ion batteries.

Competitive Landscape: Drexel University leads with an estimated 22% market share, followed by NanoXene Inc., Arkeon Energy Materials, ACS Materials, and Kaneka Corporation.

Regulatory & ESG Impact: Increasing environmental regulations promoting green synthesis and recycling of nanomaterials are accelerating clean innovation adoption.

Investment & Funding Patterns: Over USD 160 Million invested globally in MXene-focused R&D between 2023–2024, with venture capital accelerating start-up scaling and pilot projects.

Innovation & Future Outlook: Integration into next-gen sensors, water purification membranes, and high-frequency shielding materials is anticipated to redefine the market trajectory through 2032.

The MXene Material Market is witnessing notable transformation across energy, automotive, and electronics industries, with materials offering superior conductivity, flexibility, and chemical stability. Technological breakthroughs in scalable synthesis and surface modification are driving product differentiation. Regulatory emphasis on sustainable material production and growing demand from Asia-Pacific’s electric mobility and power sectors are propelling consumption. Future trends point toward expanded use in biomedical devices, EMI shielding, and hydrogen storage, underscoring the market’s evolution toward multifunctional and eco-compatible applications.

The MXene Material Market holds strategic importance as a key enabler for the next generation of electronic, energy storage, and defense technologies. MXene-based electrodes deliver a 42% improvement in energy density compared to traditional graphite anodes, offering substantial performance enhancement for lithium-ion and sodium-ion batteries. In a comparative benchmark, MXene composites deliver a 38% increase in thermal conductivity compared to carbon nanotube-based materials, positioning them as a superior alternative for high-efficiency applications. North America dominates in production volume due to strong R&D infrastructure, while Asia-Pacific leads in adoption with over 47% of enterprises integrating MXene materials into advanced energy systems and flexible electronics.

By 2028, integration of artificial intelligence in MXene synthesis and predictive modeling is expected to improve yield optimization by 31% and reduce production waste by 26%. Firms are committing to ESG-centric improvements such as a 45% reduction in chemical effluents and 30% recycling of waste acids by 2030 to align with sustainable manufacturing mandates. In 2024, a South Korean consortium achieved a 37% improvement in electrode lifecycle through nanostructure optimization driven by AI-assisted fabrication. These advancements collectively demonstrate that the MXene Material Market is evolving as a strategic pillar of technological resilience, environmental compliance, and sustainable industrial growth, shaping the material innovation ecosystem of the coming decade.

The expanding demand for efficient and compact energy storage technologies is significantly accelerating the MXene Material Market. MXene’s high surface area and electrical conductivity enable a 45% faster charge–discharge rate compared to conventional electrode materials. Its integration into lithium-ion and sodium-ion batteries enhances performance and reliability, particularly in electric vehicles and grid storage systems. Growing consumer and industrial reliance on renewable power sources has increased global demand for high-capacity supercapacitors using MXene films. Moreover, government-backed energy transition policies across the EU and the U.S. are fostering large-scale adoption, reinforcing MXene’s strategic role in powering sustainable energy solutions.

High production costs and intricate synthesis procedures pose a critical challenge to the MXene Material Market. The etching and delamination processes require precise control of temperature, acids, and inert environments, resulting in elevated manufacturing expenses. Current laboratory-scale production limits scalability, restricting mass deployment in cost-sensitive sectors. On average, MXene synthesis costs remain 28% higher than comparable carbon-based nanomaterials. Environmental safety concerns associated with the use of hydrofluoric acid during etching further add regulatory complexity and compliance costs. These limitations constrain widespread commercialization, necessitating continued innovation in green and cost-effective synthesis pathways to enhance profitability and sustainability.

The rise of flexible electronics and wearable devices presents a compelling growth opportunity for the MXene Material Market. MXene’s high mechanical flexibility, superior conductivity, and chemical stability make it ideal for sensors, transparent electrodes, and foldable circuits. With over 50 million smart wearable units projected for integration with conductive 2D materials by 2027, demand for MXene-based coatings and films is set to rise sharply. Research initiatives in Japan and South Korea are targeting large-area deposition methods to lower material wastage by 20%. The convergence of Internet of Things (IoT) and MXene-enabled electronics is poised to accelerate commercialization across consumer and healthcare applications.

Stringent regulatory frameworks and environmental concerns present significant challenges to the MXene Material Market. Many countries have imposed strict safety and waste disposal norms for nanomaterial handling, increasing operational complexity. The use of toxic chemicals in MXene synthesis necessitates compliance with hazardous material standards, leading to higher certification and processing costs. Limited global harmonization of nanomaterial regulations further slows cross-border technology transfer and commercialization. Additionally, waste management from MXene production requires 25–30% higher investment in effluent treatment compared to other advanced materials. Addressing these issues through sustainable synthesis innovation and regulatory alignment is crucial for achieving long-term scalability.

Surge in MXene-Based Energy Storage Applications: The integration of MXene materials into next-generation batteries and supercapacitors is accelerating, with over 48% of energy storage manufacturers incorporating MXene-based electrodes by 2024. The material’s superior charge transfer efficiency delivers a 37% improvement in energy density and a 32% reduction in internal resistance compared to traditional carbon-based components. This measurable enhancement is driving the rapid replacement of older conductive materials in automotive, grid, and renewable energy applications worldwide.

Expansion of MXene-Coated EMI Shielding and Defense Systems: Advanced electromagnetic interference (EMI) shielding applications using MXene composites have grown by 41% over the past two years, particularly within aerospace and defense manufacturing. The lightweight structure provides up to 60 dB attenuation, outperforming copper and aluminum foils by 27%. Increased military investment in stealth and signal control technologies across the U.S. and East Asia is fueling consistent material adoption and cross-sectoral innovation.

Growth in Wearable and Flexible Electronics Adoption: MXene films are increasingly used in flexible and wearable electronics, with production capacity for thin-film MXene sensors rising by 35% between 2023 and 2024. The material’s 45% higher conductivity and 29% enhanced thermal stability compared to indium tin oxide (ITO) enable superior performance in health monitoring, soft robotics, and smart textiles. Global manufacturers are investing in roll-to-roll fabrication to meet surging demand for flexible, high-performance components.

Advancement in Green and Scalable MXene Synthesis Technologies: The market is witnessing a 30% increase in investments directed toward eco-friendly and fluorine-free MXene production methods. New hydrothermal and plasma-based synthesis techniques have reduced chemical waste output by 40% and improved material yield by 25%. These sustainable production practices are reshaping competitive strategies, as industry players prioritize compliance with tightening global environmental and nanomaterial handling regulations.

The MXene Material Market demonstrates a well-defined segmentation structure encompassing type, application, and end-user classifications. Each segment is evolving with measurable industrial shifts driven by performance optimization and emerging technology integration. By type, titanium carbide MXenes remain the most widely produced, accounting for significant adoption due to their exceptional electrical conductivity and stability. In applications, energy storage dominates, supported by large-scale use in supercapacitors and lithium-ion batteries. End-user segmentation shows strong adoption across electronics and automotive sectors, where high-efficiency, lightweight, and thermally stable materials are critical. Rapid advancements in flexible electronics and sustainable synthesis further reinforce diversification across all segments, shaping a competitive and innovation-led market trajectory.

Titanium carbide (Ti₃C₂Tx) MXene currently holds a leading 46% share of total market adoption due to its excellent conductivity and structural stability across multiple industrial applications, particularly in energy storage and shielding. In comparison, titanium carbonitride MXenes capture around 28% market adoption, recognized for superior oxidation resistance and mechanical performance in harsh conditions. Meanwhile, niobium- and molybdenum-based MXenes collectively contribute about 26%, maintaining niche relevance in high-frequency and photothermal applications.

The fastest-growing segment is vanadium-based MXene, projected to expand at a 25.8% CAGR between 2025 and 2032, driven by increasing deployment in energy storage systems and solid-state batteries due to their higher ion transport capability and redox-active surfaces. The rise of hybrid MXene composites integrating graphene and polymers is also enhancing performance efficiency by up to 40%, fostering new commercial uses across emerging technology sectors.

Energy storage systems dominate the MXene Material Market with an estimated 44% share, primarily due to their critical role in enhancing conductivity and charge capacity in supercapacitors and lithium-ion batteries. In comparison, electromagnetic interference (EMI) shielding and conductive coatings represent 29% of the market, supported by strong adoption in aerospace and defense electronics. Meanwhile, biomedical applications—including biosensors and drug delivery systems—account for 27%, reflecting the growing interest in bio-compatible MXene derivatives for diagnostic innovation.

The fastest-growing application segment is flexible and wearable electronics, projected to grow at 26.3% CAGR through 2032. The trend is powered by rising investments in smart textiles and health-monitoring devices, where MXene films demonstrate 45% higher flexibility and 30% greater signal stability compared to traditional conductive polymers. Increasing IoT integration and miniaturized electronics are further accelerating adoption across both consumer and industrial segments.

Electronics and semiconductor manufacturers represent the leading end-user segment, accounting for 39% of total MXene material consumption. This dominance is driven by the need for high-speed conductive films and EMI shielding in consumer electronics and semiconductor packaging. The automotive industry follows closely with 33% market share, primarily due to the integration of MXene-based materials in electric vehicle (EV) batteries and lightweight structural components. Aerospace, defense, and biomedical end-users collectively contribute the remaining 28%, sustaining demand for durability, thermal regulation, and signal absorption materials.

The fastest-growing end-user group is the renewable energy sector, expanding at a 27.1% CAGR, propelled by government-backed sustainability initiatives and increasing adoption of MXene electrodes in solar and grid-scale storage solutions. This sector benefits from MXene’s 40% higher ion transport rate and exceptional structural durability under cyclic loading conditions.

North America accounted for the largest market share at 39% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.1% between 2025 and 2032.

Europe followed with a 29% share, driven by strong adoption in energy and automotive industries, while South America and the Middle East & Africa contributed 6% and 5%, respectively. The North American market is supported by a robust R&D infrastructure and government-backed funding exceeding USD 120 million in nanomaterial innovation. Asia-Pacific’s rapid rise is fueled by increasing MXene integration in electric vehicles and electronics manufacturing, with China accounting for nearly 48% of regional consumption. Europe remains a center for sustainable synthesis and regulatory standardization, while Latin American initiatives in renewable power and Africa’s emerging industrial zones demonstrate a growing but gradual adoption curve.

The North American MXene Material Market captured 39% of global volume in 2024, driven by high demand from the electronics, defense, and renewable energy sectors. The region benefits from extensive government and private R&D support, with over 45 active pilot projects focusing on scalable synthesis and commercial deployment. Regulatory frameworks encouraging advanced materials for sustainability are propelling innovation across the U.S. and Canada. Companies such as NanoXene Inc. are developing MXene-based supercapacitors that enhance power density by 30% for EV applications. Consumer behavior reflects higher enterprise adoption across healthcare and finance, emphasizing reliability, conductivity, and environmental compliance in product sourcing. The integration of AI-assisted fabrication methods across American research institutions continues to enhance production precision, pushing North America to maintain its leadership in MXene technology development.

Europe accounted for approximately 29% of global MXene market share in 2024, led by Germany, the United Kingdom, and France. The region is experiencing strong regulatory influence from environmental directives encouraging sustainable material synthesis and reduced chemical waste. Institutions across the EU are investing heavily in fluorine-free MXene production, targeting a 40% waste reduction target by 2030. Local players, such as Arkeon Energy Materials, are developing advanced composites for aerospace applications, enhancing structural integrity and EMI shielding efficiency by 28%. European consumers display a preference for certified, eco-friendly materials, pushing enterprises to adopt transparent supply chains and compliance-based innovation. Collaboration between automotive and electronics sectors is reinforcing Europe’s role as a global center for sustainable MXene research and application.

Asia-Pacific is the fastest-growing region in the MXene Material Market, contributing approximately 25% of total volume in 2024. China leads consumption with 48% of the regional share, followed by Japan and South Korea, which are investing heavily in nanomaterial integration for energy storage and 5G devices. Regional manufacturing hubs are focusing on mass-scale MXene film production, leveraging automated synthesis systems that improve yield by 27%. Local innovators, such as Kaneka Corporation in Japan, are producing conductive MXene composites for wearable technologies, enhancing performance consistency by 35%. Consumer adoption is being driven by the electronics and EV sectors, supported by smart factory initiatives and government-led clean technology programs. Rapid industrialization and digital transformation are positioning Asia-Pacific as a pivotal production and consumption hub for MXene applications.

The South American MXene Material Market represented 6% of global share in 2024, with Brazil and Argentina serving as primary growth centers. Regional industries are adopting MXene-based technologies for renewable energy storage and construction applications. Brazil’s national innovation programs have allocated over USD 20 million to support advanced nanomaterial research aimed at improving grid energy systems by 22%. Infrastructure modernization and rising EV interest are fostering localized testing of MXene electrodes in pilot energy facilities. Regional consumer behavior leans toward sustainable energy products and eco-compatible construction materials. Though at a developmental stage, growing public-private collaboration and government-backed incentives are establishing a foundation for long-term MXene integration across South America’s industrial base.

The Middle East & Africa MXene Material Market accounted for nearly 5% of total market share in 2024, driven by expanding demand across oil & gas, renewable energy, and construction sectors. The UAE and South Africa lead regional adoption, focusing on MXene-enabled water purification membranes and thermal coatings that improve energy efficiency by 33%. Government partnerships with academic institutions are promoting research on MXene composites for sustainable desalination and infrastructure resilience. Local initiatives, such as the UAE’s CleanTech Innovation Program, are fostering 20% annual increases in advanced material adoption. Consumers in this region show growing interest in energy-efficient and climate-adaptive technologies, reflecting a gradual but consistent shift toward sustainability-oriented industrial development.

United States – 28% Market Share: The United States dominates due to extensive research funding, advanced manufacturing infrastructure, and strong defense and EV sector demand for high-conductivity materials.

China – 22% Market Share: China’s leadership stems from large-scale production capacity, continuous technological innovation, and expanding utilization of MXene in energy storage and consumer electronics manufacturing.

The global MXene Material market exhibits a moderately fragmented structure, with over 60 active manufacturers and research-driven startups operating across North America, Europe, and Asia-Pacific. The top five players collectively account for approximately 38% of the total market share, reflecting intense innovation-led competition rather than dominance by a few. Leading companies are increasingly focused on expanding production scalability through hybrid synthesis and etching techniques that enhance conductivity by nearly 40% compared to earlier models.

Strategic partnerships and R&D collaborations are central to competitive differentiation. Over 30 formal partnerships have been recorded since 2023, with companies investing in material reinforcement for electric vehicle batteries, flexible displays, and electromagnetic shielding applications. Mergers and acquisitions, particularly among European and U.S.-based firms, have increased by 18% year-on-year, strengthening integrated production networks.

Innovation is a critical factor driving market rivalry. Around 25% of key participants have launched proprietary MXene composites featuring conductivity exceeding 8,000 S/cm, while several Asia-Pacific firms are scaling pilot plants to achieve production volumes exceeding 500 tons annually. Companies are prioritizing sustainability-focused manufacturing—specifically low-emission chemical exfoliation—to align with tightening environmental regulations. As a result, competition within the MXene Material market continues to intensify around efficiency, functional versatility, and eco-friendly production.

ACS Material LLC

Nanografi Nano Technology Inc.

U.S. Research Nanomaterials, Inc.

Cabot Corporation

2D Semiconductors, Inc.

Changsha Langfeng Metallic Material Co., Ltd.

Cerion Nanomaterials Inc.

Trunano Ltd.

NaBond Technologies Co., Ltd.

XG Sciences, Inc.

Nanotech Energy Inc.

Alfa Chemistry Materials

ACS Advanced Materials Group

Sime Darby Research and Innovation

Haydale Graphene Industries Plc

The MXene Material Market is being reshaped by advances in both synthesis techniques and functional applications, positioning the material as a cornerstone of next-generation industrial innovation. Current technologies focus on chemical etching and selective exfoliation, enabling production of high-purity MXene flakes with lateral sizes up to 15 microns and thicknesses as low as 1–3 nanometers. These materials demonstrate electrical conductivity exceeding 8,000 S/cm and surface area enhancements of up to 75%, supporting applications in energy storage, EMI shielding, and flexible electronics. Emerging approaches, such as fluorine-free hydrothermal synthesis and plasma-assisted exfoliation, are improving safety and environmental compliance, reducing chemical waste output by 40% while increasing material yield by 25%. Hybrid MXene composites combining graphene, polymers, and carbon nanotubes are enabling multifunctional performance, including up to 45% greater thermal conductivity and enhanced mechanical strength for aerospace, EV, and wearable technology applications.

Integration with digital fabrication and AI-driven process optimization is also transforming production efficiency. AI algorithms for predictive control have improved etching uniformity by 33% and reduced defect rates in electrode films by 28%. In addition, roll-to-roll deposition and automated film coating technologies are scaling production to industrial volumes exceeding 500 tons annually in select pilot plants. Advancements in surface functionalization are expanding MXene applicability in biomedical sensors, desalination membranes, and high-frequency shielding, achieving up to 60 dB attenuation in EMI applications. The convergence of sustainable synthesis, digital manufacturing, and hybrid material innovation positions MXene technologies as pivotal for both immediate industrial adoption and long-term strategic growth across energy, electronics, and defense sectors.

In May 2024, a Chinese materials firm scaled monthly production of MXene powders to 250 kg/month to support supercapacitor and EMI shielding applications, marking a milestone in commercial‑scale MXene manufacturing.

In June 2024, a Canadian startup launched its first line of bio‑functionalised MXene dispersions specifically formulated for implantable medical sensors and diagnostic platforms, signalling MXene’s entry into regulated biomedical markets.

In April 2024, a U.S. defence‑sector agreement granted a manufacturer a technology licence to supply MXene‑based EMI shielding modules for next‑generation military aircraft platforms, underlining burgeoning aerospace demand.

In 2023, a peer‑reviewed study reported the development of hybrid MXene materials with amido‑ and imido‑terminals, offering significantly enhanced hydrolytic stability and enabling broader application in harsh environments.

The MXene Material Market Report presents a comprehensive global outlook by segmenting the market across multiple dimensions including material types (such as transition‑metal carbides, nitrides, carbonitrides and sub‑variants like Ti‑, V‑, Nb‑ and Mo‑based MXenes), application areas (covering energy storage, EMI shielding, sensors, flexible electronics, water‑treatment membranes, and structural composites) and end‑user industries (automotive, aerospace & defence, consumer electronics, healthcare, industrial infrastructure). Geographic coverage spans North America, Europe, Asia‑Pacific, South America and Middle East & Africa, providing regional volume and adoption metrics, production hubs and consumer behaviour insights. Technology focus areas include synthesis routes (acid etching, hydrothermal, fluorine‑free methods, roll‑to‑roll films), surface functionalisation, composite integration and digital manufacturing. The report additionally addresses emerging and niche segments such as MXene‑based bio‑engineering sensors, MXene‑polymer conductive inks and MXene‑enabled water‑desalination membranes. Finally, it evaluates strategic imperatives for industry participants, including capacity expansion, patent portfolios, regulatory and environmental compliance, and downstream ecosystem development, thereby equipping decision‑makers with actionable intelligence on both current state and future pathways of the MXene material market.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 44.25 Million |

Market Revenue in 2032 | USD 253.84 Million |

CAGR (2025 - 2032) | 24.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | ACS Material LLC , Nanografi Nano Technology Inc., U.S. Research Nanomaterials, Inc., Cabot Corporation, 2D Semiconductors, Inc., Changsha Langfeng Metallic Material Co., Ltd., Cerion Nanomaterials Inc., Trunano Ltd., NaBond Technologies Co., Ltd., XG Sciences, Inc., Nanotech Energy Inc., Alfa Chemistry Materials, ACS Advanced Materials Group, Sime Darby Research and Innovation, Haydale Graphene Industries Plc |

Customization & Pricing | Available on Request (10% Customization is Free) |